“Think of all that investors fear.”

Editor’s note: This article is from the micro-channel public number “bullet Finance” (ID: wwwhygc), Author: Walker, Editor: total egg.

WeDoctor, known as “China’s Internet Medical Leader”, officially submitted a listing application to the Hong Kong Stock Exchange on April Fool’s Day in 2021.

This means that in addition to Alibaba Health, JD Health, and Ping An Good Doctor, the Hong Kong Stock Exchange has finally gathered the “four kings” of China’s Internet healthcare.

Originally, this was a great encouragement to Chinese Internet entrepreneurs. However, after the announcement of WeDoctor’s IPO prospectus, it was like a pot of cold water that extinguished the public’s enthusiasm for this company.

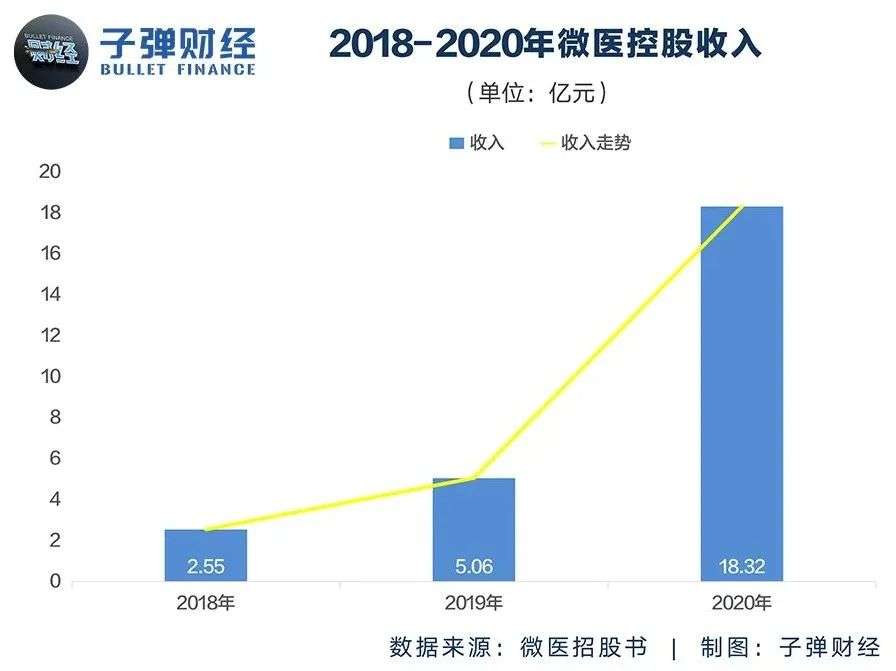

The prospectus shows that as of December 31, 2020, WeDoctor Holdings has connected more than 7,800 hospitals in China, 270,000 registered doctors, approximately 222 million registered users, and operated 27 Internet hospitals. From 2018 to 2020, the revenue of WeDoctor Holdings will be 255 million, 506 million and 1.832 billion, respectively, with a compound annual growth rate of 168%. In particular, revenue in 2020 will increase by 262% year-on-year compared to 2019.

Compared with the data of the other three, WeDoctor is slightly behind, but it seems that the overall strength is on par with its opponents.

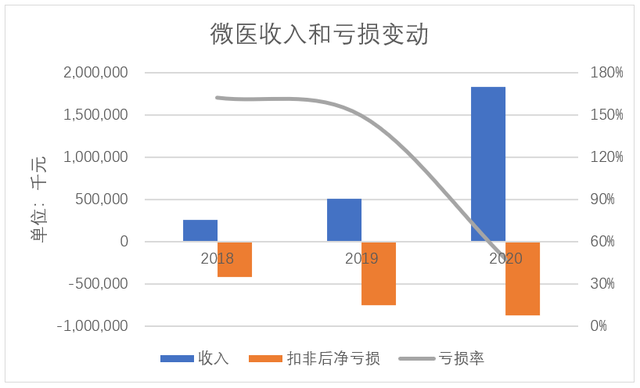

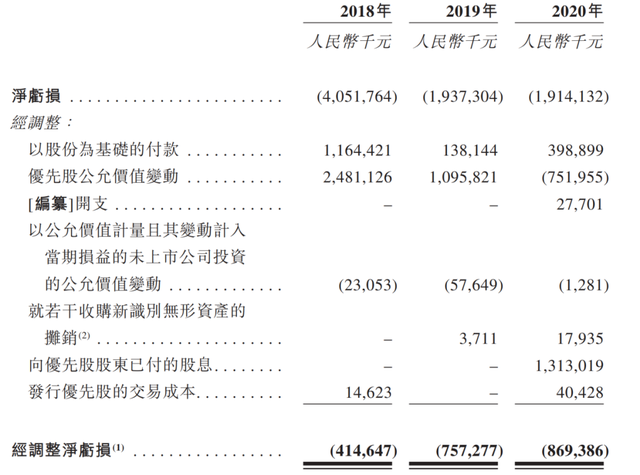

However, in terms of profit, it is a bit jaw-dropping. Data show that WeDoctor’s net losses from 2018 to 2020 are 4.05 billion yuan, 1.94 billion yuan and 1.91 billion yuan, respectively, with a total loss of 7.9 billion yuan in three years. Excluding the influence of factors such as changes in the fair value of convertible preferred shares and share-based compensation expenses, the adjusted losses of WeDoctor in the past three years were 410 million, 760 million, and 870 million, respectively, with a total of 2.04 billion yuan.

The key point is that after three years of adjustments, WeDoctor’s losses, that is, the loss value caused by the business, are increasing with the growth of income. This means that WeDoctor is still in the stage of strategic losses, and the loss amount is relatively large. high.

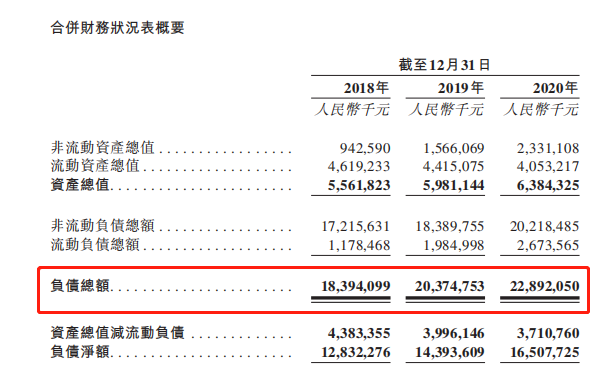

In addition, in addition to continuous accumulated losses, WeDoctor’s debt and cash flow situation is not ideal. Data show that from 2018 to 2020, WeDoctor’s total liabilities are 18.394 billion yuan, 20.375 billion yuan and 22.892 billion yuan respectively. From the data, it can be seen that the total debt of WeDoctor is increasing year by year, and the growth is increasing year by year. In 2019, it increased by 1.98 billion yuan compared with 2018, and in 2020 it increased by 2.517 billion yuan compared with 2019.

In contrast, the total revenue of 2.593 billion yuan in the three years from 2018 to 2020 appears to be “a drop in the bucket” in front of the total debt value.

“Under normal circumstances, when such an Internet company is listed, we will not participate at all.” Zhang Ran, a well-known investment bank analyst in Hong Kong, told Bullet Finance and Economics that he thinks such Internet companies may have ” “Using capital to push up sales revenue in order to obtain a higher valuation in the capital market” means.

“If such a company succeeds in going public, it will be a disaster for many rigorous investment bank analysts. To be honest, it is the consensus of all our analysts that they are not optimistic about this company.” Zhang Ran said, In his view, WeDoctor is an example of “listing on the market with illness.” According to “Bullet Finance”, the reasons why analysts are not optimistic about this company are concentrated on WeDoctor’s debt of more than 20 billion and revenue of less than 3 billion.

The problem is that behind such financial data, there is actually a “four dissimilarity” model where it is difficult to make money after a savagely growing industry is standardized.

1. A model that is difficult to make money

Although it is also known as the “Four Kings” with the three listed Internet medical companies, WeDoctor has taken a completely different route from the other three.

Actually, WeDoctor does not make a living by selling drugs, but on chronic disease management and medical services. Unexpectedly, the Internet drug sales business of the other three listed companies is also difficult to make money. Therefore, these companies have begun to expand their business, in addition to selling drugs, they also carry out medical examinations, medical aesthetics, oral and genetic testing and other projects.

This means that WeDoctor almost exclusively owns a track for medical Internet services, and the prospects look smooth.

However, the market value of Ali Health and JD Health are both at 300 billion Hong Kong dollars, and the highest point of JD Health even exceeded 400 billion Hong Kong dollars. However, the market value disclosed in the WeDoctor IPO prospectus is only 15 billion U.S. dollars (about 116.6 billion Hong Kong dollars).

This can also be understood in the capital market, because the Internet medical track where these 4 companies are located has had a period of “barbaric growth”, but in recent years, the country has increasingly strengthened supervision in this field. Feedback to the business level of listed companies will inevitably have to be adjusted.

“In the past few years, the state encouraged the development of Internet medical services. Later, it may have developed too fast and some problems have appeared, such as prescribing drugs without review. Therefore, the policy has been tightened. Especially during the epidemic, the policy has also been tightened. Encourage the development of Internet medical care, because it really protects peopleHealth has played an important role, but it is obvious that supervision is still very cautious. Therefore, even if some documents have now been issued to encourage the development of Internet medical care, no one dare to move too much. “Li Yi (pseudonym), who once worked for the Beijing Municipal Health Commission, told Bullet Finance.

He believes that there is nothing wrong with the cautious attitude of supervision. After all, there are many stakeholders in the medical industry chain, which affect the whole body. Every slight change may cause industry shocks. Moreover, how to ensure the compliance and legality of services such as Internet consultations and prescriptions, we have not yet explored a suitable plan.

The general view is that the cash flow of Internet drug sales business is the most normal. This business model has also attracted more and more attention, but WeDoctor did not choose this track as its main business. In the 706-page prospectus, “digital medical service platform” has become the most frequent keyword.

The so-called “digital medical service platform”, according to WeDoctor’s prospectus, is two aspects of business.

One is medical service. WeDoctor provides online and offline integrated consultation and diagnosis and treatment services. Specifically, it includes online appointments, offline first visits, medical record acquisition, online follow-up visits, electronic prescriptions, dispensing services, and settlement of medical expenses through public medical insurance and commercial health insurance.

The other is health maintenance services, that is, through a membership-based service model, WeDoctor provides digital chronic disease management services and health management services.

The prospectus shows that in 2020, WeDoctor’s total revenue will be 1.832 billion yuan, of which medical service revenue in 2020 will be 706 million yuan, accounting for 38.6%; health maintenance service revenue will be 1.125 billion yuan, accounting for 61.4%.

In this business story, in order to support the valuation, WeDoctor puts itself a “seemingly very reasonable” data cloak.

According to the prospectus, as of December 31, 2020, WeDoctor has 27 Internet hospitals, with 222 million registered users on the platform, and an average monthly paying user of 25.4 million, providing a total of about 40 million digital medical services. consultation service. There are more than 7,800 hospitals connected, covering more than 95% of the top three hospitals, and there are 270,000 registered doctors on the platform.

This data looks very eye-catching, and it has been explained by many media as the core basis for its listing, but the problem is that the company’s selected Internet medical services are actually not optimistic.

“Many times, noAn industry must have prospects if it does the data. Zhang Ran told “Bullet Finance” that in his years of experience, he has seen countless examples of surprise investments and marketing for the purpose of listing financial report data.

After all, Chinese public hospitals’ medical visits are of a welfare nature, and they do not have profitability. If WeDoctor move online to increase services and increase prices for profit, a large number of users will eventually be transferred back. Ask the offline hospital for help.

Of course, due to the current uneven distribution of medical resources in my country, users in the sinking market may move a larger proportion of them online in order to obtain better medical resources, but this group is more sensitive to prices.

“It’s okay to turn medical services into the Internet, but this is just a public welfare act. If you want to make money in this way, it’s tantamount to’idiotic dreams’.” Li Yi (pseudonym) said to Bullet Finance He believes that unless local health commissions purchase Internet-based services for the purpose of public medical care, they want to rely solely on commercialization to prop up an Internet-based medical giant. Under the current regulatory situation, there is no possibility of success.

Therefore, it is the specialized nursing, chronic disease management and corporate health management services that may support the future profit prospects of WeDoctor.

“These are actually the areas that the state allows Internet companies and private capital to explore. However, specialty nursing has high profits but low demand, and chronic disease management has a large demand but a long stream. Corporate health management means collective physical examination and data concentration. The management model is now facing fierce competition similar to various medical examination groups. From this perspective, WeDoctor has indeed not found a satisfactory profit model.” Li Yi (pseudonym) added.

From the past performance of WeDoctor, we can also see that its profit model is still being explored. Although the overall growth rate of income is very high, the net loss after deduction is also increasing year by year.

It is not difficult to see that even if it has not embarked on the Internet drug sales track with many rivals, WeDoctor will find another way to become a digital medical service platform, but the profit prospects of this road are not clear.

2. Behind the tens of billions of debts

Because of such a seemingly vigorous, but in fact, Internet medical business with an inconspicuous profit model as its main business, WeDoctor’s financial statements show a “weird status quo.”

On the one hand, WeDoctor’s “significant increase” in revenue in the past three years has only completed nearly 2.6 billion yuan in total; on the other hand, WeDoctor’sThe balance of liabilities in 2019 and 2020 will both exceed 20 billion yuan.

WeDoctor’s explanation is very simple, that is, companies have invested heavily in the construction of a large amount of Internet medical service infrastructure, claiming to have achieved “high-intensity development and technical barriers” in this field.

From the development of some similar platforms, it can be seen that the so-called “large investment” refers to the contracted hospital-related equipment Unicom, platform construction, technology research and development, and investment in offline smart registration equipment, and so on.

In the medical industry, it is understandable that a startup company has such a development idea, but the problem is that the medical service field is a welfare public welfare expenditure field advocated by the state, and the general medical hospitals are not profit-making.

This means that the large amount of investment that WeDoctor previously invested in contracted hospitals is actually doing Internet public welfare services, and will not increase the overall business.

Under such circumstances, WeDoctor will of course carry a heavy burden of development. In fact, it has done a lot of information equipment and research and development work that should be invested by local medical authorities in many countries.

This is also the fundamental reason why it will maintain more than 20 billion in debt.

“Based on the reality that it is more than 20 billion in debt every year, you can see that this is a company with very unhealthy cash. This kind of business behavior is unimaginable-annual revenue of less than 2 billion, three years The total income only earned nearly 10% of the debt. This figure actually means that the principal and interest expenses of the company’s annual loan repayment all come from newly borrowed debt or preferred stock issued by internal convertible bonds.” Zhang Ran analyzed “Bullet Finance”, “Thinking about it makes investors feel scared.”

In addition, with regard to WeDoctor’s claims of “significant decline”, it has been mentioned in some publicity drafts that WeDoctor’s loss rate has narrowed from 163% in 2018 to 47% in 2020. In fact, there is There is also a huge mystery hidden.

It can be seen from the IPO documents that the loss of WeDoctor in 2020 should be no different from that in 2019, which is about 1.9 billion yuan. But in the final adjustment, one of them paid a dividend of 1.313 billion yuan to preferred shareholders, which was deducted from the final statistics.

Of course, there is also a change in the fair value of preferred stocks in the loss adjustment in 2020. This is a negative value, which means that some preferred stock shareholders have been transferred to current common stocks, and there is a middleThe stock price of the preferred stock fell to the stock price of the common stock.

So, strictly speaking, the so-called adjusted net loss basically has no reference value. Moreover, behind the loss of so much in 2020, WeDoctor also paid a dividend of 1.3 billion to preferred stock shareholders. Although it was deducted from the financial statements, this should also be included in the actual capital loss in actual operations. Part of the amount.

It is worth mentioning that this part of the report reflects two interesting points.

One is that WeDoctor, with a total income of less than 1.9 billion in 2020, actually paid more than 1.3 billion preferred stock dividends. If you count the costs and expenditures that the company has listed in the list, this basically puts the company The cash flow obtained from daily operations has been exhausted; the other is that when shareholders of preferred stocks transfer to common stocks, stock prices are lost.

“From the perspective of our investment bank analysts, paying so many preferred stock dividends at one time before listing means that a large number of preferred stock shareholders are not optimistic about this company and have not converted shares. “Lin Xi, a senior investment bank analyst in Hong Kong, told Bullet Finance that this is actually a hidden danger left by WeDoctor in its previous financing.

“In WeDoctor’s previous financing operations, most of them are likely to be strategic investors. The other party chose to enter in the form of preferred stocks. In fact, on the basis of ensuring that their investment is not lost, they want to pass this The four kings of Internet medical services have a share of the company’s development.” Lin Xi further said.

In fact, before the listing, the shareholders rushed to demand dividends to protect the capital. It is that these strategic investors are not optimistic about the performance of the company’s prospects.

“More importantly, the conversion of preferred stocks into common stocks also resulted in stock price losses.” Lin Xi believes that the appearance of this value in the balance sheet generally means that the company issues convertible preferred stocks overseas before listing. For financing, these convertible preferred stocks can be converted into ordinary shares in accordance with the agreed ratio after the company’s listing is completed. The agreed price is often significantly lower than the issue price per share after the listing.

“Under normal circumstances, the larger this value is displayed when an Internet company is listed, the more it can prove that the entire capital market is optimistic about this company.” Lin Xi said that the WeDoctor prospectus disclosed US$15 billion (more than 1,100). Billion Hong Kong dollars), the fair value of the preferred shares has changed less than 800 million Hong Kong dollars. “Combined with WeDoctor’s payment of 1.3 billion preferred stock dividends at the same time, you can see that many preferred shareholders did not exercise their rights, but chose to take Money withdrawal.”

“Station B, which was just listed on the Hong Kong stock market, reported a loss of 102.4 billion due to changes in the fair value of preferred stocks, while the market value of Hong Kong stocks at station B was close to 300 billion.” Lin Xi believes that comparing the two data Later, we can see what the attitude of strategic investors is towards WeDoctor.

“Even the strategic investors who have been following are not optimistic about this company’s stockWill it be recognized by investors after listing? “

3. Where is the future?

As we all know, medical institutions and public hospitals are rare areas where competition barriers are extremely high but it is difficult to make money, and it is precisely this field that WeDoctor cuts into.

“To be honest, I personally don’t like this model.” Li Yi (pseudonym), who was once an official of the medical department, believes that the role of the medical industry includes the general public, patients, medical staff, public hospitals, and private medical institutions. , Pharmaceutical companies, medical devices and biological preparations, etc., the current Internet medical model is nothing more than one or several links.

“But looking at these links, the best money should be the last ones, followed by patients and the general public. The middle links (medical care + public hospitals) are basically unlikely to make money because the country does not Allowing these links for the purpose of making money is welfare and public welfare.” Li Yi (pseudonym) revealed to Bullet Finance.

In fact, some policies issued by local health committees also indirectly prove this point of view. Relevant media reports can see that local governments are encouraging grassroots hospitals to implement the “family doctor” system, and most grassroots medical institutions have begun to operate. The “family doctor” model has public endorsements and offline advantages, and is easier to be accepted by patients. This will also cause competitive pressure on WeDoctor’s existing business in the future.

In addition, professional nursing, chronic disease management, etc., where WeDoctor is most likely to make money, have become the key areas for the other three competitors to cut into. After that, WeDoctor’s competitive pressure will increase.

As can be seen from the marketing data, only medical services such as professional nursing and chronic disease management can be advertised. Although the marketing expenses of WeDoctor Holdings are increasing, according to the statistics of TalkingData mobile data, in 2018 and March 2019, WeDoctor App has been ranked fifth in mobile healthcare, and fell to ninth in March 2020. In 2021 Falling to the thirteenth place in February.

It is not difficult to see that in this micro-medicine called “the most profitable field”, the pressure of competition is increasing day by day.

Now, WeDoctor, which has fully demonstrated its advantages, has successfully reached the door of the Hong Kong Stock Exchange, only one step away from listing. However, in the Hong Kong stocks, “penny stocks everywhere” is the norm for investors. If WeDoctor still cannot prove to the capital market its prospects for large-scale profitability, even if it goes public, it will not be able to solve its own problems.