Think about it.

Editor’s note: This article is from the WeChat public account “personal T-user” ( ID: Java_simon), author Zhang Suyue.

There is research data showing that the average life expectancy of entrepreneurial companies is less than three years. This shows that some startup companies can’t afford this average time. So, how do they do for companies that have survived the catastrophe?

The answer is that startups need to act quickly and create new things. Of course, if it accepts the external investment of venture capitalists, then it must also grow rapidly and eventually find a way out. After all, they are responsible to investors.

For VCs, the ultimate liquidity is achieved in one of several ways. If the companies they support are temporarily privatized, then early investors may choose to cash out through the secondary market or make further offers through a well-funded buyer. For example, in January 2018, Softbank and a consortium of other investors bought $9 billion worth of Uber stock from employees and early investors. However, not all startups are as concerned as Uber, and because these transactions involve private company stocks, they are rarely disclosed.

The most intuitive and direct way for startup stakeholders (including investors, founders, and shareholding employees) to gain liquidity is through one of two exit paths. In mergers or acquisitions (M&A), the acquirer buys shares in the startup, usually in cash or stock. In the case of an initial public offering (IPO) or direct listing, the company changed from private holding to public listing, subjecting it to additional regulatory scrutiny, as well as the speculations of retail and institutional traders.

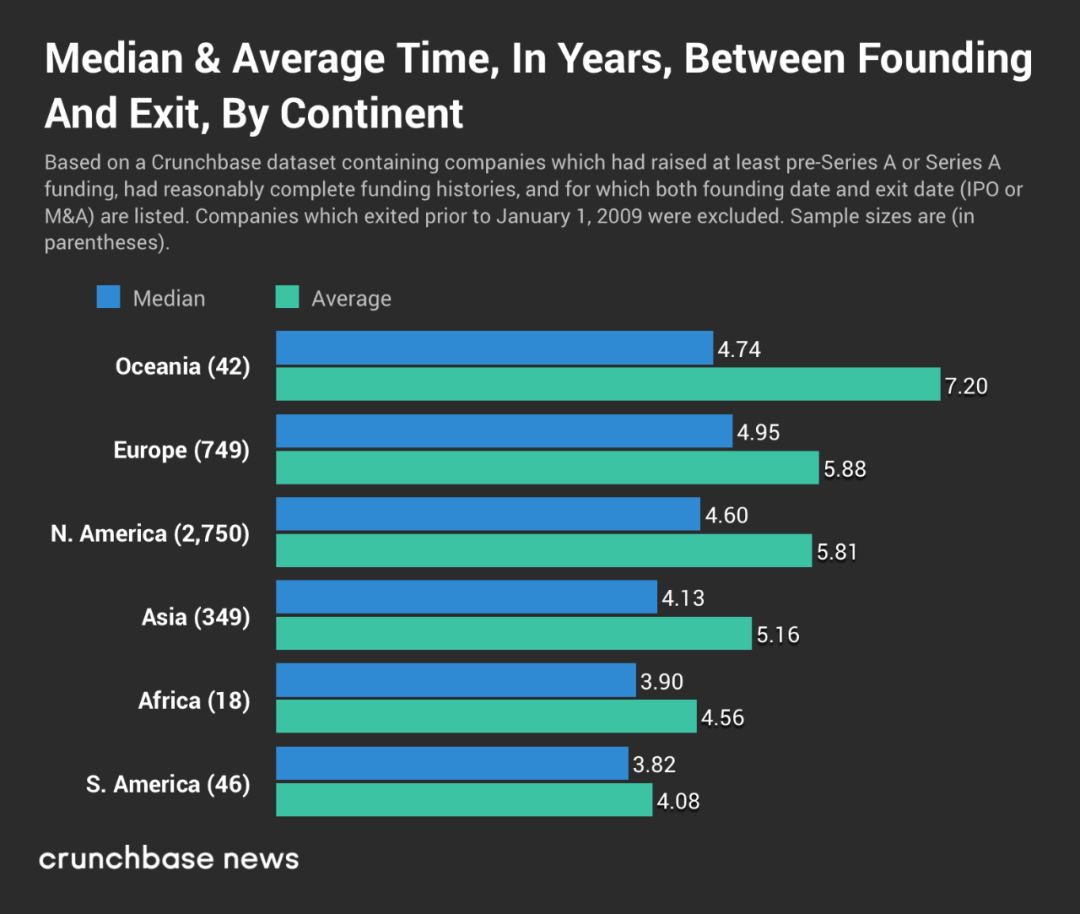

Although each company is unique, they are still subject to local market conditions. The length of time from the establishment of a start-up to the exit through an IPO or merger will vary from region to region. Through a survey of thousands of venture capital-backed startups around the world, we found that exit times vary widely, depending on a variety of factors.

VC Fund Operation Time

Once a company gets external financing from venture capital, time will be tight. This is true at least in the United States, where most venture capital funds operate for 10 years. Of course, there are many exceptions and contract terms that can be used to extend or shorten the period of a particular fund, but in general this is the case.

From a new fund, a company may get new funding in the first one to three years. General partners and their partners will help their new portfolio companies grow in the next few years (and prepare follow-up inspections)Check), through the board of directors for governance, risk management and consulting roles. They then reap the capital gains in the last few years and return those proceeds to the limited partner, extracting a portion of the profits from the usual spin-offs of the general partner.

Therefore, the life cycle of venture capital funds determines the rhythm of their portfolio startups.

Regional differences

In the chart below, we plotted the average time and intermediate time between the date of the establishment of a company and the date of listing or acquisition. We used a relatively limited data set and used a similar approach to last year’s valuation multiple analysis. We limit our research to companies that have at least pre-A round financing (pre-seed, seed round, angel round or corresponding round) or Series A financing. However, companies that do not have venture capital support, whose known financing history begins with the B series or later, and companies with large gaps in financing history are excluded.

We noticed that the sample sizes shown in parentheses vary widely. The average is also very different. Especially in the case of small sample sizes, outliers (in which case the company spends a very long time, or find an exit in a very short time) may distort the average.

However, we have found a general trend: start-ups in developed economies have a slightly longer life cycle than emerging economies. Although there is not enough data to determine whether the investment capital of emerging economies can produce a better multiple (calculated by dividing the terminal valuation at exit from the equity raised). Crunchbase News’ previous analysis showed that companies with early exits (whether in the financing phase or in the market) have higher investment capital (MOIC) P/E ratios. Other analyses we have done also show that companies with less financing typically produce better MOICs than VC-backed companies with relatively abundant funds.

What is driving this trend?

What caused the time difference from one area to another? It’s hard to say from a numerical perspective alone. However, we believe that there are some possibilities to explain.

First of all, we can’t rule out that this is the illusion caused by sampling bias. Because in the United States and Europe, where the performance of our filtered data sets is good, the scenarios of start-ups are more mature, so more companies are investing more time in the market before they are acquired or listed. In South America, especially Brazil, venture capital-backed entrepreneurship is a relatively newThe phenomenon. In emerging markets, the average age of all operating private companies may be younger, which may affect our results.

The stronger capital market in developed economies is likely to keep companies private for a longer period of time. This is also true for the IPO market. The surge in venture capital and private equity investment in the near future will bring capital on a scale of IPO without having to bear the regulatory burden and market risk of the actual city. But the ability to continue financing may also extend the time of mergers and acquisitions. As more venture capital can be used to help companies grow independently, the incentive to integrate into a larger company through mergers and acquisitions will diminish.

There is no doubt that there are many other explanations for this high level trend. Excavation on a national basis may expose more features. For example, one country may deregulate public offerings (IPOs) while another country may maintain stricter regulation of M&A transactions. However, on the whole, our data show that there are differences between the regions of the developed economies and the regions that are mainly emerging economies, albeit to a small extent.

In this way, companies are living fast in a wind-supported economy, but there are also speeds.

So, in general, in addition to the impact of the survival time of entrepreneurial enterprises, some external factors have also played a role in fueling the situation. However, in essence, can you really meet the needs of users, and why should companies that are recognized by users always worry about their own risks? !