Turning losses into profit in the first quarter cannot represent stable growth in the future.

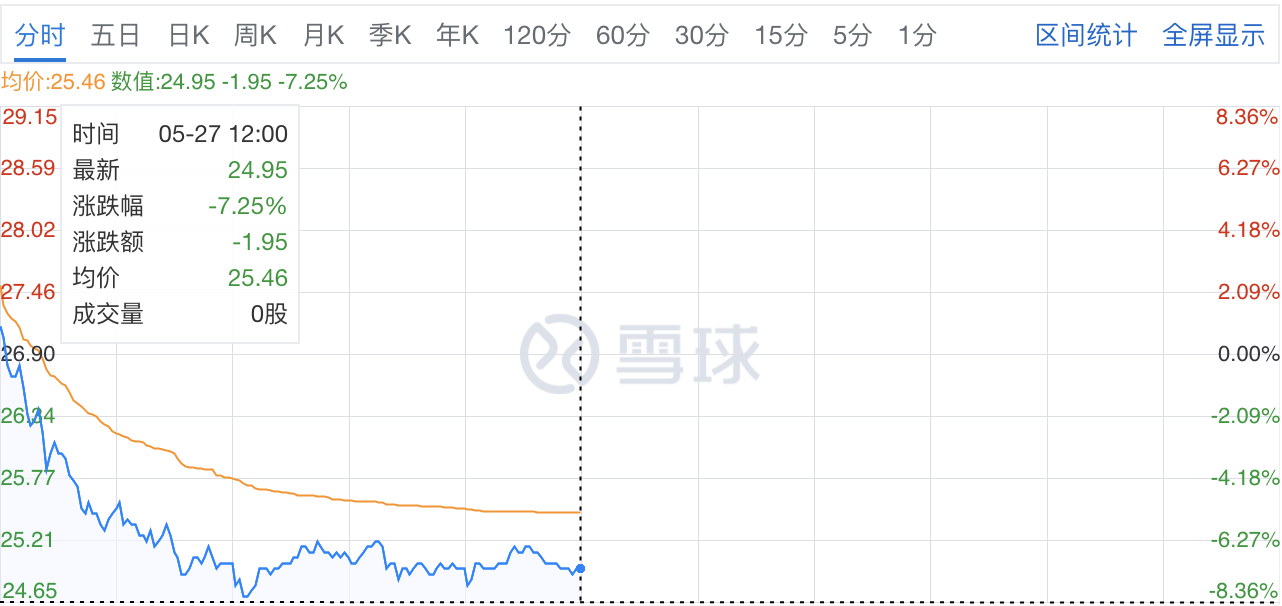

Today, Kingsoft (03888.HK) opened 2.97% higher to HK $ 27.7 / share. After the opening, there was a diving trend. It once fell by more than 8% to HK $ 24.65 / share, which was the lowest in a month.

As Hong Kong stocks were closed for lunch, Kingsoft ’s decline narrowed to 7.25%, to HK $ 24.95 / share, with the latest total market value of HK $ 34.25 billion.

Source: Snowball

After the Hong Kong stocks closed on May 26, Kingsoft released the unaudited financial report for the first quarter of 2020, and the company ’s first quarter results turned into a profit. The data shows that Kingsoft’s first-quarter revenue was 1.171 billion yuan, an increase of 32% year-on-year; the first-quarter net profit attributable to the mother was 0.06 billion yuan, and the loss for the same period last year was 67.764 million yuan.

After the company’s spin-off cloud service was listed in the United States, Kingsoft Cloud was accounted for by an associated company, leaving Kingsoft Software’s total revenue only for online games and office software. Among them, Kingsoft Software ’s online game revenue increased by 30% year-on-year to 781 million yuan, and office software and services and other revenue increased by 36% year-on-year to 391 million yuan.

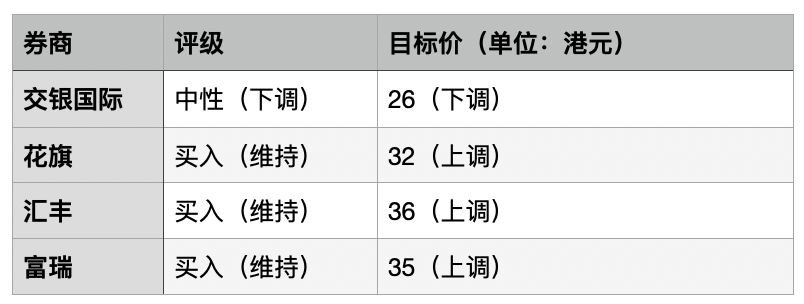

After the announcement of the financial report, a number of brokers issued research reports and adjusted their ratings and target prices, but there was a clear disagreement among brokers.

The adjustment of the rating and target price of Kingsoft by various banks Drawing:

Among them, BOCOM International believes that there is no stock price catalyst in the near future, and downgrades the rating to “Neutral”, and lowers the target price to HK $ 26. The bank said in its research report that Kingsoft ’s revenue was 4% lower than the bank ’s expectation because the game revenue was lower than expected. As users resume work and resume classes, the bank expects its game revenue in the second quarter to fall 4% month-on-month and 31% year-on-year. The seasonality of WPS promotes the recovery of authorized revenue. It is expected that revenue will increase by 30% month-on-month and 31% year-on-year.

Citigroup, contrary to the views of Bank of Communications International, said in its research report that Kingsoft ’s revenue in the first quarter was higher than the bank ’s expectations. The research report pointed out that the revenue of its game “Jian Wang” series of computer games increased by 44% year-on-year, althoughAlthough the scale and participation of users will return to normal levels after resuming work, the outlook remains stable. And its June launch of “Fingertips” is expected to continue the company’s momentum in 2020 and drive profit improvement. Therefore, Citigroup raised its target price to HK $ 32 and maintained its “Buy” rating.

Similarly, HSBC believes that after 9 consecutive quarters (from the third quarter of 2017 to the third quarter of 2019), the growth rate of 9 drops, and after the stable game in 2020 is launched, the bank believes that online games will be in the future 12 months to maintain its positive trajectory, so maintain the “buy” rating, and raised the target price to 36 Hong Kong dollars.