It is expected that as the demand for new energy vehicles continues to expand, industrial metals such as copper, which are closely related to it, still have a large room for growth.

Text | Ding Mao

Edit | Li Yuqian

NIO, Tesla, BYD, Hongguang MINI EV, the demand for new energy vehicles is soaring, what else can we invest in besides stocks?

Beginning in the second quarter, bulk commodities, especially industrial metals, ushered in a round of rising cycles, due to the unexpected rebound of the Chinese economy and the outbreak of demand for new energy vehicles in China and Europe.

As an ordinary investor, how to grasp the investment opportunities?

Commodity returns strongly

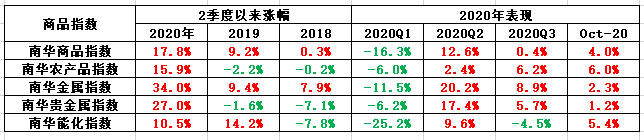

Since the second quarter of 2020, as the domestic economy has gradually stabilized, the bulk commodity market has ushered in a strong rebound. In terms of the comprehensive yield of South China Commodities, from April 1 to October 22, 2020, bulk commodities achieved an increase of 17.8%, better than the 9.2% and 0.3% in the same period in 2019 and 2018.

From the classification index, the performance of industrial metals and precious metals is even stronger.

Figure 1: Commodity and classification index performance

Data source: choice financial terminal, sorted out

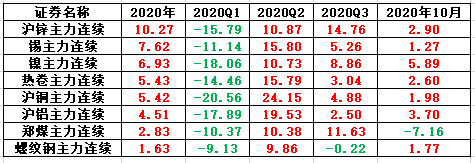

Figure 2: Industrial metal + thermal coal yield rate (%)

Data source: choice financial terminal, sorted out

The reason for the strength of industrial metals

(1) China’s economy rebounds beyond expectations

After the outbreak of the epidemic in 2020, countries have generally adopted strict control measures, and the global economy has quickly fallen into recession.

Thanks to effective epidemic prevention and control measures and easing policy support, my country’s economic recovery is ahead of other countries, leading to a sharp rebound in industrial metal prices.

The reason for this is that, on the one hand, after the relaxation of epidemic control measures, the resumption of work and production in the secondary industry is faster than that of the tertiary industry; on the other hand, compared to consumption, investment is sensitive to lower interest rates and fiscal expansion Higher degrees (real estate is most sensitive to the decline in interest rates under loose monetary policy, and the main source of funding for infrastructure is fiscal bond issuance).

Based on this, we can see that since the second quarter, the most important driving force for my country’s economic recovery is the unexpected recovery of real estate investment, infrastructure, and industrial production.

Whether it is the recovery of real estate, infrastructure or industrial production, all have a high degree of dependence on industrial metals. After the epidemic, with the gradual acceleration of the recovery in the three major areas, the demand for industrial metals continued to rise, which eventually pushed up the current round of rebound in industrial metal prices.

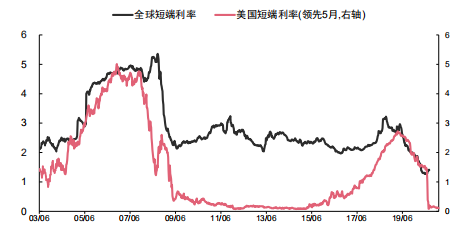

(2) Global liquidity is flooding

In addition to the Chinese factor, the loose global liquidity during the year also played an important role in supporting the prices of industrial products. Bulk commodities have both physical and financial characteristics, so compared to other investment products, bulk commodities have better anti-inflation properties.

During the year, developed economies represented by the Federal Reserve generally introduced super-loose monetary policies, causing global liquidity to overflow. On the one hand, the expansion of liquidity can better support the bottoming and rebound of the economy, and on the other hand, it is also easy to trigger the rise of inflation in the later period.

The flood of liquidity in the global market (especially in the United States) has increased investors’ expectations of future inflation, which to a certain extent triggers anti-inflationary demand for commodities and supports the upward movement of commodity prices.

Figure 3: The global short-end interest rate declines rapidly

Data source: Caixin Securities, sorted out

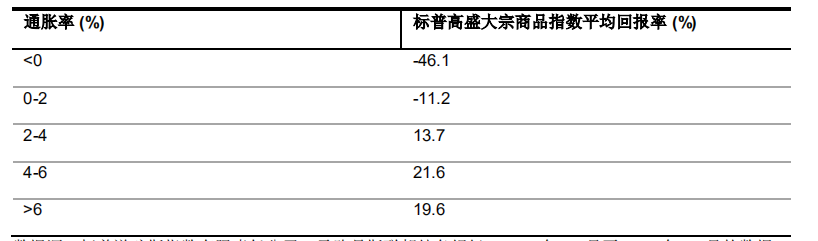

Figure 4: The relationship between U.S. inflation and commodities

Drawing

Future outlook

Looking forward to the fourth quarter, we are still optimistic about the investment opportunities related to commodities, especially industrial metals. The specific reasons can be summarized into 2 points:

(1) Sino-US economic recovery resonates

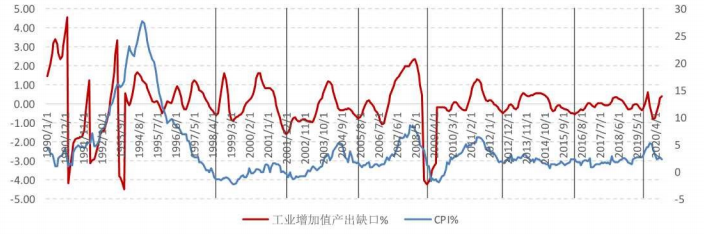

Since the second quarter, my country’s economy has taken the lead in recovering. After August, the economic recovery has accelerated significantly. As shown in Figure 5, according to Caixin Securities’ output gap index (According to the calculation of industrial added value), the current economic cycle actually started in October 2019, but due to the impact of the epidemic at the beginning of the year, the economy experienced a short recession. After the impact of the epidemic bottomed out in April, my country’s economy entered the recovery cycle again in August. Begin to accelerate the recovery process.

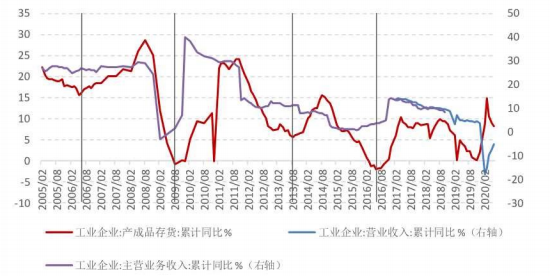

Combined with the inventory cycle, the inventory cycle has entered a passive destocking stage starting in May, and the inventory turning point appeared in August, indicating that the domestic inventory cycle may be in the channel of “passive destocking-active restocking”.

On the whole, my country’s inventory cycle is in good agreement with the industrial output gap, indicating that after the fourth quarter, my country’s economy is expected to transition from the recovery phase to the expansion phase.

Figure 5: Industrial production output gap

Data source: Caixin Securities, sorted out

Figure 6: China inventory cycle

Data source: Caixin Securities, sorted out

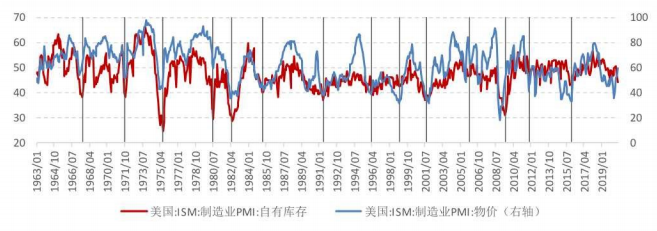

Compared with the strong performance of the Chinese economy, the overall US economic recovery during the year was weak. As shown in Figure 7, in February 2020, the US economy fell into recession, ending the expansion cycle since June 2009. After May, with the recovery of demand, the US inventory cycle has entered a passive destocking phase in which prices rise and shrink.

But starting in June, the second outbreak of the epidemic extended the time for this round of passive destocking. Looking ahead, it is expected that with 1After the election in January, the United States is expected to introduce more stimulus policies to accelerate the recovery of demand, making US inventories expected to bottom out from the end of the fourth quarter to early next year.

Figure 7: U.S. inventory cycle

Data source: Caixin Securities, sorted out

From a comprehensive point of view, starting in the fourth quarter, the strong recovery of China’s economy combined with the resonance of the US economic rebound is expected to promote the further release of industrial metal demand and drive industrial metal prices to continue to rise.

(2) Demand for new energy vehicles soars

According to Goldman Sachs, a relatively alternative reason for the increase in industrial metal prices during the year was the rapid advancement of new energy-related policies in China and Europe.

In Europe, in 2020, the European Commission issued the most stringent carbon emission limit regulation in history. At the same time, 24 of the 27 EU countries have introduced new energy vehicle incentive policies. Driven by policies, the European new energy vehicle market expanded rapidly, surpassing China in the first half of the year to become the world’s largest new energy vehicle market.

According to data from the European Automobile Manufacturers Association (AECA), in September 2020, Germany, the United Kingdom, France, Norway, Sweden, Portugal, Italy, Switzerland, Spain and other nine Guoxin Energy’s vehicle sales totaled approximately 133,000 vehicles, a year-on-year increase of 195%. But the current penetration rate of new energy vehicles is still maintained at a low level of 12%.

In China, with the recovery of optional consumption in my country in July and August, my country’s auto consumption rebounded rapidly, supporting the stability of the overall consumption level.

According to the data from the Travel Association, in September 2020, my country’s new energy vehicle sales will be138,000 vehicles, a year-on-year increase of 67.7%, setting a new historical record in September; wholesale sales of new energy passenger vehicles in September exceeded 125,000, a year-on-year increase of 99.6%.

What’s more gratifying is that this round of sales surge is based on the decline of subsidies, showing a strong rebound in C-end demand.

Looking forward, it is expected that with the continuous expansion of new energy market demand in China and Europe, industrial metals such as copper, which are closely related to new energy manufacturing, still have a large room for growth.

In addition, if in the future Biden can be successfully elected. It is expected that the United States will also launch a corresponding The “green infrastructure” policy is expected to further push up the price increase of industrial metals.

Configuration recommendations

In the financial market, direct investment in bulk commodities belongs to futures investment, which has high leverage. The act of increasing leverage will amplify the volatility of commodities and make investors bear more risks, which is extremely unfriendly to ordinary investors.

Therefore, for ordinary investors who want to participate in this round of commodity cycle, instead of directly investing in commodity futures, analysts recommend that everyone pay attention to the procyclical raw material sector that is more related to industrial products. For example, steel, cement, coal, etc.; and the upstream raw material sectors in the new energy automobile industry chain, such as non-ferrous metals (copper, aluminum, lithium, cobalt), etc.