After the release of Pinduoduo’s Q3 earnings report, the increase in stock price is indeed surprising. Behind the surge in stock prices, we might as well take a look at what data from Pinduoduo has been recognized by investors.

Editor’s note: This article is from the WeChat public account“Songguo Finance” (ID: songguocaijing1).

After the e-commerce giant Ali released the new quarter’s financial report, Pinduoduo also released the new quarter’s report card. After the Q3 financial report was released, Pinduoduo’s share price rose more than 20% and shocked the capital market, and its total market value passed the $160 billion mark.

It is worth noting that JD’s current market value exceeds 130 billion U.S. dollars, which is less than 30 billion U.S. dollars away from Pinduoduo. It is reported that Jingdong will release a new financial report on November 16. It is estimated that many officials are also calculating the chances of Jingdong’s market value catching up with Pinduoduo.

Returning to the financial report itself, what data of Pinduoduo has been recognized by the outside world this quarter? Behind the dazzling data, how should we objectively view the development value of Pinduoduo in the future?

Pingduoduo’s stock price rose sharply due to its first profit in a single quarter

After the release of Pinduoduo’s Q3 earnings report, the price increase was indeed surprising. Behind the surge in stock prices, we might as well take a look at what data from Pinduoduo has been recognized by investors.

From the perspective of revenue, Pinduoduo’s revenue was 14.21 billion yuan in this quarter, an increase of 89.11% year-on-year; under non-GAAP, it achieved a net profit of 466.4 million yuan, the first quarterly profit. With the improvement of the domestic epidemic situation, the growth rate has also rebounded from the previous quarter. Judging from the three quarterly financial reports released this year, Pinduoduo’s revenue growth rate is picking up.

Behind the realization of profitability, the main reason is that Pinduoduo’s operating loss rate has significantly narrowed this quarter. Prior to this, Pinduoduo had been in a loss-making situation, but this quarter’s profitability could indeed boost some investors’ confidence in its performance.

In addition to good revenue and profit performance, Pinduoduo’s performance on these core data is also worthy of recognition:

· In the 12 months ending September 30, 2020, Pinduoduo’s GMV was 1,457.6 billion yuan, a year-on-year increase of 73%;

· In terms of user data, the number of active buyers of Pinduo for many years reached 731.3 million in this quarter, an increase of 36% year-on-year. The number in the previous quarter was 683.2 million, a net increase of 48.1 million;

· This quarter, Pinduoduo invested 10.72 billion yuan in market expenses, with a market expense ratio of 70.88%, a year-on-year decrease of 21.07;

· Operating loss rate narrowed from 37.16% in Q3 2019 to 9.12% at present;

Among them, Pinduoduo’s annual active buyers enter the 700 million threshold. This is indeed an important node. From “Pinduoduo, which is used by 500 million people” to “Pinduoduo, which is used by 700 million people”, it takes one time At the same time, this also further widened the gap in user scale between JD.com and Pinduoduo.

Judging from the performance of the above core data, it is indeed remarkable. It can also be seen that Pinduoduo has a certain ability in market expenses and turnaround in the short term.

Behind the surge in stock prices, some doubtful voices appeared in the capital market. Some investors speculated that there might be the possibility of institutions pulling up, believing that Pinduoduo’s stock price rose a little abnormally. In addition to this possible factor, looking closely at this financial report, perhaps we can also see that behind the bright financial report, the anxiety of Pinduoduo cannot be ignored.

Pinduoduo is still anxious behind the brilliant performance

In this earnings conference call, Pinduoduo executives answered many analysts’ questions about the new business, Duoduomai. Ma Jing, Vice President of Finance of Pinduoduo, explained that shopping for food is an important opportunity for Pinduoduo and will continue to invest in related plans.

In the opinion of many insiders, according toPinduoduo subsidies to grab the market, and Duoduomai will still implement this strategy. Once the follow-up vigorous promotion of Duoduobuying, Pinduoduo’s follow-up profit may not be optimistic. In addition to the anxiety on the level of profitability will continue to take place, what other factors will affect investors’ valuation judgments on Pinduoduo?

User-customer unit price influences GMV scale, and Pinduoduo ARPU is lower than Ali and JD

In the e-commerce industry, in addition to revenue, the number of active consumers and GMV are also key data that investors consider. In this quarter, Pinduoduo’s GMV increased by 73.8% year-on-year. From 2019Q3 to 2020Q2, the year-on-year growth rates of Pinduoduo’s GMV were 143.68%, 113.44%, 107.61%, and 78.92%, respectively. The growth rate has declined.

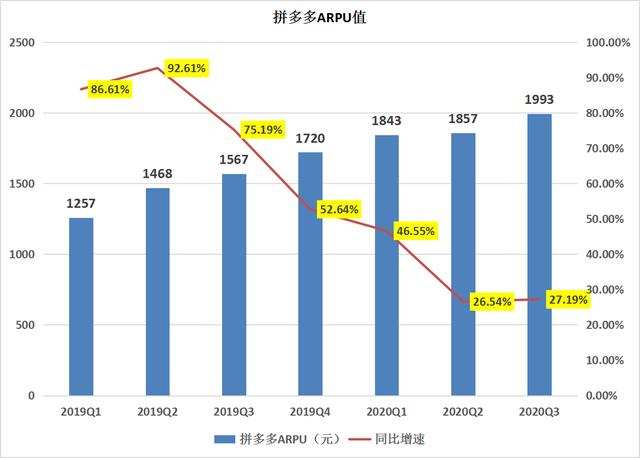

Although Pinduoduo’s annual active buyers reached 731.3 million, the eye-catching user growth failed to drive Pinduoduo’s GMV to achieve higher growth. According to industry insiders, this is mainly affected by the limited increase in Pinduoduo’s ARPU value. In this quarter, Pinduoduo’s ARPU value was 1993 yuan, an increase of 27.19% year-on-year.

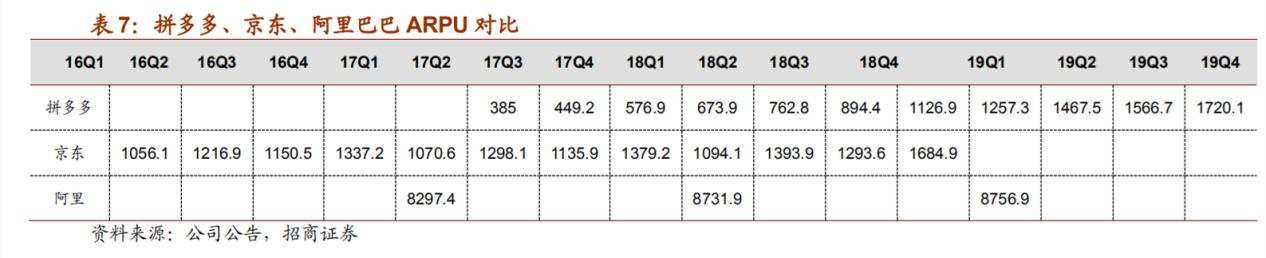

In addition to the year-on-year decline in the data, one aspect of Pinduoduo that worries some investors is that its single-user customer unit price is lower than that of Jingdong and Ali. In recent quarters, neither Ali nor JD.com has publicly announced the GMV of the platform. However, from previous research reports of China Merchants Securities, we can also see that the gap in ARPU between Pinduoduo and Ali and JD.

(Tuyuan China Merchants Securities)

Judging from the data in the Q4 quarter of 2019, Pinduoduo’s ARPU was 1720.1 yuan, far lower than Ali’s fiscal year of 8756.9 yuan. Not only is there a big gap with Ali in ARPU, it is also difficult for Pinduoduo to catch up with JD on this data. Why is Pinduoduo’s ARPU low? This may be closely related to the products sold by Pinduoduo.

In the third quarter, Pinduoduo’s user visit frequency, number of categories visited, and average daily usage time all increased. The peak order volume on weekdays exceeded the 100 million single mark recently. The main agricultural products are indeedLet Pinduoduo take a differentiated route to break a blood path in the e-commerce field, which will also drive users to consume high-frequency on the platform, thereby promoting the growth of GMV, but Pinduoduo is not worth digging this part of products from users.

In order to increase the ARPU value, Pinduoduo has also made a lot of efforts in the supply chain of high-priced goods, such as the layout of the supply chain in cosmetics, clothing, 3C products, etc., but the number of high-priced goods is currently insufficient. Recently, Apple has rectified its supplier channels, and Pinduoduo’s practice of borrowing subsidies to drive sales of iPhones has also been affected.

In addition, starting from the second quarter, Pinduoduo’s subsidies have shifted from electronic products with high unit prices to agricultural products with low unit prices, and subsequent subsidies are likely to focus on agricultural products. Although the agricultural product + subsidy strategy can attract users’ high-frequency consumption, since the ARPU contributed is not as high as the high-priced electronic products, this will also increase the GMV of Pinduoduo in the future.

The scale of users determines the volume of e-commerce, and Pinduoduo faces user growth anxiety

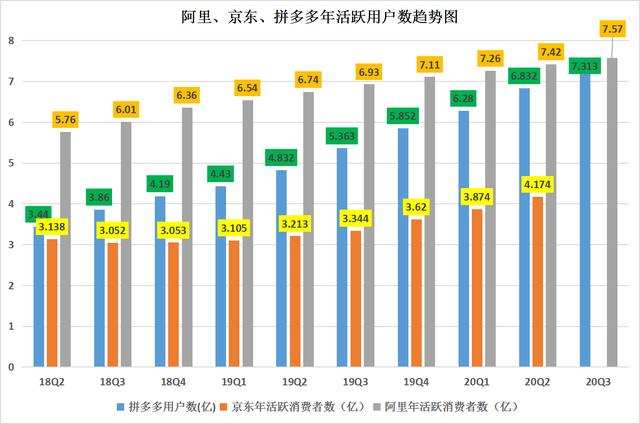

For investors, the user scale and user growth rate of e-commerce platforms are the key to measuring the company’s value. According to the year-end active users disclosed by Ali, JD and Pinduoduo, they were 757 million, 731.3 million, and 417.4 million, respectively.

Backed by Tencent WeChat, this may be an important reason why many investors support Pinduoduo. According to Tencent’s financial report, the monthly active accounts of Tencent’s WeChat and WeChat in the third quarter were 1.21 billion, a year-on-year increase of 5.4%. WeChat has 1.2 billion users. It is a normal thing for Pinduoduo to maintain a huge user base, but whether its user base growth rate has been maintained at a relatively high level, that is what Pinduoduo needs to solve. .

On the one hand, it is obvious that Pinduoduo borrowed tens of billions of subsidies to gain customers. This is why it was possible to add users faster after the subsidy was introduced last year, but the stickiness of platform users is not high. Once the subsidy is stopped, whether the follow-up will bring about stable user growth remains variable. The slowdown in user growth and the low retention rate will affect Pinduoduo’s performance in user data.

On the one hand, Tencent’s WeChat is also diverting to Jingdong, and Jingxi is at the secondary entrance of WeChat. In the last quarter, JD.com added 30 million in a single quarter, a year-on-year growth rate of 29.9. Among them, Jingxi, which focuses on sinking markets, became JD’s mining incremental users. The effective assistant . In the sinking market, Alibaba and JD.com are making efforts. Pinduoduo is not only trying to keep its base camp, but in the WeChat ecosystem, it is also facing robbing JD for incremental users. Pinduoduo’s traffic anxiety is not small.

As of September 30, the balance of Pinduoduo cash, cash equivalents and restricted cash was 44.53 billion yuan, of which 38.813 billion were restricted cash, and restricted cash included the occupation of merchants’ funds. If the effects of accounts payable and merchant deposits are excluded, Pinduoduo’s net operating cash flow is basically outflow. From this, it can be seen that the pressure of money is prominent in the daily operation of Pinduoduo.

Except for restricted cash, Pinduoduo’s cash and cash equivalents are only 5.716 billion yuan-this figure shows that Pinduoduo’s remaining funds are not sufficient. Relying on the capital of upstream merchants to obtain operating cash flow, many people in the industry say that Pinduoduo’s method of maintaining cash flow is unhealthy.

At the same time, it is not a long-term solution for Pinduoduo to occupy upstream and upstream funds. Because the platform has big hidden worries about funds, merchants’ undrawn accounts cannot be effectively protected. Moreover, once the funds are disconnected on the platform, merchant accounts may suffer losses, which will also have a greater impact on the reputation of the platform. Looking at the cash flow of Pinduoduo, this also reveals a problem: Pinduoduo’s own e-commerce business cannot yet produce blood, and there is no other business that can contribute revenue to support growth. Once Pinduoduo can only rely on continuous financing, this will also bring certain risks to its operations.

Although from the perspective of this new financial report of Pinduoduo, many core data have indeed attracted the attention of many investors. But if you look at it from a longer-term perspective, as WeChat user dividends diminish, user growth slows, which may affect the slowdown in the growth of Pinduoduo’s revenue. Once the growth of Pinduoduo is hindered, its market value breakthrough will still face considerable resistance if it wants to continue to set new highs.

The source of the article: Songguo Finance, please indicate the copyright for reprinting.