From the perspective of opening stores in the third quarter, fast fashion is rising in low-tier cities…

Editor’s note: This article is from WeChat public account “to win business network” (ID: winshang), author: Lu Zhizhen.

From the opening of the store in the third quarter, fast fashion is rising in the low-end cities…

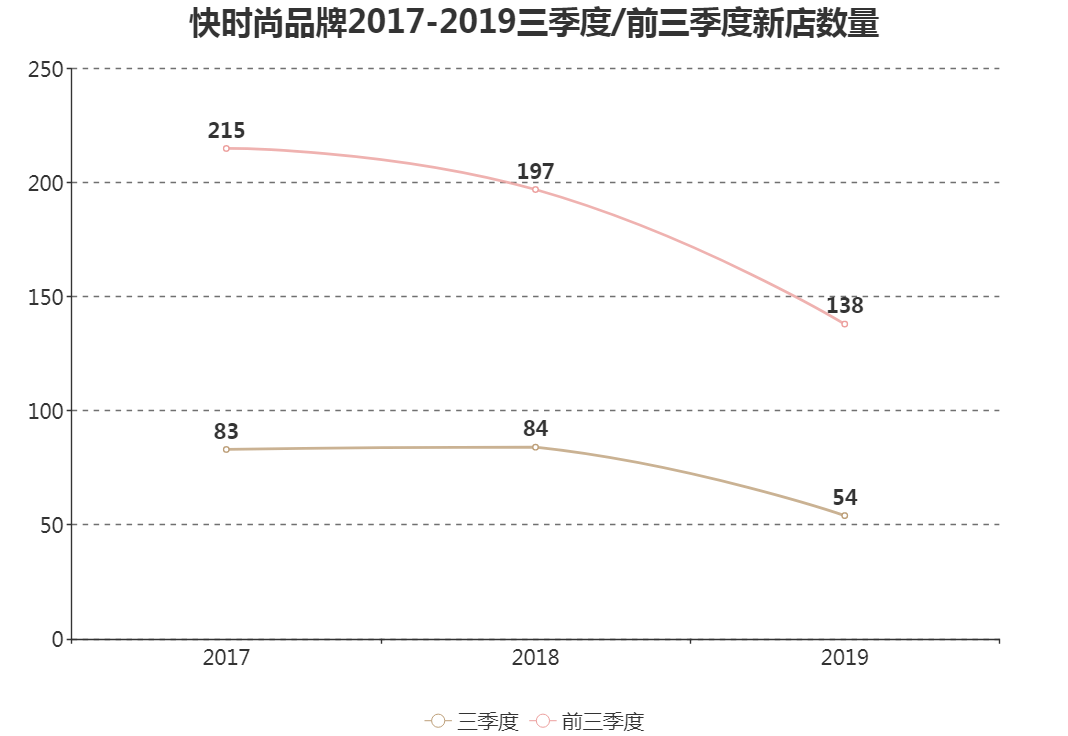

According to the incomplete statistics of Winner.com, including H&M, ZARA, Uniqlo, MJstyle, MUJI, UR, C&A, GAP Within the eight fast fashion brands, a total of 54 stores (excluding upgrades and reopened stores) were added in the Mainland in the third quarter, a decrease of approximately 36% compared with the same period last year. (Detailed expansion form at the end of the article)

Data Source: Public Data Mapping: Winner Network

A total of 138 stores were added in the first three quarters of this year, a significant decrease over the past two years. The fast fashion brand stayed in the “peak period” of the staking in the Mainland in 2017, and then contracted the pace of expansion.

Today, the domestic fast fashion pattern has undergone tremendous changes. The three international fast fashion giants, Uniqlo is still triumphantly, covering 160 cities in Huamen store; ZARA is still “chronic”, the new store is growing in single digits; H&M expansion seems to be somewhat powerless… GAP, MUJI, UR and other store strategies Gradually change.

01Fast fashion collective slowdown, Uniqlo “a ride on the dust”

Data Source: Public Information SystemFigure: Winners Network

In terms of brands, The second quarter of UNIQLO opened 22 new stores, this is the only brand in this season that broke the double-digit number of new stores.

The rest of the brand new stores are in single digits. Domestic brands UR and American old GAP are tied for second place with 8 new stores; MUJI, H&M and MJstyle are closely followed, with 6 new and 4 new ones respectively. 3 stores; C&A, which has been quiet for a long time, has added 2 new ones in the third quarter; there is only one new ZARA store.

Data Source: Public Data Mapping: Winner Network

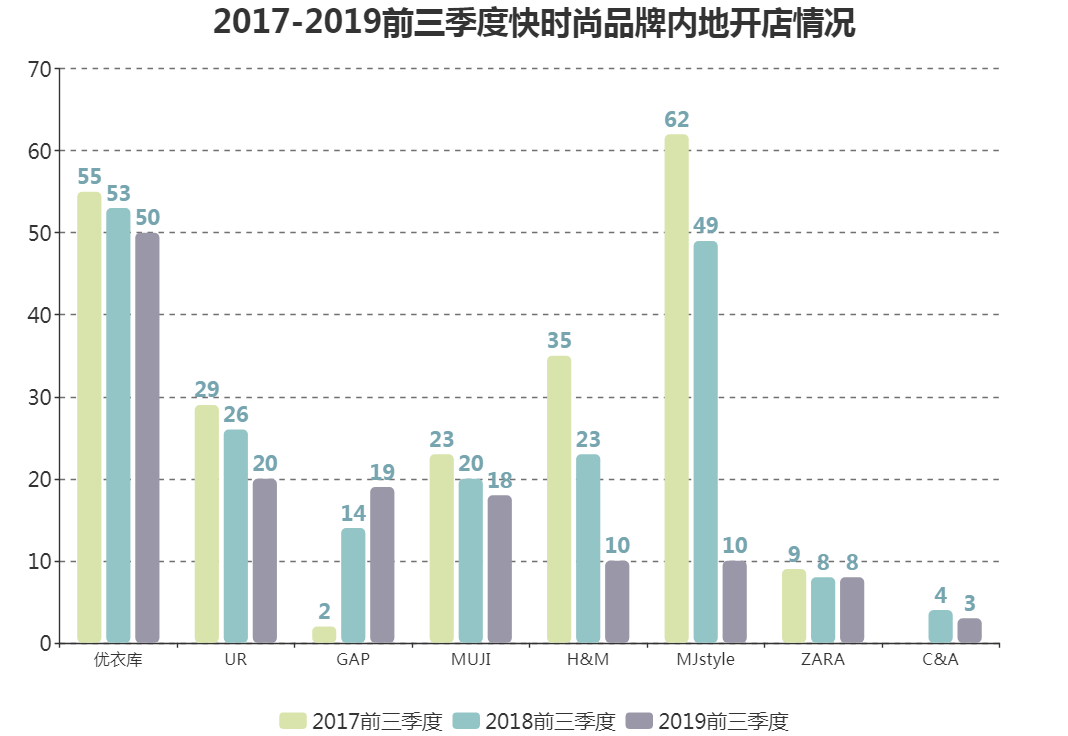

In the first three quarters of this year, the largest number of new stores was Uniqlo, a total of 50, and the distance from the second UR20 was far. From the first three quarters of 2017-2019, The number of new fast fashion brands in the Mainland is declining, where:

-

International fast fashion giant Uniqlo and ZARA are relatively stable, the former maintains more than 50, the latter has not broken through 10;

-

H&M is left behind, only 10 new stores in the first three quarters of this year, compared to last year’s “waist”;

-

The two domestic brands UR and MJstyle are shrinking and expanding;

GAP is the only exception, contrarian expansion, from 2 new stores in the first three quarters of 2017 to 19 in 2019, surpassing MUJI, H&M, etc. the third. As of the end of September, GAP Greater China stores have exceeded 200.

02The rise of the low-line city, Wanda Plaza became “Xiangxiang”

From a regional perspective, the fast-growing new stores in the third quarter are still mainly located in the East China region, a total of 16 companies, accounting for nearly 30%, mainly in Jiangsu, Zhejiang and Shandong. Among them, there are 6 Uniqlo, H&M3, GAP, Muji, and UR each.