Is SaaS the “magic panacea”?

Editor’s note: This article is from the micro-channel public number “BT Finance” (ID: btcjv1), Author: BT Finance.

The Chinese New Year has only passed for less than a month, and I have been busy with likes.

On February 17, China Youzan (HK: 08083) issued an announcement stating that the former chairman of the board of directors and executive director Guan Guisen was suspected of being involved in a criminal offence due to his affiliated sole proprietorship company (intention to spend more time to deal with litigation and His personal affairs), from China Youzan resigned the company’s chairman and executive director, and the actual controller Zhu Ning took over as the chairman of the board of directors.

On February 28, China Youzan issued a privatization announcement again and announced that it had applied to the Stock Exchange for the shares of Youzan Technology to be listed on the Main Board of the Stock Exchange by way of introduction.

For investors and the market, this announcement can be described as “not very harmful and extremely confusing.”

What is the relationship between “China Youzan” and “Youzan Technology”? Can you get listed on introduction? Why does the Stock Exchange also have a main board? Should the shareholders of “China Youzan” sell it, and should investors who want to buy “Youzan Technology” buy the bottom?

The answers to the above questions must start with the backdoor listing of Youzan in 2018.

China Youzan and Youzan Technology

Youzan, formerly known as “Pocket Pass”, was founded in Hangzhou Beta Cafe at the end of November 2012. It is a business service company. In 2014, on the occasion of its 2nd anniversary, “Pocket Pass” was officially renamed “Youzan”.

Different from e-commerce platforms such as Taobao and Pinduoduo, Zan focuses on de-platform and user-centric new retail channel development concepts. In 2014, with the full opening of WeChat Pay, the value of private domain traffic with WeChat as the entrance began to be released, and Youzan gained the first opportunity for rapid development.

After years of service ecological construction, Youzan officially started the commercialization process in 2016, and announced that new merchants will start to charge for opening stores. In order to better connect online and offline, Youzan has begun to fully develop its SaaS platform. At this time, Hong Kong-listed company China Innovation Payment Group (CIG) and Youzan entered each other’s sights.

Gao Huitong, a wholly-owned subsidiary of CIG, obtained a payment business license issued by the Central Bank in June 2012. In 2013, it obtained a license extension approved by the Central Bank and was allowed to conduct Internet payment services nationwide. CIG and Youzan have joined forces. Youzan will have its own payment channels to make the entire SaaS platform closed-loop more complete, and CIG will receive Youzan’s commercial traffic, which is also conducive to the development of payment services.

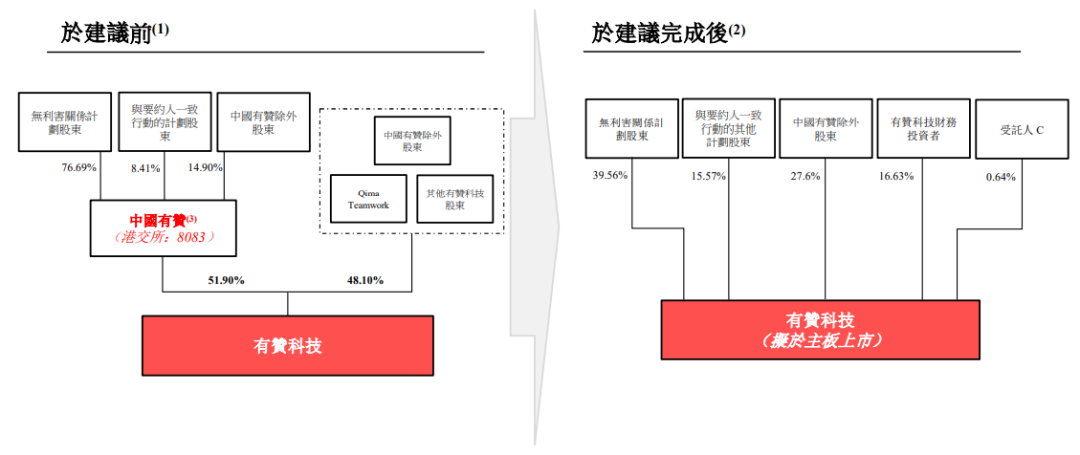

In March 2017, the two parties reached a cooperation agreement in which CIG exchanged 90.44% of the issued shares for 51% of the issued shares of Youzan Group, and Youzan realized a backdoor listing. After the transaction was completed in 2018, China Innovative Payment was renamed “China Youzan” in the secondary market.

So, China

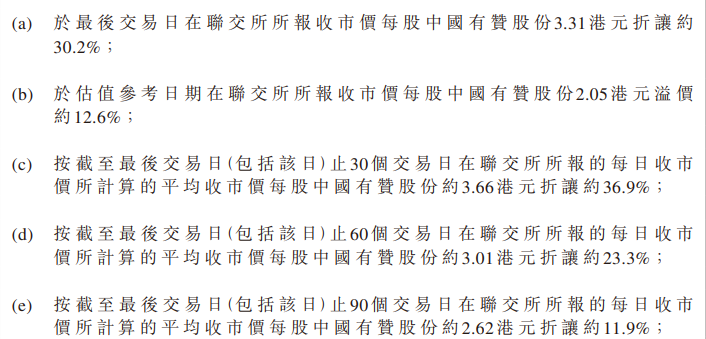

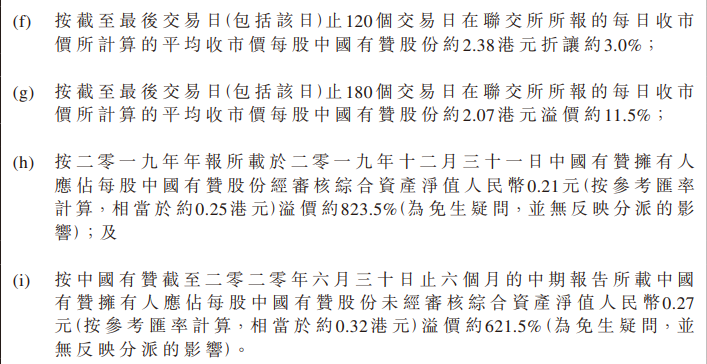

As of the close of the Hong Kong stock market on March 3, 2021, China Youzan’s share price has risen to HK$3.220. If old shareholders don’t run away now and wait to become shareholders of Youzan Technology, it looks like a blood loss. However, international investment banks such as Citigroup and UBS have given a “buy” rating after the announcement of China Youzan’s privatization. Citigroup even raised its target price to HK$5; SPDB International and China Securities Investment Corporation have also maintained “Buy” ratings. “Buy rating”, with target prices of HK$4 and HK$3.6 respectively. Why?

The main reason is that the reference price of China Youzan’s privatization valuation is relatively reasonable, and the theoretical total value of 2.3088 HKD per share is directly proportional to the 51.9% equity of Youzan Technology held by China Youzan. After this round of adjustments, Youzan’s truly “valuable” SaaS business has been included in the valuation, and its normal business operations will not be affected. Coupled with the increased liquidity after the move to the main board, Youzan Technology’s share price has greater room to rise.

To put it simply, the businesses that are divested are all businesses that have little room for imagination, and the ones that are brought back are “popular fried chicken”; it turns out that ten people may want the stock, and then a hundred people may want it. Therefore, if you are not in a hurry to spend money, old shareholders do not need to rush away. The discounted price may be compensated by the call auction on the first day of listing, and there will be more room for growth in the future.

Besides, since there is no new issue of stocks, people (including senior executives, etc.) currently interested in Youzan Technology account for more than half of its shareholders. It is even more impossible for the offeror that is 100% controlled by Zhu Ning to be privatized. China Youzan and the introduction of Youzan Technology harmed their own interests in the process of listing.

Similarly, since the old stockpify has also achieved three consecutive quarters of profit since the 2020 mid-year report.

Youzan’s revenue from SaaS is higher than that of Weimob and Shopify. But if you only “pure” and don’t make money, what’s the use of “pure”? Is it embarrassing to develop other business profits to feed back the construction and development of the SaaS part? Not really.

In addition, the competition among cloud business service providers is fierce, and the market is fragmented. In 2019, the total market share of China’s top five cloud commercial service providers (calculated by revenue) is only about 19.6%, which means that there is no absolute leader in this field. Although Youzan is ranked first, there is no Matthew effect for the time being. Blessings.

At present, Youzan’s operation is quite “conscientious” in taking into account the interests of existing investors, and at the same time satisfying the need to reshape its own image. Next, we need to look at its long-term business development and profitability, to know whether Youzan is a good company worth investing in, or a master of capital operation?