The Fed has started an aggressive rate hike cycle.

At 2:00 am Beijing time on May 5th, the Federal Reserve will announce the May interest rate decision, and then Fed Chairman Powell will hold a press conference at 2:30.

The market generally expects the Fed to announce a 50 basis point interest rate hike and announce a plan to shrink its balance sheet. Affected by this, U.S. bond yields rose further. The 10-year U.S. bond yield once exceeded 3%, the first time in 3.5 years; the U.S. dollar index also climbed to a 20-year high, hovering at a high of 103, and non-dollar currencies fell across the board; global stock markets generally declined.

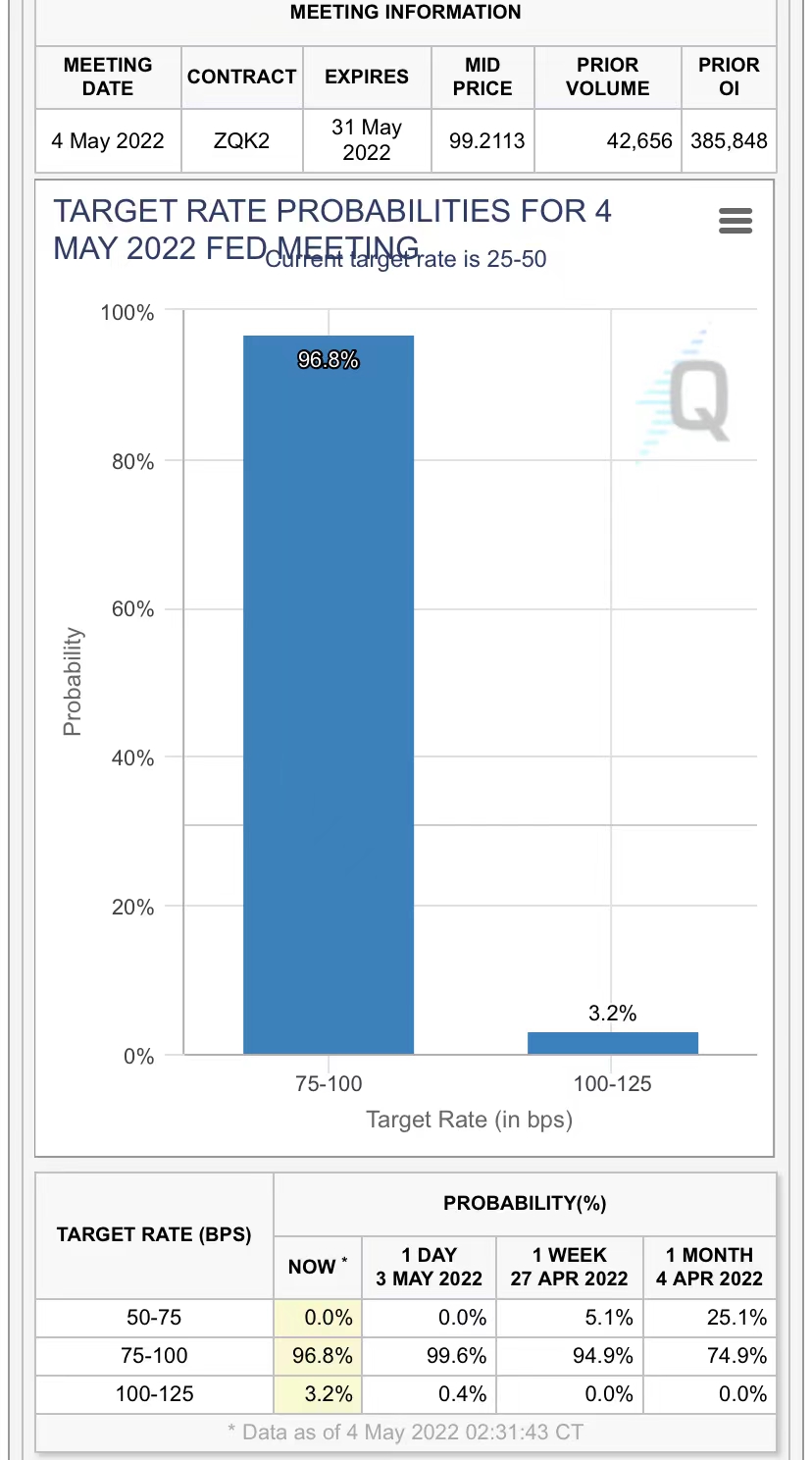

CME Group’s Fed Watch tool, FedWatch, recently showed that the market generally expects a 96.8% chance of the Fed raising interest rates. It also means the market has almost fully priced in a 50 basis point rate hike from the Fed.  Point 1: Next, add How will the information path be interpreted?

Point 1: Next, add How will the information path be interpreted?

At its March meeting, the Federal Reserve announced a 25 basis point increase in the target range for the federal funds rate to between 0.25% and 0.5%. It was the first rate hike by the Fed since December 2018.

At the upcoming meeting on interest rates in May, the Fed is likely to raise interest rates by 50 basis points, which will be the first time since 2006 that the Fed has two consecutive policies The meeting raised interest rates. The 50 basis point rate hike would also be the first since 2000, while the last 75 basis point hike dates back to 1994 during the Greenspan era.

Nomura Securities global head of macro research Su Bowen (Rob Subbaraman) told the news that in the next three meetings, the Fed is expected to raise interest rates by 50 basis points. Then add 25 basis points over the next 3 meetings. Nomura expects the Fed to raise rates by a total of 225 basis points between now and the end of the year.

The Swiss Pictet Wealth Management team expects the Fed to raise interest rates by another 50% at its May and June policy meetings due to concerns about continued wage increases and further spread of inflation. bps, while July reverted to a 25 bps rate hike. The Fed may be more flat in the second half of the yearThe pace of rate hikes continues, with 25 basis points at every Fed meeting, regardless of economic data.

Zhongjin Macro reminded that it is necessary to pay attention to whether Powell will consider a one-time interest rate hike of 75 basis points. At the press conference after the last March meeting, Powell’s attitude was relatively moderate. On that day, US stocks rebounded positively. However, the good times did not last long. In the next speech, Powell’s attitude quickly turned eagle, and US stocks continued to suffer setbacks.

Zhongjin Macro speculates that even if Powell is mild this time, his remarks will be discounted. On the contrary, if Powell continues his previous attitude at the IMF annual meeting, or even rejects the option of a one-time rate hike of 75 basis points, it will be interpreted by the market as a hawkish signal.

However, Kristina Hooper, chief global market strategist at Invesco, pointed out that the market should not fear the Fed’s aggressive rhetoric, but should welcome them; hawkish speech can help the Fed take on the heavy responsibility . And can shape consumer psychology around inflation. The Fed and other central banks can use this to arrange a soft landing and avoid a recession.

Aspect 2: When will the table be reduced?

The minutes of the Federal Reserve’s March meeting showed that meeting participants agreed that rising inflation and tight labor market conditions were evidence that the upcoming meeting It will start shrinking its balance sheet on 2017-2019 at a faster pace than in the 2017-2019 period. Participants generally agreed that the balance sheet would be reduced by as much as $95 billion a month, including $60 billion in Treasury bonds and $35 billion in agency debt. Participants also generally agreed that the cap could be phased in over a period of three months or a little longer if market conditions required it.

Zhongjin Macro believes that compared with raising interest rates, the uncertainty of shrinking the balance sheet is greater, and the market may be too concerned about raising interest rates, thus ignoring the importance of shrinking the balance sheet . The essential difference between raising interest rates and shrinking balance sheets is that the former is a price tool, while the latter is a quantitative tool. The probability of raising interest rates can be determined by the interest rate market. Investors can track interest rate hike expectations in real time, but shrinking balance sheets cannot. No indicator can. It clearly reflects the market’s expectation of the decline in liquidity caused by the shrinking of the balance sheet. In addition, the price of financial assets in the United States has risen sharply in the past two years, and the rise in housing prices and inflation is closely related to the over-issue of money (quantitative monetary expansion). If the quantity of money starts to contract, asset prices, house prices and inflation will all suffer. Especially for financial asset prices, because financial markets have nonlinear characteristics and are prone to herding effects, the marginal change in liquidity is morePhysical assets are more sensitive. Investors should pay attention to this, and cannot simply assume that asset prices were stable at the beginning of the last round of balance sheet reduction, and this time they can rest easy.

Aspect 3: Will there be a recession?

At the last meeting in March, Powell had been emphasizing that the U.S. economy was very strong, but the U.S. first-quarter GDP data released last week surprised the market .

On April 28, Beijing time, data released by the U.S. Department of Commerce showed that the U.S. gross domestic product (GDP) in the first quarter of 2022 unexpectedly fell by 1.4% year-on-year. , is expected to grow by 1.1%, compared with the previous value (Q4 2021) of 6.9%. It marked a sudden reversal of the U.S. economy from its best performance since 1984.

Koo Chaoming, chief economist at Nomura Research Institute, told the news that a slowdown in the U.S. economy is possible, but not a recession. In other words, compared with the 6.9% GDP growth in the fourth quarter of 2021, the growth rate will slow down, which is necessary to curb inflation. In the next few months to a year, the market may fluctuate, and the stock market will decline to a certain extent. Once the Fed has the upper hand on inflation and the medium- and long-term conditions are under control, optimism about the U.S. economy can be maintained.

The Pictet Wealth Management team expects that the current rate hike may take a toll in the future. U.S. economic growth is set to slow this summer due to rising interest rates and waning fiscal policy support, when the Federal Reserve is likely to pause its tightening policy. When economic growth momentum slows, the housing market may bear the brunt. But there will be no recession in the second half of the year, and it has fine-tuned its full-year 2022 U.S. GDP growth forecast to 3.0% from 3.2%.

Zhongjin Macro emphasized that this time Powell’s views on the trend of the U.S. economy have changed, and how he understands the relationship between monetary tightening and economic recession is worth paying attention to. It remains to be seen whether the slowdown in the economy, for example, will act as a constraint on the Fed’s monetary tightening.