Chinese economists have analyzed the causes and consequences of the US stock market crash in detail and provided a lot of information. This article combs the causes of the US stock market crash and the causes and consequences of the US government’s adoption of a series of policies, and tries to find out the internal logic.

Reviewing the evolution of the US subprime mortgage crisis:

Financial crisis triggered economic recession

Financial crisis triggered economic recession

In order to better understand the US stock market crash, the Fed ’s policy and how it will develop in the future, we first need to review 2007 to The 2008 US subprime mortgage crisis and the series of policies adopted by the US government in response to the subprime mortgage crisis.

The subprime mortgage crisis in the United States can be divided into six development stages:

The first stage, no income, The poor class without work and assets borrowed a lot of subprime loans.

In the second stage, due to various reasons, the default rate of these loans has risen sharply.

In the third phase, due to the sharp rise in default rate, the prices of subprime-based assets (such as MBS, CDO, etc.) fell sharply; at the same time, the money market appeared Shortage of liquidity, the interest rate of short-term bonds such as asset-backed commercial paper (ABCP) has risen sharply.

In the fourth stage, financial institutions had to compress their balance sheets to meet capital adequacy requirements, so credit crunch occurred.

In the fifth stage, financial institutions, especially some systemically important financial institutions, went bankrupt and the entire financial system was in crisis. The bankruptcy of Lehman Brothers was a landmark event in the outbreak of the US subprime mortgage crisis.

In the sixth stage, the US real economy fell into recession.

The third stage of the subprime crisis (the stage of liquidity shortage in the money market) and the fourth stage (the stage of the credit crunch) are very similar to the current stock market crash in the United States Place. Comparing the similarities and differences between them is very helpful for us to understand the US stock market crash.

First discuss the third stage: the stage of insufficient liquidity.

Why during the subprime mortgage crisis, the collapse of asset prices such as MBS and CDO will cause insufficient liquidity?

Because assets such as MBS and CDO are long-term assets, its duration may be ten, twenty or thirty years, and the purchase of these financial assets is a long-term investment . However, financial institutions that want to hold these long-term assets need to borrow money from the money market to buy these long-term assets. For example, many financial institutions need to issue short-term financing instruments such as ABCP for three months or longer.

An example shows that financial institutions wanting to buy 10 billion MBS will have to raise 10 billion from the money market. The financing period is three months or six months. But the duration of MBS assets may be ten years, twenty years or even longer. Therefore, these financial institutions must continue to raise funds from the money market, borrowing new ones and returning old ones, in order to hold MBS and CDO for a long time. It is through short-term investment and long-term gains (investment income-financing costs).

But once the price of bonds such as MBS and CDO falls, short-term investors who provide funding for long-term investors in the money market, such as ABCP buyers, are worried because Long-term investors may default and are no longer willing to buy ABCP. As a result, the money market suddenly suffered from insufficient liquidity.

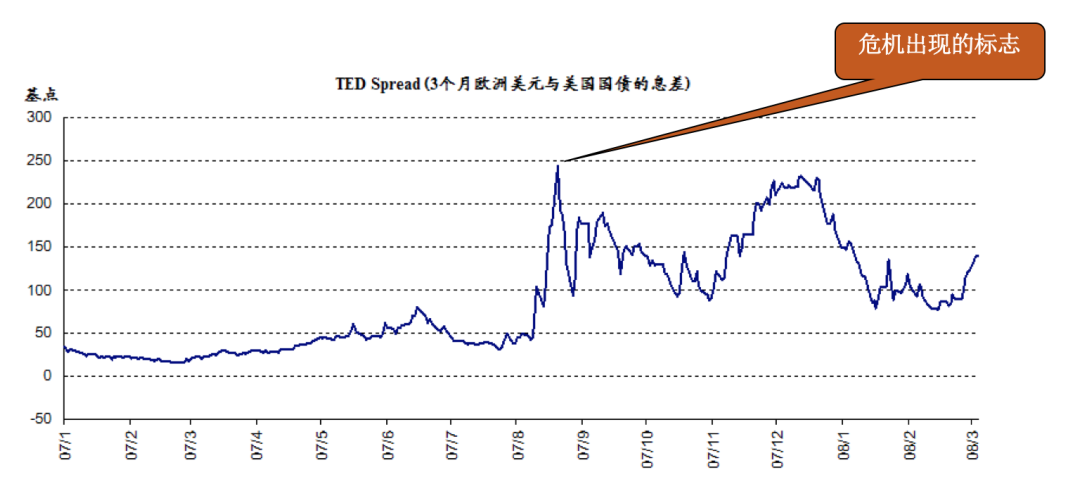

As shown in the figure, at this time, the spread of the three-month European dollar and U.S. Treasury bonds suddenly increased sharply, and other spreads that showed insufficient liquidity were also large. rise. This is a very important node.

As asset prices fell and money market investors were reluctant to purchase short-term financing bonds such as ABCP, financial institutions holding long-term assets had to do everything they could to raise funds to solve the problem of insufficient liquidity. If you can’t find the money, you have to sell your long-term assets.

As asset prices fell and money market investors were reluctant to purchase short-term financing bonds such as ABCP, financial institutions holding long-term assets had to do everything they could to raise funds to solve the problem of insufficient liquidity. If you can’t find the money, you have to sell your long-term assets.

As asset prices fell and money market investors were reluctant to purchase short-term financing bonds such as ABCP, financial institutions holding long-term assets had to do everything they could to raise funds to solve the problem of insufficient liquidity. If you can’t find the money, you have to sell your long-term assets.

At this time, it entered the fourth stage, the credit tightening stage.

One goldFinancial institutions want to buy assets and make profits, they must rely on leverage, not just capital. In other words, financial investors must borrow other people’s money to make long-term investments and increase profits by increasing assets. At this time, there will be a problem of leverage.

The so-called leverage ratio is the ratio of assets to capital. During periods of rising asset prices, the leverage ratio of financial institutions is usually very high. The leverage ratio is 10 times or 20 times in the normal period, and may be as high as 50 times or more during the rise of asset prices.

Before the outbreak of the subprime mortgage crisis, the lever rate of large financial institutions in the United States was very high. Once the price of an asset falls, it is calculated using mark to market in accordance with accounting principles, and the price of the balance sheet must be revalued. For example, the original book assets were 10 billion yuan, and only 5 billion after the revaluation, so the assets were reduced by half.

According to accounting standards, capital must also be deducted by the same amount. Suppose a financial institution has 1,000 units of assets and 50 units of capital. The institution ’s leverage ratio is 20 times. As asset prices fall, the numerator and denominator must be reduced by the same number when calculating leverage. This means that if the same 30 units are deducted, the asset price will be reduced from 1000 units to 970 units, and the capital will be changed from 50 units to 20 units, so that the leverage ratio will become 48.5 times.

During the financial crisis, the risk is very high. Financial institutions should reduce the leverage ratio but not increase the leverage ratio, otherwise no investors dare to hold the assets of these institutions. For example, no investors will come to buy short-term bonds issued by highly leveraged financial institutions. In this way, financial institutions must take measures to reduce the leverage ratio to a level acceptable to investors.

There are two ways to reduce leverage:

❶ Increase capital. For example, financial institutions now have only 970 units of assets and 20 units of capital. If the capital of 28.5 units can be increased at this time, the leverage ratio will fall back to 20.

❷ Compress the balance sheet of financial institutions and reduce assets. This approach is used more in reality. For example, the asset price plummeted, leaving only 970 units. If you then reduce 570 units to 400 units, the leverage ratio will return to 20 times.

So, reducing assets is to make financial institutions leverageMain practices maintained at a level that reassures public investors. While reducing assets, it means that liabilities are also reduced. The money sold for assets is used to pay off debts. Assets and debt are reduced at the same time. In other words, in order to stabilize leverage, a financial institution will reduce assets and compress its balance sheet.

For a single financial institution, it is a reasonable decision to sell assets to repay debt and reduce leverage. But if all financial institutions do this, there will be a so-called synthetic reasoning error: asset prices fall further, so further sales of assets are needed to reduce the leverage that has risen. In this way, there is a vicious circle: asset prices fall-sell assets-assets talked about further decline.

My assets are the liabilities of others. For example, the bank ’s assets are loans to the enterprise (the enterprise ’s liabilities), and compressing assets means reducing loans to the enterprise. Businesses will not get loans (no debt). On the one hand, the financial crisis will lead to the closure of financial institutions; on the other hand, it will also trigger a crisis in the real economy. If the production enterprise cannot obtain bank loans, production will be difficult to maintain and the enterprise will close down.

In short, the approximate process of the evolution of the subprime mortgage crisis is: subprime default; the price of securitized assets (MBS, CDO) fell; liquidity shortage in the money market; banks, Financial institutions such as investment bank hedge funds deleveraged and compressed balance sheets; due to liquidity shortages, credit contractions, and capital chain disruptions, financial institutions closed down; lending activities stopped, production enterprises were unable to invest and produce, and economic growth was affected.

At the same time, the plunge of asset prices is transmitted to the resident sector through the wealth effect, resulting in residents also reducing consumption, so investment and consumption are reduced. As a result, the economic growth rate showed negative growth and the economy fell into recession.

The Fed takes two steps to deal with the subprime crisis: Stabilize finance and stimulate the economy

The Fed takes two steps to deal with the subprime crisis: Stabilize finance and stimulate the economy

The Fed takes measures in two steps to deal with the subprime crisis: The first step is to stabilize finance; the second step is to stimulate the economy. Similarly, we are now facing the impact of the epidemic, and we should take two steps to restore the macroeconomics. The first step is to stabilize the entire supply chain and restore the production system steadily; the second step is to stimulate economic growth.

What did the Federal Reserve and the Treasury then do to stabilize finance? What is the logic? Can be discussed further.

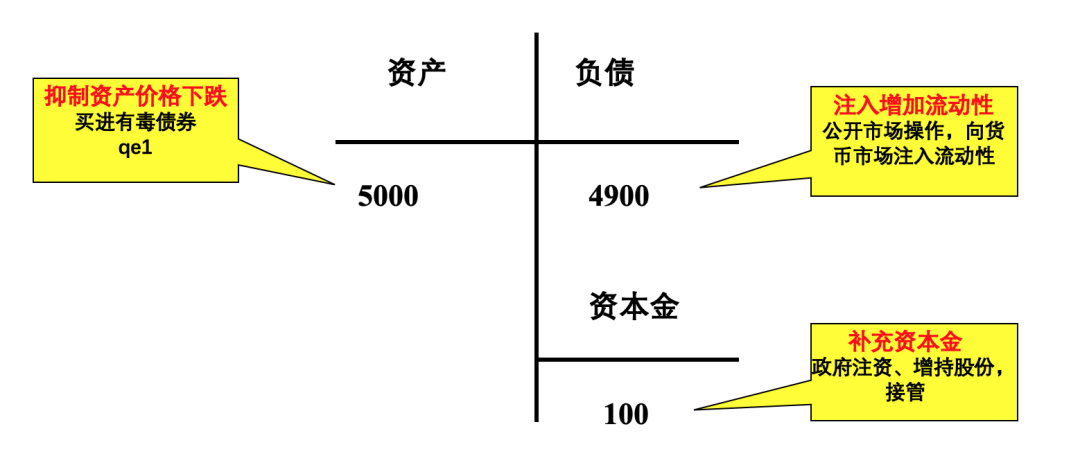

The Fed sends troops in three ways: the first way is the asset side, the second way is the liability side, and the third way is the capital.

times The origin of the loan crisis is the decline in asset prices, such as the decline in the prices of MBS and CDO. At this time, the Fed must first contain the decline in the prices of these assets. Investors do not buy, the government buys. So an important content in QE1 is Buy toxic assets. Similarly, when Hong Kong rescued the stock market when investors threw out stocks, the Hong Kong financial management authorities went into the market to buy stocks and did not allow stock prices to fall.

In short, the first step taken by the Fed in response to the financial crisis is to buy assets. Of course, it is also possible to carry out several measures at the same time, so it can also be said that buying assets is one aspect of the Fed ’s response measures.

Another path is to inject liquidity through open market operations. Short-term investors are reluctant to buy ABCP and will not repurchase after the expiration. Large institutions cannot hold short-term funds to hold long-term assets At this time, the Fed injected liquidity into the currency market, making short-term investors willing to continue to purchase short-selling bonds such as ABCP. At the same time, they can provide financial support to financial institutions that sell short-term asset bonds such as ABCP, so that they are no longer forced to sell such bonds at low prices. Assets.

Another way is to replenish capital. For example, the United Kingdom nationalized Northern Rock when it faced bankruptcy, or the government used debt to convert shares to finance Institutional capital injection.

As shown in the figure, assume that assets are 5000 units, liabilities are 4900 units, and capital is 100 units. Once the financial crisis comes, without the help of the government, the reasonable response of financial institutions through synthetic error of reasoning will make these numbers become smaller and smaller and fall into a vicious circle.

If you want to stabilize these figures, you should make the asset price fall on the asset side; on the liability side, save financial institutions from being forced to reduce liabilities; in the capital project In the past, the government increased its shareholding and took overSupplement capital for financial institutions. The takeover of the two houses in the United States and the nationalization of North Rock Bank are both concrete examples of starting with capital to contain the financial crisis from further deterioration.

After the subprime mortgage crisis, the Fed used the above three methods to stabilize the entire financial system. When we analyze the US stock market crash and try to understand the policies of the US government, we can examine how the US government started to stabilize the financial market from the above three aspects.

The second stage of the US governance of the financial crisis is to start stimulating the economy after stabilizing the financial markets. The main US policy is QE + rate cuts.

QE operation has four times, QE1, QE2, QE3, QE4, each time the goal is different. In general, the Fed ’s main purpose of QE is to raise asset prices.

The Fed purchased toxic assets (mainly MBS) and also purchased a large amount of long-term government bonds. The former stabilizes the price of assets such as MBS, while the latter leads to an increase in the price of government bonds.

The rise in the price of government bonds means that the yield of government bonds falls. Treasury bonds are the safest asset. Once there is external risk, investors will flock to the treasury market, which the Fed does not want to see. The Fed lowered the interest rate of government bonds and pushed investors and public investors to other asset markets.

Funds will not be transferred to the infamous MBS and CDO, so they will be transferred to the stock market in large quantities. As a result, the stock price rises and produces a strong wealth effect: that is, people buy stocks through various funds, their assets increase in value, and then increase consumption. In addition, the increase in stock prices makes it easier for companies to obtain funds.

QE causes stock prices to soar, and the latter stimulates consumption and investment through the wealth effect and the Tobin Q effect. The increase in effective demand quickly brought the United States out of the economic crisis and maintained economic growth for nearly 10 years, which played a role in promoting economic growth.

QE has two other important purposes, one is to create inflation and the other is to induce the depreciation of the US dollar. Both are conducive to US economic growth and reduce the debt burden. But these two policy objectives seem to be not very ideal.

QE such as the purchase of government bonds through large-scale open market operations is counted as money printing? QE more than 10 years agoWhen the policy was first introduced, the academic circles in the US and China asked: Is QE a general open market operation or is it money printing?

Because QE is different from ordinary open market operations: first, QE is huge; second, QE not only buys US Treasury bills, but also MBS, CDO and the like Toxic assets; third, not only buying ordinary US Treasury bonds, but also long-term Treasury bonds, these operations are unusual.

There are three main reasons why QE does not belong to money printing:

❶ Whether money printing depends on the purpose If the purpose is to finance deficits, it is money printing; if the purpose is to stimulate economic growth, it is not money printing.

❷ QE is a temporary policy. When the economy resumes normal growth, the Fed will withdraw from QE and sell the over-bought government bonds. The toxic assets that are bought now are sold when the price rises. Not only can the excess money be recovered, but also the Ministry of Finance can make a profit.

❸ The main problem facing the United States is the economic recession, and there is no need to worry about inflation for the time being.

In fact, the United States has been talking about withdrawing from QE since mid-2013, but what is the actual implementation?

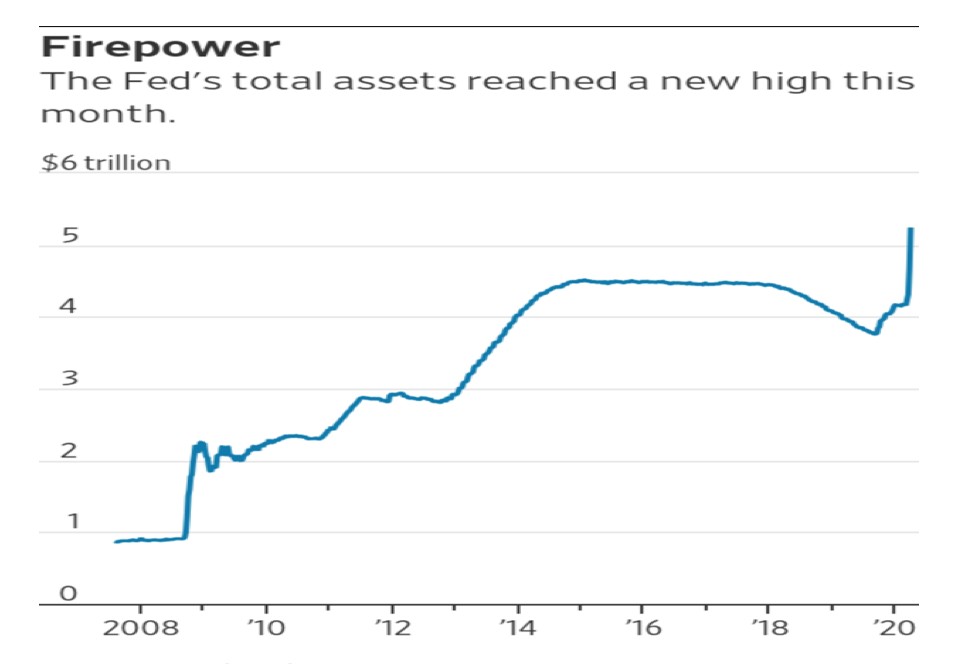

As shown in the picture, from 2014, the Fed ’s assets no longer increase. Before the outbreak of the crisis, the Fed’s assets were more than 800 billion US dollars, and later rose to more than 4 trillion US dollars. After 2016, it has been declining slowly, and in 2018, the decline was more prominent. But now due to the impact of the new coronary pneumonia and the stock market crash, assets have become 5 trillion US dollars, and the withdrawal of QE has become far away.

I personally think that QE is printing money. From the perspective of the United States, QE is reasonable, and there was no other better option at the time. But any policy comes at a price, and QE is no exception.

I personally think that QE is printing money. From the perspective of the United States, QE is reasonable, and there was no other better option at the time. But any policy comes at a price, and QE is no exception.

I personally think that QE is printing money. From the perspective of the United States, QE is reasonable, and there was no other better option at the time. But any policy comes at a price, and QE is no exception.

The Fed ’s QE and other policies, including the US fiscal policy, Has a great impact on the size and structure of the US capital market. After the subprime mortgage crisis, changes in the US capital market, especially structural changes, are inseparable from today ’s stock market crash.

QE boosts the stock market bubble, and corporate debt implies huge risks. Can a new round of financial crisis be avoided?

QE boosts the stock market bubble, and corporate debt implies huge risks. Can a new round of financial crisis be avoided?

Here are the changes in the US asset structure:

First, each The total amount of treasury bonds is close to 20 trillion. Before the subprime mortgage crisis, the balance of US Treasury bonds was not high, but now it is very high, which is more than 100% of GDP. This is the most important change in the US capital market.

Second, the stock market has always occupied the most important position in the US capital market. The importance of the stock market before the subprime mortgage crisis has further increased. It turned out to be the most important, but now it is even more important. At the end of 2019, the market value of the stock market was around $ 30 trillion. Its changes have a very large impact on the US finance and economy.

Third, the current corporate debt is about ten trillion yuan, a significant increase from the previous.

Fourth, the importance of housing mortgage loans in the US capital market ranked second in the past, but its importance has declined. This is the change in the US capital market after the Fed implemented the QE policy during the subprime mortgage crisis.

So the overall situation is: the share of national debt has increased, the importance of the stock market has increased, and the long-term corporate debt has also increased significantly.

Before this stock market crash, most people believed that the surge in stock prices was the result of the good performance of the US real economy, not a bubble. The stock market crash can no longer clearly prove that there is a serious bubble in the US stock market. Why is there a bubble? There is no doubt that this is the result of QE. It can be said that the purpose of QE itself is to create a stock market bubble to stimulate economic growth.

What specific ways does the Fed ’s policy of rushing funds into the stock market be achieved? There seem to be two main ways:

First, because of the long-term low interest rates caused by QE, long-term investors such as insurance funds and pensions began to switch to stock investment.

These investors are very concerned about investment safety. The risk of treasury bonds is low, and the rate of return is very low, but now the rate of return on treasury bonds is too low. Financial institutions that manage long-term investment funds need to guarantee a certain rate of return, otherwise they cannot account to investors.

Although stock risk is greater than Treasury bonds, its return is high, and the risk of stocks does not seem to be particularly high now, so the demand for stocks by financial institutions has increased , Which has driven up stock prices.

Second, large companies repurchase their own stocks. The rise in the US stock market is related to the repurchases of large companies.

According to reports, from 2012 to 2015, companies on the SP500 list repurchased $ 4.37 trillion in stock. The top 10 companies in the United States have repurchased their own companies in large quantities. Stock repurchases raise stock prices, lower the price-earnings ratio, and increase dividends, but actual profits may not increase at all.

Xu Zhi and Zhang Yu preached in an article that the annual compound growth rate of U.S. listed companies ’U.S. stocks’ earnings reached 11%, while the company ’s compound profit growth rate It is only 8%, and the 3% gap between the two is artificially pushed up by the repurchase, which means that about 27% of the profit of US listed companies is a story bubble that is inflated by the repurchase behavior. The specific figures can continue to be discussed, but the stock market bubble and the repurchase behavior caused by the stock price is really inseparable.

In short, the rise of the US stock market is, in general terms, caused by the Fed ’s extremely expansive monetary policy (such as zero interest rates, QE, etc.); from a specific operational level, it is due to long-term investors The shift to the stock market and the repurchase of large stocks by large companies resulted. Stock prices that are out of touch with the growth of the real economy will skyrocket, and sooner or later there will be problems. New crown pneumonia and the plunge in oil prices are just the last straw that overwhelms camels.

In short, the rise of the US stock market is, in general terms, caused by the Fed ’s extremely expansive monetary policy (such as zero interest rates, QE, etc.); from a specific operational level, it is due to long-term investors The shift to the stock market and the repurchase of large stocks by large companies resulted. Stock prices that are out of touch with the growth of the real economy will skyrocket, and sooner or later there will be problems. New crown pneumonia and the plunge in oil prices are just the last straw that overwhelms camels.

In many investment bank research reports, in addition to policy-level analysis of the reasons for the U.S. stock market bubble and stock market crash, there are also a large number of asset markets involved Technical analysis of the investment strategies of participants and financial institutions.

The role of some financial market participants has changed since the subprime mortgage crisis. The chief culprit of the subprime mortgage crisis is investment banking. After the financial crisis, investment banks became financial holding companies, and their business areasAnd investment methods have also changed.

From the perspective of investment strategy, the subprime mortgage crisis is largely caused by the excessive securitization of subprime mortgages; in this U.S. stock disaster, hedge funds and assets The management agency is the most active role in the capital market. The most discussed investment strategy in the analysis of the causes of stock disasters is probably the Risk Parity Strategy. This strategy is based on the risk and return levels of different assets to determine asset allocation. Fund managers have specific volatility level targets, and they will automatically reduce their holdings once they exceed the standard.

Because in the early days of the US stock market crash, funds such as Bridgewater (the risk parity strategy was invented by Bridgewater founder Dario many years ago) and others executed risk parity strategies. A large number of stocks and other assets, some market participants accused the risk parity strategy fund is the culprit of this stock disaster. Other market participants pointed out that the risk parity strategy is to reduce the impact of external shocks on asset prices, and the risk parity strategy fund is the victim rather than the perpetrator.

How the facts can be discussed, but the outbreak of the US stock market crash proves that no matter what technical measures are taken, even if the asset types in the asset portfolio are very different, the correlation is very low. When big shocks come, such as the New Coronary Pneumonia and the Oil Crisis, any strategy to diversify risk will fail.

Some traders complain that the Volcker rules prevent them from getting the necessary liquidity in times of crisis. After the subprime mortgage crisis, the purpose of supervision and introduction of the Volcker Rules was to isolate investment banks and commercial banking businesses and restrict banks from providing funds for hedge funds and hedge funds.

Walker ’s law improves the security of financial markets, and there is no problem in itself, but it does restrict banks from providing liquidity to financial institutions with liquidity shortages. Therefore, when the stock market bubble collapses frequently, Volcker’s law does exacerbate the liquidity shortage in the capital market, which is not conducive to the stabilization of the stock market. But is there a better option?

The new coronary pneumonia epidemic and oil prices have plummeted since mid-February. You can see that new coronary pneumonia is the most fundamental and most important reason for the plunge in US stocks. From the high point of February 12th to March 20th, the US indexes all plunged, and Dow Jones fell by 35.1%. This situation is similar to the situation where the prices of financial assets such as MBS and CDO plummeted during the subprime mortgage crisis.

Once a problem occurs in the asset market, it will soon lead to a shortage of liquidity and the spread of the money market will start to rise. Measure flowThe interest rate spreads include the difference between various short-term asset interest rates and OIS and the 3-month AA financial CP and OIS spreads. When the subprime mortgage crisis broke out in 2007 and 2008, the interest rate in the money market rose sharply. After the outbreak of the stock market crash, interest rates of various asset shortages and risk-free assets also suddenly rose, which are the basic signs of liquidity shortage.

It can also be seen that although the spread between LIBOR and OIS has also increased significantly, it is still a bit far from the increase compared to 2008, which may be Various measures were taken after the financial crisis. After the stock market crash, the fall in the price of gold is also a manifestation of liquidity shortage. When people urgently need dollars, they will choose to sell gold.

After the outbreak of the financial crisis, the rise of the US dollar index is also predictable. After the economic and financial crisis broke out in developed countries since the 1980s, their national currencies will not depreciate like developing countries, but will appreciate. This is because when there is a problem in China, financial institutions and large companies have to transfer overseas funds to solve the problems of liquidity shortage and insufficient capital supplement.

U.S. Treasury bonds are a safe haven. In general, when something goes wrong with an asset, the funds will flee the corresponding market and enter the treasury market. Increased demand for national debt will increase prices and decrease yields. However, in this stock market crash, the price of US Treasury bonds did not rise but fell, and the yield did not fall but rose. How is this going? The rise in US Treasury yields shows that cash in the currency market is extremely scarce, and even Treasuries have to be sold for cash. Therefore, compared with the 2008 subprime mortgage crisis, the liquidity shortage after the US stock market crash may be more serious.

Everyone is talking about the stock market crash, but the greater threat to financial stability may come from corporate debt. Friedman once said that no matter what happens in the stock market, as long as there is no major problem with monetary policy, there will be no major event. But for corporate debt it is difficult to say so.

As mentioned earlier, due to the Federal Reserve ’s QE and zero interest rate policies, the volume of corporate bonds in the US capital market has increased dramatically. Not only that, in the US bond market, the proportion of high-yield bonds is very high. High-yield bonds generally refer to junk bonds with high risks. The proportion of high-yield bonds in the energy sector is very high. When problems arise in Saudi Arabia and Russia, energy prices fall and risks rise, it is natural that the yields of high-yield bonds soar.

Taking the interest rate of US Treasury bonds as a benchmark for comparison, the spreads of different levels of corporate bonds in the US have risen sharply. Corporate debt spreadThe generally obvious rise indicates that the market is not optimistic about US corporate bonds. It can be seen that the spread of US corporate debt has not reached the level during the sub-prime mortgage crisis, but it has clearly increased. Corporate bonds are different from stock markets, which have a strong consistency in price movements during periods of prosperity or depression. Due to different maturities and varieties, the consistency of corporate bond price trends is poor, but this may be precisely the reason why we must pay close attention to corporate bonds.

Due to the rapid increase in leverage, US corporate debt is already under great pressure. The new crown pneumonia worsened the company’s debt.

Everything depends on the development of the new coronary pneumonia situation. If the epidemic continues for a long time, a large number of highly leveraged companies will inevitably fall into bankruptcy. A large number of corporate debt defaults will make the financial crisis inevitable. Under such circumstances, the United States and the world will fall into a double crisis of finance and economy.

In this U.S. stock market storm, risk assets declined even faster than during the subprime mortgage crisis, but during the subprime mortgage crisis, Lehman Brothers and other large financial institutions The incident of bankruptcy has not occurred so far. Therefore, according to the conventional definition, it cannot be said that a financial crisis has occurred in the United States.

This stock disaster is not fundamentally different from the 2008 financial crisis. The direction of US economic development is determined by viruses

This stock disaster is not fundamentally different from the 2008 financial crisis. The direction of US economic development is determined by viruses

It can be said that up to now, the Federal Reserve A series of measures to deal with the stock market disaster are correct and timely. Understanding the series of anti-crisis measures taken by the US monetary authorities since 2008, we can better understand the series of measures taken by the Federal Reserve since March 2020, and better assess the consequences of these measures and the potential for China influences.

After the stock disaster, the Fed ’s main measures include:

On March 15, the discount window 利 rate will be lowered 1.5 percentage points to 0.25%, the statutory deposit reserve ratio fell to 0.

On March 16, it was announced that the overnight interest rate will be reduced to zero, and the quantitative easing of US $ 700 billion will be resumed.

On March 17, the Commercial Paper Financing Facility (CPFF) and Primary Dealer Credit Mechanism (PDCF) were restarted.