The supply strategy will be adjusted and optimized according to market performance.

Editor’s note: This article is from the micro-channel public number “Shell Research Institute” (ID: beikeyanjiuyuan), Author: Policy Research.

In 2018, the entry of restricted competitive houses into the market has a significant effect in stabilizing house prices. However, 2020 is destined to be an extraordinary year for Beijing’s price-limiting houses. The volume of auction-restricted housing plots has dropped significantly. There are rumors in the market that the auction-restricted housing is about to withdraw from the stage of history. Buyers who just need houses have the last chance to buy a house. Coming, is this really the case?

01

The price of limited-competition rooms is the price of mid-to-high-end projects, and gradually moves closer to high-end projects

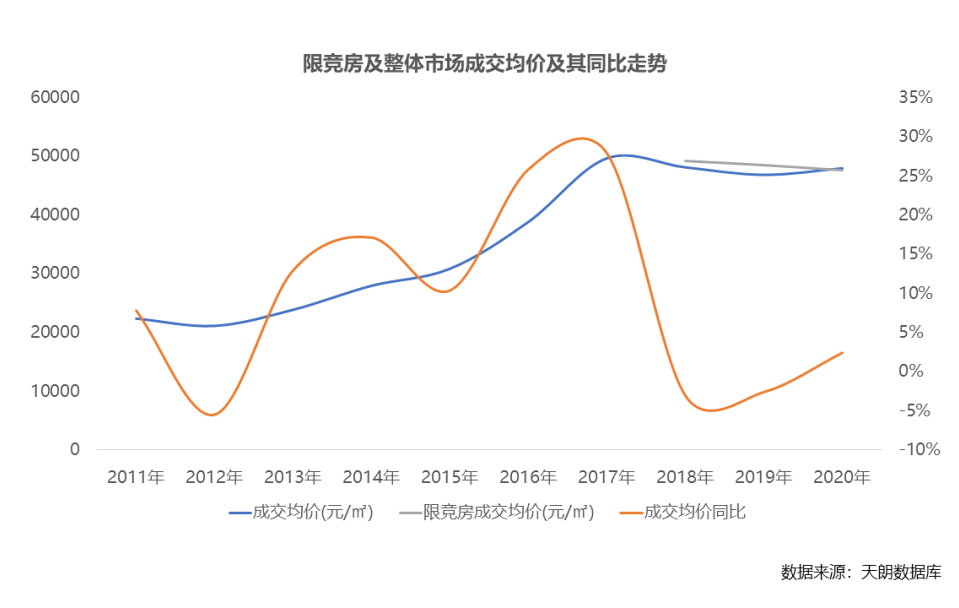

Since 2016, in order to limit the increase in land prices and housing prices, Beijing has introduced new rules in the process of land “bid, auction, and listing”, restricting the area of residential buildings and average sales prices to be constructed in the future for the land to be sold , That is, “the proportion of residential buildings with a residential building area of less than 90 square meters must account for more than 70% of the housing area”, thereby stabilizing the supply of rigid demand and stabilizing housing prices. Since the entry of restricted-competitive housing in 2018, it has significantly restrained the increase in overall housing prices. In 2018, the average transaction price of commercial residential buildings in Beijing dropped by 3% year-on-year, the first decline since 2011.

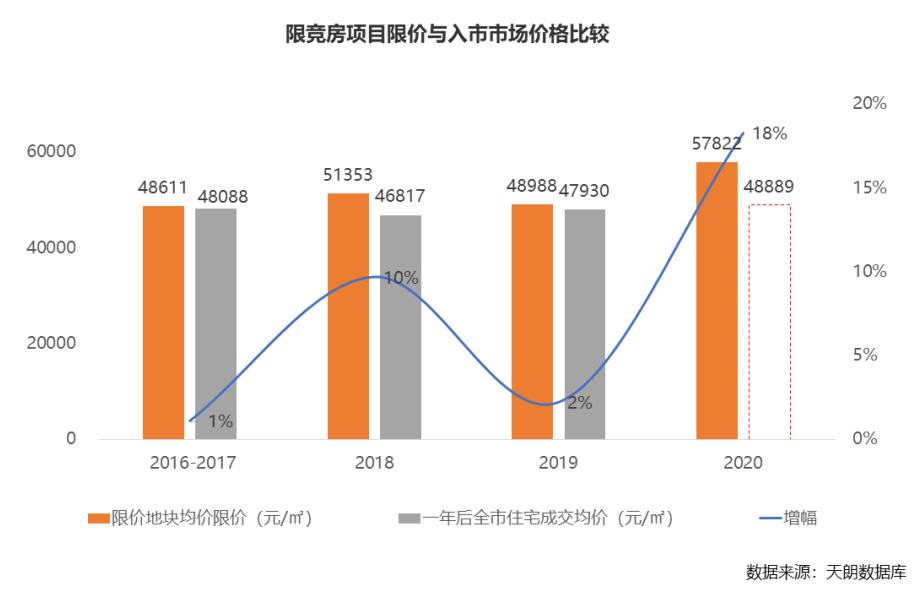

However, from the perspective of the price of restricted-competition housing, its adjustment strategy for the overall housing price is mainly to limit the prices of mid-to-high-end projects in hotspots, so as to restrain the excessively rapid price increase in hotspots, and then pull Low overall housing price growth. Competitive housing projects are in fact mid-to-high-end projects, rather than pure rigid demand projects. As can be seen from the table below, since 2016, the average price of restricted land parcels has been higher than the average transaction price of the overall residential market one year later (calculated based on the development cycle of one year). At the same time, according to the forecast of the average growth rate of the average transaction price of commercial residential housing in Beijing in the past two years, the average transaction price in 2021 will be around 49,000 yuan. Then the price limit of the auction-restricted housing project in 2020 will be 18% higher than the overall market. The project is gradually moving closer to high-end projects.

02

In 2020, the proportion of price-limited homestead transactions will be greatly reduced, and sufficient volume may be the main reason

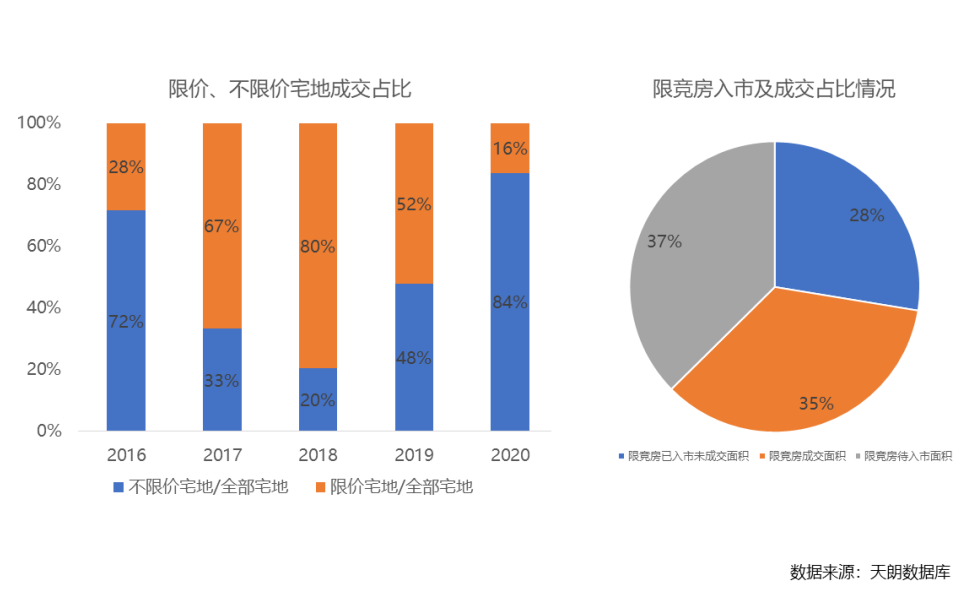

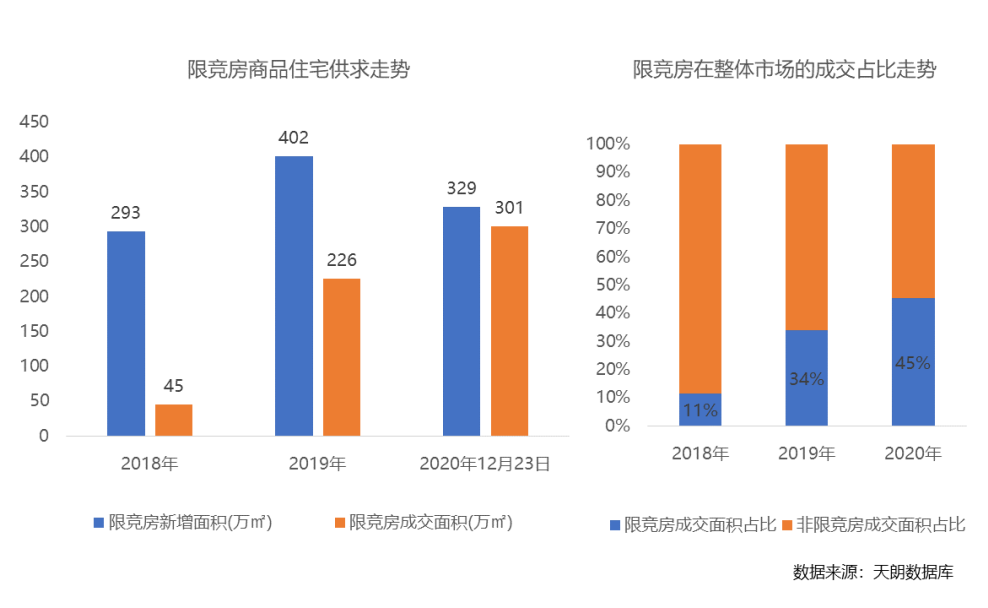

In 2020, the planned construction area of price-limit residential land transactions is 950,000 square meters, accounting for 16% of the total transaction area, and the proportion of price-limit residential land transactions has dropped significantly. According to statistics from the Shell Research Institute, as of December 23 this year, a total of 16.34 million square meters of land for restricted competition have been sold, and 5.72 million square meters of land for restricted competition have been sold. 65% of the restricted housing products are still waiting to be sold. According to the current rate of sale, it will take at least 5-10 years for the sale of restricted-competition housing products. Sufficient stock may be the main reason for the decrease in the transaction volume of price-limited homes.

03

The location of price-limited land moves closer to the city, and the floor price rises accordingly

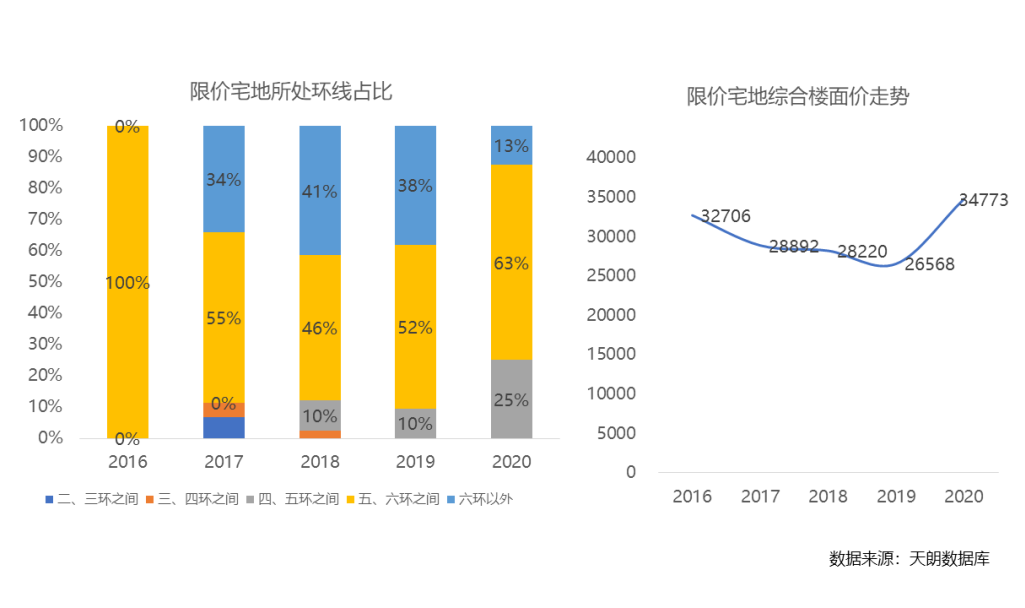

In 2020, the proportion of restricted-price homesteads within the Fifth Ring Road will increase to 25%, and the proportion of restricted-price homesteads outside the sixth ring will gradually shrink to 13%. According to statistics from the Shell Research Institute, since the launch of restricted-competitive housing in 2018, the total sales rate is 56%, which is lower than the 72% sales rate of the overall new housing market in the past three years. It is relatively difficult to sell restricted-competitive housing products. In addition, among the areas with a cumulative supply of more than 500,000 square meters since 2018, Chaoyang District and Fengtai District have higher sales rates of 87% and 67%, respectively; while Fangshan District and Shunyi District have sales rates of 47% and 39% are below average. It can be seen that the location value is still a key factor in the sale of restricted housing.

04

Assume the role of a house price stabilizer, and the transaction volume of restricted-competition housing accounts for nearly 50%

As of December 23, 2020, the transaction area of restricted-competition housing in Beijing’s commercial residential market this year was 3.01 million square meters, an increase of 33% year-on-year, showing an upward trend year by year. As far as the overall market is concerned, the proportion of the transaction volume of restricted-competition housing is also gradually increasing, accounting for 45% of the transaction, gradually approaching 50%. In combination with the previous article, the stock of restricted-competition housing products is large, and it plays an important role as a price stabilizer. ,It will not exit the market in the short term. It is expected that in the short term, the price growth rate of Beijing’s new house market will remain stable, and the possibility of a substantial increase in house prices is unlikely.

05

In line with market demand, the supply strategy of limited-competition housing is gradually optimized

As the supply structure of limited-competition housing projects tilts towards high-end projects, its supply strategy has also begun to adjust. In December of this year, two price-limiting land plots in Changping District and Chaoyang District of Beijing were transferred. The transfer announcement stated that “the proportion of residential buildings with a floor area of less than 90 square meters must reach 70% or more.” The expression of “building area” is changed to “building area inside the apartment”. Compared with the “building area inside the apartment”, the “building area” has an additional share area, while the share area of ordinary commercial residential buildings is generally 20%-30 %, it can be seen that this adjustment means that for projects subject to “70/90” restrictions in the future, 70% of the residential product floor area ceiling will be increased to 110-120 square meters. The policy adjustment of “set type” of restricted-competition housing to “in-set” meets market demand. As mentioned above, the price of limited-competition houses actually corresponds to more customers who have just changed than first-home customers. Especially for high-end projects, the original 90/70 policy limits the floor area of most products to less than 90 square meters. , Mainly for one, two-bedroom and small three-bedroom products, it is difficult to meet the needs of improving customers. The change from “set type” to “set inside” actually increases the floor area of the apartment type to 110-120 square meters, providing room for expanding and improving the supply of products. This is a strategic adjustment for the restricted-competition housing system in the development process to meet market demand. Instruct future limited-competition housing projects to enhance market competitiveness, thereby promoting the efficiency of market elimination. It is expected that in the future, limited-competition housing as a price stabilizer will still coexist with the new housing market, but the supply strategy will be adjusted and optimized accordingly with market performance.