It’s not easy for the elephant to turn around.

Another acquisition transaction of nearly tens of billions of dollars occurred in the semiconductor field.

October 20th, SK Hai Lux official announced news that will acquire Intel’s NAND flash memory and storage business, including Intel’s NAND SSD business, NAND components and wafer business, and its NAND flash memory manufacturing plant in Dalian, China, at a price of 9 billion US dollars. Intel will retain its unique Intel® OptaneTM business, and the acquisition is expected to be completed in March 2025.

SK Hynix official news

Before this, there was news that Intel planned toto a Price sold its memory chip division to SK Hynix Inc. (SK Hynix Inc.). Affected by this news,As of the close of US stocks on the 19th, Intel’s stock price rose 0.78% to $54.58, an intraday increase of 2% to $56.23; Hai Lux shares fell 0.29% to close at $13.93, and rose 2% during the session to $14.25.

In recent years, Intel’s “slimming” is not the first time. In 2019, Intel adjusted mobile phones at a price of $1 billionThe modem business was sold to Apple, and in February this year, it was reported that Intel plans to sell the home connection chip division to MaxLinear. SK Hynix plans to acquire Intel’s NAND assets.It was reported last year.

As the world’s leading leader in the semiconductor industry, why does Intel sell storage this “founded” business this time?

Continuous losses in NAND business< /h3>

According to data from DRAMeXchange, as of the second quarter of 2020, Intel ranks sixth in the world with a market share of 11%, while SK Hynix is the world’s fifth largest NAND supplier with a market share of 12%.

NAND, also known as NAND Flash, is a kind of non-volatile storage particles. Simply put, this type of memory can stably retain data after a power failure and is usually used to manufacture hard disks and other products.

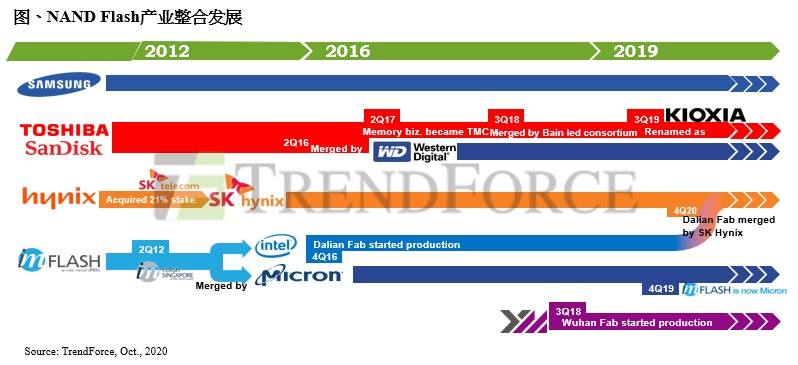

For a long time, this market has been almost monopolized by six major storage manufacturers including Samsung, KIOXIA (formerly Toshiba Storage), Micron, Western Digital, SK Hynix, and Intel. Once the transaction is completed, if the market share of Intel and SK Hynix is simply added together, according to the data of 2020Q2, SK Hynix’s market share will exceed 20% and will be close to Samsung, becoming the second largest supplier of NAND. The entire NAND market structure will be rewritten.

Source: TrendForce

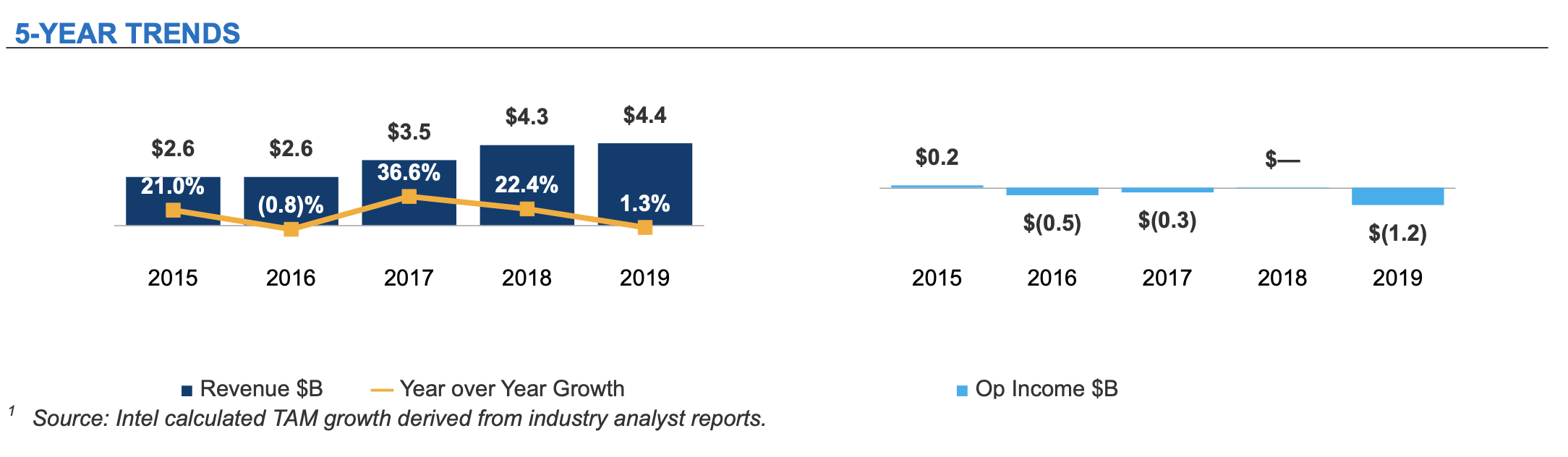

For Intel, the NAND business is not its main business. According to its 2019 annual report, the annual revenue of the Non-Volatile Memory Solutions Division (NSG) where NAND is located accounts for only 6% of the total revenue

Data shows that As of June 27, 2020, Intel’s NAND business in the first half of this year was NSG brought about $2.8 billion in revenue and about $600 million in operating profit. In the first half of the year, Intel achieved total revenue of $39.5 billion, accounting for only about 7%.

In fact, Intel’s NSG business unit has suffered losses for many years and won’t make a profit until the second quarter of 2020. According to the financial report, the business lost 540 million U.S. dollars, 260 million U.S. dollars, and 5 million U.S. dollars in 2016, 2017, and 2018, respectively. In 2019,< span style="letter-spacing: 0px;">Operating profitThe loss reached 1.2 billion US dollars, and it was not profitable until this year.

NSG revenue source:intel 2019 Annual Report

As we all know, storage is the category with the largest proportion of integrated circuits, accounting for about 1/3 . Among them, DRAM and NAND are the most important segmented products, accounting for about 95% of the total. According to statistics from DRAMeXchange, the market size of NAND Flash in 2019 reached 46 billion US dollars, accounting for 42% of the entire storage market.

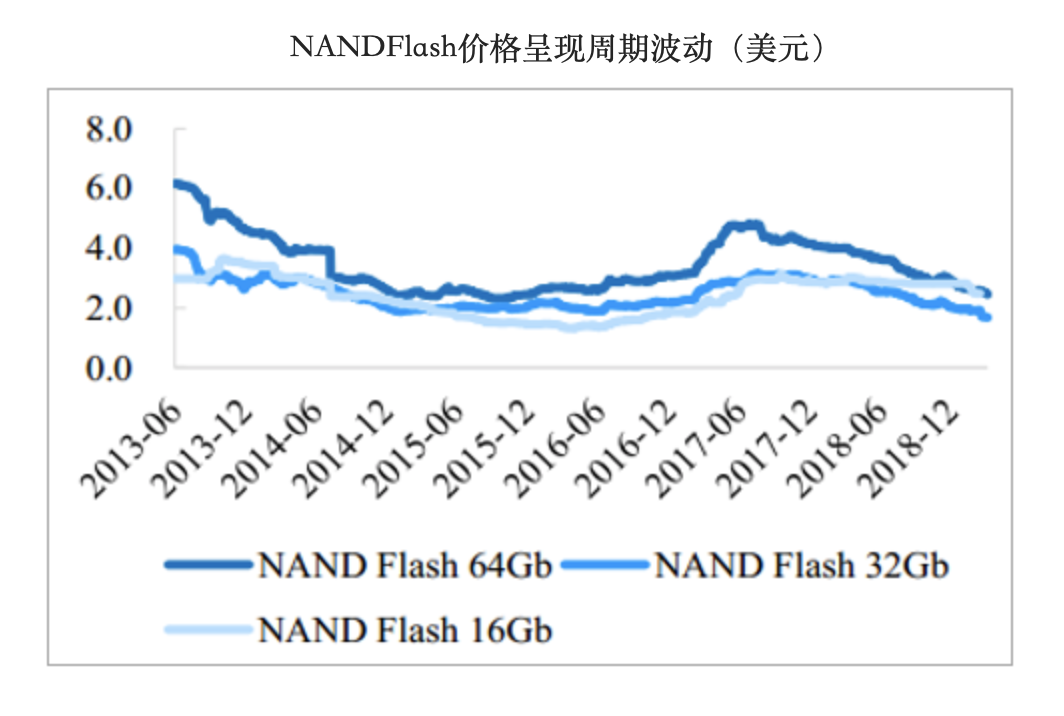

The memory industry has periodic fluctuation characteristics. From the historical performance point of view, the memory industry is always in an alternating ups and downs cycle. Its industry cycle is stronger than the overall cycle of the electronic component market. This is mainly due to the alternation of supply and demand, and the mismatch of supply and demand. relationship. Since 2015, the demand for mobile terminals such as PCs and smartphones has increased sharply, stimulating market demand for NAND. In addition, in 2017, the NAND process began to shift from 2D to 3D, but it was not as smooth as expected, affecting production, and prices rising sharply. Increased production by supply-side manufacturers.

In 2015, Intel announced the construction of the second phase of the Dalian plant, which is mainly used to produce NAND flash memory. In 2018, Samsung Electronics announced that it plans to spend 7 billion US dollars in the next three years to expand about 67% of the NAND flash memory capacity of the Xi’an plant. Flash memory manufacturers such as Toshiba and Micron are also expanding their production capacity simultaneously. The domestic NAND flash memory of Yangtze River Storage is also in 2018. Mass production began in the year.

Source: Public data compilation

According to the outlook put forward by DRAMeXchange, the supply of NAND Flash will increase by 42.9% in 2018, and the demand side will grow by 37.7%, gradually turning into balance. But facts have proved that the oversupply situation has appeared, and the price of NAND began to decline in 2018. According to Yole’s forecast, the price of NAND in 2018 has dropped by 15%. Until 2019, various manufacturers adjusted their strategies, and the price of NAND began to stabilize and rise gradually in the third quarter. In 2020, affected by the epidemic and other public events, the demand for home office will increase sharply, the recovery of supplier capacity will be slow, and the price of NAND will rise, which will also benefit manufacturers including Intel and SK Hynix.

Larger price fluctuations have also affected Intel’s profitability in the NAND business. Earlier, foreign media reported that it was affected by the significant drop in the price of flash memory chips. The development and production of flash memory also requires a lot of capital, and it is difficult to guarantee profits. Intel has been considering exiting this market for some time.

It’s not easy for an elephant to turn around, Intel must focus on key businesses

It is also mentioned in the official press release,Intel plans to transfer this transaction The funds obtained are used to develop industry-leading products and strengthen its business focus with long-term growth potential, including artificial intelligence (AI), 5G networks and intelligent and autonomous driving-related edge devices.

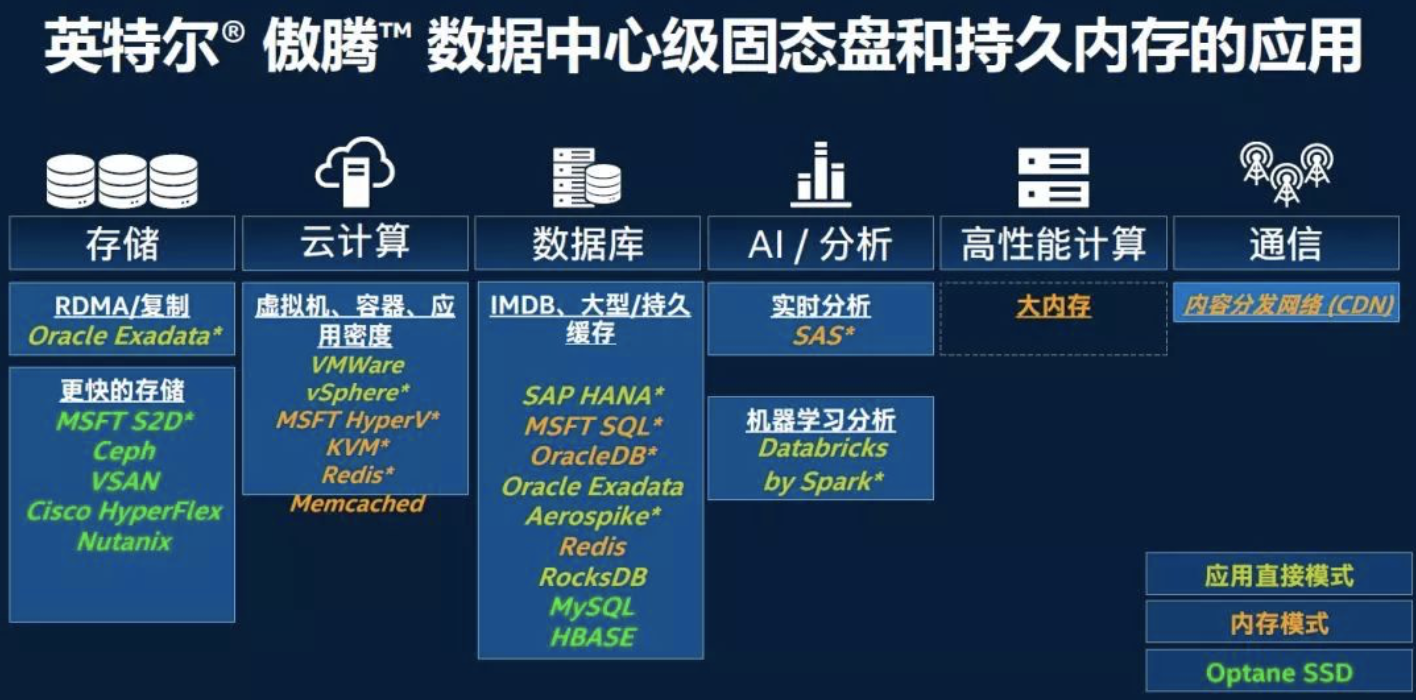

It is worth noting that this acquisition does not include the “Optane business” based on 3D Xpoint technology. According to public information, NAND flash memory products produced by Intel are mainly used in equipment such as hard disks, U disks and cameras.

The business goal of Optane is the data center market for new applications such as cloud computing, artificial intelligence, and big data. In April 2019, Intel launched the SCM product (Storage Class Memory)-Optane Data Center Class Persistent Memory SCM.

After the product was released, it has been used by many major manufacturers, and there are also corresponding storage vendors who have developed corresponding solutions, such as Alibaba, Tencent Cloud, Inspur, China Telecom, Dell (EMC) and other giants all use this program. In addition, a variety of distributed storage including VMware vSAN, Qingyun NeonSAN, SMATX, open source Ceph, etc. have also designed a variety of representative solutions based on Optane .

Source network

Data center is undoubtedly one of Intel’s core businesses. In February 2019, Intel’s new CEORobert·Swan mentioned in the open letter Intel’s transformation—— Transform from PC-centric to data-centric.

Now, in the data center (IDC) market, Intel will face more and more competition. Earlier this month, AMD’s acquisition of Xilinx was also interpreted as an important step to further strengthen its competitiveness in the IDC market. And AMD has preempted Intel to release 7nm process data center processors, and Intel announced in the second quarter of this year that 7nm process processors were six times later than its target release time. In September, this made the market full of worries about it.

Although this sale does not involve a processor, AMD is coming in aggressively, and Intel’s other product types and processors form a better match to serve the IDC market. The best choice. On the other hand, Optane is not invincible. Intel’s traditional rivals in the storage industrySamsung, Toshiba,Micron, SK Hynix has also launched or will launch similar products. How to maintain an advantage in this market and obtain a larger market share is also an issue that Intel must consider.

For SK Hynix, this will also be a good deal. SK Hynix’s annual report shows that in the second quarter of 2020, the company’s revenue reached 8.6 trillion won, an increase of 33% year-on-year, and an increase of 20% from the previous quarter; operating profit for the quarter reached 1.95 trillion won, an increase of 205% year-on-year, and an increase of 143% month-on-month; Net profit was 1.26 trillion won, a year-on-year increase of 135% and a month-on-month increase of 95%. Its financial report shows that as of March 31, 2020, SK Hynix’s cash and cash equivalents are 3.92 trillion won (equivalent to 34 billion U.S. dollars), and it has sufficient cash reserves to complete the acquisition.

From the perspective ofSK Hysley’s business structure, the proportion of DRAM business revenue in the second quarter Up to 73%, and NAND flash memory business revenue accounted for only 24%. After injecting Intel’s power, SK Hysley is expected to usher in a more balanced business structure.

On the other hand, the acquisition of Intel’s NAThe ND business can also meet SK Hynix’s needs for increasing the commercial value of high value-added products and increasing production capacity. Located in Dalian, China, Intel invested 2.5 billion US dollars in construction in 2006 and 5.5 billion in 2015 to upgrade and expand production. It mainly produces 96-layer 3D NAND flash memory.

In 2019, major OEMs have expanded their 9X-layer 3D NAND production capacity, but SK Hynix has been slow. The acquisition of Intel’s Dalian plant can make up for its lack of capacity in this area. According to previous news, in July 2019,SK Hynix is encountering During the crisis of Japan’s cut-off of supply to South Korea, I would like toNegotiating with Intel to acquire the Dalian factory and 3D NAND business .

However, some analysis pointed out that the integration of Intel and SK Hynix NAND Flash is the focus of SK Hynix’s future attention. Because the two technical routes are different, inproduct structure design and process parameters need to be adjusted ,I’m afraid I still need to go through a more painful running-in period.