Has this company’s market value of 100 billion yuan been overestimated?

Editor’s note: This article is from the micro-channel public number “sloth Life Fine” (ID: huamian224), Author: sloth editorial department.

Picture source: Bull Group official website

Today I’m going to talk about the Bull Group [603195].

The market and capital have mixed opinions on the Bulls. Some people think that a seller of sockets with a market value of 100 billion is seriously overvalued and greatly deviates from the current level. Another voice thinks that the valuation is reasonable, and even More room for growth.

In the past few days, “The Sloth” has consulted the analysis and research reports of some brokers, and is still at a loss as to whether the bull is worth more than 100 billion. The discussion on the stock bar is even more messy. When the bulls are rising well, the market is extremely optimistic. The recent decline has been a bit severe. Although the market value of 100 billion is still strong, the stock market has already been criticized. As of the close on March 10, the bull’s stock price was 178.29 yuan per share, an increase of 1.04%, and the market value was 107.1 billion yuan.

The value is not worth 100 billion, we do not make an evaluation. Neither optimistic nor bearish. After reading the Bull’s prospectus and financial reports over the years, let’s talk about our views from an industry perspective. (The editor does not trade stocks and does not constitute investment advice).

In the electricity consumption scene, “10 yuan small pieces” leveraging “100 billion big business”

Bull was established in 1995. It mainly focuses on the research and development, production and sales of civil electrical products. Starting from the category of safety sockets, it extends to power connections and electrical products such as decorative switches, LED lighting, digital boutiques, etc., and also incubates circuit breakers. It has made a preliminary layout in the smart home field such as smart switches and smart lighting. The products are widely used in power consumption scenarios such as homes and offices.

The equity structure of Bull Group is mainly concentrated in the hands of the two brothers Ruan Liping and Ruan Xueping. On December 4, 2017, Hillhouse Capital acquired 2.235% of the Bull Group’s equity through a transfer of 800 million yuan through a major shareholder transfer. It is worth 35.8 billion yuan. On February 6, 2020, Bull Group IPO, Hillhouse Capital owns 2.011 shares%.

In order to better understand the fundamentals, we have split and compared the production and sales of 2019 and the unit price of products:

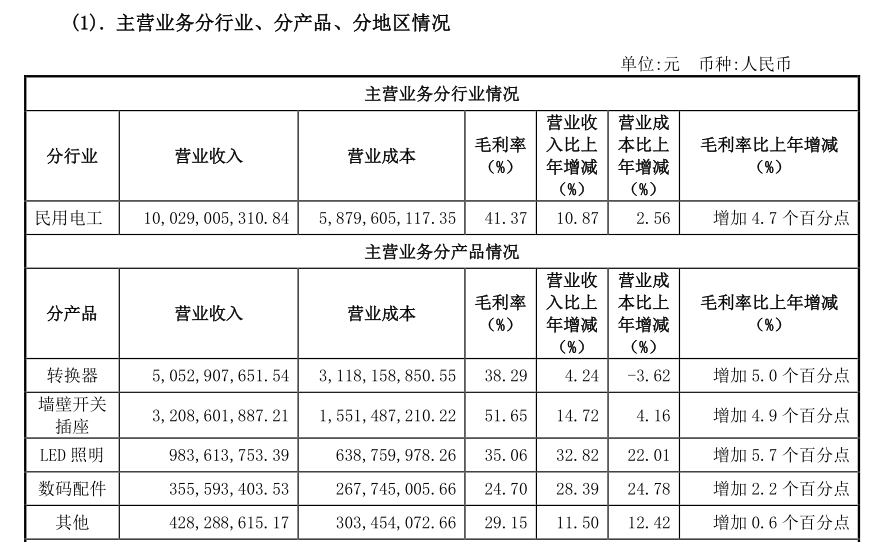

In 2019, Bull’s annual revenue exceeded 10 billion yuan, net profit attributable to shareholders of listed companies was 2.304 billion yuan, and a gross profit margin of 41.37%.

In terms of category, it mainly includes four major product systems (ranked by revenue scale):

1. Converters: 374 million pieces were produced, 345 million pieces were sold, operating income was 5.053 billion yuan, and the unit price was 14.65 yuan/piece;

Two, wall switch sockets: 481 million pieces were produced, 450 million pieces were sold, and operating income was 3.209 billion yuan, and the unit price was 7.14 yuan/piece;

Three, LED lighting: produced 96.98 million pieces, sold 94.31 million pieces, realized operating income of 984 million yuan, and the unit price was 10.43 yuan/piece;

Four. Digital accessories: 31.71 million pieces were produced, 31.21 million pieces were sold, and operating income was 356 million yuan, with a unit price of 11.39 yuan/piece.

Obviously, the Bull has a relatively leading performance scale and can maintain a considerable gross profit margin. It is difficult to find a target company in China. The revenue of 10 billion is piled up by a huge amount. The annual sales volume of nearly 1 billion products, the unit price of each single product is about 10 yuan, and the average single piece net profit exceeds 2 yuan (except for digital products).

Pricing is based on the idea of fast-moving consumer goods, channel density has become an important killer feature

From the perspective of channels, the pricing method for bulls in the secondary market may not be based on home building materials companies, but based on fast-moving consumer goods.

I mentioned the indicators of customer unit price and sales scale. The unit price of home furnishing companies ranges from several thousand yuan to several hundred thousand yuan. The middle range is very large. The average unit price of bulls is only a dozen yuan, so I force the analogy. , It seems unreasonable.

Looking at channels again, for a consumer goods company, the number of channels reflects its existing comprehensive strength, and the breadth and depth of the channels are very important. The total number of stores of the leading listed companies of home furnishing companies is currently about 8,000. According to the channel classification of provinces, cities, prefectures, counties, towns and villages, the penetration rate is still relatively limited, especially in the low-line market, which has not penetrated yet, plus the industry’s own attributes Restrictions, it is difficult for the home furnishing industry to run out of oneConsumer brand.

At this point, Bull’s channel penetration has exceeded 1 million marketing outlets, and a large number of hardware stores, grocery stores, office supply stores, and supermarkets have been covered by Bull’s penetration. This offline marketing network is used throughout the home building materials industry. , It is difficult to find similar samples and difficult to copy.

We went to find the channel analogies of several FMCG industry brands:

Yili shares, the market penetration rate of normal temperature liquid dairy products is 84.3%, and only 1.91 million offline liquid milk terminal outlets (as of December 2019). The market value is about 250 billion yuan, and the price-earnings ratio is 31 times.

Nongfu Spring has a total of 4,454 distributors covering more than 2.43 million terminal retail outlets across the country (as of May 31, 2020). The market value is about 510 billion Hong Kong dollars, and the price-to-earnings ratio is 37 times.

Haitian Flavour Industry has achieved 100% coverage in prefecture-level cities through channels, and 90% of provinces have sales of over 100 million yuan. The number of terminals must be at least in the millions. The market value is about 540 billion yuan, and the price-earnings ratio is 88 times.

The Bull currently has a price-earnings ratio of about 50 times and a market value of about 107 billion yuan. Because the secondary market’s views on fast-moving consumer goods are also very different, it is difficult to say now, whether the bull is currently at a high position or a low position depends on who the target is, for example, the lighting category that the bull is working on. Then, Op Lighting, the leading listed company in the lighting industry, achieved revenue of 8.355 billion yuan in 2019, net profit of 890 million yuan, market value of 24.1 billion yuan, and price-earnings ratio of 35.46 times.

The “offensive and defensive” of Xiaomi and the Bulls

As mentioned earlier, Bull’s products start from converters and continue to extend to the fields of wall switch sockets, LED lighting, and digital accessories products. In its listing prospectus, each sub-sector listed its main competitors. The foreign competitors mentioned by Bulls are Philips, Siemens, Schneider, and Panasonic, and domestic competitors are Xiaomi, Op, Chint, NVC, and Delixi.

There is a lot of discussion about the competition between Xiaomi and Bull on the Internet, especially in April 2015, Xiaomi launched a power strip with a USB interface, which combines the traditional strong electrical interface and the weak electrical interface of the USB into a single plug line On the board, it hit the market with a cost-effective price of 49 yuan. Lei Jun was his platform and claimed that Xiaomi’s power strip can sell 400 million units in China a year.

In public opinion reports at the time, it was even said that the Mi plug strip would “bloodblow” the entire socket industry. The invasion of Xiaomi put some pressure on Bulls, and Bulls chose to quickly follow up the e-commerce channels. In June of the same year, it launched a power strip with a USB interface, and emphasized that it has stronger security properties. It is cheaper than Xiaomi and offers free shipping. In this battle, the Bulls have a firm foothold. Ruan Liping, the founder of the Bull, is very grateful to XiaoRice, cross-industry competition will bring a lot of inspiration.

In terms of sales, Bull’s sales are far more than Xiaomi, and Xiaomi is not the Bull’s rival for the time being. Take converters (plug-in strips) as an example. In 2018, Bulls achieved an operating income of 4.847 billion yuan, while the operating income of Xiaomi’s converter was only 297 million yuan.

The monopoly advantage is emerging, and the opponents facing the product extension are not weak

Bull can obtain such a high market value because of its monopolistic brand recognition and advantages in the field of sockets, as well as its monetization advantage in the future wave of intelligent home appliances.

Why do you say that a monopoly is being formed? The domestic converter market scale is calculated according to 15 billion yuan, and the bull’s performance of more than 5 billion yuan has already accounted for 33% of the market share. In 2018, Tmall’s market share of converter products was 66.39%; in 2018, Tmall’s market share of wall switch socket products was 26.08%. Capital’s eyes are sharp and there is a high probability that this advantage will be appreciated.

It has gradually expanded from the field of sockets to the field of smart homes, focusing on safe electricity use and digging into user scenarios, which indeed tells a lot of stories. But next, whether the Bull can tear a hole in new categories such as lighting and digital accessories, break out and occupy a certain market, may affect how high the market value can be supported in the future, But the challenge is huge. After all, every sub-category has relatively strong competitors at home and abroad, such as Op Lighting, NVC Lighting, Philips and so on.

On the whole, Bull is not a bad company with tens of billions in revenue and 100 billion in market capitalization. The capital market does give high expectations, but in the future, Bulls will also face some pressure. Although channel expansion We can learn from the ideas of FMCG, but it cannot be copied completely. After all, FMCG belongs to the high-frequency category, and the consumption scene is very wide. It can be installed with millions of outlets. From this point, the bull and the pure fast The channel density of consumer goods is not an order of magnitude at all, and cannot be completely equalized.

So, in the future, the density of the bull’s channel will be in a state where bullets fly, and it is difficult to see greater surprises and incremental space for channel coverage. When the growth of the original channels is weak, it is necessary to find a second growth curve. For example, the establishment of a To B business unit to develop channels for real estate, home furnishing, and home improvement companies. This is the channel that many home building materials companies have been working on in recent years.

In January of this year, Bull and Huawei formed a strategic cooperation to lay out the field of fast charging and became the first third-party company with Huawei. Bull is building a smart electrician ecosystem, but it is difficult to become a user-level platform, especially for the layout of smart homes, it is difficult to bypass Xiaomi and companies in the ecological chain, Xiaomi and Bulls, the former rivals, may have the opportunity to form new business connections in the future.

– Summary-

In terms of market value, Bull has become a leading company in the domestic building materials field by market value. In the entire big home circuit, the Bulls have indeed formed a unique advantage, but whether it is as expected by the capital market, whether there is a bubble in its market value, whether it can stabilize above 100 billion for a long time, or it will be adjusted in the shock, it is difficult to play now in conclusion. But the bull is making a seemingly simple business scale and influence.

Just like the home service market we reported in the last issue, this market is very interesting. We sound like a very traditional business, but it is in the field of pest control, nanny cleaning, home care and other extremely focused fields that have been out of the market. Among the companies recognized by the market, the company with the highest market capitalization has exceeded 20 billion U.S. dollars, and many companies have a market capitalization of nearly 10 billion U.S. dollars. Many domestic companies are also exploring. (For details, please click to view the content of the previous issue)

Following this topic, we also raise a question. In the entire residential field, what other scenes are worth focusing on and digging, and have the opportunity to dig out tens or even hundreds of billions of companies? Do kitchen scenes, bathroom scenes, living room and bedroom scenes, and even product-based companies that focus on a certain segment, have enough opportunities? Welcome to communicate with the editor and look forward to it.