Behind the domestic LCD dry turn over Samsung, the industry chain is hindered and long.

Editor’s note: This article is from the micro-channel public number “intellectual stuff” (ID: zhidxcom), Author: Yunpeng, Editor: Desert shadow.

In the past year, LCD screen manufacturers have really made no small profits.

During the epidemic, home office, study, and life have become the norm, and the demand for TVs, monitors and other products has also ushered in a rapid rise.

Since most of these devices use traditional LCD panels, the price of LCD panels has also risen, “dreaming back to the high point in early 2018.”

Chinese screen manufacturers have made a lot of money in this wave of rising LCD prices. On the other hand, South Korean screen giants such as Samsung and LG, which announced that they would withdraw from the LCD industry in 2019, have expressed that they will fight for another year!

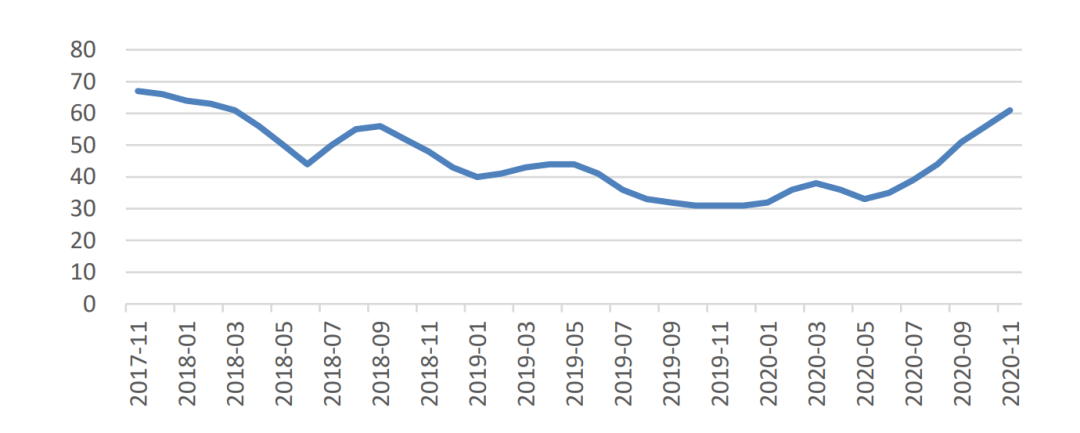

▲32-inch LCD panel price trend, data source: Wind

Standing at the moment, can we really say that Chinese screen manufacturers have no rivals in the field of LCD screens? In the field of LCD screens, do Chinese panel manufacturers really have the core technology in their hands?

From the early “lack of cores and fewer screens” under various technical blockades and restrictions of European, American, Japanese, and Korean companies, to more than half of the LCD screen market share today, how did Chinese screen manufacturers turn their backs on counterattack?

01.

Net profit soared three times,

Mainland China’s dual giants account for half of LCDs

Opening the 2020 full-year performance forecasts of various domestic screen factories, there are full of “I made money”.

Take BOE, TCL China Star, Shenzhen Tianma, Visionox and other major screen manufacturers as examples, and their net profit has increased by at least 60% year-on-year.

Among them, the highest year-on-year increase in net profit reached about 227%, which was more than three times that of the same period last year, while BOE’s net profit exceeded RMB 5 billion.

There is no doubt that behind this surge in net profit, the strong price performance of the LCD screen industry this year is inseparable. And today’s LCD screen industryFrom the final panel manufacturing side, it is already the “world” of Chinese manufacturers.

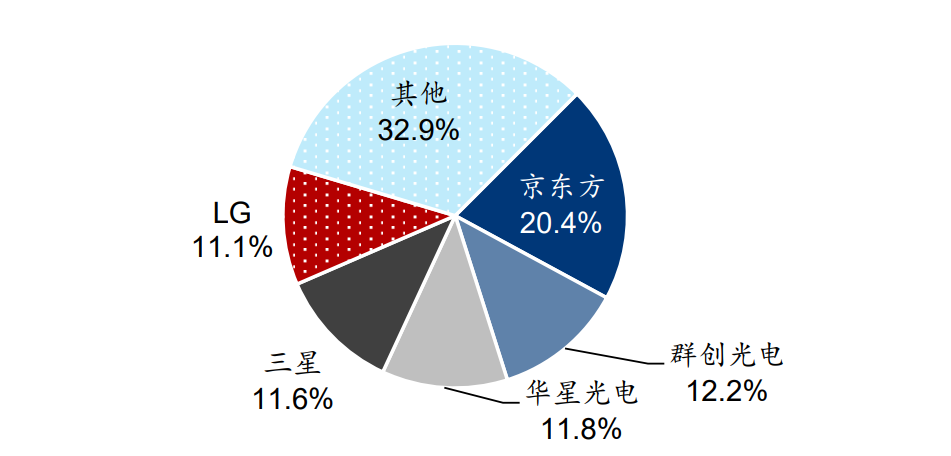

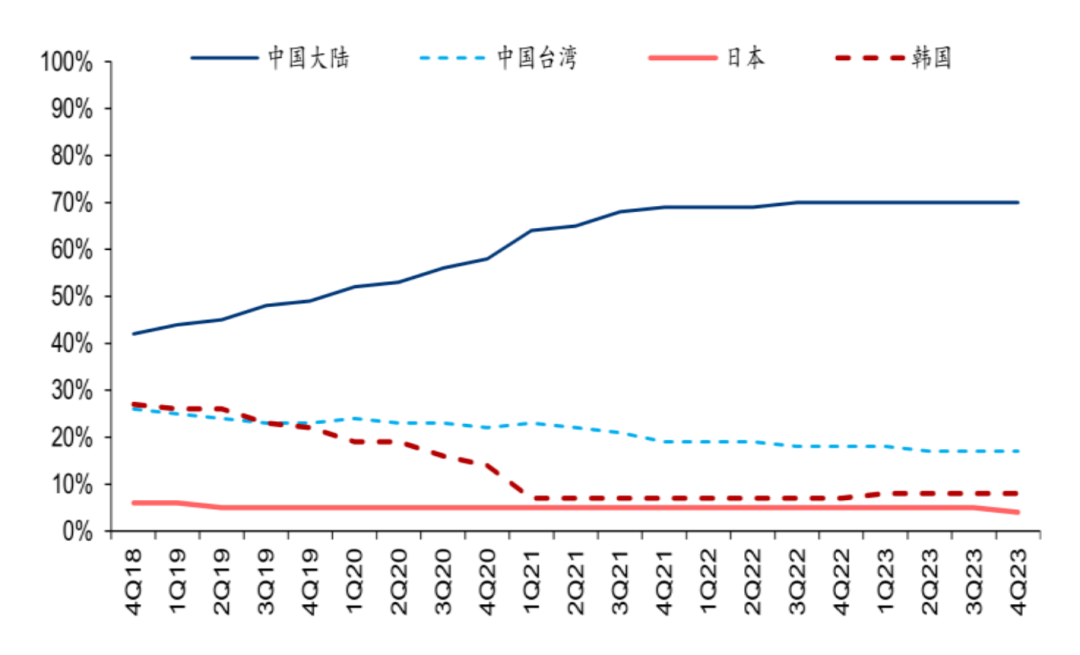

In the past 2020, the total market share of mainland Chinese manufacturers in the field of large-size LCD screens has exceeded 50%. In May last year, BOE ranked first in the world with a market share of 22.8%, and TCL China Star also reached 12.9%, ranking third in the world.

▲Global large-size LCD panel shipment area share in July 2020, data source: Omdia

Large-size LCD screens are mainly used in the production of TVs and monitors, and the total area of these two types of products accounts for nearly 90% of the total. Therefore, large-size LCD panels are undoubtedly one of the most important battlefields for LCD panel competition.

There is no doubt that the “two giants” pattern in mainland China has been formed, and this has brought stronger bargaining power and increased profit levels, which are the source of the beautiful results in the earnings forecast.

At present, BOE’s gross profit margin in the field of large-size LCD screens has reached more than 15%, while TCL Huaxing has exceeded 10%, both of which are higher than the industry average of 8.07%.

Of course, the increase in the share of Chinese manufacturers is inseparable from the gradual decline of the LCD production lines of the Korean giants and the gradual decline in production capacity.

In April 2020, Samsung announced that it would shut down all LCD panel production lines in South Korea and China by the end of 2020. In January of the same year, LG also announced that it would shut down South Korea’s LCD TV panel production lines at the end of the year, leaving only Guangzhou, China. 8.5 generation line.

▲Data source: IHS

In the first quarter of 2020, the Korean production capacity accounted for approximately 23%. By the first quarter of this year, Omdia predicts that its share will reach 8%, which is a significant drop.

Although Samsung and LG both regretted the postponementThe LCD production line is shut down, but those who should come will only be late and will not be absent.

02.

The core technology of LCD panel is still weak,

U.S., Japan, South Korea and Germany dominate

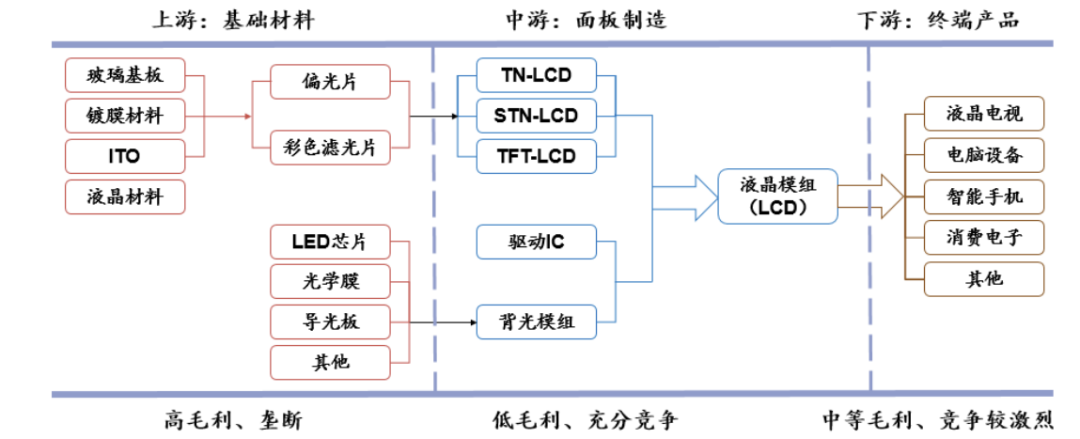

Looking at the entire LCD screen industry chain, it can be roughly divided into three major categories: raw materials and equipment, manufacturing, and terminal products.

Most of the Chinese screen factories are in the mid-stream position, which is the assembly and production of panels. The products that come out of the production line of the Chinese screen factory are basically a packaged screen module, which can be directly sent to the product factory of the terminal manufacturer.

▲LCD screen industry chain situation

On the surface, Chinese screen makers basically do “processing with supplied materials”, which brings out our most obvious shortcoming, that is, our lack of control of upstream core technologies.

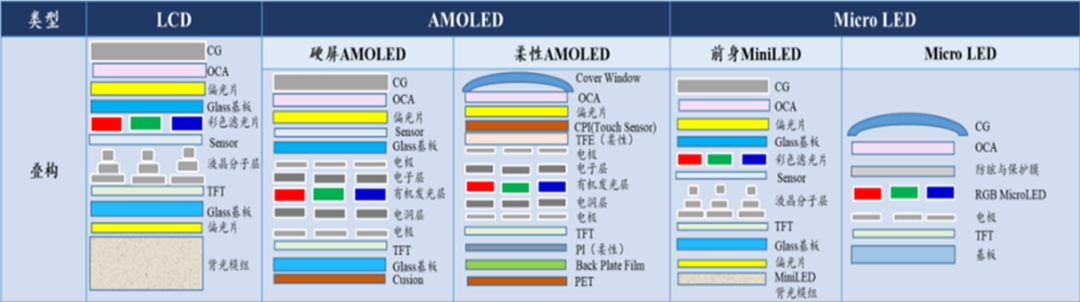

Nowadays, most of the screens used in most TVs, laptop computers, PC desktop computers, and various car monitors are still LCD panels.

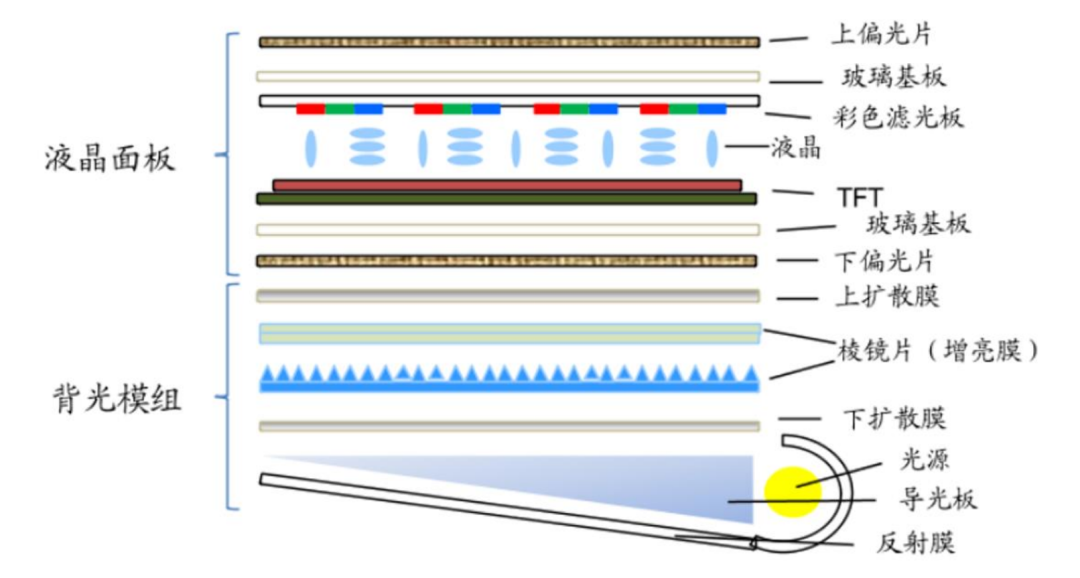

These screens seem to have a thickness of only millimeters, but in fact, an LCD screen is made up of many layers of film when taken apart.

Since LCD screens are “passively illuminated” and need a light source, LCD screens are naturally composed of two large parts: a liquid crystal panel and a backlight module.

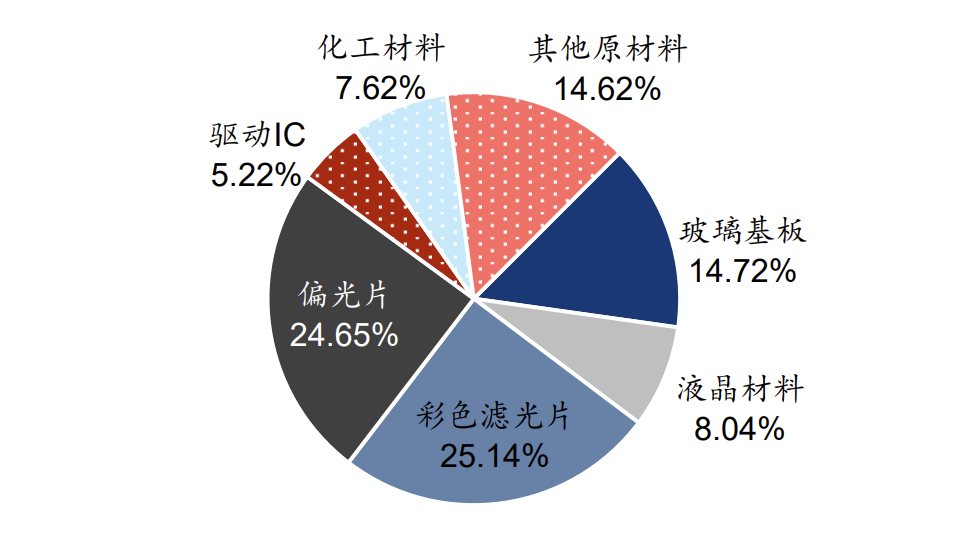

In terms of the panel itself, the two parts with the highest cost ratio are polarizers and color filters. The sum of the cost ratios of these two parts alone is about 50%. This material sounds familiar to us, but the technical barriers to actual production are very high.

▲Rough structure of edge-lit LCD panel

Currently, polarizers and color filters are almost dominated by Japanese and Korean companies. Nidec, Sumitomo Chemical, Sanli Chemical, South Korea’s LG, and Samsung are the world’s top five polarizer giants, occupying an absolute dominant position.

Look at the color filter side. At present, the main screen manufacturers choose to make their own products. For example, LG’s self-made ratio exceeds 90%, and Samsung has more than 75%.

The domestic leading LCD manufacturers, such as BOE and Tianma, all make less than 30% of their own products, and the remaining 70% will be purchased from Japan Toppan Printing, Dainippon Ink, Japan Toray and other companies.

Currently, domestic screen manufacturers hope to increase the proportion of self-made localization of color filters, and they are also supporting supply chain companies. For example, Dongxu Optoelectronics invested 3 billion yuan in 2015 to introduce the technology and production line technology of Dainippon Ink , And achieved mass production and shipment in 2018.

However, domestically produced color filters are mostly low-end and mid-range, and there is still a big gap in the domestic high-generation color filter field that needs to be filled.

▲55-inch LCD panel raw material cost split

Of course, since LCD screens are mentioned, liquid crystal materials are indispensable. The full English name of LCD is “Liquid Crystal Display”, which translates to LCD screen, which is what we usually call “LCD screen”.

Liquid crystal is the basic material of liquid crystal panels. At present, in the field of mixed liquid crystal materials, German and Japanese companies represented by Merck, Japan, and DIC have monopolized over 90% of the global market share. The liquid crystal plays a vital role in the performance of the panel.

Currently, domestic liquid crystal materials are on the low end, and many representative companies are increasing their research and development efforts. For example, 800 million LCD has now become BOE’s largest domestic LCD supplier in 2017. In addition, Chengzhi Yonghua, Jiangsu Hecheng and other companies are also conducting research and experiments in this field.

In addition to the LCD panel itself, the layer of glass covered on it is also very important, and the cost ratio is close to 15%. The glass used in the LCD panel is actually quite special. It is made of aluminosilicate. Alkali-free glass substrate composed of other components.

It looks like thisIt is a piece of glass, but wanting to produce it involves technical barriers in many aspects such as process, formula, and equipment.

In the field of LCD screen glass, the Corning family of the United States has eaten 50% of the market. It can be said that it is the undisputed industry overlord. Japan’s Asahi Glass and Nippon Electric Glass rank second and third. American and Japanese companies together accounted for nearly 90% of the LCD glass market.

As mentioned earlier, LCD screens need to be “lighted” by the backlight module to be able to light up. Therefore, the backlight module is also a vital part, and this part of the cost accounts for about one-fifth of the entire LCD screen module. One.

The production technology of the backlight module itself is not high, and it is a labor-intensive industry. This is also what domestic companies are good at. However, the backlight module is composed of various optical films. At present, 80% of the global optical film production capacity is They are all monopolized by overseas giants, among which Japanese companies are absolutely dominant, such as the familiar Mitsubishi, Toray and so on.

Just like chip production, we are caught by the lithography machine. In the field of high-end screen production, we are also restricted in terms of production equipment.

LCD screen production mainly involves equipment such as technology, measurement, inspection and repair, and the more advanced equipment of this type is basically produced by Japanese, Korean and Taiwanese companies.

For a simple LCD screen, there are actually many upstream subdivision fields, and each field has accumulated a large number of key technologies. In these materials and equipment fields, the development of China’s LCD screen supply chain is still in its infancy.

Although domestic screen makers are playing an increasingly important role in the midstream production and manufacturing sector and have no rivals in LCD market share, there are still many gaps to be filled in the core technology field of LCD panels upstream.

▲TCL Huaxing 8.5 generation LCD production line

Generally speaking, the closer to the middle and lower reaches, the larger the size of the enterprise and the heavier the right to speak in the supply chain. In fact, although the upstream enterprise has the core technology, it leavesWith the Chinese screen factory, their technology cannot be converted into products efficiently.

The ability to make LCD technology large-scale, high-efficiency, high-yield, and low-cost landing into a tangible panel module that can be used in terminal products is a capability in itself.

Leaving Chinese screen makers, upstream material companies in the United States, Japan, and South Korea have no skills and cannot convert technology into products. This is one of the reasons why Chinese screen makers have become more and more powerful in the LCD field.

He has a need, you have the technology, I will help you realize it. This is what the Chinese screen factory is good at.

The status of Chinese screen manufacturers as the “manufacturing center” in the LCD market cannot be replaced by other countries in a short period of time.

03.

20 years of catching up, from lack of core and screen to grab food from the tiger’s mouth

We know that the screen industry can actually be called the display semiconductor industry, and its technical content is still very high. In the early years, overseas giants blocked these technologies very strictly.

Samsung, LG and other South Korean display panel giants have always had an unquestionable voice and leadership in the field of screens. For example, in the field of high-end OLED screens, Samsung and LG have been steadily sitting on small and large sizes for a long time. First, and far ahead of domestic manufacturers.

However, in the field of LCD screens, the two domestic head screen manufacturers have already eaten more than half of the share, and they have also shown a crushing advantage to South Korean manufacturers in terms of net profit. How did domestic screen companies do it step by step?

Although Japanese and Korean companies are now louder in the screen industry, it was actually the Americans who invented the liquid crystal display technology around 1970. However, for various reasons, the United States “wasted halfway”, and Japanese companies have promoted the liquid crystal display technology. And finally landed in mass production.

The first industrialization of LCD technology was in the 1990s. About 30 years have passed since today. In 1990, the joint ventures of Japan’s NEC, IBM, and Toshiba, DTI and Sharp, launched their first large-size products. Color LCD production line.

From this period, Japanese companies have accumulated a large number of key technologies in the LCD panel industry, and the formulation of industry standards is often jointly formulated by these companies.

Glass substrates of Asahi Glass and Electric Glass, scanning lithography machines and stepper lithography machines of Nikon and Canon, color films and polarizers of Nitto Denko, advanced printing equipment of Dainippon Printing, etc. They are all accumulated during this period.

▲Nikon stepper lithography machine

In the mid-1990s, during the recession of several LCD panels, South Korean companies represented by Samsung and LG began to make large-scale countercyclical investments and obtained many Japanese LCD technology and related talents. Taiwanese companies also During the LCD recession in the late 1990s, many Japanese LCD industries were transferred.

There is a saying, “Who doesn’t eat dumplings?” But at the same time, every family has a hard-to-read experience. The development of the industry will go through various cycles. Undertaking industrial transfers and countercyclical investment acquisitions are all Some ways of the initial development of the LCD industry in mainland China.

At the beginning of the 21st century, China’s head panel companies began to introduce and accumulate technology. In 2002, Shanghai Broadcasting Group and Japan’s NEC jointly established Shanghai Broadcasting Corporation NEC, and built the first LCD production line in mainland China.

The following year, BOE acquired Hyundai’s LCD business, and through technology absorption and digestion, it independently built a fifth-generation LCD production line in China and put it into production in February 2005.

▲BOE 5th generation LCD production line

In the early stages of technological development, it was commonplace to face blockades from overseas giants. When you don’t have it, they won’t give it to you. Once you have it, they will immediately open up, cut prices, and suppress it. In the development of domestic LCD technology, such a routine is also the same.

The step-by-step development of the domestic LCD screen industry needs to seize the industry’s countercyclical investment opportunities, and at the same time, it needs the enterprise’s own hard work, policy and capital support.

The opportunity is here, we must be able to seize it.

As BOE announced in 2009 that it had begun to expand into the high-generation line, Samsung, LG, Sharp and other Japanese and Korean giants also began to plan to set up high-generation panel factories in mainland China. From 2011 to 2015, multiple 8.5-generation production lines of TCL China Star, BOE, and China Electric Panda have been put into production one after another.

2017In December, BOE’s Hefei 10.5-generation production line was officially put into operation. This is also the world’s first 10.5-generation production line. A higher-generation production line means a significant improvement in cutting efficiency for larger sizes. From catching up to overtaking, Chinese screen makers have begun to take the lead in the LCD industry.

▲BOE 10.5 generation LCD production line

In the future, the “big” in terms of quantity and the “strong” in technology is the direction that domestic screen companies still have to work hard on. According to Yuan Feng, the vice president of BOE, the LCD industry will have a golden period of about 10 years in the future, and the entire LCD industry has entered a stage of integration.

On August 28, 2020, TCL Huaxing announced that it would spend 7.6 billion to acquire Samsung’s 8.5-generation LCD production line in Suzhou. One month later, BOE announced plans to acquire the 8.5-generation and 8.6-generation LCD production lines of CLP Panda. China’s dual giant pattern has become more prominent.

DSCC predicts that with the release of the production capacity of Chinese screen factories, the shutdown of Korean manufacturers’ production lines, and acquisitions, by the fourth quarter of 2022, the proportion of LCD production capacity in mainland China will reach 70%, and Omdia also predicts this year The total LCD production area share of BOE and TCL Huaxing will reach 40%.

▲ Trend chart of global LCD production capacity, data source: WitsView

04.

Can China’s display manufacturers sit back and relax on the LCD track?

According to the forecast of mainstream data institutions, the global LCD industry will maintain a relatively stable development trend. From 2020 to 2022, the LCD panel shipment area will basically be between 310 million square meters and 316 million square meters. between.

With the withdrawal of Korean manufacturers and the further release of high-generation production line production capacity of mainland manufacturers, domestic screen companies seem to have no major challenges in the field of LCD panels for the time being.

However, as mentioned above, the domestic LCD industry chain still needs to catch up in terms of core materials and core production equipment, and there are still many gaps to be filled.

In these upstream fields, there are high technical barriers, large capital needs, and a large number of talents. This is an urgent matter. It is necessary to slowly “eat” through continuous investment, the determination of the company itself, and the support of policies. Hard bones”.

On the other hand, a question is obvious. Why are South Korean giants such as Samsung and LG withdrawing from the traditional LCD screen competition. Is it really “unbeatable”?

In fact, these giants have already targeted many new tracks, including high-end OLED, QLED, MiniLED, MicroLED and so on.

▲Main screen types and general screen structure

In terms of shipments alone, the largest screen market currently depends on the mobile terminal. The annual shipment of smart phones is about 1.3 billion, and smart phones are almost always owned by one person, unlike TVs that are based on families. Unit purchase.

In the smart phone market, it is a general trend that OLED screens replace LCD screens. OLED’s excellent display effect, low power consumption and high response speed are all necessary features of current high-end flagship phones.

In the field of small-size OLED, Samsung has eaten nearly three-quarters of the market, and this industry position is still difficult to shake in a short period of time.

In the high-end TV market, in recent years, OLED TVs have gradually moved towards the public’s field of vision. Quantum dot TVs and MiniLED TVs have been mass-produced one after another. These new display technologies have display effects that far exceed those of the traditional ones. LCD TV with LCD screen.

At present, large-size high-end OLEDs are almost firmly controlled by LG. LG has blocked the WRGB (white, red, green, and blue) pixel arrangement with better display effects in large-size areas through patents. Other opponents who want to achieve close display effects can only change lanes to catch up, which requires a lot of time, manpower and financial resources.

If you say that LCD screens are eating surplus markets, then more opportunities lie in these emerging markets.Samsung and LG use their first-mover technological advantages in the field of display technology and have already set up numerous barriers on these new tracks.

This year, Samsung will test the waters to produce 3 million MiniLED TVs, and the more complex MicroLED TV Samsung plans to land as early as next year. In addition, Samsung has also bet on quantum dot technology through the use of quantum dots and LCD The combination of OLED creates its own unique display technology.

In the field of cutting-edge screen technology, Korean companies are still leading the world. For domestic screen manufacturers, winning the LCD screen market share may be just the “first step in the long march” of the screen industry.

05.

Conclusion: LCD consolidates advantages,

But the new screen track is full of challenges

The LCD screen market may continue to maintain stable development in the past two years, and the leading advantage of domestic screen manufacturers will be further expanded. LCD TVs have gradually become a thing of the past, and the explosion of the smart car market may allow LCD screen companies to find some more opportunities.

There is no doubt that with the advent of the 5G, IoT, and AI era, smart devices will explode, and the demand for “screens” will only increase. However, high-end consumer electronic devices represented by mobile phones, tablets, PCs, smart wearables, and smart TVs are all shifting to the new track of OLED, QLED, MiniLED and other screens.

Samsung, LG and other veteran Korean giants seem to be retreating step by step, but in fact they secretly used their money to spend their money on the “knife edge” in their eyes. For Chinese screen companies, changing from a global “manufacturing center” to a “R&D center” is still a long way off.