The emergence of community group buying brought everything back to the original point, and now the giants are standing on the same starting line again.

Editor’s note: This article is from the WeChat official account “Alpha Workshop Research Institute” (ID: alpworks), of: bovine Chu Yun.

In 2020, there will be a peculiar situation in the Internet industry, and various giants have deployed fresh food group buying business.

Ali (BABA.US, 09988.HK) “Hema + Eleme + Retail Pass + Shihui Group” iron army before, and Tencent (00700.HK) Prosperity Optimal to overtake on corners, Meituan (03690.HK) established the “Optimization” division in June this year and put forward the “Thousand Cities Project.”

And as you know, on the road to grocery shopping, the most grassroots Pinduoduo (PDD.US) “will only be late and will not be absent”: “Buy Duoduo” was launched in August this year and was Regarded as the most important business, Huang Zheng hailed it as the “touchstone”. “Outsiders” Didi, byte, Kaishou is also keeping up with the pace. Didi launches “Orange Heart Optimal” Byte is brewing to launch “Today’s Grocery”, and Kuaishou has gone deep into Changsha to conduct research. Although they are all building high-rise buildings on the ground, the emergence of these three adds to the firewood of community group buying.

The giants have a basket of food in their hands. From a distance, it is an Internet conference, but from a closer look it is like a new development. Why does the Internet industry suddenly worry about the people’s grocery shopping? Where does this strange look and feel come from?

01 giant traffic abacus

The most “precious” thing in the Internet industry is not quantum computers, not source code, not 996, but traffic.

As early as 2016, JD.com adjusted its strategy due to traffic bottlenecks. In the first quarter earnings conference call that year, JD’s CFO Huang Xuande said bluntly: “For the entire vertical category, the traffic conversion brought by Tencent has dropped significantly.”

This sentence is a bit convoluted, but the meaning is very clear: Jingdong spends a lot of money to buy traffic from Tencent, but it still needs additional subsidies for conversion. In desperation, Jingdong came up with the “Jing X Project” to cooperate with large traffic users. Later launched Kepler platform, output customizable e-commerce solutions, and find ways to solve external traffic Single question.

Time flies, and there are more and more Internet giants bound by traffic.

As of June 30, 2020, the number of trading users on the Meituan platform reached 460 million, and the number of active merchants reached 6.3 million. Both indicators have achieved growth regardless of the quarter-on-quarter or year-on-year basis. However, the average transaction user The number of annual transactions has dropped to 25.7.

Meituan is not the only one suffering from the dilemma of “only shopping, not buying”. The big brother Ali, who has been overlooking the Internet, is also embarrassed on all sides. Not only are newcomers catching up behind him, but he also finds that it is increasingly difficult to achieve the Great Leap Forward growth rate.

As of the end of September 2020, Ali’s annual active buyers reached 757 million, which is the same as Pinduoduo’s 7.313Compared with 100 million yuan, only one permanent resident population in downtown Beijing was lost. What is even more frightening is that throughout the third quarter, Ali’s annual active users only increased by 15 million month-on-month; it was far lower than Pinduoduo’s 48.1 million.

The slowdown in the growth rate will add another salt to Ali’s wounds. In the third quarter of 2020, Ali failed to break the barrier of “900 million monthly active mobile users and 800 million annual active buyers”; Not only that, Ali’s mobile monthly active users only increased by 7 million in the third quarter, which is far from the previous quarterly growth of tens of millions.

The weak growth has already begun. At the end of 2019, Ali’s customer acquisition cost exceeded 800 yuan per person for the first time, and continued to rise since then, reaching 1,158 yuan in the third quarter of this year. More and more money is spent, and fewer people come. If this continues, I am afraid that the registration and bonus share model will be opened in the future.

For Pinduoduo, it is really rare to be able to approach Ali at a time when traffic is increasingly scarce. But worrying about the elderly does not mean that newcomers need not worry: in the third quarter, Pinduoduo increased by 73.48% year-on-year to 1,457.6 billion yuan, which was a lot slower than the 143.68% in the same period last year.

This shows that user growth is no longer the core driving force for GMV growth; in addition, since the second quarter of 2019, Pinduoduo’s annual consumption growth rate has also declined, and has basically stagnated in the last two quarters. . For Pinduoduo, the era of “relying on subsidies for growth” is coming to an end.

According to the conservative algorithm of the Ministry of Industry and Information Technology, China’s Internet population in a broad sense is almost close to its peak, and the overall market traffic has peaked, making new additions more difficult than climbing.

History tells us that there are no more than two solutions: you can either break through the East-style “open wasteland”, or engage in land mergers and reach into someone else’s bowl. In the past few years, the drama of “traffic grabbing” between platforms has never been closed. The famous scenes of “choose one from two” are not uncommon, which is nothing more than a true portrayal of “the introduction of fertilizer from one’s own farm”.

The essence of traffic is to seize user time, and it is the first element of monetization. But in the business of e-commerce, user stickiness (loyalty) is sometimes illusory.

Most people’s consumption decisions are determined by large subsidies, low prices, good services, and fast logistics. This principle has been fully verified by Pinduoduo and JD.com-Pinduoduo relies on low prices and JD relies on logistics.

Nowadays, mobile Internet dividends are fading, traffic is scarce, customer acquisition costs are rising, and the increase in traffic is like “new hair growing on the head of middle-aged people.” In such a dilemma, only by breaking through imagination, packaging new concepts, and creating new stories, Internet giants can get out of the predicament.

Looking back on the past few years, countless outlets have emerged, countless new tracks have been developed, requirements have been verified, models have been overturned, and countless stories have gone with the wind.

From e-commerce, mutual funds, to medical treatment, and short video, as long as there is imagination, there is the Internet. Among them, there are many old stories that have been told. The community groupsPurchase is one of them.

Although it is not a new concept, it will return to the center of the stage in 2020, igniting the enthusiasm of the entire market and driving the gods crazy.

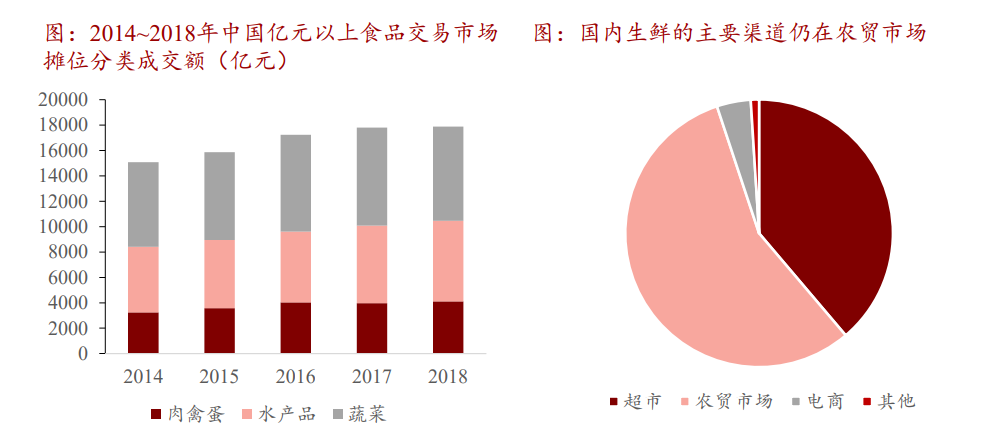

The giants’ entry into the track of community group buying is regarded as a “pioneering move” to gain sinking market traffic. The core of community group buying is fresh food, which is not only just demand but also a pain point. It projects a market of up to trillions of dollars behind it. These two points alone are enough to support the giants to go all out.

The picture is from China Merchants Securities

But a practical question is: How high is the threshold for community group buying? Can the model work? From strategy to play, are the giants ready? To answer the above questions, you need to understand a sample first.

02 Modes that are difficult to copy

In the development of community group buying, an important sample cannot be skipped, it is the best choice for prosperity.

In 2014, Yue Lihua from Yiyang, Hunan ran a local chain Shopping Department, since then, he The commissary began to take on the service of helping people buy and sell vegetables. With 30 years of “retail” experience, he smelled a business opportunity and established Prosperity Optimal.

Although the birth of Prosperity Optimal is based on consumer demand, the difficulty lies in how to effectively transform it into a business model. In this process, Yue Lihua bumped into walls and encountered several major problems in customer acquisition, cost, inventory, and distribution.

In the early days, Xingsheng preferred to be delivered by the boss himself; after that, the front warehouse and distribution team were set up; the warehouse was transformed into a small warehouse and a distribution station. Until 2016, Yue Lihua decided to incorporate the previous model into the e-commerce system, through the door The shop owner publishes a message in the WeChat group, so that nearby residents can place orders in the group, and finally pick up.

When selecting suppliers, Prosperity Optimal will select the “elimination mechanism”. Those vendors with good service will eventually stay. In this way, Xingsheng prefers to use “community pre-sale + store self-pickup” to get out of Yiyang, Hunan and spread to the whole country.

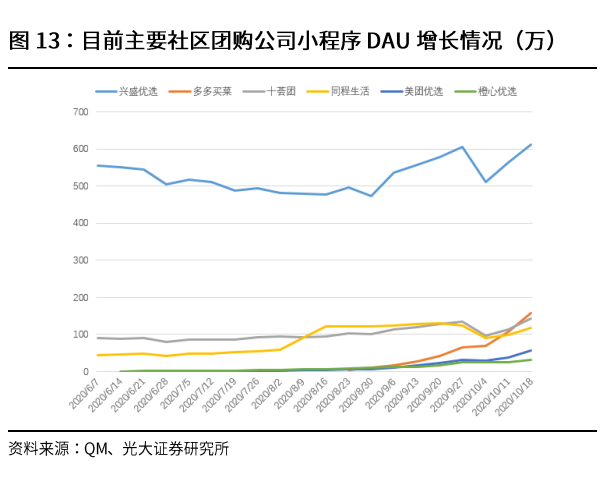

After several years of verification, community group buying represented by Prosperity Optimal has gradually become a force. From 2017 to 2019, its GMV jumped from 36 million yuan to 10 billion yuan; in September 2020, the daily order volume of Xingsheng Optimum reached 8 million, nearly doubled from the same period in 2019, and the number of customer orders increased from 10 billion. The yuan rose to 15-20 yuan.

Picture from Everbright Securities

In essence, community group buying is a consumption behavior based on the community. The person who connects the store and the consumer is called the “group leader.”

In the early development, the role of the head of the group was generally assumed by the mother and housewife. Because these people have a lot of time and energy, and have the innate conditions to operate the community. Coupled with the ability to earn commissions and high flexibility, many people join the community group buying business.

For Xingsheng Optimal, its rise is inseparable from the user habits and social preferences of the locals.

Compared with first- and second-tier cities, where work pressure is high and life is fast, the pace of lower-tier cities is much slower, there is plenty of time to spend, and the frequency of social interaction is higher. Buying food and cooking is not only for food and clothing, but also a kind of community The embodiment of demand.

From another perspective, whether it is community interaction or neighborhood relations, first- and second-tier cities are far inferior to lower-tier cities. Coupled with the difference in consumption level and consumption ability, lower-tier cities have a stronger demand for low-cost fresh food. This is also the ability of “group buying” and “group buying”.