The wind started at the end of Qingping. How much impact will the new crown pneumonia epidemic have on the economy, what are the implications of the SARS experience of that year, what are the differences today, and where are the opportunities and risks?

Editor’s note: This article is from WeChat public account “ Ocean Capital ” (ID: sino -oceancapital), author of Ocean Capital.

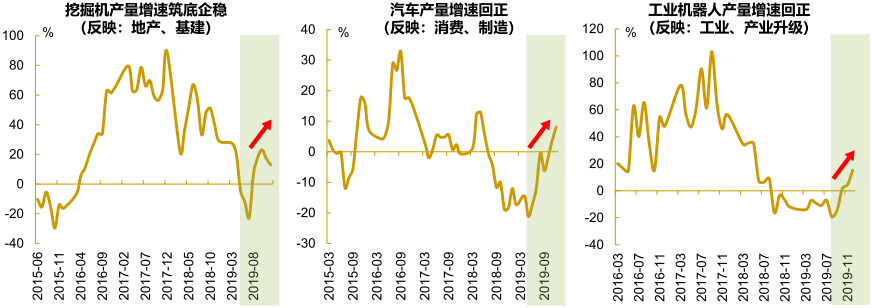

The wind starts at the end of Qing Ping. In the Chinese economy in the fourth quarter of 2019, a series of micro, forward-looking indicators showed signs of stabilization, and a round of “weak enterprise stabilization” seemed to be expected. However, in December of the same year, the news of unexplained pneumonia did not receive the attention of all parties, and the “Black Swan” incident broke out. How much impact will the new crown pneumonia epidemic have on the economy, what are the implications of the SARS experience of that year, what are the differences today, and where are the opportunities and risks?

Figure 1: A series of micro-indicators show that the Chinese economy has just been “weak and stable” at the end of 2019 (%)

I. Learn from history: What does SARS tell us?

The new crown virus has been growing rapidly in early 2020, but the impact of the epidemic is still to be traced. The review of SARS in 2003 can bring a lot of inspiration.

(1) SARS causes a short-term V-shaped trend of the economy, but it will not change the long-term trend

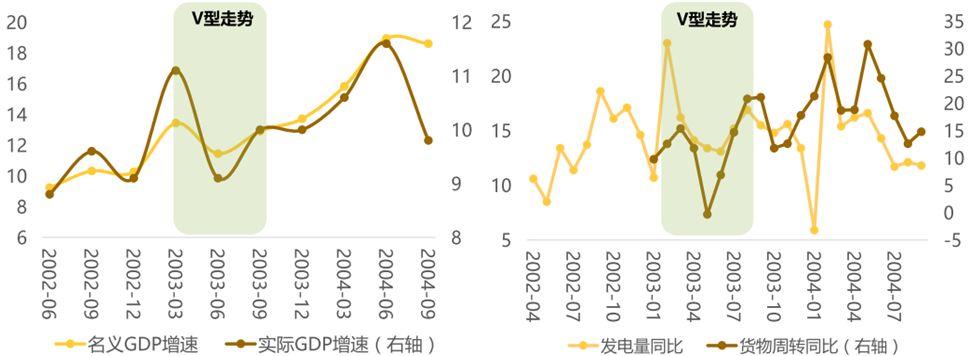

The Chinese economy squat before rebounding before and after SARS, showing a V-shaped trend. From the perspective of GDP growth rate, the impact of the epidemic was concentrated in the second quarter, and it recovered to a higher level in the third quarter. Viewed from a micro perspective, the power generation and freight turnover have shown similar V-shaped trends during SARS. Since then, GDP growth has continued to grow at a high rate from 2004 to 2007, achieving economic take-off, and has not been affected by the epidemic in the medium and long term.

In addition, from the impact of infectious diseases such as H1N1 and Brazilian Zika in the United States and Mexico, the United States economy has ushered in the longest recovery cycle in history after the epidemic. PakistanThe successful hosting of the Olympic Games after the epidemic showed that the impact of the epidemic was a short-term phenomenon.

Figure 2: During the SARS outbreak, GDP, power generation, and freight growth all showed V-shaped trends (%)

Source: Wind, Ocean Capital Research and Development Department

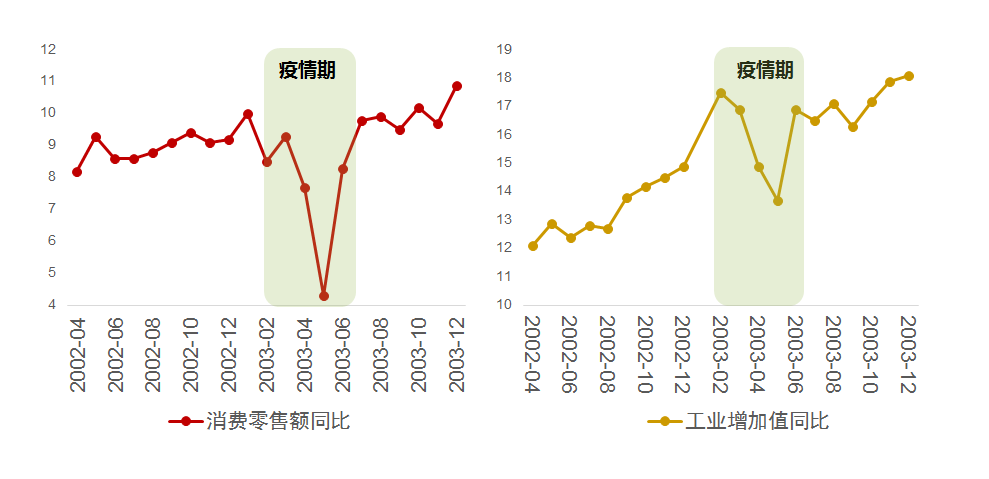

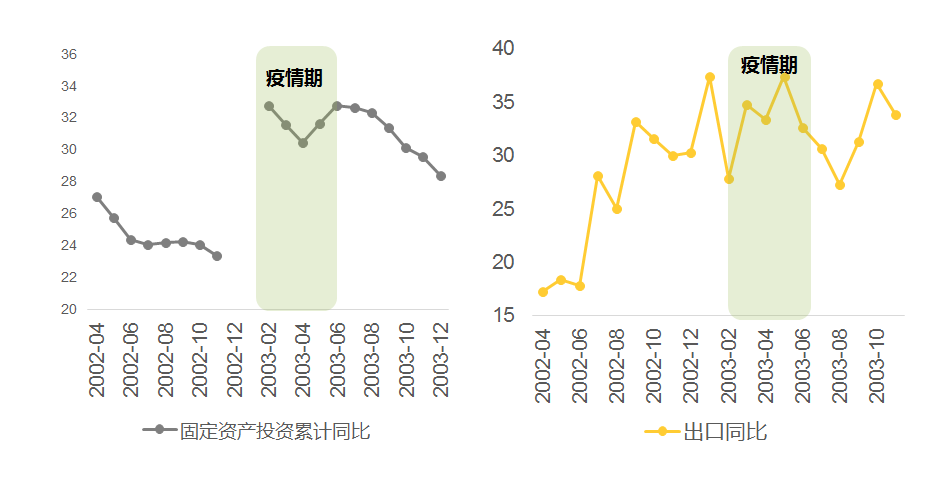

(II) Consumption is the most severely damaged, followed by industry, with less fluctuations in investment and exports.

Consumption was hit hardest by the epidemic. The growth rate of retail sales of consumer goods fell from about 9% to 4%. The second is industry. The growth rate of industrial added value dropped from about 16% to 13%, but the decline was not as large as that of consumption. Heavy industry was less affected than light industry. The least affected are fixed asset investment and exports, and the most severe epidemic situation has little fluctuation from April to May.

Figure 3: Consumption, industry, investment, and exports were affected differently during the SARS outbreak (%)

Source: Wind, Ocean Capital Research and Development Department

(3) SARS drives macro policy from stable to loose

The macro policy was originally stable in 2003, but After the outbreak, the policy temporarily turned to loose. M2 did not slow down during the epidemic period, andIs accelerating growth. After the epidemic ended, the central bank turned to tighten again due to overheating demand.

Figure 4: During the outbreak of SARS, the macro policy was loose, and the growth rate of M2 increased instead of decreasing (%)

Source: Wind, Ocean Capital Research and Development Department

Second, Look at the present: the consequences of this V-squat may be more serious

You need to see that the impact of the new crown epidemic is more severe than in SARS in three ways:

(1) The impact of “dormant” control on corporate cash flow is greater

The number of newly diagnosed new crown virus infections has expanded far faster than SARS, leading to the closure of Hubei, isolation and resumption of work in the country, and most economic activities have entered a “dormant”. The cash flow of enterprises has been greatly affected, which is rare in history.

(II) The “physical constitution” of the economy is not as strong as it was during SARS.

2003 is the stage of China ’s economic take-off and the second year of China ’s accession to the WTO. The export and investment momentum is strong, industrialization and urbanization are in full swing, and it is easy to recover quickly from the impact of SARS.

But looking at the moment, China is in a transition stage, the international environment is becoming more uncertain, and the “physical constitution” of the economy is even “thinner” than in 2003.

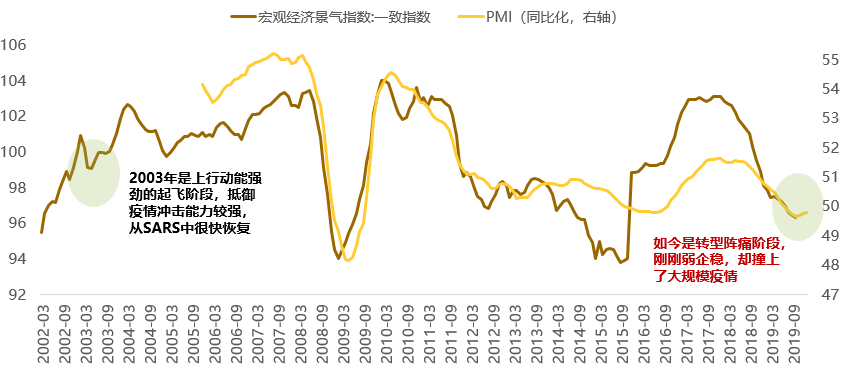

(3) “Weak and stable” just hit “Black Swan”

At the end of last year, China ’s economy just showed signs of “weak and stable business”, but its momentum is still not stable, especially PPI and corporate profit growth have not recovered. Today, they are hit by the epidemic “black swan”. If the confidence of all parties is unstable and the demand for consumer investment is reduced, it will increase the business difficulties of the enterprise. The “weak enterprise stability” may be interrupted, which in turn will further promote pessimism and the impact of the epidemic on the economy Easy to exceed expectations.

Figure 5: New crown epidemic situation is different from SARS business cycle

Source: Wind, Ocean Capital Research and Development Department

Although the squat of the V-shaped trend is more serious this time, there are three good news that are better than the SARS period:

1. Lower case fatality rate

The mortality rate of new crown virus (3.1%) is lower than SARS (7%), especially in Hubei, which has a lower mortality rate (1.3%), similar to H1N1.

2. The impact of the Spring Festival is small, the e-commerce makes up for it

The first quarter of the new crown epidemic happened during the Spring Festival. The Spring Festival had little economic activity, and the first quarter accounted for 22% of the annual GDP, which is relatively small. The penetration rate of e-commerce is now much higher than that in 2003, and it is compensated online The impact of offline “sleep”.

3. More preparation time for stronger macro policies

The most important thing is that the outbreak of the new crown is at the beginning of the year, and the “two sessions” have not yet been held. There is still time to discuss and formulate stronger macro policies.

III. Summary Outlook: What will the policy do and how will the situation look?

(I) In the short term, “stable growth” has become the primary goal of macro policies

2020 is the decisive year for building a well-off society in an all-round way, and various economic goals must be completed. But the new crown epidemic is unprecedented. If macro policy is not adjusted, the consequences of V-shaped squats will be much more serious than SARS. Therefore, the epidemic broke the multi-objective balance of stable growth, inflation control, and deleveraging, and the importance of stable growth has increased significantly.

Recently, all ministries and commissions have introduced some measures to stabilize growth. Adjust the OMO interest rate 10BP as follows, extend the transition period of the new rules for asset management, set up special reloans for epidemic conditions, and reduce the financing burden of interest-rate reduction companies by the central government. Localities have also maintained loose policy and flexibility. Some CBRCs allow banks to extend difficult enterprises, take the initiative to renew loans due within a certain period of time, and do not mandate the inclusion of non-performing loans overdue for more than 90 days.

In the future, monetary and financial infrastructure will continue to step on the “throttle” for a period of time. For example, expect LPThe new benchmark loan interest rate for R may be lowered. A number of major infrastructure projects are being launched faster. A new set of measures to implement the Politburo Standing Committee’s “actively expanding domestic demand” directives will also be introduced.

(2) In the long run, there is no need to worry too much, the sun rises as usual

The new crown virus epidemic will not change the long-term law and logic of China’s development: the historical process of new urbanization has not changed, the general direction of consumption upgrade has not changed, the trend of technological innovation has not changed, and the upgrading, transformation, and development of manufacturing have not changed. .

(3) Grasp the risks and opportunities brought by the epidemic, “Black Swan” can also lay eggs

The epidemic has added a “squat and stand up” process to the short- and medium-term operation of China’s economy and industry, except for some “squats”, some “squats”, and some “no squats”. “Slow rise”, while others are “take off in place.” Different industries are affected differently and need to be prepared in advance.

The epidemic will have some changes in future lifestyles, which are more reflected in consumer habits. Correspondingly: the business model has changed from offline to online, and e-commerce, leisure and entertainment, education and training, and cinema lines , Remote office, and even related real estate will be more profoundly affected.

We need to look at the epidemic dialectically. The opportunities and risks in it are worth continuing attention. On the one hand, we must fully prepare for the short-term risks brought by the epidemic and adjust the existing operating rhythm; on the other hand, we must realize that the epidemic has driven a “small cycle” of policy regulation, Under the logic, investment should be rationally arranged in accordance with the “small cycle”.

You need to see that the impact of the new crown epidemic is more severe than in SARS in three ways:

(1) The impact of “dormant” control on corporate cash flow is greater

The number of newly diagnosed new crown virus infections has expanded far faster than SARS, leading to the closure of Hubei, isolation and resumption of work in the country, and most economic activities have entered a “dormant”. The cash flow of enterprises has been greatly affected, which is rare in history.

(II) The “physical constitution” of the economy is not as strong as it was during SARS.

2003 is the stage of China ’s economic take-off and the second year of China ’s accession to the WTO. The export and investment momentum is strong, industrialization and urbanization are in full swing, and it is easy to recover quickly from the impact of SARS.

But looking at the moment, China is in a transition stage, the international environment is becoming more uncertain, and the “physical constitution” of the economy is even “thinner” than in 2003.

(3) “Weak and stable” just hit “Black Swan”

At the end of last year, China ’s economy just showed signs of “weak and stable business”, but its momentum is still not stable, especially PPI and corporate profit growth have not recovered. Today, they are hit by the epidemic “black swan”. If the confidence of all parties is unstable and the demand for consumer investment is reduced, it will increase the business difficulties of the enterprise. The “weak enterprise stability” may be interrupted, which in turn will further promote pessimism and the impact of the epidemic on the economy Easy to exceed expectations.

Figure 5: New crown epidemic situation is different from SARS business cycle

Source: Wind, Ocean Capital Research and Development Department

Although the squat of the V-shaped trend is more serious this time, there are three good news that are better than the SARS period:

1. Lower case fatality rate

The mortality rate of new crown virus (3.1%) is lower than SARS (7%), especially in Hubei, which has a lower mortality rate (1.3%), similar to H1N1.

2. The impact of the Spring Festival is small, the e-commerce makes up for it

The first quarter of the new crown epidemic happened during the Spring Festival. The Spring Festival had little economic activity, and the first quarter accounted for 22% of the annual GDP, which is relatively small. The penetration rate of e-commerce is now much higher than that in 2003, and it is compensated online The impact of offline “sleep”.

3. More preparation time for stronger macro policies

The most important thing is that the outbreak of the new crown is at the beginning of the year, and the “two sessions” have not yet been held. There is still time to discuss and formulate stronger macro policies.

III. Summary Outlook: What will the policy do and how will the situation look?

(I) In the short term, “stable growth” has become the primary goal of macro policies

2020 is the decisive year for building a well-off society in an all-round way, and various economic goals must be completed. But the new crown epidemic is unprecedented. If macro policy is not adjusted, the consequences of V-shaped squats will be much more serious than SARS. Therefore, the epidemic broke the multi-objective balance of stable growth, inflation control, and deleveraging, and the importance of stable growth has increased significantly.

Recently, all ministries and commissions have introduced some measures to stabilize growth. Adjust the OMO interest rate 10BP as follows, extend the transition period of the new rules for asset management, set up special reloans for epidemic conditions, and reduce the financing burden of interest-rate reduction companies by the central government. Localities have also maintained loose policy and flexibility. Some CBRCs allow banks to extend difficult enterprises, take the initiative to renew loans due within a certain period of time, and do not mandate the inclusion of non-performing loans overdue for more than 90 days.

In the future, monetary and financial infrastructure will continue to step on the “throttle” for a period of time. For example, expect LPThe new benchmark loan interest rate for R may be lowered. A number of major infrastructure projects are being launched faster. A new set of measures to implement the Politburo Standing Committee’s “actively expanding domestic demand” directives will also be introduced.

(2) In the long run, there is no need to worry too much, the sun rises as usual

The new crown virus epidemic will not change the long-term law and logic of China’s development: the historical process of new urbanization has not changed, the general direction of consumption upgrade has not changed, the trend of technological innovation has not changed, and the upgrading, transformation, and development of manufacturing have not changed. .

(3) Grasp the risks and opportunities brought by the epidemic, “Black Swan” can also lay eggs

The epidemic has added a “squat and stand up” process to the short- and medium-term operation of China’s economy and industry, except for some “squats”, some “squats”, and some “no squats”. “Slow rise”, while others are “take off in place.” Different industries are affected differently and need to be prepared in advance.

The epidemic will have some changes in future lifestyles, which are more reflected in consumer habits. Correspondingly: the business model has changed from offline to online, and e-commerce, leisure and entertainment, education and training, and cinema lines , Remote office, and even related real estate will be more profoundly affected.

We need to look at the epidemic dialectically. The opportunities and risks in it are worth continuing attention. On the one hand, we must fully prepare for the short-term risks brought by the epidemic and adjust the existing operating rhythm; on the other hand, we must realize that the epidemic has driven a “small cycle” of policy regulation, Under the logic, investment should be rationally arranged in accordance with the “small cycle”.