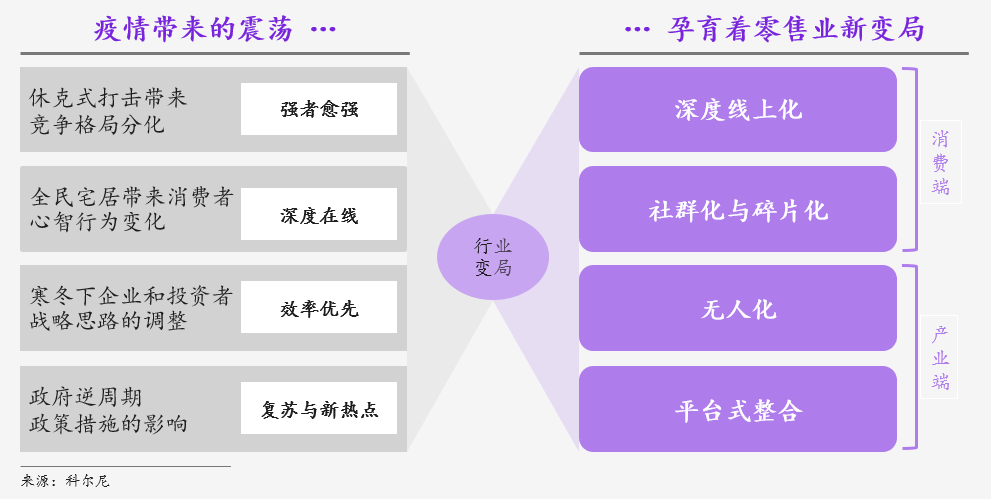

Within 1-2 years after the end of the epidemic, the retail industry will accelerate its evolution in four directions: deep online, community and fragmentation, unmanned, and platform integration.

Editor’s note: This article is from WeChat public account “ China-Europe Business Review ” ( ID: ceibs-cbr), editor: He Xiaoqing, Si Yujie

The new crown pneumonia epidemic during the Spring Festival of 2020 affects the hearts of hundreds of millions of people. The state has adopted strong anti-epidemic measures, and counter-cyclical policies for subsequent economic recovery have also been introduced. The current public opinion generally believes that the impact of the epidemic on the economy will be concentrated in the first quarter, which is prominently manifested in the collective “shock” of the retail, catering, and tourism industries under isolation and control measures.

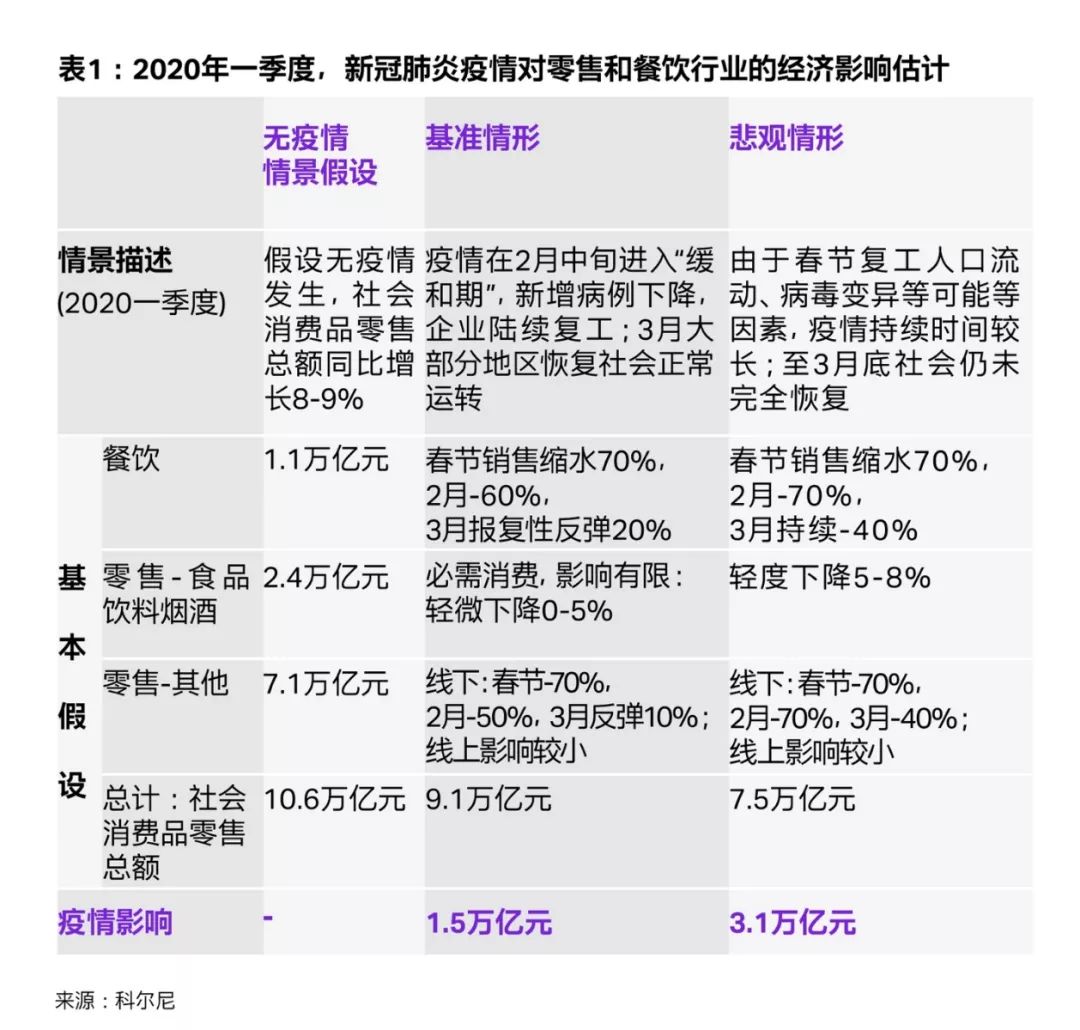

Kearney’s preliminary estimate is that in the first quarter, the epidemic will cause economic losses of 1.5-3 trillion yuan to the retail catering industry. (See below for details)

01 The retail industry has become the hardest hit area

The retail industry is the hardest hit area of the epidemic, and its impact on various business types and categories is different. Overall, there are three major impacts:

First, online influence is weaker than offline, and fresh e-commerce has become “critical” to “opportunity.” From the closure of the city to the closed management of the community, under the epidemic situation, “isolation at home, no action if you can’t move” has become a necessary measure to prevent and control the epidemic, and enterprises have also delayed the resumption of work or opened a remote office model. Due to restricted travel, offline purchase demand began to flow online.

The major e-commerce platforms have recorded significant sales growth in the people’s livelihood category; fresh e-commerce has ushered in a breakthrough-“takeaway families” are forced to buy food and cook, and elderly people who cannot go out also start to grab food online; O2O, Communities and live broadcasts have become self-help means for offline stores. After the epidemic, e-commerce is expected to further increase the total retail sales of consumer goods from 21% to 24% or higher.

Second, the near field suffers less than the far field. At present, for near-field formats such as supermarkets, convenience stores, and community fresh stores that are close to the community, the core demand for fresh products and daily necessities is still strong, and the negative impact mainly comes from the cost of some policy-based store closure requirements and epidemic prevention measures Up; while far-field formats such as shopping malls, department stores, specialty stores, and catering are generally “shocked”, and the cash flow crisis is serious. Due to the requirements of the epidemic prevention policy and the “zero return” passenger flow in business districts, shopping malls across the country have closed in large areasTo this end, nearly 80 commercial real estate operators, such as Wanda and China Resources, have taken measures to reduce rents.

Third, large platforms are more resilient than small platforms. In the face of epidemic response speed, scheduling capacity, and operational flexibility, large platforms show stronger advantages. For example, the fresh food e-commerce business is increasing rapidly, and it is also facing a bottleneck in operating manpower. Ali Hema and Jingdong Qixian mobilized the rich manpower of the catering company. Such as the daily excellent fresh, Dingdong shopping for food does not have such a large platform to move space; smaller platforms such as staying radish, during the Spring Festival did not organize self-promotion points to resume work, missed a wave of window opportunities. Seeing the general situation from the slightest, after the epidemic, the industry reshuffle will be more violent.

02 Four major changes in the retail industry after the epidemic

Looking longer term, this winter “black swan” may have a far-reaching impact on the industry. Four factors will drive the change of the industry: (1) the shock of shocks will lead to a differentiation of the competitive landscape-the stronger the stronger; (2) the residential homes bring changes in consumer mental behavior-in-depth online; (3) companies under the cold winter And adjustment of investors’ strategic thinking-efficiency first; (4) the impact of government counter-cyclical policies and measures.

Combining the derivation of these four factors, combined with the front-line retail feedback from the outbreak, Kearney believes that after the epidemic, that is, within 1-2 years after the end of the epidemic, the retail industry will accelerate its evolution in the following four directions:

Deep online. The “last moat” of offline retail represented by fresh produce was conquered, the market was deeply baptized, and the demand-side bottleneck of further expansion of e-commerce was broken. But operational efficiency issues are becoming increasingly prominent.

Community and fragmentation. The “O2O + community” has become a means of self-rescue for offline stores in the midst of the epidemic, with small programs, live broadcasts, and short videos showing their magic. The community traffic spontaneously organized by massive offline stores has exacerbated the fragmentation of consumption scenarios.

Unmanned. After the baptism of the epidemic, consumers ’psychological barriers to unmanned services have been broken, and companies are increasingly concerned about operational efficiency. The combination of the two parties will open up many application scenarios of unmanned technology in the front-end and back-end of retail.

Platform integration. The difficult environment in 2019 is superimposed with the current epidemic situation, and small and medium-sized retailers are in serious crisis and face a round of reshuffle. Large platforms such as Ali, Meituan, JD.com, and Suning have demonstrated extremely high mobilization capabilities and technology-driven advantages in the crisis. On the one hand, they better meet the challenges of the supply chain and achieve development in adversity;Ecology merchants have played a role of “buffering and earthquake resistance”, and their attraction to merchants has increased.

The stronger the stronger, the larger the platform will be more able to survive and grow in a crisis, and the large ecosystem will accelerate the acquisition of small chains and independent stores in a platform mode.

Change one: online in depth

Under the national house, many user scenarios that have been difficult to go online for many years have opened up breakthroughs overnight, such as online education, online medical care, and remote office. In the retail sector, fresh food has always been the last moat for offline retail. Generations of fresh food e-commerce have sought for years. Some market segments, such as the positioning of high-end Hema models, have been verified, but fresh food e-commerce has always been difficult to obtain. A comprehensive breakthrough across regions and scenes.

The reason is that the elderly are the main population for shopping (50% over 55 years old). They are always uneasy about buying food online, and it is more difficult to accept the new model. During the epidemic, on the one hand, the elderly were key populations for epidemic prevention and were forced to choose online, which greatly expanded the population coverage of fresh e-commerce; on the other hand, the young and middle-aged people were trapped in their homes, and the demand for meals and takeaways were usually directed. When shopping for food and cooking, the demand of existing electric businessmen has greatly increased. The demand-side bottleneck of fresh food e-commerce has been broken.

During the Spring Festival Anti-epidemic period, all major fresh-food e-commerce merchants recorded sales doubles: Hema Fresh’s daily sales in mature markets doubled year-on-year; year-on-year sales of Fresh Spring Festival doubled; The customer unit price has increased from 55 yuan to 90 yuan; the daily sales of Suning vegetable market have reached 6-8 times before the festival; the average daily order for Meituan to buy vegetables is 2-3 times before the festival. Each platform also recorded new user growth, including many elderly people, and fresh food e-commerce began to penetrate the core population of the fresh food category.

However, as the bottleneck on the demand side breaks through, the pressure on the e-commerce operator’s side stands out. Under the surge in demand, shortages and shortages of sorting and distribution manpower are common. The fresh food shortage problem is affected by the objective factors of the Spring Festival holiday and epidemic prevention traffic control, which is universal. However, from the field survey, the shortage of e-commerce is more severe than that of offline supermarkets and community fresh stores, reflecting that bothLevel differences in deep cultivation of the supply chain. While going online, online pioneers have a lot to learn from traditional retailers.

In fact, after experiencing a shortage of goods during the Spring Festival, Hema is already thinking about this. At present, Hema’s fresh products are entrusted to third-party suppliers or service providers, and have not yet opened up The full link from the origin to the dining table; and offline supermarkets such as Wal-Mart and Yonghui have deeper control over the upstream of the industrial chain.

In the first 10 days of the epidemic, Wal-Mart’s store availability rate could remain above 96%. Whether the two models are better or worse depends on the size of the business and the business model. However, after this round of baptism, in the early years, the fresh-water e-commerce companies who were running horses and rodeos in the early years, the supply chain and other long-term, hard work will be the main points of their re-examination.

Regarding in-depth onlineization, another noteworthy issue is that for most categories, the profit margin of online operations is lower than offline operations. In addition, during the epidemic, the major platforms insisted that the prices of the goods did not increase sharply, the logistics distribution parity, and the pressure on profits was huge, despite the significant increase in supply side and logistics costs. Offline consumption flows online, and when the incremental effect is not obvious, it is a big challenge for the profit pool of the entire value chain.

Change two: community and fragmentation

During the Spring Festival epidemic, many far-field formats such as department stores, shopping malls, and specialty stores closed, and the “O2O + community” became a means of self-help for offline stores. The CEO of cosmetics brand Lin Qingxuan wrote in a circle of friends that during the epidemic, although more than 30 stores in Wuhan were closed, more than 100 shopping guides in these stores moved to the community during the closure period, which actually made Wuhan’s sales performance top Second in the country.

During the epidemic, Suning, the nation ’s largest home appliance chain, guided thousands of home appliance stores in China to turn to “out-of-store sales” and launched community sales based on member data. Sportswear Lululemon has moved its offline yoga classes online to launch live broadcast classes. Shopping malls under Joy City, Long Lake, CapitaLand, etc., establish a group with merchants and continue to sell through public account and WeChat group push. And more small and medium-sized retail enterprises and stores have also widely adopted live broadcast and short video selling methods to survive adversity. It is expected that these measures will also become routine operations in stores after the epidemic.

Unlike the social e-commerce boom set off by Pinduoduo last year, this round of community selling is decentralized-traffic is decentralized and operated by massive offline retail stores, Different implementation methods (public account, WeChat group, short video, live broadcast, etc.); fulfillment is also decentralized, and can be traded through the store’s own mini-programs and distributed at local stores, without necessarily going through a centralized e-commerce company such as Tmall. platform.

In fact, prior to the epidemic, this type of transaction model already existed widely in grassroots economies and had a broad base of user bases (for example, many small fresh communities in small communities have a regular customer base of 100-300 people, Order in the group and deliver to your door). Under the influence of the epidemic, moreMulti-scale retail companies join the ranks.

This will have a profound impact on two levels:

First, the transformation of offline stores will further intensify. Stores will no longer be the center of transactions, but will become part of the “O2O + community” transaction chain.

Second, the traffic acquisition methods and transaction links are more fragmented. When it comes to traffic acquisition, the store operates communities that show their magical powers and are deeply integrated with social and content (WeChat groups, circle of friends, live broadcasts, short videos, etc.). On the transaction link, brands and retailers can rely on small programs to build their own closed-loop transactions, which is a potential threat to traditional centralized e-commerce platforms. Although mini-program e-commerce has existed for many years, this wave of offline store self-help has provided it with a wider range of application scenarios.

Change three: unmanned

During the anti-epidemic period, users are very sensitive to interpersonal contacts, and they have concerns about taking out food and express delivery. At the policy level, the development of smart express counters is one of the officially encouraged epidemic prevention measures. In Wuhan, are you hungry? Cooperate with community convenience stores to set up fresh convenience convenience pick-up stores to encourage pick-up in the community. After this round of “contactless” experience, consumers’ acceptance of unmanned services has greatly improved.

During the epidemic, among the fresh-food e-commerce companies, Suning Vegetable Market, which mainly focuses on self-picking mode, has doubled its users in Nanjing and Shanghai, with daily sales reaching 6-8 times before the Spring Festival.

Furthermore, after the widespread popularization of centralized express counters and pick-up points, it has created favorable conditions for the further expansion of “unmanned delivery” in the true sense. Under the traditional delivery-to-home model, delivery requires passing through building access and taking the elevator through several levels, which are all challenges for intelligent robots. (The food delivery robots currently used in hotels are connected with hotel elevator systems and room call systems; but Large-scale residential buildings obviously cannot achieve full docking with robots).

But if the last mile delivery is from the courier point to the centralized pick-up point, the difficulty of unmanned operation will be greatly reduced. In Wuhan, where the epidemic is most severe, JD’s intelligent distribution robot has completed the first order for unmanned distribution for Wuhan Ninth Hospital.

The special period of the epidemic also amplifies the efficiency bottlenecks of retail companies in the supply chain and logistics, and the shortage of sorting and distribution manpower. More and more companies are deploying unmanned technology to improve efficiency. For example: JD Logistics has launched a sorting robot on a large scale. Meituan is also accelerating the research and development of unmanned “micro warehouse” to optimize the door-to-door picking process.

Facing the expectations of the economic cold winter, the above unmanned application scenario may become a great tool for retail companies to improve efficiency and protect profits. The popular express delivery and take-away self-collection model, although sacrificing service levels to a certain extent, is far more economical than the traditional home-to-home model, providing a solution for the high e-commerce logistics costs. In the back-end operation scenario, the automatic picking shelves and automatic conveying equipment are becoming more mature, and the willingness to popularize enterprises that urgently need to reduce costs and improve efficiency is increasing.

Change four: platform integration

The retail environment in China in 2019 is already difficult. In addition to the impact of the epidemic, a group of small and medium-sized enterprises will fall in this cold winter. And, in the first two years of the new retail boom, many start-ups have been running for real with money raised from financing. After the epidemic, the capital circle will not underestimate the negative impact of the epidemic on the economy, and investment will be more cautious. Startup financing will be more difficult, accelerating the reshuffle of the industry. It is expected that the turbulence of heavy asset tracks such as restaurants and convenience stores will be particularly severe.

On the other side, large platforms have demonstrated extremely high mobilization capabilities and technology-driven advantages in the epidemic crisis, which has enabled them to better grasp this window and turn them into “crisis” and “opportunity” in their business growth. , Making progress in customer acquisition and sales. In addition, large platforms often have a wide range of services. Users acquired during this particular period of time, especially fresh users, can be transferred across categories and cross-industry within the ecosystem, which greatly enhances the value of the customer base.

More importantly, for the merchants in the ecosystem, the strong resources and technical capabilities of the platform have also played a role of “buffering and earthquake resistance”: Meituan provides a package of measures to help catering merchants develop takeaway businesses, and United Bank provides Preferential interest rate loans. The Suning retail cloud platform quickly organized more than 5,000 franchised individual store owners in its Guangbu County to expand community-based out-of-store sales. Some store owners were able to achieve 30-80% of sales during the anti-epidemic closing period, supporting the store’s Daily costs.

After this campaign, the basic role of large platforms in the business ecosystem has become more prominent, and the value of “empowerment” has been reflected. Traditional formats, small chains, and self-employed people are more willing to join the large platform ecosystem and develop themselves with the help of platform resources.

After the shock shock of the epidemic situation, on the one hand, industry integration is manifested as the weak being shuffled, and the stronger are stronger; on the other hand, it is also represented by the large-scale business ecosystem’s platform-type consolidation of traditional formats, small chains, and individual stores.

03 How should retail companies cultivate their internal skills

The negative effects of the epidemic are short-term. After the epidemic, there is a high probability that a wave of consumer industryPositives-retaliatory release of backlog of consumer demand, commercial real estate rent reduction, counter-cyclical stimulus policies and measures. For companies that can survive this winter, using this campaign to deepen transformation and cultivate internal skills is particularly critical to grasping opportunities in the next few years. Three of these issues deserve special attention:

First, seize the opportunity of fragmentation of consumption, and set up own user assets as a strategic priority. At the same time that consumer behavior is deeply online, online behavior trajectories are also widely differentiated, and purchases are tied to highly decentralized content and social circles. Fragmented traffic makes it more difficult for brands and retailers to operate. This is no longer a problem that can be solved by running an online store. This is a challenge, but also an opportunity-the fragmented traffic pattern has begun to weaken the traffic monopoly of the head platform, and retail companies have a better chance to build their own user assets.

For some large and medium-sized retailers, during the epidemic, on the one hand, when they developed their O2O business by relying on head traffic platforms such as Hungry and Meituan, they felt the rules and regulations brought by the platform rules. Challenges; on the other hand, their own user platforms such as applets have also gained unprecedented development opportunities.

The establishment of own user assets will come from various fragmented channels, including stores, mini-programs, user WeChat groups, social e-commerce platforms and other platforms that enable effective user interaction, from highly decentralized content and cross-industry. Alliance, etc.

To settle these fragmented traffic and effectively establish own user assets, a series of capabilities are required, including: (1) Data capabilities—the establishment and mining of user databases (many companies currently have data, (Utilization status), cross-platform, cross-scenario operation model for tracking and analyzing user behavior; (2) content capabilities-keenly observe market trends, follow and even lead trends in content marketing; (3) organizational capabilities-internal organization in Synergy of different traffic channels and user asset channels, etc.

Second, do a good job of new user precipitation and maximize consumer value. For companies that have made breakthroughs in consumption scenarios during the epidemic, such as fresh food e-commerce, supermarket O2O, online education, remote office, etc., the epidemic-resistant campaign provides a key opportunity to educate the market and acquire new customers. It is those companies that can effectively retain new customers, increase single customer contribution, and promote user fission after the epidemic.

Just as the best e-commerce companies not only seek sales breakthroughs during the Double Eleven, they are also committed to maximizing the repurchase of Double 11 customers during non-big promotion periods. Similarly, if we broaden our perspective, in the medium and long term user operations,Volume is only the first step. Doing a good job in depositing user assets and maximizing user value is the key to the success of an enterprise.

Opportunities for maximizing consumer value include: On the one hand, the “octopus” that provides categories and consumption scenarios provides a basis for the new online fresh customers obtained this time to be able to transform in multiple scenarios. On the other hand, more accurate user tagging and continuous operations will open up users’ interactions between categories and scenarios.

Third, solid operation, internal skills, self-construction and cooperation. In the past two or three years, retail companies have talked about many new concepts and created many new models. The thinking is correct, but many companies have not laid a solid foundation for basic operations. For example, the in-depth control of the upstream supply chain and the flexibility of logistics and distribution capabilities determine the online business volume during the special period of the epidemic. It is also crucial for the continued development of the business and the user service level.

In addition, profitability is an ongoing challenge for online-oriented retailers. Especially for medium-sized enterprises, in the face of the capital winter that may deepen after the epidemic, it is important to use multiple methods to improve operational efficiency and achieve their own blood production. Lean operations, cost control, and expansion of unmanned scenarios (such as self-lifting of distribution) are all directions that can be dug deeper.

It is worth noting that “internal power” can be built by itself, or it can be mined outside. Actively establishing an ecosystem partner network and “eco-operation” capabilities, and further expanding cooperation spaces, models and partners, will enable outstanding companies to turn the tests of special periods into opportunities to enhance their long-term internal strength.

In fact, as consumer interactions become more fragmented and operations become more complex, professional service providers for various operational links have emerged as needed, from member operations and data analysis to the last mile outsourcing and “shared front warehouse” “concept. Retail companies need to plan their own capability matrix—what capabilities must be built by themselves, how to integrate the capabilities of external procurement, and where is the boundary between core capabilities and ecological sharing.

(Kearney’s consultant Shen Jiaying also contributed to this article)

Author introduction:

He Xiaoqing, CEO, Kearney Management Consulting Greater China, Head of Consumer Goods and Retail Industry

Si Yujie Senior Manager of Kearney Management Consulting Company

Kearney’s consultant Shen Jiaying also contributed to this article

Looking longer term, this winter “black swan” may have a far-reaching impact on the industry. Four factors will drive the change of the industry: (1) the shock of shocks will lead to a differentiation of the competitive landscape-the stronger the stronger; (2) the residential homes bring changes in consumer mental behavior-in-depth online; (3) companies under the cold winter And adjustment of investors’ strategic thinking-efficiency first; (4) the impact of government counter-cyclical policies and measures.

Combining the derivation of these four factors, combined with the front-line retail feedback from the outbreak, Kearney believes that after the epidemic, that is, within 1-2 years after the end of the epidemic, the retail industry will accelerate its evolution in the following four directions:

Deep online. The “last moat” of offline retail represented by fresh produce was conquered, the market was deeply baptized, and the demand-side bottleneck of further expansion of e-commerce was broken. But operational efficiency issues are becoming increasingly prominent.

Community and fragmentation. The “O2O + community” has become a means of self-rescue for offline stores in the midst of the epidemic, with small programs, live broadcasts, and short videos showing their magic. The community traffic spontaneously organized by massive offline stores has exacerbated the fragmentation of consumption scenarios.

Unmanned. After the baptism of the epidemic, consumers ’psychological barriers to unmanned services have been broken, and companies are increasingly concerned about operational efficiency. The combination of the two parties will open up many application scenarios of unmanned technology in the front-end and back-end of retail.

Platform integration. The difficult environment in 2019 is superimposed with the current epidemic situation, and small and medium-sized retailers are in serious crisis and face a round of reshuffle. Large platforms such as Ali, Meituan, JD.com, and Suning have demonstrated extremely high mobilization capabilities and technology-driven advantages in the crisis. On the one hand, they better meet the challenges of the supply chain and achieve development in adversity;Ecology merchants have played a role of “buffering and earthquake resistance”, and their attraction to merchants has increased.

The stronger the stronger, the larger the platform will be more able to survive and grow in a crisis, and the large ecosystem will accelerate the acquisition of small chains and independent stores in a platform mode.

Change one: online in depth

Under the national house, many user scenarios that have been difficult to go online for many years have opened up breakthroughs overnight, such as online education, online medical care, and remote office. In the retail sector, fresh food has always been the last moat for offline retail. Generations of fresh food e-commerce have sought for years. Some market segments, such as the positioning of high-end Hema models, have been verified, but fresh food e-commerce has always been difficult to obtain. A comprehensive breakthrough across regions and scenes.

The reason is that the elderly are the main population for shopping (50% over 55 years old). They are always uneasy about buying food online, and it is more difficult to accept the new model. During the epidemic, on the one hand, the elderly were key populations for epidemic prevention and were forced to choose online, which greatly expanded the population coverage of fresh e-commerce; on the other hand, the young and middle-aged people were trapped in their homes, and the demand for meals and takeaways were usually directed. When shopping for food and cooking, the demand of existing electric businessmen has greatly increased. The demand-side bottleneck of fresh food e-commerce has been broken.

During the Spring Festival Anti-epidemic period, all major fresh-food e-commerce merchants recorded sales doubles: Hema Fresh’s daily sales in mature markets doubled year-on-year; year-on-year sales of Fresh Spring Festival doubled; The customer unit price has increased from 55 yuan to 90 yuan; the daily sales of Suning vegetable market have reached 6-8 times before the festival; the average daily order for Meituan to buy vegetables is 2-3 times before the festival. Each platform also recorded new user growth, including many elderly people, and fresh food e-commerce began to penetrate the core population of the fresh food category.

However, as the bottleneck on the demand side breaks through, the pressure on the e-commerce operator’s side stands out. Under the surge in demand, shortages and shortages of sorting and distribution manpower are common. The fresh food shortage problem is affected by the objective factors of the Spring Festival holiday and epidemic prevention traffic control, which is universal. However, from the field survey, the shortage of e-commerce is more severe than that of offline supermarkets and community fresh stores, reflecting that bothLevel differences in deep cultivation of the supply chain. While going online, online pioneers have a lot to learn from traditional retailers.

In fact, after experiencing a shortage of goods during the Spring Festival, Hema is already thinking about this. At present, Hema’s fresh products are entrusted to third-party suppliers or service providers, and have not yet opened up The full link from the origin to the dining table; and offline supermarkets such as Wal-Mart and Yonghui have deeper control over the upstream of the industrial chain.

In the first 10 days of the epidemic, Wal-Mart’s store availability rate could remain above 96%. Whether the two models are better or worse depends on the size of the business and the business model. However, after this round of baptism, in the early years, the fresh-water e-commerce companies who were running horses and rodeos in the early years, the supply chain and other long-term, hard work will be the main points of their re-examination.

Regarding in-depth onlineization, another noteworthy issue is that for most categories, the profit margin of online operations is lower than offline operations. In addition, during the epidemic, the major platforms insisted that the prices of the goods did not increase sharply, the logistics distribution parity, and the pressure on profits was huge, despite the significant increase in supply side and logistics costs. Offline consumption flows online, and when the incremental effect is not obvious, it is a big challenge for the profit pool of the entire value chain.

Change two: community and fragmentation

During the Spring Festival epidemic, many far-field formats such as department stores, shopping malls, and specialty stores closed, and the “O2O + community” became a means of self-help for offline stores. The CEO of cosmetics brand Lin Qingxuan wrote in a circle of friends that during the epidemic, although more than 30 stores in Wuhan were closed, more than 100 shopping guides in these stores moved to the community during the closure period, which actually made Wuhan’s sales performance top Second in the country.

During the epidemic, Suning, the nation ’s largest home appliance chain, guided thousands of home appliance stores in China to turn to “out-of-store sales” and launched community sales based on member data. Sportswear Lululemon has moved its offline yoga classes online to launch live broadcast classes. Shopping malls under Joy City, Long Lake, CapitaLand, etc., establish a group with merchants and continue to sell through public account and WeChat group push. And more small and medium-sized retail enterprises and stores have also widely adopted live broadcast and short video selling methods to survive adversity. It is expected that these measures will also become routine operations in stores after the epidemic.

Unlike the social e-commerce boom set off by Pinduoduo last year, this round of community selling is decentralized-traffic is decentralized and operated by massive offline retail stores, Different implementation methods (public account, WeChat group, short video, live broadcast, etc.); fulfillment is also decentralized, and can be traded through the store’s own mini-programs and distributed at local stores, without necessarily going through a centralized e-commerce company such as Tmall. platform.

In fact, prior to the epidemic, this type of transaction model already existed widely in grassroots economies and had a broad base of user bases (for example, many small fresh communities in small communities have a regular customer base of 100-300 people, Order in the group and deliver to your door). Under the influence of the epidemic, moreMulti-scale retail companies join the ranks.

This will have a profound impact on two levels:

First, the transformation of offline stores will further intensify. Stores will no longer be the center of transactions, but will become part of the “O2O + community” transaction chain.

Second, the traffic acquisition methods and transaction links are more fragmented. When it comes to traffic acquisition, the store operates communities that show their magical powers and are deeply integrated with social and content (WeChat groups, circle of friends, live broadcasts, short videos, etc.). On the transaction link, brands and retailers can rely on small programs to build their own closed-loop transactions, which is a potential threat to traditional centralized e-commerce platforms. Although mini-program e-commerce has existed for many years, this wave of offline store self-help has provided it with a wider range of application scenarios.

Change three: unmanned

During the anti-epidemic period, users are very sensitive to interpersonal contacts, and they have concerns about taking out food and express delivery. At the policy level, the development of smart express counters is one of the officially encouraged epidemic prevention measures. In Wuhan, are you hungry? Cooperate with community convenience stores to set up fresh convenience convenience pick-up stores to encourage pick-up in the community. After this round of “contactless” experience, consumers’ acceptance of unmanned services has greatly improved.

During the epidemic, among the fresh-food e-commerce companies, Suning Vegetable Market, which mainly focuses on self-picking mode, has doubled its users in Nanjing and Shanghai, with daily sales reaching 6-8 times before the Spring Festival.

Furthermore, after the widespread popularization of centralized express counters and pick-up points, it has created favorable conditions for the further expansion of “unmanned delivery” in the true sense. Under the traditional delivery-to-home model, delivery requires passing through building access and taking the elevator through several levels, which are all challenges for intelligent robots. (The food delivery robots currently used in hotels are connected with hotel elevator systems and room call systems; but Large-scale residential buildings obviously cannot achieve full docking with robots).

But if the last mile delivery is from the courier point to the centralized pick-up point, the difficulty of unmanned operation will be greatly reduced. In Wuhan, where the epidemic is most severe, JD’s intelligent distribution robot has completed the first order for unmanned distribution for Wuhan Ninth Hospital.

The special period of the epidemic also amplifies the efficiency bottlenecks of retail companies in the supply chain and logistics, and the shortage of sorting and distribution manpower. More and more companies are deploying unmanned technology to improve efficiency. For example: JD Logistics has launched a sorting robot on a large scale. Meituan is also accelerating the research and development of unmanned “micro warehouse” to optimize the door-to-door picking process.

Facing the expectations of the economic cold winter, the above unmanned application scenario may become a great tool for retail companies to improve efficiency and protect profits. The popular express delivery and take-away self-collection model, although sacrificing service levels to a certain extent, is far more economical than the traditional home-to-home model, providing a solution for the high e-commerce logistics costs. In the back-end operation scenario, the automatic picking shelves and automatic conveying equipment are becoming more mature, and the willingness to popularize enterprises that urgently need to reduce costs and improve efficiency is increasing.

Change four: platform integration

The retail environment in China in 2019 is already difficult. In addition to the impact of the epidemic, a group of small and medium-sized enterprises will fall in this cold winter. And, in the first two years of the new retail boom, many start-ups have been running for real with money raised from financing. After the epidemic, the capital circle will not underestimate the negative impact of the epidemic on the economy, and investment will be more cautious. Startup financing will be more difficult, accelerating the reshuffle of the industry. It is expected that the turbulence of heavy asset tracks such as restaurants and convenience stores will be particularly severe.

On the other side, large platforms have demonstrated extremely high mobilization capabilities and technology-driven advantages in the epidemic crisis, which has enabled them to better grasp this window and turn them into “crisis” and “opportunity” in their business growth. , Making progress in customer acquisition and sales. In addition, large platforms often have a wide range of services. Users acquired during this particular period of time, especially fresh users, can be transferred across categories and cross-industry within the ecosystem, which greatly enhances the value of the customer base.

More importantly, for the merchants in the ecosystem, the strong resources and technical capabilities of the platform have also played a role of “buffering and earthquake resistance”: Meituan provides a package of measures to help catering merchants develop takeaway businesses, and United Bank provides Preferential interest rate loans. The Suning retail cloud platform quickly organized more than 5,000 franchised individual store owners in its Guangbu County to expand community-based out-of-store sales. Some store owners were able to achieve 30-80% of sales during the anti-epidemic closing period, supporting the store’s Daily costs.

After this campaign, the basic role of large platforms in the business ecosystem has become more prominent, and the value of “empowerment” has been reflected. Traditional formats, small chains, and self-employed people are more willing to join the large platform ecosystem and develop themselves with the help of platform resources.

After the shock shock of the epidemic situation, on the one hand, industry integration is manifested as the weak being shuffled, and the stronger are stronger; on the other hand, it is also represented by the large-scale business ecosystem’s platform-type consolidation of traditional formats, small chains, and individual stores.

03 How should retail companies cultivate their internal skills

The negative effects of the epidemic are short-term. After the epidemic, there is a high probability that a wave of consumer industryPositives-retaliatory release of backlog of consumer demand, commercial real estate rent reduction, counter-cyclical stimulus policies and measures. For companies that can survive this winter, using this campaign to deepen transformation and cultivate internal skills is particularly critical to grasping opportunities in the next few years. Three of these issues deserve special attention:

First, seize the opportunity of fragmentation of consumption, and set up own user assets as a strategic priority. At the same time that consumer behavior is deeply online, online behavior trajectories are also widely differentiated, and purchases are tied to highly decentralized content and social circles. Fragmented traffic makes it more difficult for brands and retailers to operate. This is no longer a problem that can be solved by running an online store. This is a challenge, but also an opportunity-the fragmented traffic pattern has begun to weaken the traffic monopoly of the head platform, and retail companies have a better chance to build their own user assets.

For some large and medium-sized retailers, during the epidemic, on the one hand, when they developed their O2O business by relying on head traffic platforms such as Hungry and Meituan, they felt the rules and regulations brought by the platform rules. Challenges; on the other hand, their own user platforms such as applets have also gained unprecedented development opportunities.

The establishment of own user assets will come from various fragmented channels, including stores, mini-programs, user WeChat groups, social e-commerce platforms and other platforms that enable effective user interaction, from highly decentralized content and cross-industry. Alliance, etc.

To settle these fragmented traffic and effectively establish own user assets, a series of capabilities are required, including: (1) Data capabilities—the establishment and mining of user databases (many companies currently have data, (Utilization status), cross-platform, cross-scenario operation model for tracking and analyzing user behavior; (2) content capabilities-keenly observe market trends, follow and even lead trends in content marketing; (3) organizational capabilities-internal organization in Synergy of different traffic channels and user asset channels, etc.

Second, do a good job of new user precipitation and maximize consumer value. For companies that have made breakthroughs in consumption scenarios during the epidemic, such as fresh food e-commerce, supermarket O2O, online education, remote office, etc., the epidemic-resistant campaign provides a key opportunity to educate the market and acquire new customers. It is those companies that can effectively retain new customers, increase single customer contribution, and promote user fission after the epidemic.

Just as the best e-commerce companies not only seek sales breakthroughs during the Double Eleven, they are also committed to maximizing the repurchase of Double 11 customers during non-big promotion periods. Similarly, if we broaden our perspective, in the medium and long term user operations,Volume is only the first step. Doing a good job in depositing user assets and maximizing user value is the key to the success of an enterprise.

Opportunities for maximizing consumer value include: On the one hand, the “octopus” that provides categories and consumption scenarios provides a basis for the new online fresh customers obtained this time to be able to transform in multiple scenarios. On the other hand, more accurate user tagging and continuous operations will open up users’ interactions between categories and scenarios.

Third, solid operation, internal skills, self-construction and cooperation. In the past two or three years, retail companies have talked about many new concepts and created many new models. The thinking is correct, but many companies have not laid a solid foundation for basic operations. For example, the in-depth control of the upstream supply chain and the flexibility of logistics and distribution capabilities determine the online business volume during the special period of the epidemic. It is also crucial for the continued development of the business and the user service level.

In addition, profitability is an ongoing challenge for online-oriented retailers. Especially for medium-sized enterprises, in the face of the capital winter that may deepen after the epidemic, it is important to use multiple methods to improve operational efficiency and achieve their own blood production. Lean operations, cost control, and expansion of unmanned scenarios (such as self-lifting of distribution) are all directions that can be dug deeper.

It is worth noting that “internal power” can be built by itself, or it can be mined outside. Actively establishing an ecosystem partner network and “eco-operation” capabilities, and further expanding cooperation spaces, models and partners, will enable outstanding companies to turn the tests of special periods into opportunities to enhance their long-term internal strength.

In fact, as consumer interactions become more fragmented and operations become more complex, professional service providers for various operational links have emerged as needed, from member operations and data analysis to the last mile outsourcing and “shared front warehouse” “concept. Retail companies need to plan their own capability matrix—what capabilities must be built by themselves, how to integrate the capabilities of external procurement, and where is the boundary between core capabilities and ecological sharing.

(Kearney’s consultant Shen Jiaying also contributed to this article)

Author introduction:

He Xiaoqing, CEO, Kearney Management Consulting Greater China, Head of Consumer Goods and Retail Industry

Si Yujie Senior Manager of Kearney Management Consulting Company

Kearney’s consultant Shen Jiaying also contributed to this article