To accompany running or to make rules?

Editor’s note: This article from the micro-channel public number “small waves subcompartment” (ID: cifnews-NA), Publisher: waves research group, of: Chang, Editor: Zhi-yong.

Recently, a relevant person disclosed that the domestic e-commerce giant JD.com intends to deploy independent website construction service business and improve its territory in the cross-border field. Regarding this news, Hugo cross-border to verify with Jingdong, as of the time of publication, did not receive a response.

Regardless of whether JD.com enters the field of cross-border independent sites, in recent years, domestic e-commerce giants have accelerated their deployment of cross-border e-commerce, especially the independent site market is an indisputable fact, such as Youzan and YY are already in various fields The giants that “success and become famous” have also ended. After all, if JD.com enters into a cross-border independent station, will it subvert the current industry structure?

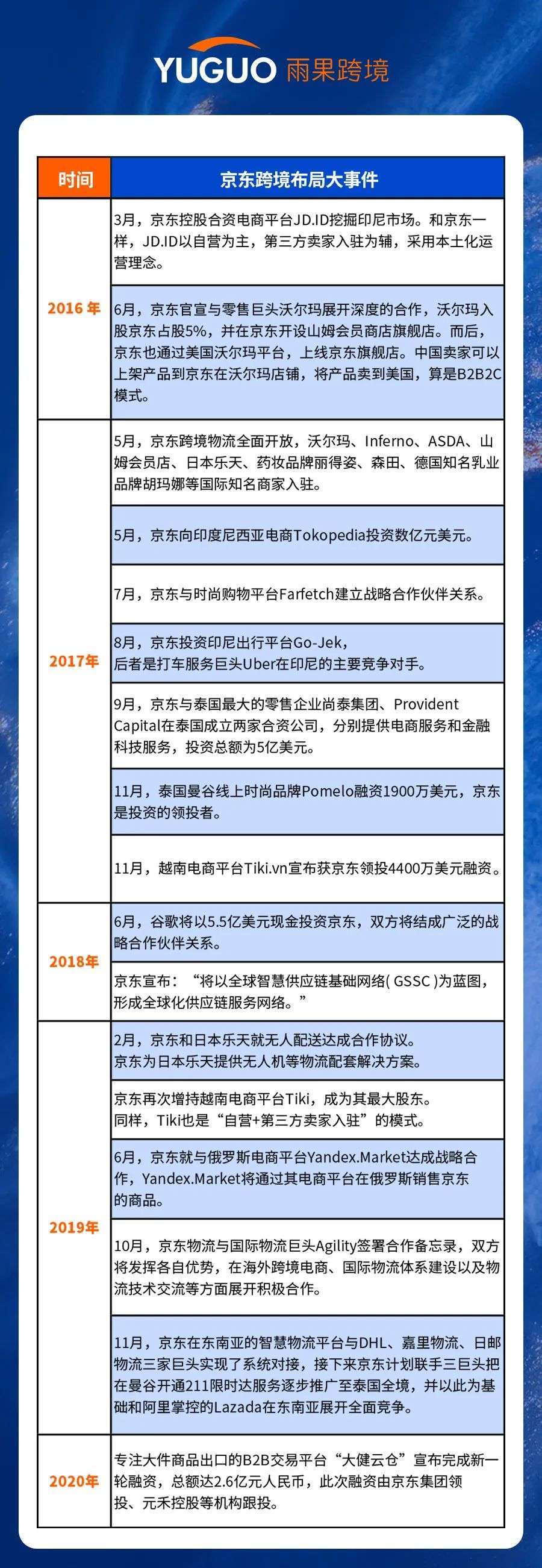

JD’s cross-border e-commerce layout

JD’s business model was originally based on Amazon’s blueprint. Just as Amazon has been actively expanding its territory in various markets around the world, JD.com’s layout in the cross-border field has never stopped.

About JD’s overseas layout in recent years, you can get a glimpse of it from the internal letter issued by Liu Qiangdong last year. “We have been continuously deploying international business: we entered the Indonesian market in 2015 and opened up the Thai market in 2017. At the same time, we are actively developing businesses such as global purchases, global sales, international logistics, and international payments. In the construction of talents, systems, and processes Adapting measures to local conditions and gradually building an international management system…We are confident to bring our accumulation in retail infrastructure, from logistics, to supply chain, technology and other capabilities to the world. We are doing roads and bridges in overseas markets, After the road is repaired and the bridge is built, we will help Chinese brands succeed overseas, benefiting customers, merchants, and partners, and create another JD overseas.”

It can be seen that JD’s overseas layout is not limited to its e-commerce business going overseas, including talents, systems, management models, logistics models, and infrastructure construction. As early as 2015, JD Global Sales opened JD Global’s English and Russian sites. In 2018, it launched a Spanish site. Currently, through JD Global Sales, merchants can sell products to more than 200 countries and regions around the world.

In addition, we have summarized some of JD’s investment and layout in cross-border fields in recent years:

Content source: public data compilation

According to foreign media, in 2015, of the US$500 million investment on Wish platform, US$45 million to US$55 million were invested by JD.com.

On this basis, if JD.com is “another city” in the field of cross-border independent stations, it will definitely be a highlight in its cross-border business landscape.

Cross-border independent station disputes over rivers and lakes

The rise of SaaS website construction technology has created the second spring of cross-border independent websites. In the entire field of SaaS site building, Shopify is undoubtedly a well-deserved leader. As early as the end of 2019, the number of sellers on Shopify exceeded 1 million. In that year, Shopify’s market value has exceeded 110 billion US dollars, accounting for 5.9% of the U.S. e-commerce retail market share, surpassing Wal-Mart and eBay, and second only to Amazon’s 37%.

Looking at the country again, SaaS website construction allows more sellers to enter the original “big seller exclusive” independent station, which can quickly and low-cost website construction and maintenance. At the same time, the prosperity of the seller’s market has also spawned more domestic Saas website building service providers such as Shopyy, SHOPLINE, shopsmith, Ueeshop, XShoppy and so on.

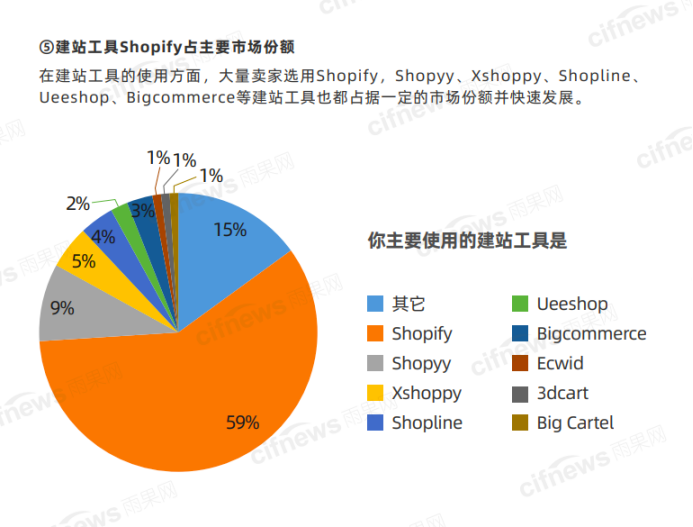

However, according to the statistics on the market share of independent website building tools in the Hugo Cross-border 2020 Q3 quarterly report, 59% of sellers choose Shopify. The proportions of other markets range from 1-9%.

Obviously, this data is basically consistent with the perception and impression of the public in the industry-in the current SaaS site construction market, in addition to Shopify, the others are still in a state of dispute.

Of course, the world is uncertain, and everyone has a chance.

We have also discovered another phenomenon. In recent years, a large number of service providers have poured into the field of independent stations. Everyone has different backgrounds and characteristics. Among these “rookie” there are many industry leaders in various fields. For example, SHOPLINE, which has a high industry exposure in the past year or two, received strategic investment from Huanju Times in August last year. The latter is the parent company of the domestic live entertainment giant YY; and not long ago, it was listed as the first Chinese company with a market value of over 10 billion. SaaS company praised, and at the end of 2020 announced the launch of the international version of the SaaS software product AllValue, which is benchmarked against Shopify.

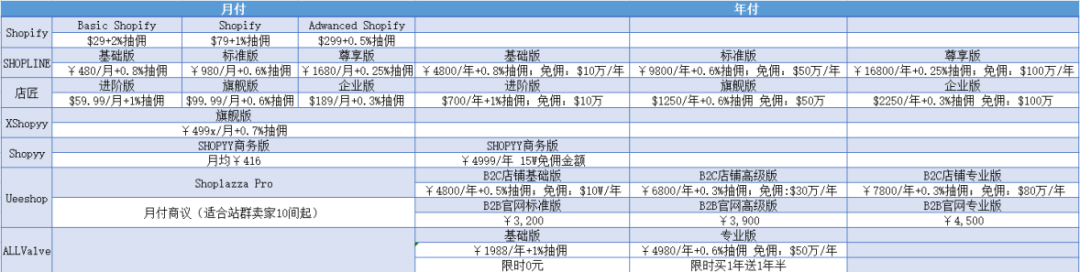

Let’s make a horizontal comparison of the above-mentioned SaaS website building tools in terms of price, functions, and features.

From the perspective of price, the prices of domestic service providers are not much different, and they may have more advantages compared to Shopify. Not only are prices relatively lower, but there are more types of optional price echelons and service items.

As shown below:

Compared with Shopify, the basic domestic website building tools have launched an annual price package option, and they all come with a certain commission-free transaction quota, which is basically between 100,000 US dollars and 1 million US dollars. Among them, shops like SHOPLINE, shopsmith, and XShoppy have also launched a monthly payment version. Ueeshop not only has annual payment packages for B2C customers, but also annual payment packages for B2B customers. There is even a payment model for Shoplazza Pro launched for station group players.

In addition, just like Shopify’s free 14-day experience, basically every company has a free experience period of varying length. The most powerful of these is the rookie AllValue, which was launched not long ago. The basic version starts from 1988 yuan/year +1% and is directly free for a limited time. The professional version also launched a buy one year get one year activity.

From a functional point of view, the introduction of each official website is nothing more than “low cost, fast site construction”, “professional marketing placement”, “rich template”, “ecological integrity” and other expressions, which seem to be similar.

“From the perspective of the technology of SaaS website building, in fact, there are not many barriers in the industry. There is not much difference between everyone, including Shopify. But when you look at it carefully, Shopify’s system may be more advanced and stable, with more templates, Plug-ins are also richer. Other tools have their own advantages because of their different backgrounds.” An industry insider told Hugo Cross-border.

As mentioned above, AllValue, like Youzan, has just entered a cross-border independent station, but Youzan’s long-standing technology research and development capabilities in the domestic SaaS field and experience in serving more than 4 million merchants can make it Grow faster.

Also like the aforementioned SHOPLINE, behind it stands the age of togetherness. According to informed sources, YY was wholly-owned by Baidu last year, with a total transaction value of approximately US$3.6 billion, and a considerable part of this huge sum of money will be focused on the overseas circuit. It is not limited to investment in the field of cross-border independent stations, but also includes short video, live broadcast and other emerging social ecology. Just like TikTok, try to establish a strong influence overseas. If Huanju’s overseas strategy is reached, the terminal’s e-commerce transactionSpeaking of, undoubtedly added a new flow entrance. With this blessing, SHOPLINE’s overseas marketing and traffic will surely increase its advantages in the future.

Another example is XShopyy. With Jiahong’s blessing, it is well versed in independent website traffic play, which has far-reaching significance for sellers’ operation guidance…

It can be seen that all companies rely on “one skill” to gain a foothold in the market, but no matter what their characteristics are, they subconsciously target a common goal-Shopify.

Picture source: Screenshot of Shopyy official website

If JD.com enters the cross-border independent station, will it have a chance to break the industry “deadlock”?

Can JD’s independent station be used?

Can Jingdong’s independent station stand out in the industry? We look at this from two dimensions:

First, what is the biggest pain point of the current cross-border independent website industry and sellers? Can Jingdong’s independent station solve the user’s biggest pain point? So get users’ votes with their feet?

Second, where is the current industry leader, Shopify? Does it have a chance to catch up with Shopify?

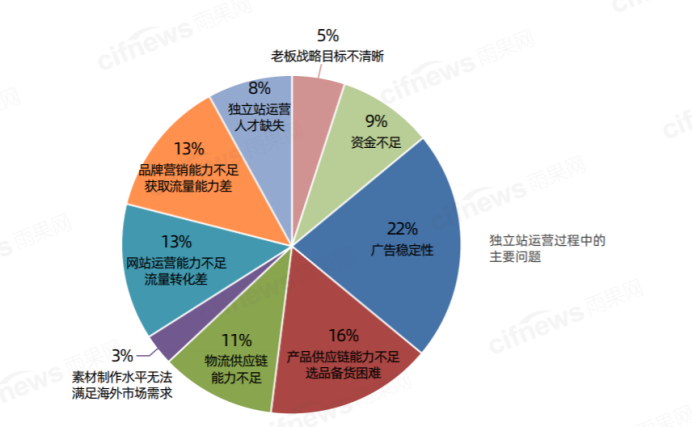

Looking at the first question first, based on Hugo’s cross-border survey data and communication with industry professionals, we have sorted out the three main pain points of current independent sellers: advertising traffic; payment and collection; account security.

Ad traffic. According to Hugo’s cross-border survey, at least half of the pain points of independent sellers in the operation process are related to advertising and drainage. Including poor operation ability, low traffic acquisition, low conversion rate, poor advertising stability, and low quality of creatives.

Pay and receive payments. Through PayPal and other tools, some sellers sell the gray five categories, or have the behavior of incorrect goods, and they are easy to be frozen; credit card payment, because there is a 180-day chargeback period. You may be complained about refusal to pay, or the payment cycle is too long.

The description, basic operation, marketing promotion, etc., may be a little higher relative failure. But if such sellers have product strength, supply chain advantages, understand product building, and brand operation, the probability of success will be higher.

From the perspective of the entire cross-border independent website industry, the future trend must be that more and more domestic merchants will enter the market, especially the massive online brands that rely on Jingdong Taobao. This kind of domestically transformed sellers belong to the incremental market of the cross-border independent station industry in the future. For these incremental customers, JD has a comparative advantage;

However, for existing customers in the current cross-border independent website industry, such as platform sellers of cross-border e-commerce, website group sellers who are good at traffic gameplay, etc., JD’s appeal will not be very great.

“Sellers like site groups, although not favored by the capital market, are very high-quality customers for advertising service providers and site building service providers. Because they have a lot of advertising costs, large quantities, and many sites. This type of sellers The’predecessor’ is more skewed, such as players who do store groups and Douyin accounts in China. Maybe they consider more: Jingdong, as a listed company, has too wide business lines and is in the field of cross-border independent stations. The resources invested may not be as much as that of domestic startups, and whether follow-up services can keep up remains to be considered.” Industry insiders commented.