The head is always strong and the pattern is difficult to change.

Editor’s note: This article is from the micro-channel public number “Marketing new engine” (ID: gh_7a9f2789980c), Author: Guo Rui Ling.

It all seems to be bad news.

According to data from CTR Media Intelligence, the overall advertising market fell 19.7% during the first half of 2020. For the first time this year, the proportion of advertisers who reduced their budgets was higher than that of advertisers who increased their budgets. The external environment is very uncertain.

The competition in the digital marketing industry has also reached a fierce stage, and the advertising market shares of Internet companies other than giants are constantly being eroded. The latest report of Shengsan predicts that BAT and Bytedance will account for more than 80% of digital media advertising revenue in 2020, and the digital marketing industry has entered an era of “oligopoly”.

From historical experience, during the economic contraction period, the more direct and quantifiable advertising forms, the more they can grow against the trend. Before and after the 2008-2009 US financial crisis, online advertising revenue represented by search/e-commerce and other performance advertising still increased on the basis of 2008, to 26 billion US dollars. However, the TV advertising market, which is dominated by brand display, has fallen from US$52 billion in 2008 to US$41 billion in 2009.

Is the fact really so pessimistic? We have counted 11 major Internet sites including Alibaba, JD, Pinduoduo, iQiyi, Bilibili (hereinafter referred to as station B), ByteDance, Kuaishou, Vipshop, Mogujie, Momo, Sogou, etc. The company’s advertising revenue in Q1, Q2, and Q3 in 2020 has sorted out four major trends.

The Matthew effect of e-commerce advertising is obvious

The value of e-commerce advertising in shortening the conversion link has been lifted to unprecedented heights with the tuyere of live broadcast and delivery. In the first half of 2020, performance advertising represented by e-commerce platforms will continue to grow from the previous month-Alibaba, The advertising revenues of JD.com, Pinduoduo and Meituan will increase by 3%, 17%, 39%, and 9.2% respectively in Q1 of 2020; Q2 will increase by 33.45%, 27%, 71%, and 19% respectively; and Q3 will increase by 20% respectively. %, 24.89%, 47.89%, 28.37%.

Among them, Pinduoduo has a large gap with JD.com in terms of revenue, profit level and GMV, but its market value exceeds JD.com, which may also reflect the value of platform advertising.

And Alibaba’s Q1 2020 wideReported revenue growth was 3%, significantly lower than the 31% in Q1 of 2019.

But the head is still the head. E-commerce advertising has a clear Matthew effect, and the industry dividends are concentrated in the three major e-commerce giants of Alibaba, JD and Pinduoduo. The second echelon of the e-commerce industry, for example, Vipshop and Mogujie’s advertising revenue did not rise after the economic recovery. From the data point of view, in the first three quarters of 2020, Vipshop’s advertising revenue increased by -10.3%, -12.14%, and -10.38% respectively; Mogujie increased by -74.4%, -71%, and -71.5%.

Social advertising also shows obvious Matthew effect

Tencent’s advertising revenue rose against the trend. In Q3 of 2020, Tencent’s online advertising achieved revenue of 21.351 billion yuan, a year-on-year increase of 16%. According to the financial reports for the first three quarters, Tencent’s social and other advertising revenues were 14.592 billion yuan, 15.262 billion yuan, and 17.752 billion yuan, with year-on-year growth rates of 47%, 27%, and 21% respectively. This is mainly due to the increase in WeChat Moments inventory and the rise in eCPM, which brings higher income. Advertisers responded well to Tencent’s video format advertisements (such as rewarded video advertisements), which promoted the rapid year-on-year growth of mobile advertising alliance revenue.

At present, the effect of Tencent’s advertising integration has achieved initial results.

However, the growth rates of other social advertising-based platforms such as Momo and Weibo’s advertising revenue have been slightly sluggish. According to the financial report, Momo’s advertising revenue in the first three quarters was 57 million yuan, 38 million yuan, and 50 million yuan, respectively, with year-on-year growth rates of -29%, -50%, and -38%. In the first two quarters, Weibo’s advertising revenues were US$275.4 million and US$340.6 million, respectively, with year-on-year growth rates of -19% and -8%.

Uncertainty about advertising on video platforms

In terms of short video-based platforms, the Kuaishou prospectus shows that Kuaishou’s online marketing business revenue reached 7.2 billion yuan from January to June this year, an increase of 222.5% over the same period last year. According to unconfirmed Reuters news, Bytedance’s advertising revenue in 2020 is expected to reach 180 billion yuan.

In terms of platforms dominated by long videos, iQiyi’s advertising revenues in the first three quarters of 2020 will be 1.537 billion yuan, 1.586 billion yuan, and 1.84 billion yuan, with a year-on-year growth rate of -27%, -28%,- 11%. However, online advertising has maintained revenue growth for two consecutive quarters.Signs of temperature.

The advertising ecology of station B is different from others. In July this year, station B launched the Huahuo business cooperation platform. In 5 months, the number of UP owners in cooperation has increased by 6 times, the number of cooperative brand owners has increased by 5 times, and the reinvestment rate has reached 75%, which is particularly stimulating the commercial cooperation of small and medium UP owners. From the data point of view, in the first three quarters of 2020, the year-on-year growth rate of advertising revenue of station B, which has accelerated the commercialization process, was 90%, 108%, and 126% respectively.

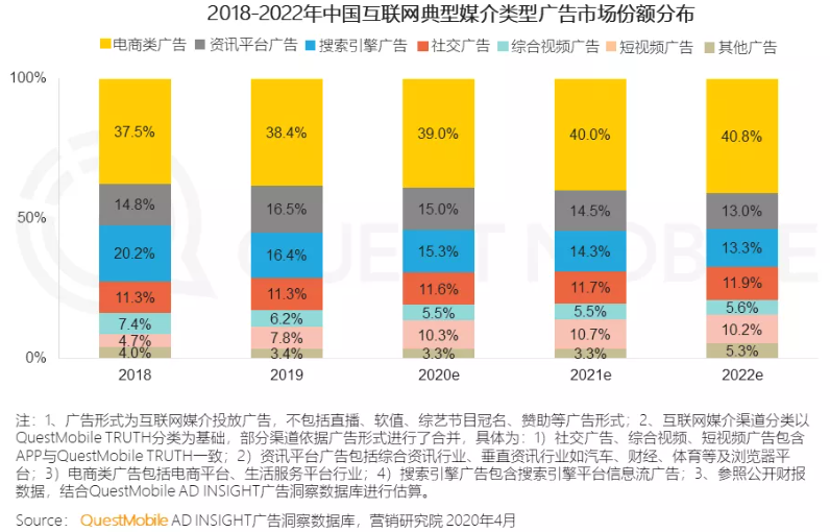

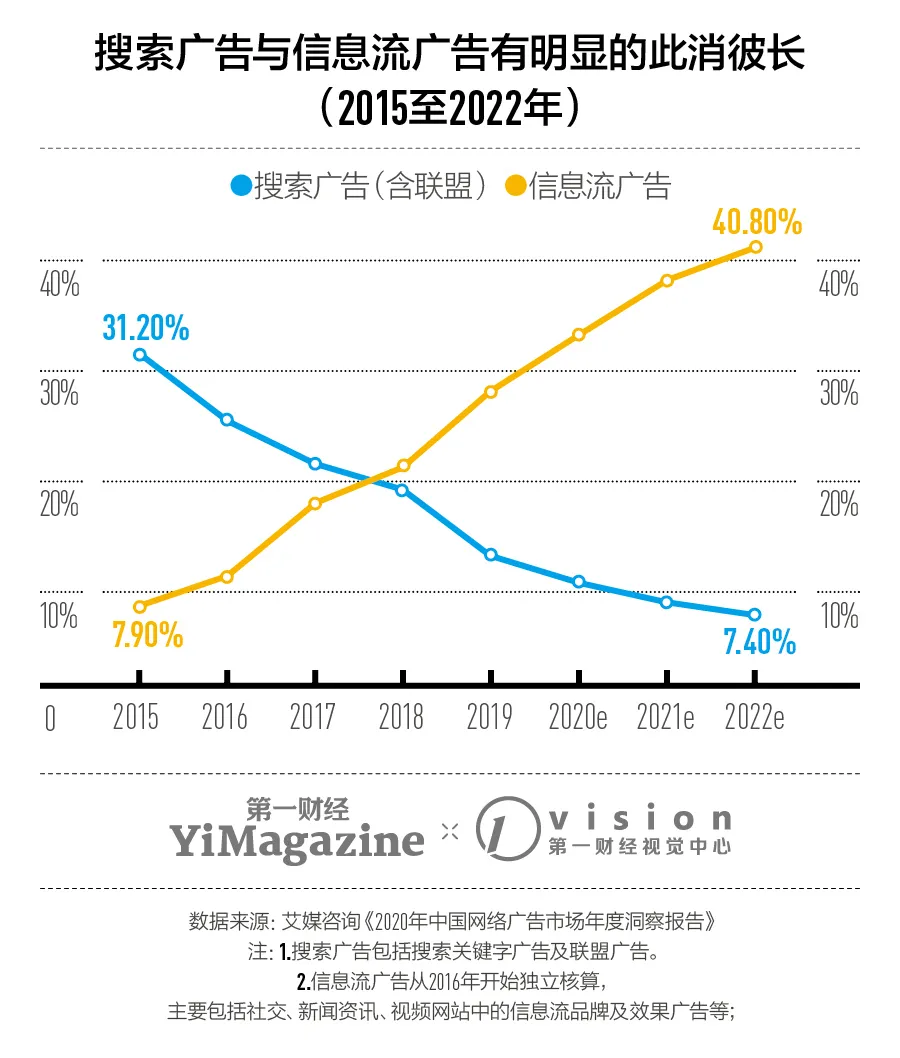

Search ads have changed, and information flow ads have been upgraded

Although the data shows that the proportion of search advertising in the entire Internet marketing service is decreasing, and the proportion of information flow advertising is rising sharply, the scale of China’s search advertising market is expected to reach 110.57 billion yuan in 2020, accounting for 14.1% of the Internet marketing market share .

The iiMedia Consulting report pointed out that in 2020, China Mobile search users are expected to reach 754 million people. The three channels for interviewed netizens to obtain information are search engines, social platforms, and e-commerce platforms, accounting for 69.6%, 49.0%, and 35.3%, respectively. Search has always been one of the main ways for users to obtain information, but the user’s search The behavior is no longer focused on search platforms with a single function.

According to Baidu’s financial report, the year-on-year growth rates of advertising revenue for the first three quarters of 2020 were -19%, -8%, and 14.41% respectively. The search advertising market has been saturated, and the Red Sea stock competition is obvious.

The entry of byte bounce adds variables to this field:

-

In February, the independent app “Headline Search” under Bytedance launched an internal test;

-

In April, the beta version of Toutiaopedia will be launched;

-

In November, Byte announced the launch of full search ads, covering product lines such as Toutiao, Douyin, and Watermelon Video.

-

According to Tech Planet, the current daily search volume of Toutiao is 200 million pv, and Douyin exceeds 450 million, an increase of 50 million over August. The search volume on the platform is the same as that of WeChat.

-

According to a ByteDance expert meeting document, 2019 ByteDance search advertising revenue has reached 2 billion, and it will be around 3 billion in 2020. It is expected to double next year.

In addition to the veteran Baidu and rookie bytes, the Tencent department is also taking action in search. In September, Tencent and Sogou reached a final agreement to privatize the latter for US$3.5 billion. After the transaction is completed, Sogou will become an indirect wholly-owned subsidiary of Tencent. At the end of 2019, WeChat also officially launched Sou Yisou.

Picture source: China Business News

In contrast, if search advertising is stock, then information flow advertising still has an increase.

Since 2012, the growth rate of information flow advertising has been higher than that of other advertising forms. During the period from 2013 to 2019, the transaction scale of China’s information flow advertising market has shown an overall year-on-year growth, with an average annual compound growth rate of 106%. The growth rate has been relatively stable and maintained at a high level in the past two years. In 2019, the transaction size of China’s information flow advertising market was nearly 181.56 billion yuan, a year-on-year increase of 57%.

Conclusion

In addition to the trends reflected by financial data, we also see that the advertising and marketing industry is becoming more pragmatic, pursuing the actual effect of each marketing budget, and also hoping to take into account the long-term operation of the brand. Brand advertising will focus on effects, and performance advertising will focus on long-term effects.

Users reach fragmentation, short-chain conversions, mini-programs shorten the purchase link, live broadcasts reduce the decision-making time… This gives more changes in the situation-after the aggregation of multi-channel traffic, advertising forms and advertising points The design and the timing of emergence have a lot of room for imagination, so it can make greater use of ecological traffic; each media is based on its own resource base and lays out in the advertising ecology. Through the ADX platform, it can break the limitations of its own traffic or resource range. Larger application of traffic.

Traffic dividend recession and market downturn “parallel”, everyone has to face anxiety and pressure, but also find ways to pursue growth. But there is a chance if there is change, 2020 is not easy, and 2021 is more worth raising and letting go.