The Internet does not have a second half, but sinks, sinks, sinks!

Editor’s note: This article is from WeChat public number “letter list” (ID: wujicaijing), author Tan Yuhan.

There is no second half of the Internet, but sinking, sinking, sinking!

In April of this year, Snowball founder Fang Sanwen once launched a reward question and answer on the snowball. “If you don’t put a lot of money, don’t market, the number of users, GMV, customer order, customer price can be of any order of magnitude. Growth?”

You can also ask: When the marketing cost growth slows down, what level of growth will there be? The fight for the second quarter of 2019 gave an answer.

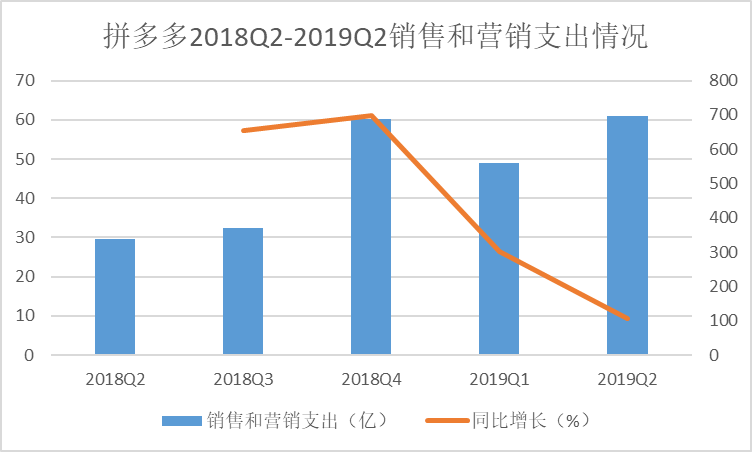

In the second quarter, a lot of sales and marketing expenses were 6.1037 billion yuan, from absolute In terms of numbers, this is still a huge expenditure. In the second quarter, the company has also launched a 10 billion subsidy activity. The platform is still paying for future growth through large-scale marketing expenditure, but the 105% year-on-year growth rate and the previous three quarters. Compared with the figures of 302%, 699% and 655%, it has dropped significantly.

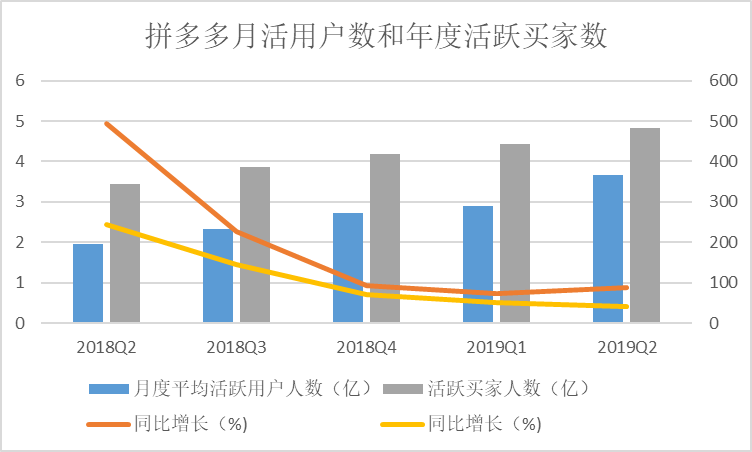

The number of GMV and monthly active users has not been affected by the slowdown in marketing expenses. The slowdown in year-on-year growth is lower than sales and marketing expenses, and maintains rapid growth. In the 12 months ended June 30, the total number of GMVs was 709.1 billion yuan, an increase of 171% year-on-year; the average number of monthly active users was 366 million, an increase of 88% year-on-year and an increase of 76.3 million. This shows that the efficiency of a lot of marketing expenses has been improved this season.

This quarter’s earnings report also contributed two figures that are higher than market expectations. The total revenue increased by 169% and 7.29 billion yuan, which exceeded the market consensus of 6.1 billion yuan. Under non-GAAP, the net loss was 411.3 million yuan, which was 70% lower than the 1.791 billion yuan in the first quarter. The market’s general estimate of a loss of 1.87 billion yuan was a net loss of 673.4 million yuan in the same period last year.

In the past two quarters, the company has been criticized by the market for high cost of marketing and marketing, the cost of customers has risen sharply, and the loss has been expanding. Why has the loss been greatly narrowed in this quarter?

One

Under the US GAAP, the actual net loss of 411.3 million yuan generated in the second quarter is generally expectedThe difference of the net loss of 1.87 billion yuan was mainly at the total revenue. Compared with expectations, the actual total revenue exceeded 1.19 billion yuan.

The main contribution to total revenue was online marketing technology service revenue, reaching 6.461 billion yuan, an increase of 173% over the same period last year of 2.371 billion yuan. The explanation given by the multitude is that the platform merchant system is improving, reducing the fixed expenditure cost of the merchants, and the advertising products and marketing tools have improved the return on investment of the merchants.

At the conference call after the release of the first-quarter earnings report, Jiuding, a vice president of strategy, explained the data on revenue conversion rate. “The company’s current focus is not on revenue conversion rate, but on how to enrich product categories. Do a good job in customer service.” Jiuding said that these will help to improve user interaction and user interaction with the platform. These interactions will increase the visibility of the platform brand, and the sales and investment returns of the merchants will increase. More willing to invest more on the platform, the conversion rate will continue to increase. “In terms of revenue generation, the platform is still in its infancy, and we are still placing sales growth at a higher priority when balancing revenue generation and platform sales growth.”

But the growth rate of revenue conversion rate is clearly visible, as evidenced by the second quarter financial data. On the conference call after the earnings report, Credit Suisse analysts mentioned that in order to attract quality merchants, the company once offered a discount, but in the second quarter, the revenue conversion rate resumed growth.

Jiu Ding said that the company will insist on subsidies for quality businesses. This policy has been implemented since the first quarter of this year. The company is also striving to maintain a balance between subsidies and revenue growth. In the second quarter, subsidies were reduced, so revenue conversion rate There are certain fluctuations. “The current fluctuations in revenue conversion rate are negligible. In the longer period of time, the conversion rate will be relatively stable.”

From the 12-month dimension, in the 12 months ended June 30, the revenue conversion rate was 2.94%, compared with 2.92% in the previous quarter, compared with 2.17% in the same period last year. This figure has gradually increased in this year and has remained in a stable range. As GMV maintains rapid growth, revenue will naturally increase.

two

The two influencing factors of dismantling GMV are user size and average consumption.

User size is the more prominent figure in this quarterly earnings report. As of the end of June, the number of active buyers of the multi-platform platform reached 483.2 million, and the number of active buyers in the single quarter increased by 39.9 million. In the previous three quarters, the number of new buyers in the single quarter has declined successively, mainly due to the e-commerce season attribute. influences.

The same rebound is also the number of monthly active users. In the second quarter, the figure was 366 million, an increase of 88% compared with 195 million in the same period of last year. This growth rate is higher than the growth rate of the previous quarter. In absolute terms, the number of monthly active users increased by 76.3 million in a single quarter..

In a certain time dimension, e-commerce giants are often a major growth point To support growth, such as customer unit price or number of users, but the number of users has increased rapidly, and the annual expenses per active buyer has also increased significantly. In the 12 months to the end of the second quarter, this figure is 1467.5 yuan. Growth of 92%.

A lot of these user-level growth is attributed to the 618 strategy. Since June 1st, the joint multi-brand merchants have launched a 10 billion subsidy campaign to subsidize 10,000 products, including Apple series electronic products, Dyson home appliances, Bose, Sony headphones and so on.

During the

618 period, more than 1.1 billion physical orders were sold, and sales increased by over 300% year-on-year. Among them, nearly 70% of orders come from cities of the third line and below. In the “spelling mode”, Chery Automobile, Midea Air Conditioner, Electric Shaver, Electric Toothbrush and Genuine Guoxing Apple Series are popular among third- and fourth-line consumers.

From the supply side perspective, the growth of the platform GMV is caused by the products provided by the platform meeting the needs of users. At the end of June, many vice presidents of the company have mentioned that the starting point of the traditional e-commerce and retailers is to help the merchants to sell goods. The starting point of the fight is to help users find the most suitable products. If there is no such commodity in the market, then there is a lot of responsibility to help them “create”.

In December last year, the company launched a new brand plan, hoping to remove unnecessary circulation channels and redundant costs in the retail chain, so that industrial products can reach consumers directly from the production line. Simply put, the offline retailer supply chain is: production – logistics – distribution – terminal – consumer; traditional e-commerce supply chain: production – brand side – generation of operations – logistics – consumers; A lot of supply chain is: production – logistics – consumers.

Under such a streamlined chain, member companies and pilot brands have to make concessions in the early stages. Even after the new branding plan has been internally established, the team has been thinking for a long time to decide whether to push this strategic project. “This is contrary to the traditional brand development model.” Jing Ran said that the traditional brand development model is to pursue high value-added, to promote large-scale expansion and product development investment with high profits, while the new brand plan is to remove channels, marketing, etc. All added value.

Until the one-generation foundry brand became the new first-line brand, the new brand planning team was considered a reassurance. Home Guardian is a member of the new brand plan. Its parent company designs and manufactures products for the world-renowned sweeping robot brands, including Honeywell, Whirlpool, Philips, etc., with an annual production capacity of more than 1 million units. Most of these products are priced at 1,000 yuan. Above, join the new brand plan to jointly create new productsThe sweeping robot under the card is priced at 278 yuan.

The data provided by many parties is that from the end of 2018 to June this year, the home guards sold more than 300,000 sweeping robots, and most of the orders came from the sinking market. “When the price of the sweeping robot is more than one thousand yuan, its target users may only have 10 million people. If the price is lowered to about 300 yuan, the target user may surge to 100 million people, which is a tenfold increase. “Good analysis.

In essence, the rapid growth of the multi-GMV is driven by the increase in retail efficiency.

three

The net loss of the company has narrowed in the second quarter, in addition to the speed-up growth achieved by the revenue side, but also the effective control of the cost side.

In the previous four quarters, sales and marketing expenses accounted for more than 100% of the total revenue. The fight for almost all of the revenue was directed to marketing, in order to purchase the number of users and the future growth of revenue, and In the second quarter, marketing expenditure accounted for 83.7%.

Zhu Ding, vice president of strategy and strategy, said that the company did not set a marketing expenditure quota and a proportion of revenue. From the perspective of the growth rate of GMV and users, the efficiency of marketing expenses has indeed increased in this quarter.

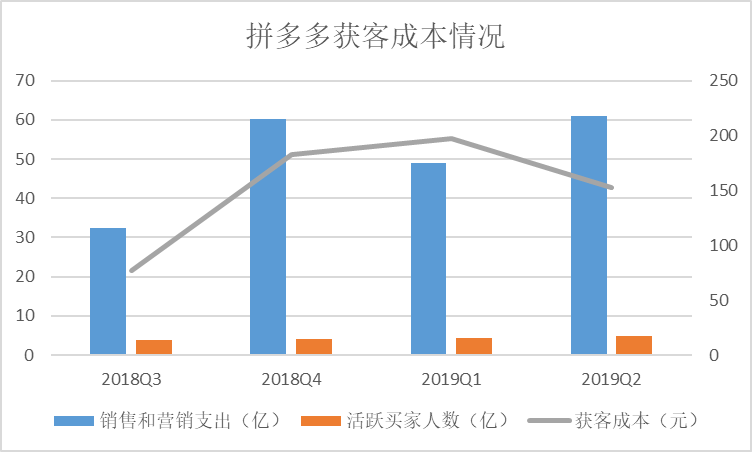

Comprehensively and rudely calculate the cost of getting a lot of customers (= sales and marketing expenses / new buyers in a single season), in the second quarter and third quarter of 2018, respectively, 61 yuan and 77 yuan, but in the first The steep rise in the fourth quarter reached 183 yuan, and the high customer cost continued to 197 yuan in the first quarter of this year. In the second quarter, the cost of passengers declined, falling back to 153 yuan. In fact, even the passenger cost of 197 yuan this year is significantly lower than other e-commerce giants.

Huang Wei mentioned the fight in the conference call after the release of the first quarter earnings report In the form of a lot of sales and marketing expenses, brand advertising is to help raise awareness; online pay-per-action advertising is to increase user traffic and increase user usage; shopping vouchers and discount promotions can improve users’ repurchase rates and repurchase habits. Inspire users to try out new features of the platform.

For the latter two, Huang Wei mentioned that the company has real-time performance monitoring and evaluation, including several factors that can calculate the rate of return, such as shopping frequency, shopping categories, interaction with other users, and The number of new users, the number of inactive users, and more. There are many different monitoring cycles for these indicators. Some are one day, some are one week, and some are one quarter. According to the difference in return rate, the marketing expenditure of these channels is continuously adjusted.

The efficiency gains from sales and marketing expenses may also stem from this, constantly adjusting marketing expenses based on rate of return.Channels and increase the percentage of performance ads and subsidies. “In the second half of 2019, we will continue to expand the benefits and subsidies.” Jiuding said.

four

These marketing expenses are not just sinking market users.

In the first quarter of 2019, 44.2% of the new users were from second-tier and above cities. The latest data given by Huang Wei is that in January of this year, the GMV of users in the first- and second-tier cities of the multi-platform platform was 37%. In June, the proportion has risen to 48%. But he also said that too much has not changed the user development strategy, the growth of first- and second-tier cities is because the platform has always focused on user needs, putting user interests first.

“This shows that the company’s investment in brand recognition has paid off, and the number of users in low-tier cities is also increasing. It is a service for all groups.” Jiuding, vice president of strategy, said.

This is another transformation from the supply side. On July 31 last year, the company announced two announcements, respectively, to issue targeted investment invitations for consumer goods and furniture and building materials such as apparel, food, cosmetics, etc., and invited brand owners to settle in. In August, many brands went online, and Netease carefully selected Hundreds of brands such as Armani and Bose have settled in.

Among the 10 billion subsidy activities launched during the 618 period, large subsidies have flowed to 3C digital products such as Apple mobile phones with higher unit prices.

A lot of good agricultural products are also playing a leading role. During the 618 period, nearly 70% of agricultural product orders came from first- and second-tier cities.

In June of this year, after the news that the poly-sales will become an independent business group, more and more people are also thinking about the independence of the “time-limited spike” channel, the establishment of the second-selling business group, and entering the first- and second-tier cities. Whether this is true or just a public relations war, the pace of moving towards a first- and second-tier cities has accelerated significantly.

When the e-commerce giants rushed to the sinking market where many of them started, the fight was also going up, squeezing into the first- and second-tier markets that had long been considered to have been divided.