Channel is king, but content is king.

Editor’s note: This article is from the micro-channel public number “of people and gods Fen” (ID: tongyipaocha), Author: God people were excited.

The world is suffering for a long time

The article should start with a piece of news. On the first day of New Year’s Day, the Huawei App Store suddenly removed all Tencent’s games (or Tencent took the initiative to remove it, the truth is unknown), but one day later, Tencent’s games were restored. , The negotiation behind the two sides is also unknown.

When the incident happened, the crowd in the game industry was very excited and hoped that Tencent would take the lead as an opportunity to change the current unfair share of games on Android phones.

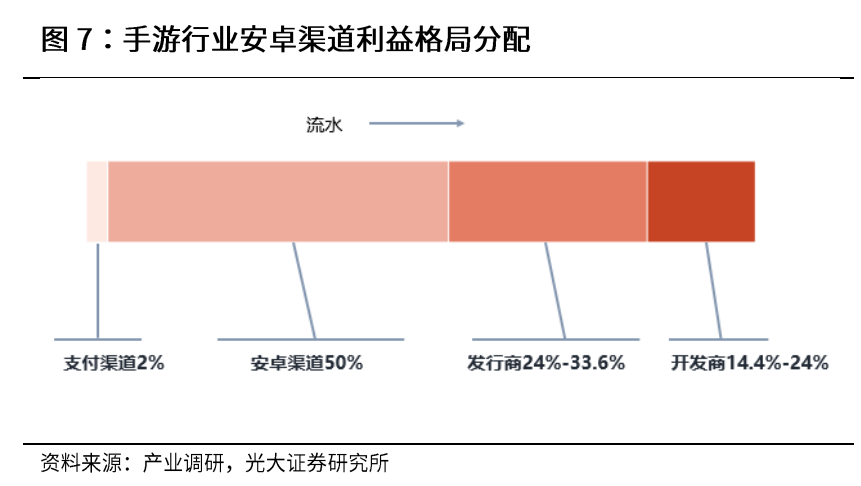

Currently, the Apple store is divided into three (channels) and seven (developers), while the mobile game app stores of major domestic mobile phone manufacturers are divided into five to five. Developers must also “pay channel fees” for channels, plus channels The problem of the payment period of arrears sharing can be described as “the world is suffering for a long time.”

In a nutshell, it’s easy to come to the conclusion that Huawei’s “shop bullying” is not that simple. Tencent Games’ share of the game market is higher than Huawei’s share of the Android phone market. The “shop” is even bigger, how can you be bullied for so many years?

This three-seven-to-seven game sharing ratio has lasted for so long, and everything that exists must be reasonable. In the past, I did not think it was unreasonable, and it must be because it was in the interests of most participants; today I think it is unreasonable, and there must be some changes that make this benefit distribution system difficult to maintain.

Actually, the dispute between Huawei and Tencent is not a competition between two large companies, nor is it just a conflict of interest between the upstream and downstream of the game industry, but the “channel is king” led by Huami OV and the “content” led by Tencent. The competition between the two game business models of “Being King” is the reason why I pay attention to this incident. This case has far-reaching significance for the entire content industry.

How the existing business model is formed

Actually, the pattern of the fifty-five split is not always the case. Android phones did start like the Apple Store. Game developers took 70% of the split, but from 2011 to 2013, it suddenly dropped to the current fifty-five split. .

In the past three years, what happened?

The first change occurred on the mobile phone: In 2011, Xiaomi released an epoch-making product-Xiaomi 1, with pricing1999 yuan, equipped with all the smart phones above 3000 yuan at that time, and equipped with a highly customized MIUI operating system. Since then, Android smartphones have started the business model of “low hardware margins and highly dependent on operating income”.

Huawei’s report is not very detailed. Take Xiaomi as an example. The profit ratio of Internet business has exceeded that of mobile phones and other smart hardware:

With this business model, the market share concentration of Android smartphones continues to increase, forming a four-dominant system of HOVM, leading to the second change.

The second change is the decline of third-party app stores.

Early game distribution is in the hands of third-party application stores, 91 assistants, pea pods, etc., they have fierce competition with mobile phone manufacturers’ application products, but because mobile phone manufacturers control the underlying hardware, there are various Means to “cut Hu” game manufacturers spend their own money to attract downstream customers from third parties.

Because of the weak competition, the third category of applications has maintained the original share ratio so far. In the application treasure, developers can get 60% of the turnover share, but still can’t prevent the loss of share, and the download volume is less than 20%.

The third change occurred within the mobile gaming industry.

Since 2011, with the popularization of smartphones, mobile games have entered an explosive growth period. Game developers’ choice is to change the previous classic games into mobile games and quickly seize the market. In contrast, the game is divided into proportions Not the most important.

In the future, the explosive growth of mobile game users has promoted the proliferation of “skin-changing games”. Small and medium-sized game manufacturers have used multiple skins to go online in the form of application stores to seize multiple resource positions on the list. , Resulting in a short-term increase in user downloads. Categories such as Xianxia and Legend have become the hardest hit areas for skin-changing games at the time-this kind of extremely low-cost games can be profitable even with a 10% share.

The increase in the concentration of mobile phone manufacturers, the strong right to speak, the fierce competition of game manufacturers, and the decline of third-party app stores, these three changes have led to the gradual tilt of the Android game market share to mobile phone manufacturers and redefine it The business model of mobile phones and mobile games:

Mobile phone business model: low hardware margins to obtain mobile phone users, increase advertising and service revenue to subsidize hardware;

Mobile game business model: Inferior low-quality and low-cost skin-changing games seize new mobile game users, responding to low commissions with low development costs.

This business model of “sacrificing the environment for development” is indeed very effective in the early stage of industry development, making mobile phones and mobile games become one of the few industries with global advantages in China.

However, any successful business model is based on a certain underlying user ecology. Once this ecology changes, the original business model will become outdated and even hinder the development of the industry.

Channel is king, or content is king

The dispute between mobile phones and mobile games is essentially a dispute between “channel is king” and “content is king”. Almost all content industries have had this debate in a certain period of time.

These two business models represent two different user ecosystems:

The ecology corresponding to “channel is king” is that users don’t care about content, and they just need to find things faster and more easily.

The typical industry where channels are king is fast-moving consumer goods such as beverages. Consumers don’t care what they drink, but they can drink it when they want to drink it.

Why are the categories such as Xianxia and Legend become the “hardest hit” for skin-changing games? This kind of customers play “feelings” rather than games. They play mobile games to cherish the memories of killing monsters and explosive equipment in the past. They are used to the quality of games more than ten years ago, and they like simple and rude gameplay. They are the group with the most spending power.

Film in the content industry was “the channel is king” ten years ago. No matter what the bad movie, the distributor can get a good box office as long as it can run through multiple rows of movies in the theater, leading to the disaster of bad movies at that time.

“Channel is king” has evolved a business model of “service subsidy hardware” in the mobile phone industry. This business model where the wool comes from pigs and the dog pays is essentially to allow krypton gold mobile game players to subsidize Mobile phone buyers who do not play games.

The underlying user ecology corresponding to “content is king” is that gamers are only willing to pay for good content, and there are enough channels to identify good games.

Movies have taken the first step long ago. For rotten films packaged by traffic stars, as soon as Douban Maoyan’s ratings come out, the attendance rate immediately drops, and the theater manager follows the downgrading of the number of films, causing a big box office jump. The day disappeared. The new films of little-known directors can also be screened in advance, with enough word-of-mouth to win multiple rows of films in theaters. This is the change after the film industry entered the era of “content is king”.

Games are also transitioning to the era of “content is king”, feelings will always be sold out one day, and real gamers will only pay for good content.

nearIn the past two years, excellent works including “Tomorrow’s Ark”, “Original God”, and “Awakening of Nations” have not been listed in the app stores of Android mobile phone manufacturers, but relying on word-of-mouth communication to achieve good sales.

To put it simply, game users have crossed the river, and the game industry chain is still pretending to “touch the stones”. This is a common story in the business world. But the problem is that the low-level hardware environment of mobile games is in the hands of mobile phone manufacturers, and mobile game developers dare not make it hard.

Many people place their hopes on the competent authority to coordinate. I personally feel that this is not the best method.

New business model is typed out

Mobile phone manufacturers seem to have the upper hand in the game, but in fact they are all passive, and the old business model building is also shaky.

First of all, despite the decline of third-party app stores, the rise of game communities such as Tap Tap and Haoyoukuaibang has brought a new model of “zero commission, advertising promotion”, which is the most popular among mobile game manufacturers After “Yuan Shen”, there will be more excellent games to cooperate with this type of platform and become a new competitor of mobile application stores.

Secondly, mobile phone manufacturers are reluctant to lose new boutique games and those national-level games of Tencent NetEase. Moreover, this will result in only secondary games in the mobile phone manufacturers’ app stores, which will exacerbate the loss of heavy game users and form ” Bad money drives out good money”, making fine games even more reluctant to enter.

It is said that after NetEase’s “Fantasy Westward Journey” was first negotiated into three (channels) and seven (developers), half of the domestic Top 10 products have been negotiated, and Tencent’s 6 key products in 2019 have also been negotiated. (This time I don’t know why the talk of “Call of Duty” collapsed), this trend will spread to all head games in the future.

Finally, the competition of mobile phone manufacturers has reached the state of being a leading player. Last year, “Huawei falls, Xiaomi is full”. The high degree of homogeneity of mobile application stores has also caused the problem of channel price wars. Application stores often give game players recharges and discounts. However, such discounts have led to confusion in the game price system, which in turn has brought game manufacturers to the operation. Come troubled.

Rather than doing this kind of ecological destruction competition, manufacturers should lower their share ratio and introduce high-quality games to help the platform gain user stickiness.

But having said that, the Android mobile app store is still different from the Apple store.

The launch of new games requires a lot of traffic exposure. Apple and Google App Stores”Recommendation” is basically very Buddhist, but domestic Android manufacturers are very active in “operations”. Take Tencent as an example. Although products such as “Glory of the King” do not need to be actively recommended by app stores, Tencent also has A large number of homogenized products also require diversion from the store.

The business model is typed out and negotiated, but it will never be coordinated “above”. If any party feels that they can fight again, all agreements can be secretly torn up.

The industry chain is also a “food chain”

The industry chain is not only a process of value creation, but also a “food chain”. Each link has a different role and a different share of profits. In the end, the link with high barriers and high user stickiness often eats meat, and other links drink soup.

Some people say that when Chinese people do business, they can reduce their profits to zero when they have pricing power. When they don’t have pricing power, they must reduce their profits to zero.

But smart players will never eat up the profits of the upstream and downstream, which will destroy the entire ecology; smart players should always pay attention to the changes in the needs of the final consumers, and actively adjust these changes in time. When necessary, we must have the courage to revolutionize the business model completely. Otherwise, the result is likely to be completely subverted by new players.