When the hustle and bustle came to an end, calmness became the beginning of the golden age.

Editor’s note: This article is from WeChat public account “ Rongzhong Finance ” (ID: thecapital), author Shi Xiaopu, Miao Tong.

In the equity investment market in 2019, state-owned assets and US dollar funds have become two major protagonists.

According to statistics, as of the end of November, the total amount of capital raised in the venture capital industry exceeded one trillion yuan, a decrease of 10% year-on-year. The total scale of Chinese LP subscriptions accounted for 68.8%, and US dollar funds accounted for nearly 15% of the total funds raised. “Folk capital” is minimal.

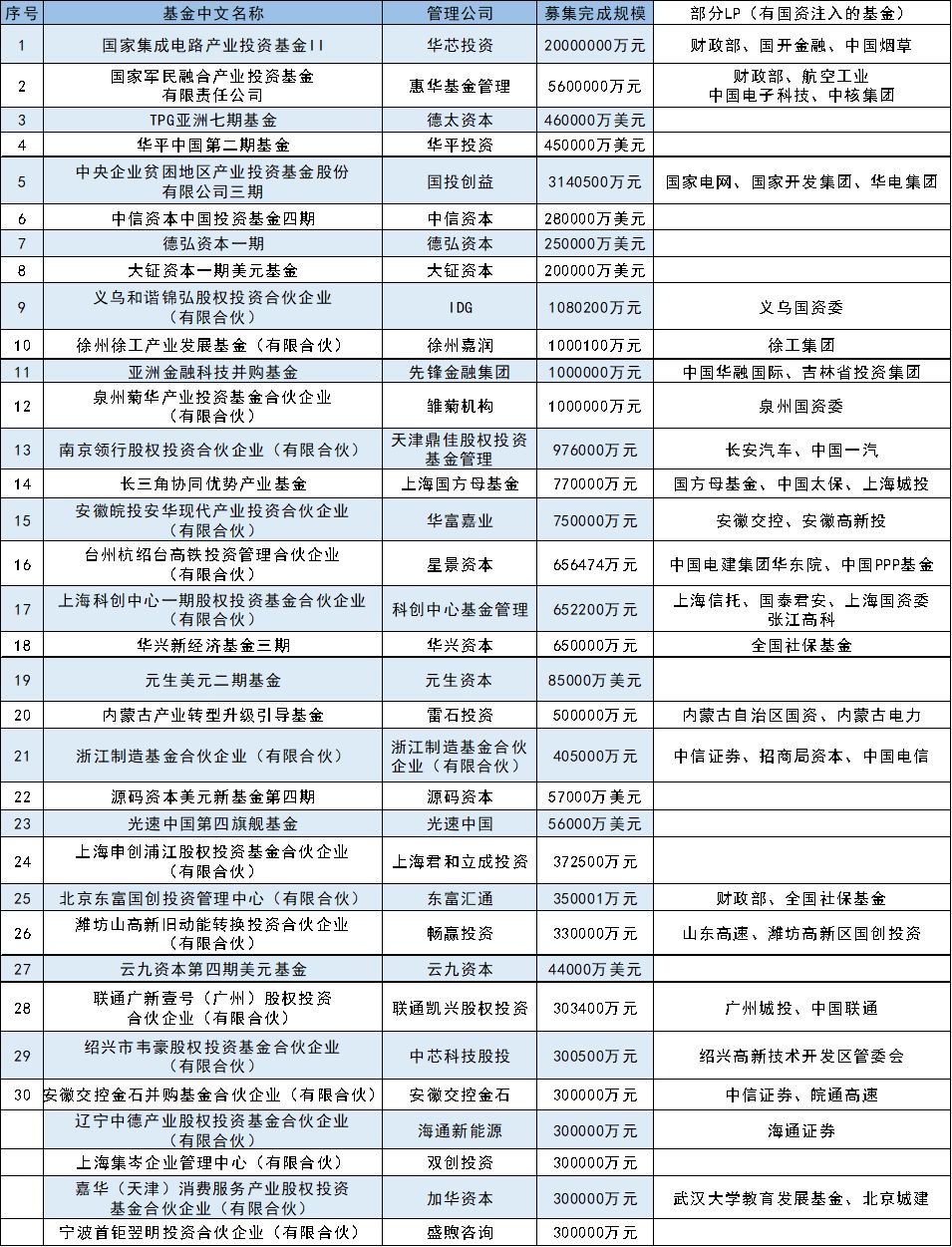

The investment amount was 730 billion yuan, a decrease of nearly 30% compared with the same period in 2018. On the exit, the number of IPOs increased by 70% year-on-year, and nearly 1500, becoming a major IPO year. According to the statistics of Rongzhong Finance, the TOP30 funds raised in the primary market in 2019 are as follows:

Note: Statistics are based on the end of November 2019 Scale ranking

The number of funds has been cut, and the dollar fund has risen

According to statistics, as of the end of November 2019, a total of 330 funds had been raised in the primary market. Compared with the 686 funds raised in the same period last year, the number of was almost cut.

Sorted by the scale of fundraising completion, 25 RMB funds raised a total of RMB 41336875 million in the TOP30 fund of 2019.Nine US dollar funds raised a total of 188.2 billion US dollars (funds with the same fundraising scale were included in the selection, and 34 funds were selected).

In the TOP30 of the same period in 2018, four US dollar funds raised a total of 19.193 billion US dollars, and RMB funds raised a total of 32158369 million yuan. Compared with 2018, the fundraising amount of US dollar funds rose 874% this year, and the fundraising amount of RMB funds rose 28%. Dollar funds are on the rise.

![2019 Private Equity Fund TOP30: State-owned and US dollar funds are]()

In the future, the US dollar foundation will be more abundant. Northern Lights Deng Feng once stated that RMB funds will be difficult to change in the short term, while head funds and US dollar funds are in a state of “investing in projects at any time.”

On the reasons for the rise of the US dollar fund, in addition to the global capital’s optimistic attitude towards China’s long-term development potential, Rongzhong Finance believes that in the past two years, the number of IPOs of Hong Kong and US stocks has increased significantly, and the US dollar fund has successfully exited, thereby Bet on the Chinese market. Secondly, the strong performance of the US stock market has led to a return of funds, resulting in a significant increase in the allocation of funds to the Asian and Chinese markets in 2019.

State-owned assets still occupy the absolute C position

Continuing the C position of state-owned assets in 2018, as of the end of November 2019, 22 of the fundraising TOP30 funds have state-owned properties, and the government is one of the main funders, or central enterprises, urban investment State-owned enterprises including companies are active.

The largest fundraising scale in 2019 is the National Integrated Circuit Industry Investment Fund Phase II with a scale of 200 billion yuan. It was co-sponsored by the Ministry of Finance, China Development Bank, China Tobacco, Yizhuang SDIC, China Mobile, Shanghai Guosheng, China Electronics, China Electronics Technology, and Huaxin Investment.

The National Military-civilian Fusion Industry Investment Fund, with a fundraising scale of 5.6 billion yuan, was initiated by the Ministry of Finance and the National Defense Science and Industry Bureau. Its shareholders include central enterprises such as China Electronics Technology Corporation, AVIC, China Aviation Development Corporation, China Shipbuilding Corporation, China National Nuclear Corporation.

In addition, the funds directly invested by state-owned assets are in Beijing Dongfu Guochuang Investment Management.Xin (Limited Partnership), “Huaxing New Economic Fund Phase III” and Inner Mongolia Industrial Transformation and Upgrade Guidance Fund and other funds.

Beijing Dongfu Guochuang Investment Management Center is invested by the Ministry of Finance and the National Social Security Fund. The total fundraising of the third phase of the Huaxing New Economic Fund exceeds 6.5 billion yuan. Among the investors, except the old shareholders, the National Social Security Fund, banks, and insurance , Market-based mother funds, etc. have joined one after another. The investors of the Inner Mongolia Industrial Transformation and Upgrade Guidance Fund include autonomous state-owned companies, Inner Mongolia Electric Power (Group) Co., Ltd., etc.

In addition to direct financial contributions, state-owned enterprises including central enterprises and urban investment companies are also very active. For example, investors in the Yangtze River Delta Synergy Advantage Fund include China Pacific Insurance, Shanghai Urban Investment, Yangtze State Investment and so on.

Yiwu Harmonious Jinhong Equity Investment Partnership (Limited Partnership) is owned by Sichuan Shuangma Cement, Weifang Shangao New and Old Kinetic Energy Conversion Investment Partnership (Limited Partnership) is controlled by Shandong Expressway Group and Xuzhou Xugong Industry Development Fund (Limited Partnership) Investors include XCMG, a central enterprise.

In addition, in the TOP30, some GPs are held by state-owned assets, such as Huaxin Investment, which is the Phase II manager of the National Integrated Circuit Industry Investment Fund, and State Investment, which is the Phase III manager of the Central Enterprise Poor Area Industrial Investment Fund Co., Ltd. Creating benefits, etc.

Consumption upgrade and industry integration have received much attention

In terms of investment, in the TOP 30 fundraising scale in 2019, there are five national-funded central SOE funds. Compared with the top 30 fundraising funds in 2018, which mainly focus on the Belt and Road Initiative and international joint industrial funds, the main areas invested this year are Mainly focus on the national infrastructure and people’s livelihood-related infrastructure construction and local poverty reduction.

“National Integrated Circuit Industry Investment Fund II” will invest in investment planning around national strategies and emerging industries, such as smart cars, smart grids, artificial intelligence, the Internet of Things, 5G, etc.

The National Military-civilian Integration Industry Investment Fund is mainly invested in high-tech enterprises with mature patents and technologies in growth and maturity periods with broad technological application prospects in the military-civilian integration industry.

“Phase III of the Central Enterprise Poor Area Industrial Investment Fund Co., Ltd.” has been invested in 14 concentrated and extremely poor areas such as “Three Districts and Three States”, investing in a number of leading enterprises that have a major role in promoting regional industries and good results in poverty reduction. IPO project. At the same time, it will also cooperate with local governments to set up sub-funds in poor areas to leverage more social capital into poor areas.

The “Yangtze River Delta Synergy Advantage Industry Fund” managed by Shanghai Guofang’s parent fund aims to promote long-term growth by investing in “hard technology” sub-funds, “complete industry chain” sub-funds, and “star projects”. The deep integration of the triangular industrial chain, the accelerated development of advantageous enterprises in the industrial chain, and the acceleration of the formation of a future-oriented advantageous industrial cluster in the Yangtze River Delta.

“Inner Mongolia Industrial Transformation and Upgrade Guiding Fund”Gold promotes social capital investment, stimulates the motivation and vitality of social investment, and guides social capital to invest in pillar industries and strategic emerging industries.

Secondly, large consumption, medical care, fintech, and corporate services are still the areas that institutions focus on. “Dehong Capital Phase I”, “Dazheng Capital Phase I USD Fund”, and “Yuansheng Capital USD Phase II Fund” , “Lightspeed China Fourth Flagship Fund”, “Huaxing New Economic Fund Phase III”, “Cloud Nine Capital Phase IV USD Fund” and other 6 funds all focus on domestic consumption upgrade and industry integration industry sectors, including consumer Internet, medical Health, technology finance and business services.

Among them, “Huaxing New Economic Fund Phase III” will also focus on emerging tracks including new energy and advanced manufacturing.

Funds focusing on big data, artificial intelligence, and blockchain are only one “Asian Fintech M & A Fund”. In addition, chips, new energy vehicles, and new technologies related to clean technology all have 1 branch, and the scale of fundraising is all 10 billion.

The only special fund in the TOP30 fundraising scale is “Taizhou Hang Shao Tai High-speed Railway Investment Management Partnership (Limited Partnership)”. Its largest shareholder, Fuxing International, holds 40.43% of the shares, and will be mainly engaged in railway investment, construction and operation management, and comprehensive development and utilization of supporting land along the line.

According to the statistics of Rongzhong Research Institute, in the first half of 2019, the funds that completed fundraising were mostly growth and venture capital funds. VC is mainly concentrated in emerging areas such as health care, internet, IT and information technology, and artificial intelligence. The investment amount in the former two accounts for 16.32% and 13.09%, respectively. PE investment focuses on the manufacturing and automotive industries, with investment amounts of 15.59% and 10.81%, respectively. Compared with 2018, the investment activity of the entertainment media industry has dropped significantly.

According to the survey, 60% of institutions will focus on the four strategic emerging industries of artificial intelligence, medical and health, high-end equipment manufacturing, big data and enterprise services in the coming year. Especially in the field of hard technology and high-end manufacturing, due to the background of international relations and policy support, it has attracted much attention from investment institutions.

2019, past and future

From a global perspective, the capital winter is not just happening in China.

Global funds, especially the North American market, have slowed their fundraising. In Q2 2019, a total of 244 funds were raised, setting a new low in five years. Among them, 139 funds raised in the North American market raised a total of US $ 68 billion, and 45 funds raised in the Asian market raised a total of US $ 15 billion. At the same time, the speed of fundraising has greatly improved. Under the “stringent” requirements of LP, nearly half of the funds were raised within half a year.

If divided by fund type, the most active is the VC fund, but its total fundraising is small. 5% head base on the marketGold raised about 70% of the funds in the market. In the industry’s opinion, the total amount of global investment will continue to decline for some time to come, but the main way of LP investment will be based on M & A funds.

Look again at the Chinese market.

From 2015 to 2017, local GPs expanded dramatically. The scale of RMB fundraising increased from less than 200 billion yuan in 2014 to 100 billion yuan in 2017. Some established US dollar GPs have also started to raise RMB funds.

In 2018, shortly after the introduction of the new rules on asset management, the primary market “suddenly cooled”. Compared with the same period, the number of newly raised funds and the total amount raised were down by 47.2% and 19.4%, respectively. Under the cold winter of capital, state-owned assets have become the life-saving straw for GPs. Under the 28 rule, head institutions and state-owned institutions have raised most of the funds on the market.

At the same time, the exit of the equity investment market has begun to enter a “harvest”. According to statistics, in the first half of 2019, there were a total of 831 equity investment market exit cases in the primary market. In addition to the launch of the Science and Technology Innovation Board as a way to increase equity exits, driven by environmental impact and driven by their own business needs, investors prefer to speed up the pace of returning funds and settle down.

Combined with macroeconomic conditions and equity investment data, In 2019, the primary market will gradually return to rationality, entering the stage of inventory clearance and high-quality development.

“Based on the underlying foundation of the investment logic, the industry is divided into stages, and the capital is divided into layers. Only when we find the combination of the two can we maximize our effectiveness and obtain investment income.” According to Zhu Shan, chairman of Rongzhong Group, “Model innovation and technological innovation complement each other and must not be partial; Industry and investment require two rounds of action. One important aspect is that investment institutions empower traditional economies and enterprises by holding listed companies, and Energy-based mergers and acquisitions. “

Currently, China ’s largest investment theme is industrial upgrading, and the country is gathering a lot of high-quality resources, including capital.

When the hustle and bustle comes to an end, calmness becomes the beginning of the golden age.

On the reasons for the rise of the US dollar fund, in addition to the global capital’s optimistic attitude towards China’s long-term development potential, Rongzhong Finance believes that in the past two years, the number of IPOs of Hong Kong and US stocks has increased significantly, and the US dollar fund has successfully exited, thereby Bet on the Chinese market. Secondly, the strong performance of the US stock market has led to a return of funds, resulting in a significant increase in the allocation of funds to the Asian and Chinese markets in 2019.

Continuing the C position of state-owned assets in 2018, as of the end of November 2019, 22 of the fundraising TOP30 funds have state-owned properties, and the government is one of the main funders, or central enterprises, urban investment State-owned enterprises including companies are active.

The largest fundraising scale in 2019 is the National Integrated Circuit Industry Investment Fund Phase II with a scale of 200 billion yuan. It was co-sponsored by the Ministry of Finance, China Development Bank, China Tobacco, Yizhuang SDIC, China Mobile, Shanghai Guosheng, China Electronics, China Electronics Technology, and Huaxin Investment.

The National Military-civilian Fusion Industry Investment Fund, with a fundraising scale of 5.6 billion yuan, was initiated by the Ministry of Finance and the National Defense Science and Industry Bureau. Its shareholders include central enterprises such as China Electronics Technology Corporation, AVIC, China Aviation Development Corporation, China Shipbuilding Corporation, China National Nuclear Corporation.

In addition, the funds directly invested by state-owned assets are in Beijing Dongfu Guochuang Investment Management.Xin (Limited Partnership), “Huaxing New Economic Fund Phase III” and Inner Mongolia Industrial Transformation and Upgrade Guidance Fund and other funds.

Beijing Dongfu Guochuang Investment Management Center is invested by the Ministry of Finance and the National Social Security Fund. The total fundraising of the third phase of the Huaxing New Economic Fund exceeds 6.5 billion yuan. Among the investors, except the old shareholders, the National Social Security Fund, banks, and insurance , Market-based mother funds, etc. have joined one after another. The investors of the Inner Mongolia Industrial Transformation and Upgrade Guidance Fund include autonomous state-owned companies, Inner Mongolia Electric Power (Group) Co., Ltd., etc.

In addition to direct financial contributions, state-owned enterprises including central enterprises and urban investment companies are also very active. For example, investors in the Yangtze River Delta Synergy Advantage Fund include China Pacific Insurance, Shanghai Urban Investment, Yangtze State Investment and so on.

Yiwu Harmonious Jinhong Equity Investment Partnership (Limited Partnership) is owned by Sichuan Shuangma Cement, Weifang Shangao New and Old Kinetic Energy Conversion Investment Partnership (Limited Partnership) is controlled by Shandong Expressway Group and Xuzhou Xugong Industry Development Fund (Limited Partnership) Investors include XCMG, a central enterprise.

In addition, in the TOP30, some GPs are held by state-owned assets, such as Huaxin Investment, which is the Phase II manager of the National Integrated Circuit Industry Investment Fund, and State Investment, which is the Phase III manager of the Central Enterprise Poor Area Industrial Investment Fund Co., Ltd. Creating benefits, etc.

Consumption upgrade and industry integration have received much attention

In terms of investment, in the TOP 30 fundraising scale in 2019, there are five national-funded central SOE funds. Compared with the top 30 fundraising funds in 2018, which mainly focus on the Belt and Road Initiative and international joint industrial funds, the main areas invested this year are Mainly focus on the national infrastructure and people’s livelihood-related infrastructure construction and local poverty reduction.

“National Integrated Circuit Industry Investment Fund II” will invest in investment planning around national strategies and emerging industries, such as smart cars, smart grids, artificial intelligence, the Internet of Things, 5G, etc.

The National Military-civilian Integration Industry Investment Fund is mainly invested in high-tech enterprises with mature patents and technologies in growth and maturity periods with broad technological application prospects in the military-civilian integration industry.

“Phase III of the Central Enterprise Poor Area Industrial Investment Fund Co., Ltd.” has been invested in 14 concentrated and extremely poor areas such as “Three Districts and Three States”, investing in a number of leading enterprises that have a major role in promoting regional industries and good results in poverty reduction. IPO project. At the same time, it will also cooperate with local governments to set up sub-funds in poor areas to leverage more social capital into poor areas.

The “Yangtze River Delta Synergy Advantage Industry Fund” managed by Shanghai Guofang’s parent fund aims to promote long-term growth by investing in “hard technology” sub-funds, “complete industry chain” sub-funds, and “star projects”. The deep integration of the triangular industrial chain, the accelerated development of advantageous enterprises in the industrial chain, and the acceleration of the formation of a future-oriented advantageous industrial cluster in the Yangtze River Delta.

“Inner Mongolia Industrial Transformation and Upgrade Guiding Fund”Gold promotes social capital investment, stimulates the motivation and vitality of social investment, and guides social capital to invest in pillar industries and strategic emerging industries.

Secondly, large consumption, medical care, fintech, and corporate services are still the areas that institutions focus on. “Dehong Capital Phase I”, “Dazheng Capital Phase I USD Fund”, and “Yuansheng Capital USD Phase II Fund” , “Lightspeed China Fourth Flagship Fund”, “Huaxing New Economic Fund Phase III”, “Cloud Nine Capital Phase IV USD Fund” and other 6 funds all focus on domestic consumption upgrade and industry integration industry sectors, including consumer Internet, medical Health, technology finance and business services.

Among them, “Huaxing New Economic Fund Phase III” will also focus on emerging tracks including new energy and advanced manufacturing.

Funds focusing on big data, artificial intelligence, and blockchain are only one “Asian Fintech M & A Fund”. In addition, chips, new energy vehicles, and new technologies related to clean technology all have 1 branch, and the scale of fundraising is all 10 billion.

The only special fund in the TOP30 fundraising scale is “Taizhou Hang Shao Tai High-speed Railway Investment Management Partnership (Limited Partnership)”. Its largest shareholder, Fuxing International, holds 40.43% of the shares, and will be mainly engaged in railway investment, construction and operation management, and comprehensive development and utilization of supporting land along the line.

According to the statistics of Rongzhong Research Institute, in the first half of 2019, the funds that completed fundraising were mostly growth and venture capital funds. VC is mainly concentrated in emerging areas such as health care, internet, IT and information technology, and artificial intelligence. The investment amount in the former two accounts for 16.32% and 13.09%, respectively. PE investment focuses on the manufacturing and automotive industries, with investment amounts of 15.59% and 10.81%, respectively. Compared with 2018, the investment activity of the entertainment media industry has dropped significantly.

According to the survey, 60% of institutions will focus on the four strategic emerging industries of artificial intelligence, medical and health, high-end equipment manufacturing, big data and enterprise services in the coming year. Especially in the field of hard technology and high-end manufacturing, due to the background of international relations and policy support, it has attracted much attention from investment institutions.

2019, past and future

From a global perspective, the capital winter is not just happening in China.

Global funds, especially the North American market, have slowed their fundraising. In Q2 2019, a total of 244 funds were raised, setting a new low in five years. Among them, 139 funds raised in the North American market raised a total of US $ 68 billion, and 45 funds raised in the Asian market raised a total of US $ 15 billion. At the same time, the speed of fundraising has greatly improved. Under the “stringent” requirements of LP, nearly half of the funds were raised within half a year.

If divided by fund type, the most active is the VC fund, but its total fundraising is small. 5% head base on the marketGold raised about 70% of the funds in the market. In the industry’s opinion, the total amount of global investment will continue to decline for some time to come, but the main way of LP investment will be based on M & A funds.

Look again at the Chinese market.

From 2015 to 2017, local GPs expanded dramatically. The scale of RMB fundraising increased from less than 200 billion yuan in 2014 to 100 billion yuan in 2017. Some established US dollar GPs have also started to raise RMB funds.

In 2018, shortly after the introduction of the new rules on asset management, the primary market “suddenly cooled”. Compared with the same period, the number of newly raised funds and the total amount raised were down by 47.2% and 19.4%, respectively. Under the cold winter of capital, state-owned assets have become the life-saving straw for GPs. Under the 28 rule, head institutions and state-owned institutions have raised most of the funds on the market.

At the same time, the exit of the equity investment market has begun to enter a “harvest”. According to statistics, in the first half of 2019, there were a total of 831 equity investment market exit cases in the primary market. In addition to the launch of the Science and Technology Innovation Board as a way to increase equity exits, driven by environmental impact and driven by their own business needs, investors prefer to speed up the pace of returning funds and settle down.

Combined with macroeconomic conditions and equity investment data, In 2019, the primary market will gradually return to rationality, entering the stage of inventory clearance and high-quality development.

“Based on the underlying foundation of the investment logic, the industry is divided into stages, and the capital is divided into layers. Only when we find the combination of the two can we maximize our effectiveness and obtain investment income.” According to Zhu Shan, chairman of Rongzhong Group, “Model innovation and technological innovation complement each other and must not be partial; Industry and investment require two rounds of action. One important aspect is that investment institutions empower traditional economies and enterprises by holding listed companies, and Energy-based mergers and acquisitions. “

Currently, China ’s largest investment theme is industrial upgrading, and the country is gathering a lot of high-quality resources, including capital.

When the hustle and bustle comes to an end, calmness becomes the beginning of the golden age.

From a global perspective, the capital winter is not just happening in China.

Global funds, especially the North American market, have slowed their fundraising. In Q2 2019, a total of 244 funds were raised, setting a new low in five years. Among them, 139 funds raised in the North American market raised a total of US $ 68 billion, and 45 funds raised in the Asian market raised a total of US $ 15 billion. At the same time, the speed of fundraising has greatly improved. Under the “stringent” requirements of LP, nearly half of the funds were raised within half a year.

If divided by fund type, the most active is the VC fund, but its total fundraising is small. 5% head base on the marketGold raised about 70% of the funds in the market. In the industry’s opinion, the total amount of global investment will continue to decline for some time to come, but the main way of LP investment will be based on M & A funds.

Look again at the Chinese market.

From 2015 to 2017, local GPs expanded dramatically. The scale of RMB fundraising increased from less than 200 billion yuan in 2014 to 100 billion yuan in 2017. Some established US dollar GPs have also started to raise RMB funds.

In 2018, shortly after the introduction of the new rules on asset management, the primary market “suddenly cooled”. Compared with the same period, the number of newly raised funds and the total amount raised were down by 47.2% and 19.4%, respectively. Under the cold winter of capital, state-owned assets have become the life-saving straw for GPs. Under the 28 rule, head institutions and state-owned institutions have raised most of the funds on the market.

At the same time, the exit of the equity investment market has begun to enter a “harvest”. According to statistics, in the first half of 2019, there were a total of 831 equity investment market exit cases in the primary market. In addition to the launch of the Science and Technology Innovation Board as a way to increase equity exits, driven by environmental impact and driven by their own business needs, investors prefer to speed up the pace of returning funds and settle down.

Combined with macroeconomic conditions and equity investment data, In 2019, the primary market will gradually return to rationality, entering the stage of inventory clearance and high-quality development.

“Based on the underlying foundation of the investment logic, the industry is divided into stages, and the capital is divided into layers. Only when we find the combination of the two can we maximize our effectiveness and obtain investment income.” According to Zhu Shan, chairman of Rongzhong Group, “Model innovation and technological innovation complement each other and must not be partial; Industry and investment require two rounds of action. One important aspect is that investment institutions empower traditional economies and enterprises by holding listed companies, and Energy-based mergers and acquisitions. “

Currently, China ’s largest investment theme is industrial upgrading, and the country is gathering a lot of high-quality resources, including capital.

When the hustle and bustle comes to an end, calmness becomes the beginning of the golden age.