This article comes from 36 氪 compilation team “God Translation Bureau”, translator is scale, love Fan Er is authorized to publish.

WeWork is going to go public, how do you view the company’s development prospects? Recently, famous analyst Ben Thompson published an article entitled “The WeWork IPO” on his official blog to analyze the giant players in the shared office field. He believes that WeWork’s development potential can be viewed from the perspective of AWS, and WeWork has no real competitors and has a lot of capital support. But these advantages have also had a negative impact on WeWork.

In the recent past, there has been a lot of discussion about WeWork’s upcoming IPO, and there is a reason behind this.

The prospectus documents they submitted, whether from the company’s vision or from the company’s leadership in the public disregard of corporate governance practices, are a very “daring” document.

And, even though WeWork raised a lot of money, it still had huge losses.

I suspect that all of these things are related.

Examples of AWS

Imagine now that in 2006, you are looking for investors with a bold new business plan: to make a computer hardware.

But at this time, IBM just sold its PC business to Lenovo a year ago, and the server seems to be on the same commoditization path. In addition, companies like Dell have introduced x86 solutions that replace the architecture of traditional vendors like Sun.

From these perspectives, this business plan doesn’t sound particularly promising or sensible.

But in 2006, Amazon launched Amazon Web Services (AWS).

At the time, this was a computer hardware business that commercialized hardware, with an operating margin of about 30%.

It turns out that having a company manages commodity hardware for everyone else has several important advantages that justify these profit margins:

- Because payments are based on usage, the new company basically has free access to the entire server stack for free (for new companies, no business), the payment is zero).

- Growing companies don’t need to pay for months or years ahead of future growth, and they don’t need to spend time on large-scale expansions. Instead, they can pay for new features as needed.

- A mature company no longer needs to have the ability to manage server installations, but instead can focus on its core capabilities while outsourcing related services to cloud providers.

In all three cases, the fundamental shift is to turn the server as a capital investment into a variable cost. The benefit of doing this is not to save money, but to increase flexibility and choice.

At least this is the beginning: Today, AWS provides services that go far beyond basic computing and storage capabilities and extend to features like server-less (inconsistently, this requires a large number of always-available servers) .

WeWork’s “bullish” case

In a broad sense, AWS is WeWork’s “bullish” case. Think about the term “fixed cost.” Nothing is more fixed than the cost of real estate, but WeWork’s services can translate real estate costs into variable costs for various companies, and the benefits are roughly consistent with public clouds:

- The new company can immediately enter a fully equipped office, pay only for one or two desks, and then grow as needed.

- Growing companies don’t need to spend a lot of time building a few months or years before future growth, but pay more for space as needed.

- Mature companies no longer need to have properties all over the world. In fact, they can expand to new areas with very low risk and cost.

Please note that just like public clouds, price is not necessarily the main driver of WeWork. However, with AWS as an example, the cost of paying for the underlying infrastructure is certainly far less than the cost of any customer.

On the one hand, AWS can spread the cost of a global data center to a large number of customers; on the other hand, AWS can bargain with hardware vendors or simply design and build its own components.

To some extent, WeWork can achieve similar benefits.

In one location, because all WeWork members share a common space, the functionality of a public space build is much more powerful than the functionality built by any member. Similarly, WeWork offers a variety of options for all members at outlets around the world.

Wework is also gaining expertise in the effective use of office space, even though oneThis knowledge is just thinking about how to put more people into less space.

But opening a three-digit office space each year means that the company naturally learns and iteratively applies to office space faster than any other company, and it is committed to applying sensors and machine learning. Before this challenge.

One more question is whether WeWork can surpass the size of the original real estate industry: in the field of office space, how can it have the unique ability to be equivalent to “server-less”, which can only be unlocked by one company, for all Do people provide all the real estate needs?

WeWork’s loss and ambition

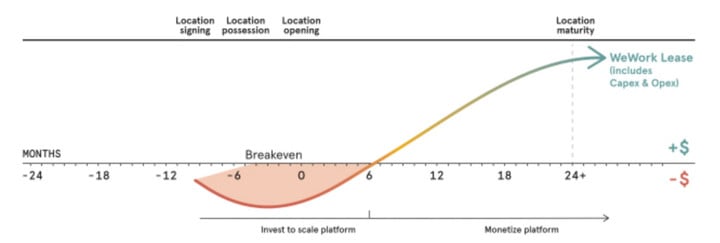

Considering this prospect, at least in theory, WeWork’s huge losses are reasonable. However, creating a company that takes on all fixed costs to provide variable cost services to other companies means a lot of upfront investment.

Just as Amazon needs to build a data center and buy a server before selling storage and computing, WeWork also needs to set up office space before selling desktop computers and meeting rooms.

In other words, if WeWork doesn’t have a huge loss, it will have a rapid expansion, which will be very strange. From its prospectus document:

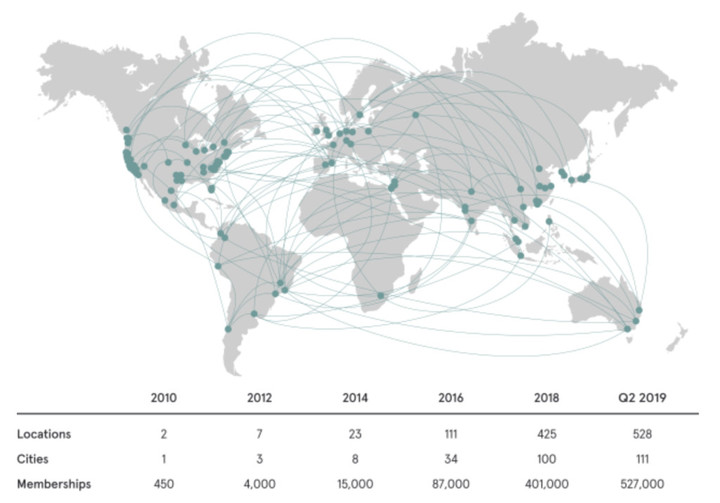

▲ WeWork’s aggressive growth rate

This company also gives such a chart, but because of the lack of the y-axis, it is not particularly useful to look at it alone:

However, it’s useful to put these two figures together: more than 300 office spaces (more than half) in the second picture are at a loss, which helps explain why WeWork’s “cost” is almost its income. Twice. If the company stops opening new office space, it seems reasonable to expect this gap to shrink rapidly.

However, considering whether WeWork’s view of the entire target market, whether the company will reduce the speed of opening office space is still questionable. It wrote in the prospectus:

As of June 1, 2019, we have offices in 111 cities and we estimate there are approximately 149 million potential members. For US cities, we define potential members by estimating the number of jobs (posts) that need to be done in the office based on US Census Bureau statistics.

For non-US cities, we believe that any of the professions identified by the ILO, including managers, professionals, technicians, assistant professionals, and clerical support, are potential members because we believe these people A work space with a desk and other services is required.

We believe this is our target market because our members have a wide range of expertise from all walks of life and our solutions are available to different types of individuals and organizations. We will also develop new solutions based on the needs of our members.

We expect to expand in existing citiesZhang, and conduct business in as many as 169 other cities. We assess whether to expand in a new city based on multiple criteria, primarily to assess the needs of potential members and the strategic value of the entire city as part of our portfolio of coverage areas.

Based on data from the Demographic Statistics and Organisation for Economic Co-operation and Development, we identified market opportunities for 280 target cities, with an estimated total potential membership of approximately 255 million.

Applying the average revenue generated by each of our WeWork members for the six months ended June 30, 2019 to the 149 million potential members of our existing 111 cities, we estimate the target market The opportunity is $945 billion.

With a total of 255 target cities in the world, our potential members have a total population of approximately 255 million, and we estimate a potential market opportunity of $1.6 trillion.

Have you seen it? Wework treats almost every work in the office in the world as its own market. By definition, this move means that it will go beyond the real estate company. The following content also comes from the prospectus:

Our membership service is designed to meet the different space needs of our members. We offer standard, configurable and on-demand membership. We also offer Powered by We, an advanced solution that is configured and deployed at the organization’s location for your organization’s needs.

Beauty and optimize existing workplaces by leveraging our analytical, design and delivery capabilities while also providing organizations with an efficient option. The technologies we deploy include software and hardware solutions that provide employees with better insight and an easier-to-use workplace experience.

This ambitious scale is once again reminiscent of AWS. In 2013, Amazon management stated for the first time that AWS may eventually become the company’s largest business. At the time, AWS accounted for only 4% of Amazon’s overall revenue (but a profit share of 33%).

By 2018, AWS has grown by 1000%, accounting for 11% of Amazon’s total revenue (and 59% of profits), and this share is expected to grow even if AWS faces faster growth, such as Microsoft Azure. Competitor. This is largely because existing companies are turning to cloud computing, not just startups.

At the same time, WeWork used its broad definition of the target market to claim that it achieved only 0.2% of the overall opportunity in the world and achieved a 0.6% chance in the top ten cities.

Equitablely, people may wonder if, in particular, existing companies will hesitate to hand over the management of existing offices to WeWork, which will greatly reduce opportunities.

But on the other hand, big companies now account for 40% of WeWork’s revenue (and are still rising) and, more importantly, WeWork does not have any significant competitors.

WeWork (lack of competition)

This is a very important part of the competition and one of the more convincing reasons for the WeWork opportunity.

WeWork’s most obvious competitor is a company called IWG. By the end of 2018, the company had 3,306 office space and 445,000 workstations. In contrast, as of June 30, 2019, WeWork had 528 office spaces and 604,000 workstations.

Please note that the dates are inconsistent – this is not a perfect comparison – but this just means that these are two very different companies: By the end of 2018, WeWork had only 466,000 stations.

A year ago, when the Wall Street Journal pointed out that WeWork’s valuation was five times that of the IWG (now 13 times), WeWork had only 150,000 workstations, and the IWG had 414,000.

In other words, WeWork is much more concentrated than the IWG and grows exponentially; but the IWG is making a profit (previous year: £154 million).

However, this further illustrates one point: IWG is limited by income, both good and bad; on the other hand, WeWork is perhaps the easiest to understand as aIt seems that the obvious beneficiaries of the world with unlimited capital.

In the long run, it’s hard to see the IWG’s competitiveness. Frankly speaking, it’s hard to see other companies compete: who will fund WeWork’s competitors instead of simply investing more in WeWork itself. funds?

Capital and economic recession

The question of capital may be the biggest problem facing WeWork: From the beginning of the company’s establishment, the industry insiders (very) wanted to know what would happen when the economy was in recession.

When the economy grows, it is one thing to sign long-term leases at low prices and rent office space at high prices; when the economy is in recession, there is no progress in obtaining long-term lease contracts, and WeWork customers are likely to have nowhere to go. What happens when I go?

This is a reasonable concern, and it is almost certain that this is the biggest reason we are skeptical about WeWork in the short term, but this company has reason to refute:

First, WeWork believes that in times of economic downturn, increased flexibility and lower costs (as opposed to traditional office space) may actually attract new customers.

Second, WeWork claims that its growing corporate customer base has nearly doubled its leasing commitments to 15 months with a corresponding revenue of $4 billion; although this is much shorter than WeWork’s prevailing 15-year lease But perhaps enough to keep the company stable during the recession.

Third, WeWork points out that if the company has sufficient capital, the recession will actually accelerate it as the cost of leasing and construction declines.

The company has another “worry” advantage in the recession: an opaque corporate structure.

Although “We Company” is a collection of entities, this fact has many shortcomings. However, one of its biggest benefits is that it is difficult for the landlord to enforce the lease commitment for any lease that WeWork has given up. The British “Financial Times” reported that:

The landlord has limited things to do in order to enforce lease commitments. Like other companies in the shared office sector, the company created a special purpose vehicle for its lease, which means that if the parent company is unable to pay the rent, the landlord has no direct recourse.

In the past, companies in the industry changed lease terms when the economy was in a downturn. Regus, now the IWG, renegotiated the lease when the tech bubble burst in 2002. Recently, a subsidiary of the IWG rented a site near London Heathrow Airport to apply for voluntary liquidation.

In response to these concerns, WeWork has provided guarantees for some of its rental payments, although this is only a small part of the overall debt. WeWork at IP