MCN is still in an outbreak.

Editor’s note: This article comes from the WeChat public account “chopped pepper entertainment investment” (ID: ylwanjia) , author: Liujing Mu.

MCN is still in the outbreak period.

From the development of blowouts a few years ago to the gradual rationalization of the market, MCN has long been an important part of the new media industry. In 2020, MCN will also usher in important changes. Many problems also follow.

What will be the development trend of MCN? In terms of content and overall format, where will iterate? For the market, how will the institutions at the bottom of the head break? For investors, what investment value does MCN have, and how should capital intervene?

Based on these issues, Crowray has spent hundreds of months in-depth visiting hundreds of MCN institutions at different levels, summarizing the development status of the organization, strategic layout, business model changes, future trends and other perspectives in 2019 to create “2020 China” MCN Industry Development Research White Paper, with a view to providing detailed and objective data references for MCN industry practitioners and investors.

Through the white paper, we can understand that compared with last year, MCN has greatly improved in content, strategy, and operation; MCN has a variety of development paths, which can develop independent brands, and can also form a supply chain platform. Extend to downstream entity business; pay more attention to the professionalism and institutional methodology of the reds, abandon the “brokerage” MCN institutions, and establish industry standards.

It is foreseeable that a big jump in MCN is under way.

This evolution not only means diversification of monetization models, but also involves the formation of a closed chain of the entire industry chain of supply chain, marketing, service business, and consumer end, making MCN institutions no longer a single online celebrity company. Instead, it has become an important link of the commercial body of the Internet celebrity industry, linking with various industries and fields, delivering mature content services for it, and becoming the new infrastructure of the Internet industry in the future.

Change

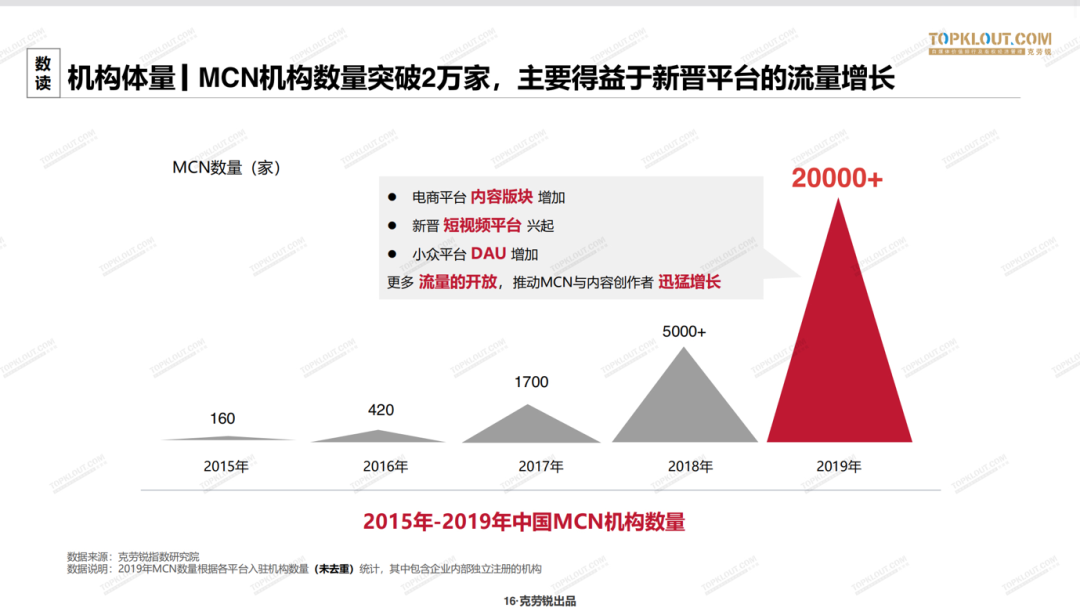

Since the wind of MCN has blown into China in the past few years, it has never stopped. Instead, it has become increasingly fierce. In the past year, the number of MCNs reached a blowout last year.

According to the Crawray white paper, the number of MCN organizations exceeded 20,000 in 2019, an increase of 400% compared to 2018In the past, the total amount exceeded the sum of the three years of 2015-2018. In all institutions, nearly 60% of the revenue scale reached 10 million, and 30% of the revenue scale exceeded 100 million. 88% of MCN institutions ‘revenues rose, and 74% of institutions’ profit margins rose.

With the increase in scale, how has the MCN organization changed?

From the perspective of the external environment, there has been a clear division of labor and clustering in the field of new media content under the Internet, which is an obvious sign that an industry is beginning to move towards industrialization.

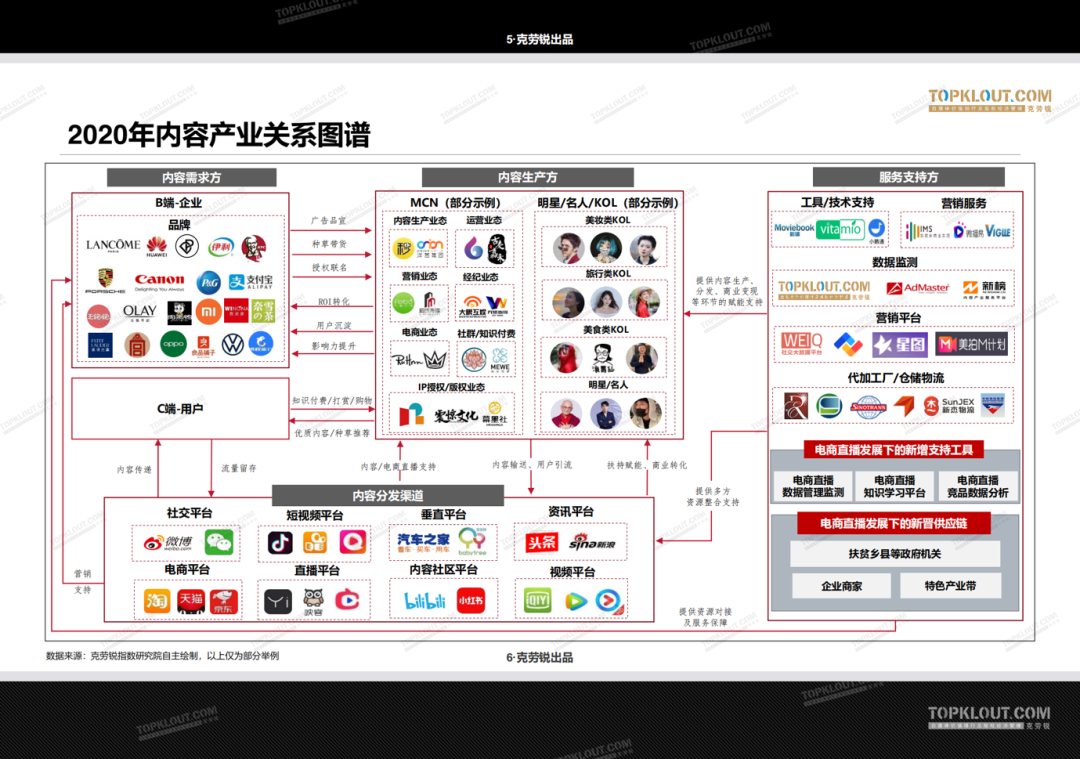

Content producers composed of MCN, celebrities and KOLs, through content distribution channels including social, e-commerce, information, short video and other platforms, and then service providers that can provide data monitoring, marketing services, and technical support After being packaged and finally delivered to the content demand side composed of B-end enterprises and C-end users, a mature industry closed loop has been completed.

Workers who want to do their best must first sharpen their tools. Obviously, as a content producer that thrives on an algorithm platform, data plays a pivotal role. Capture hot spots for content creation, analyze account data performance and adjust strategies in a timely manner, analyze operation of competing products, and analyze data of live streaming products … and so on. And service supporters who can provide these supports can accelerate the process of MCN industrialization. For example, Crowe, who published this white paper.

As a domestic third-party data monitoring agency that ranks in the value of self-media, relying on a powerful data system, Crawray can provide self-media with big data value assessment, multi-dimensional business value judgment, and copyright broker management and other technical support to promote Industry development.

MCN itself is also changing quietly.

The first is the increase of players. There are traditional radio and television systems, such as Hunan Radio and Television MCN, Heilongjiang Satellite TV and other local radio and television, as well as Wanda Film, Huayi Brothers and other old-fashioned film and television companies. In addition, celebrities, brand companies, etc., also want to take a slice of the pie.

Second, the short video gradually entered the second half. The content consumption habits and scenes of users are also changing, and people have gradually become accustomed to using live broadcast rooms as consumption scenes. In the future, this trend will continue.

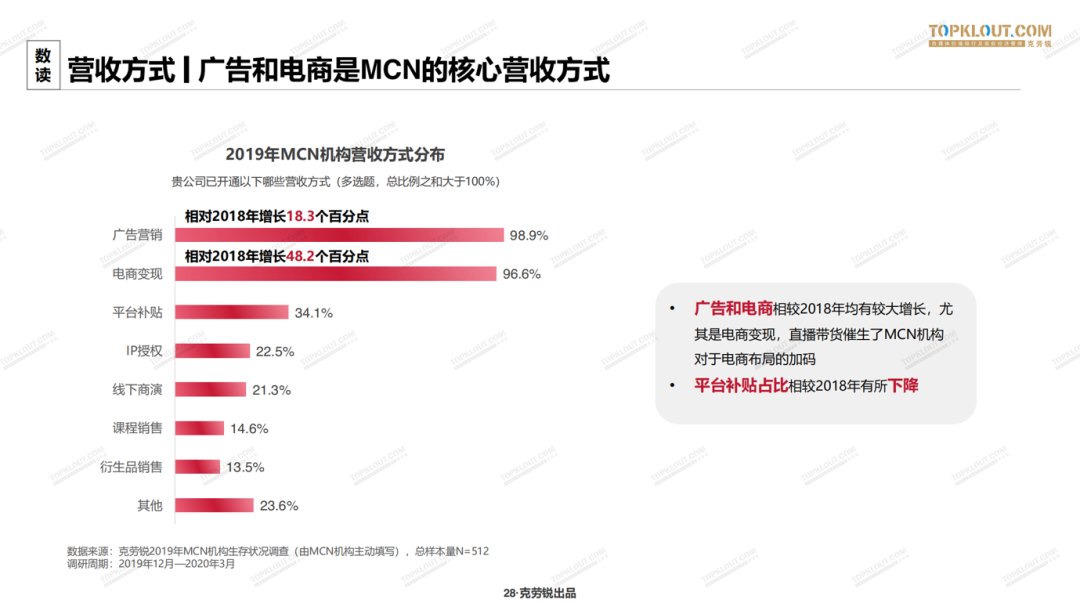

According to the white paper, although in 2019Annual advertising is still the core income, but the revenue of e-commerce live broadcast, whether it is growth rate or incremental, far exceeds advertising. This has also led to the commercial layout of major MCNs, with 40.2% of organizations choosing to focus on e-commerce live broadcast in 2020.

In terms of content, compared to before, simple hotspots can no longer attract the attention of users, the field is more subdivided, and the content needs to be more unique, vertical, and deep. In terms of content, it is also closer to short videos and live broadcasts. Along with this, the requirements for branding have become more stringent, which is a challenge for MCN’s content production.

With the expansion of the market, the relationship between the capital market and MCN has also changed subtly. The “Internet celebrity concept” has become a popular concept in the stock market, and the secondary market has gradually joined. Many listed companies such as the three-five interconnection and Wanda Movies, etc., involve the acquisition of MCN institutions. In addition, the platform is also more willing to find high-quality MCN institutions to invest.

With more entrants and capital injections, coupled with the market ’s higher and finer content requirements for MCN content, these pressures have driven MCN to quickly upgrade its industry, enhance its competitiveness, and keep up with the general trend.

The upgrade to “MCN” is already on the line.

Obviously, the development of MCN has transitioned from the wild period of “barbarous growth” to the era of industrialization. This marks the growing maturity of the MCN development road and the completeness of the industrial chain. It no longer serves as a platform attachment, but symbiosis with each other. In this way, the Red Sea in the MCN industry is far from coming.

Dilemma

However, cocoon breaking is always accompanied by pain. From the external point of view, the upgrade of MCN is a general trend, but there are still many blames to clear on this road.

In the white paper, Xiaoyu noticed a very small detail. Platform subsidies have decreased in the proportion of MCN institutions’ revenue in 2019. For the proportion of the future business layout, platform subsidies accounted for only 1%, which is a significant decrease compared to 2018.

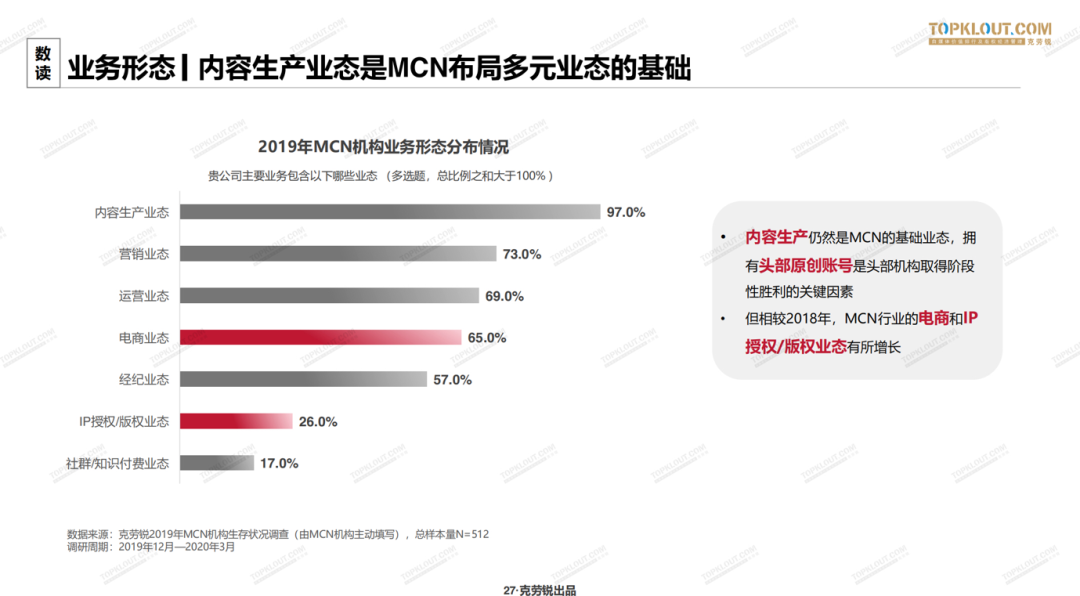

This little detail shows that the platform dividend is disappearing, MCN also realized this, and began to focus on the layout of multiple formats. As can be seen in the white paper, content production is still the basic format of MCN and the foundation of all diversified formats. But at the same time, it will also find that MCN has also increased in the layout of e-commerce and IP licensing / copyright formats.

Crawray found through research that in addition to the gradual disappearance of platform dividends, MCN’s income has also stabilized. How to break through the income ceiling has become the biggest problem that MCN institutions currently need to face.

Because content production formats account for the highest proportion of MCN institutions, behind the dilemma of realization, what is exposed is the dilemma of institutions in content production.

The first is content homogeneity. In 2019, MCN institutions gradually choose content categories that have a stronger relationship with “consumption”. In the fields of beauty, fashion, pan-entertainment, food, etc., which realize faster, a large number of MCN institutions have gathered.

This has led to the influx of too many organizations in some vertical content, further aggravating the competitive situation. This phenomenon inevitably produces a lot of homogenized content, as well as more rapid creative iteration. It is often difficult to achieve both “high-frequency creation to attract users” and “smooth high-quality content to retain users”.

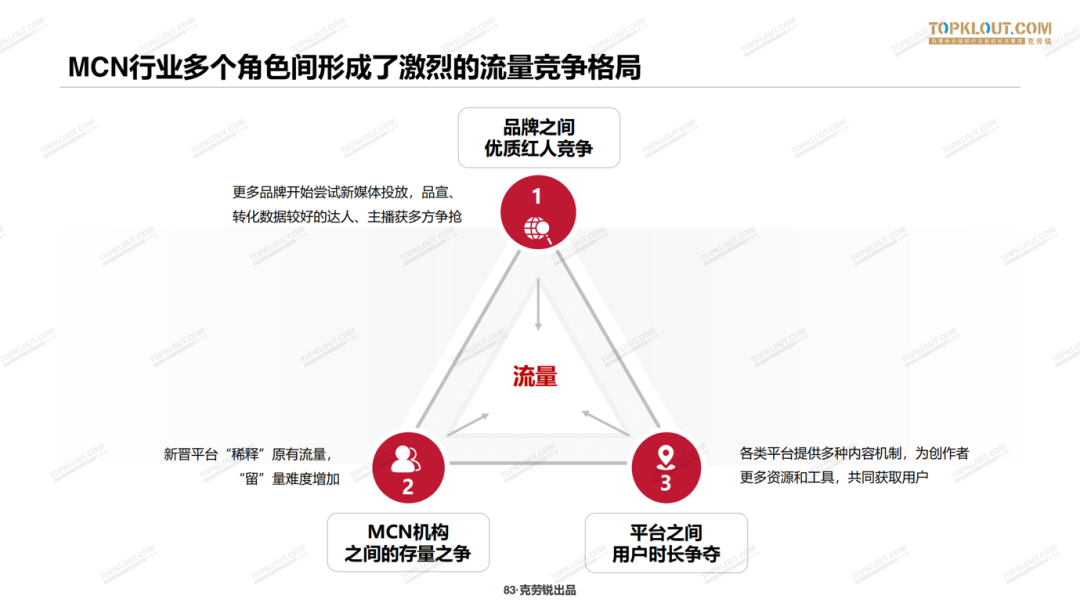

There are a lot of high-quality content that has been made first, and then there are a lot of new entrants who want to rush into the field. The battle for traffic is also starting, and every character in it is not immune to being involved in this war.

Through a lot of interviews, Crawley found that there is a fierce competition pattern from the Reds, MCN, to the platform. Internet celebrities and anchors are competing for brand investment resources; between new media platforms, they also need to compete for user time and increase stickiness to gain more users.

For MCN organizations, the situation is more complicated.

From the end of 2019, the MCN industry has seen a head pattern, the Matthew effect is forming, and “big fish eat small fish” has gradually become a trend. Anchors with high influencers and high traffic conversion rates are more likely to come from the big MCN. For the waist and tail MCN, how to increase the monetization ability and retain high-quality content producers has become the biggest anxiety.

However, the head machineThe structure also has difficulties. Cross-platform expansion of content business is a common choice for the head MCN. However, different platforms have different content and play styles, which puts forward new requirements for organizations.

At the same time, many MCN organizations still have problems in personnel training and internal management system confusion. Talents are difficult to find, difficult to retain, and difficult to manage. High employment costs, mixed talents, and insufficient manpower are the constraints of many MCNs. After all, people are the core of content creation and the key factor affecting high-quality content.

Third-party data agencies can effectively assist in relieving such dilemmas. Through Crawray’s cross-platform full-dimensional data integration, a fair, objective and transparent data platform is established to provide authoritative references to stakeholders such as institutions, celebrities, content channels, and brands.

Through Crawray ’s multi-dimensional value rankings, the influence of self-media has been more intuitively reflected. Brand owners can make clearer judgment when choosing channels and platforms to grab content; through the rankings, the reds You can also see the information and fan portraits in the relevant vertical fields, and monitor the content data, and have a clearer direction for their own ascending path; for MCN institutions, judge future development trends and traffic depressions in the vertical field through data , And the latest market trends, help the development and operation of the organization.

Breakout

Facing MCN’s increasing difficulty in realizing cash and industry ceilings, Crowley summarized the eight major paths for MCN to “cap off”, which can be roughly divided into two directions: “business” and “non-business”: >

Obviously, MCN will gather more identities, “Internet celebrity economic business bodies”, MCN gather more identities, improve the industry chain, the role is toward diversified development, and trying to output to the media in reverse, is not a pure content company , And more like a “net red economy business body”.

Among these paths, there are many who have successfully tested the water.

Weiya, the top player in the live broadcast industry, and the company behind it, Qian Xun, in addition to live broadcast e-commerce, is a huge supply chain platform. It is understood that Qianxun has now built a super SKU supply chain base that can cover multi-national goods, partition by category, and total more than 10,000.

A strong supply chain not only provides good protection for related vertical anchors, but also allows better control of the quality and delivery of goods, resulting in long-term accumulation and stable development.

Wei Nian, who belongs to Li Ziqi, has developed from a national IP to the present, and has become a new consumer brand based on fashion, food and other vertical categories. By building IP into a brand and developing products that match the IP background such as snail powder, beef sauce, salted duck eggs, etc., the business model of “IP + e-commerce” has been run through.

In addition, some MCNs are also trying to incubate industry methodologies and develop training and physical businesses. These include Onion videos from Office Ono and Degula K, as well as short video training institutions to speak freely. They rely on their own rich IP to build experience and form a methodology, and then set up online and offline training courses to feed the industry and reverse output to the media.

It can be seen that the development link of MCN will become more diversified, and further focus on brand management. With the continuous improvement of methodology, the industry will gradually become more standardized, professional and standardized.

As mentioned in the Crawray white paper, some of the earliest forms of MCN, such as the broker-centric MCN centered on the Reds, have gradually been eliminated by the market. In addition, in response to the shortage of talents, some institutions have begun to standardize the cultivation of reds to accelerate their commercial transformation capabilities.

Whether MCN is called “MCN” is not so important.

However, all of these development channels must be based on content production. As a content distribution channel, the platform and MCN are not only the content bearing, but also the mutual empowerment of values, and an important factor for whether they can successfully break through the realization ceiling.

In order to clarify the content value, commercialization capability and traffic mode of each platform, Crowray conducted an in-depth study and comparison of 8 mainstream platforms on the market, to find out the differences between the various platforms Provide more precise selection ideas.

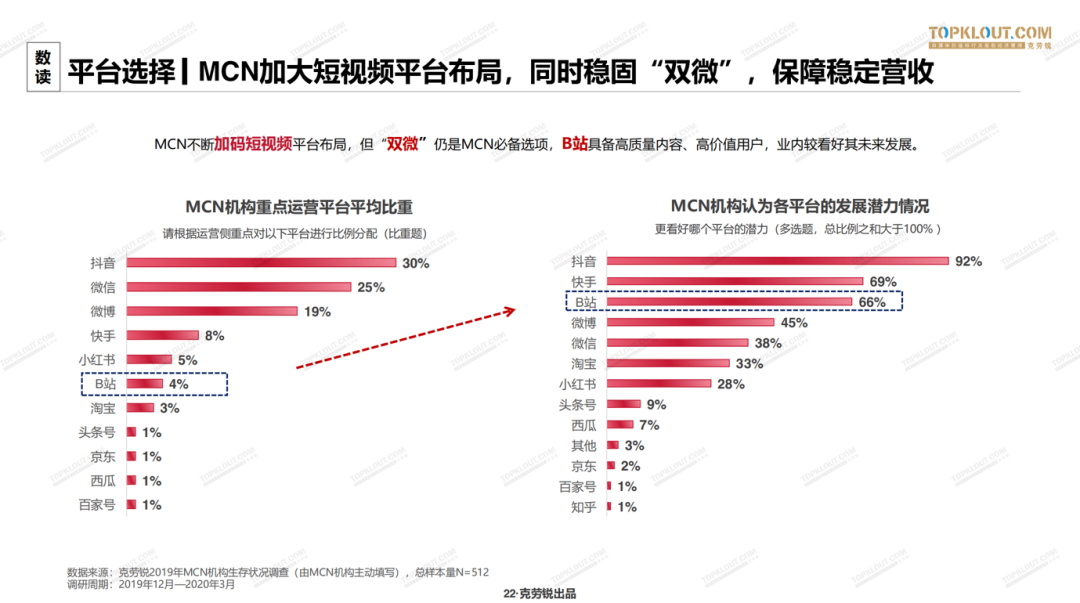

In terms of commercialization capabilities, “Double Micro” is still very stable. Xiaoyu found in the white paper that although MCN continues to lean on the layout of short video platforms, “Shuangwei” is still the “big brother” who can stabilize MCN’s revenue, and it is also a must for MCN’s military.

However, from the perspective of development potential, Station B is more optimistic about its development, and it is also a potential traffic depression in the future. As for “quick shaking”, it continues to be optimistic. This shows that, at least in the coming year, the overall pattern of new media platforms will not change much, and the increase in traffic and users will continue to slow down.

Multi-platform operation is already a megatrend for many MCNs. However, each platform has obvious differences. For MCN and the brand, it is necessary to understand the characteristics of the platform more intuitively and comprehensively in order to make more efficient and correct decisions on content selection and operation for different platforms.

In fact, Crowe has made a detailed analysis of each platform, including the platform’s traffic distribution mechanism, commercial monetization capability, support policies, and platform operations, culture, etc. Make predictions on development trends.

Crawray is affiliated with IMS (the world ’s first red-man new economy company). Since its establishment in 2014, Crawray has been devoted to the research of the new media industry, covering all circles of the industry. , With data as the core, serving the entire ecology of media. Since last year, Crowe has released the “MCN Industry Research White Paper” series. Each year, it conducts full research on hundreds of head, waist, and tail MCN institutions in the industry, providing valuable value through data analysis and industry insight Industry trends, objectively pointing out the plight of institutional development, and judging the development trend, has a strong reference significance in the industry.

The industrialization of MCN is about to erupt. At the same time, this is also a war between MCN, platforms, and brand owners. MCN is both a platform user, content producer, andIt is the extension and reflection of the value of the platform; and the brand owner as the “gold master dad” is the source of income for the organization and the platform. It also needs to rely on the content and platform for promotion. The three play against each other and are interdependent.

How to gain more benefits in this multi-party competition and maintain the delicate balance between them? The third-party professional data agency represented by Crawray provides a fair and transparent data platform as a reference, which has become a scale to maintain the balance of this discourse system.