Can Jinshan Cloud, who has won a bet on a sub-scenario, win a second time?

Editor’s note: This article is from the micro-channel public number “technology showcase” (ID: kejixinzhi), Author: Wei Yuqi, Editor: Non-Ming.

In 2006, Amazon launched a product called S3. However, Amazon’s halo did not bring much help to S3. Compared with Amazon’s e-commerce business, it was simply small and transparent. It was even interrupted for a full 9 hours without being noticed by customers. This is the first product of AWS (Amazon Cloud Service) that is regarded by Robin Li as “old wine in new bottles” and now contributes nearly US$50 billion in revenue and more than 60% of profits (2020) to Amazon.

In order to make this little transparency rank first in the market, Amazon waited for several years and invested heavily. Bezos has made it clear internally that cloud computing services are like a seed, and we all know that it will become a big tree in the future, which will have a very large impact on the company’s revenue. For this big tree, today’s investment is worth it, even if it is a short-term profit decline or investors’ doubts.

The myth of AWS has revealed the reality of the cloud computing industry for latecomers: the cloud computing industry has a lot to do, and those who are not strong should not cue.

Those who are catching up are like BAT. They have a big business. Although it is harder, the result will not be too bad. Although the strength of the startup company is not as good as that of the big company, it is fortunate that it has no burden and is more flexible. Kingsoft Cloud is somewhere between the two, with Kingsoft Group and Xiaomi Group as shareholders, so that it will not worry about survival like a startup company; in the case of insufficient comprehensive strength, it can only choose to avoid the “line of sight” of the giants. , Choose to focus on sub-scenarios such as game cloud and video cloud.

Looking at it now, although the differentiated route has helped Kingsoft Cloud get a ticket to the cloud computing market, it has also increased the risk of its further development. On the one hand, its annual revenue growth rate has been declining for three consecutive years, and the growth rate of its two pillar businesses has declined in 2020; on the other hand, it will focus on financial cloud, government and enterprise cloud, and hybrid cloud in the future. There is fierce competition.

With the sword going slant forward, Jinshanyun has the possibility of entering the first echelon, but also the risk of becoming the other.

01 2020 with mixed blessings and worries

In the past 2020, the cloud computing industry was one of the few industries that have benefited from the epidemic, which gave Kingsoft Cloud, which has a low market share, an unexpected boost. The financial report released on March 17 is somewhat contradictory to Jinshanyun standing in the spotlight.

On the one hand, Jinshan Cloud had two questionable areas before, namely, excessive reliance on large customers and huge losses. The 2020 earnings report can be regarded as bringing back some face for Jinshan Cloud.

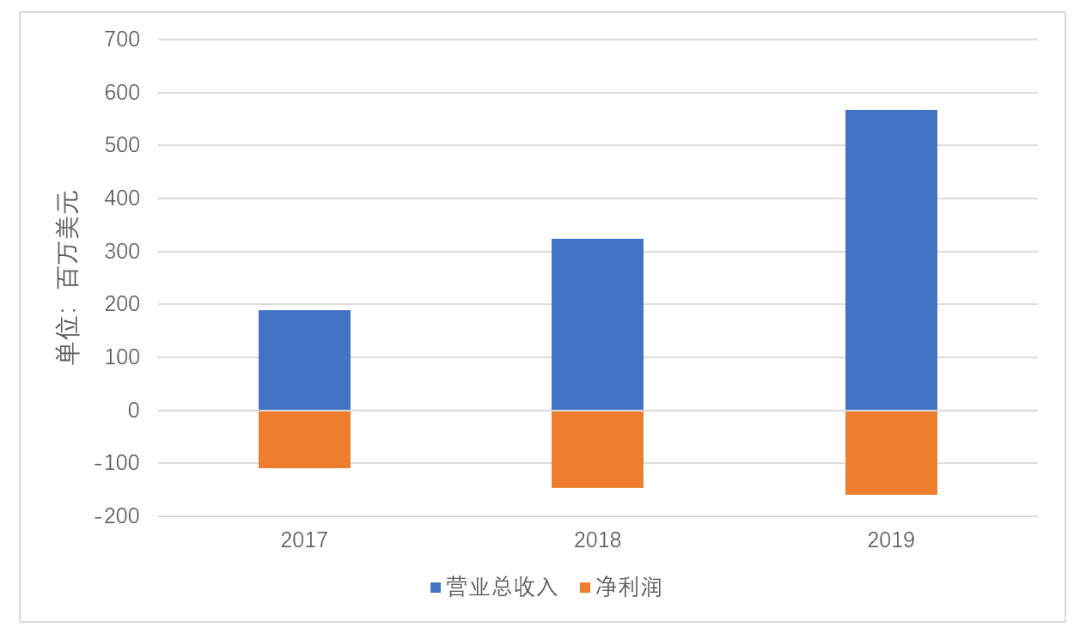

From 2017 to 2019 before listing, its loss increased from 714 million yuan to 1.112 billionThe total loss in three years reached 2.832 billion yuan (RMB, the same below). For this reason, Kingsoft Cloud had to emphasize in the prospectus that having a history of net losses and uncertain future profitability is one of the company’s risks.

In the fourth quarter of 2020, Kingsoft Cloud’s net loss has shrunk by 20.4% year-on-year, and its scale has dropped from 230 million yuan in the same period in 2019 to 105 million yuan. The net loss for the whole year also narrowed sharply, from 1.11112 billion yuan in 2019 to 920 million yuan. The net loss rate has declined for four consecutive years, and was 57.8%, 45.4%, 28.1%, and 14.6% from 2017 to 2020, respectively.

At the same time, Jinshan Cloud’s annual total revenue has achieved an upward triple jump and hit a new high. Its total revenue from 2018 to 2020 was 2.218 billion yuan, 3.956 billion yuan, and 6.577 billion yuan.

On the other hand, the performance of Kingsoft Cloud in other aspects does not match the general trend of the industry. After the release of the financial report, Jinshan Cloud’s stock price fell by more than 10% before the market. The direct cause was that the fourth quarter’s revenue fell short of expectations. This is not because Jinshan Cloud’s revenue is lower than outside expectations, but its growth rate has declined.

The revenue for the fourth quarter of 2020 was 1.922.7 billion yuan, an increase of 63.8% year-on-year, and the growth rate was lower than the previous three quarters. The growth rates of Kingsoft Cloud in the first three quarters of 2020 were 64.5%, 64.1%, and 72.6% respectively.

The revenue guidance given by Kingsoft Cloud for the first quarter of 2021 is 1.83 billion-1.93 billion yuan, almost no growth from the previous quarter. This shows that the high growth of Kingsoft Cloud will soon become a thing of the past after the epidemic has eased. This is also one of the key reasons why the capital market is not optimistic about this financial report.

For the whole year of 2020, the year-on-year growth rate of Kingsoft Cloud’s revenue was 66.2%, which was not only lower than 78.4% in the same period in 2019, but also lower than 79.5% in the same period in 2018. In other words, Kingsoft Cloud has experienced a year-on-year decline in revenue growth for three consecutive years. In 2015, Jinshan CloudThe growth rate is as high as 256.1%.

The decline in revenue growth is actually related to the poor performance of the pillar business.

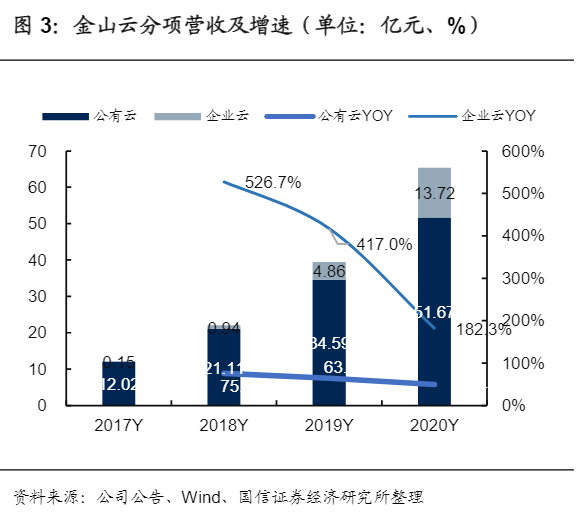

Currently, Kingsoft Cloud’s revenue consists of three parts, among which the other (advertising agency, ancillary services) business scale is relatively small and has little impact on the overall. There will be only 37.7 million yuan in 2020, which is higher than 11.2 million yuan in 2019.

The scale of enterprise cloud business is slightly larger. In 2019, it was 486.3 million yuan, accounting for 12.3% of total revenue. In 2020, it reached 1.363.7 billion yuan, an increase of 182.3% year-on-year. This speed, like revenue, has continued to decline. The growth rates in 2018 and 2019 were 518% and 417%.

The public cloud business is the mainstay of Kingsoft Cloud’s revenue. In 2019, it contributed 3.458.8 billion yuan in revenue to Kingsoft Cloud, accounting for 87.4% of revenue. The scale in 2020 reached 5.166.9 billion yuan, accounting for 78.5%, a year-on-year increase of 49.4%, lower than 61.9% in the same period in 2019.

On the issue of “large customers”, Kingsoft Cloud has two problems.

One is the cliché of relying too much on large customers. The prospectus shows that although the proportion of the top three customers in the revenue of Kingsoft Cloud is decreasing year by year, the share still exceeds 50%. The top three customers of Kingsoft Cloud are Jinshan Group, Xiaomi Group, and Cheetah, which are closely related to it. From 2017 to 2019, the three provided Jinshan Cloud with 56%, 60%, and 57% of revenue respectively.

In contrast, Kingsoft Cloud’s number of senior customers reached 243 in 2019. In other words, the combined contribution of the other 240 customers is not as large as the contribution of “Jinshan + Xiaomi + Cheetah” to Kingsoft Cloud, which is evident in the degree of dependence on major customers. Although Kingsoft Cloud did not disclose the specific information of its major customers in 2020, in view of the absence of major changes in 2020, revenue from these three companies still accounted for a large share.

Secondly, the customer growth rate of Kingsoft Cloud has declined. In the fourth quarter of 2020, the number of customers was 322, and the growth rate dropped from 57% in 2019 to 32.5%.

The pros and cons after 02 Alin

Since its birth, Jinshan Cloud has had to make a choice to decide its development five or even ten years later, that is, when the giants have already occupied domestically and internationallyWith the advantage, it can only choose to cut in from the “small road”.

It is not too late for Kingsoft to get involved in data storage services. As early as 2007, Kingsoft established an Internet storage laboratory, but Kingsoft Cloud was not established until 2012, and the cloud computing service was officially launched in 2013.

At this time, although the domestic cloud computing industry is not as hot as it is today, there are already giants in the market. Among them, Alibaba Cloud is already a leader in the industry, Tencent also fully opened Tencent Cloud in 2013, Baidu’s Baidu Cloud is biased towards C-end users, at this time the number of C-end users exceeded 100 million.

In other words, Jinshan Cloud wants to break the wrist with BAT, and neither Jinshan Group nor Xiaomi can provide more help to it. Take capital as an example. In 2015, Alibaba Group announced a strategic increase of US$1 billion to Alibaba Cloud to accelerate the deployment of data centers around the world. In 2020, Alibaba Cloud announced that it will invest 200 billion yuan (approximately US$28 billion) in the next three years for the development of core technologies such as cloud operating systems, servers, chips, and networks, and the construction of data centers.

Tencent and Baidu are also investing heavily. The former announced that it will invest 500 billion in the next five years, and the latter said that it will expand the server scale to 5 million in ten years. According to market estimates, it is equivalent to investing 300 billion yuan.

The total financing of Kingsoft Cloud before listing was only 1.02 billion U.S. dollars. Even with the 510 million U.S. dollars raised at the time of listing, it still cannot compete with BAT. This trend runs through the birth of Jinshan Cloud to the present.

This is more directly reflected in revenue. Alibaba Cloud’s single-quarter revenue has surpassed that of Jinshan Cloud for the whole year. Its revenue in the fourth quarter of 2019 was 10.721 billion yuan, and its annual revenue reached 36.8 billion yuan. Moreover, Alibaba Cloud’s 2019 quarterly average growth rate is still higher than 67% despite a year-on-year decline. It can be seen that the gap between Kingsoft Cloud and the industry’s first line is very obvious.

Lei Jun also stated in an open letter issued after Kingsoft Cloud’s listing, “The investment in cloud services is huge, and potential opponents are super strong. Kingsoft’s overall strength is insufficient and there are many difficulties.” It is under such circumstances that Kingsoft Cloud has implemented Lei Jun. The “Al in Cloud Service” strategy proposed for it. Kingsoft Cloud abandoned the large and comprehensive model of following the giants and chose to bet on sub-scenarios, such as video and games.

From the results, Kingsoft Cloud’s differentiated strategy succeeded in the first battle and helped Kingsoft Cloud successfully go public. However, Kingsoft Cloud’s differentiated choices also increase the risks it needs to bear.

In terms of specific routes, Kingsoft Cloud chose to focus on specific application scenarios. In the early days, it was video and games. In recent years, it has added finance and government enterprises.

The differentiation logic of Kingsoft Cloud is to choose a single point of breakthrough when there is no advantage in the whole scene, and be the first in the subdivision scene. This is actually similar to the relationship between integrated e-commerce platforms and vertical e-commerce platforms. The difference is that the technical attributes of the cloud computing industry are stronger, and Kingsoft Cloud’s first-mover advantage can help it establish technical barriers in segmented areas.

It cannot be ignored that Kingsoft Cloud is unique in technology and its R&D investment is not weak. It’s just that after BAT gains weight in the cloud computing industry, how long can Kingsoft Cloud’s first mover advantage be maintained?

In fact, there are signs of this trend. According to IDC data, in the “video cloud” market in Kingsoft Cloud’s dominant zone, Tencent Cloud ranks first and Kingsoft Cloud ranks fourth.

In terms of government and enterprise cloud, the giants have also been eyeing this piece of cake. It is difficult for Jinshan Cloud to “get quiet and good years” again in this scene.

Chongqing Municipal Bureau of Big Data Application Development has conducted public procurement on the government cloud platform in September 2019. Compared with the budget of hundreds of millions of government affairs projects in first-tier cities, this project has a budget of only 50 million yuan, but it still attracted fierce competition. Finally, Alibaba Cloud, Tencent Cloud, Huawei Cloud, and Ziguang Cloud were selected. The fierce competition between government and enterprise cloud is evident.

The same is true for financial clouds. As the closest to finance in the Internet industry, Alibaba Cloud has also launched a financial cloud. At the Yunqi Conference in 2020, Alibaba Cloud demonstrated a characteristic cloud platform built in cooperation with twelve financial institutions, covering multiple financial segments such as banking, insurance, securities, and financial leasing.

03 How does Kingsoft Cloud achieve tenfold growth?

Since the first generation of WPS, the Jinshan system has been developed for more than 30 years. With the listing of Jinshan Cloud and Jinshan Office, Jinshan Group has assembled the “troika” of Xishanju, Jinshan Cloud and Jinshan Office. . The troika of “one-milk compatriots” has extremely high similarities in some respects.

With its differentiated choices, Kingsoft Cloud once rushed to the third place in the domestic public cloud market, but the emphasis on “focusing on segmentation scenarios” also limited the development space. In the entire cloud computing industry, this limitation is not obvious under the premise of rapid growth. However, the cloud computing industry cannot maintain high-speed growth forever. Once the industry has an inward volume similar to that of the mobile phone industry, it currently ranks in the first echelon in China. The later Jinshan Cloud has the risk of becoming the other.

Xishanju in the game field has long become the other. For many years, most of the market in the game industry has been occupied by Tencent and NetEase. Since 2015From the first half of the year to the first half of 2020, the market share of these two companies increased from 49% to 74%. After Xishanju tried multiple directions, the martial arts game is still its biggest advantage, and its current pillar is the “Swordsman Love” series in the 1990s. Although the “Swordsman Love” series can still be played, there is not much room for Xishanju’s development in the industry.

Kingsoft Office has taken a favorable position in the online office industry with WPS. However, with office platforms such as Ali, Tencent, Byte, etc., graphite documents are cut from the sub-scenario of documents, and Kingsoft Office is no longer worry-free. Especially in 2020, the revenue and monthly activity growth of Jinshan Office will start to slow down.

It is not difficult to find that the success of the “troika” of the Jinshan system is very similar, that is, to focus on a certain segment of the industry and then iterate quickly.

This logic has a prerequisite for Kingsoft Cloud in the cloud computing industry, that is, its scale must be large enough, because the cloud computing industry has a strong Matthew effect, that is to say, Kingsoft Cloud Cloud must increase its scale to gain more advantages. Lei Jun also mentioned in the open letter after the listing of Kingsoft Cloud: Only by making the scale more than ten times larger can Kingsoft Cloud reach a more comfortable position.

From the perspective of the trend of the cloud computing industry, the direction that may increase Kingsoft Cloud by more than tenfold is hybrid cloud, but Kingsoft Cloud has been slow in its actions and progress in this regard.

Before the emergence of hybrid cloud, cloud services were divided into public cloud and private cloud. The advantage of public cloud is low cost, but it cannot be compared with private cloud in terms of security and compliance; private cloud needs to be customized for customers, and the cost is higher. Hybrid cloud combines the advantages of public cloud and private cloud in theory. Enterprises can put core data in private cloud and non-core data in public cloud, which is more data and cost-friendly.

Similar to the development trajectory of public clouds, hybrid clouds also took root and gradually developed abroad. The first to realize the opportunity was Microsoft, which began to invest in research and development of hybrid cloud in 2015. Hewlett-Packard and Cisco both announced the closure of their public cloud platforms and switched to hybrid cloud, and Amazon launched its hybrid cloud product Outposts in 2018. In a word, in the United States, hybrid cloud has become a battleground for military strategists.

This shareholder wind has also blown to China. According to CCW Research, China’s hybrid cloud market is expected to expand rapidly in the next few years and become an important pole of cloud computing. The market size in 2020 is 25.3 billion yuan, and it is expected to reach 2024.The annual market size will reach 89.29 billion yuan, and the compound annual growth rate in 2020-2024 will reach 35.3%. Hybrid cloud is also mentioned in the “14th Five-Year Plan” and referred to as the industry focus.

On hybrid cloud, the problem with Kingsoft Cloud is that time and barriers to competition have changed.

On the one hand, compared with games, videos and other scenes that emphasize “applications”, hybrid cloud does not have a high barrier for Alibaba Cloud and other more comprehensive heads, and it is difficult for Kingsoft Cloud to use “focus” to establish Sufficient competitiveness.

On the other hand, Alibaba Cloud launched its self-developed native hybrid cloud in 2014. Qingyun Technology, established in 2012, has focused on hybrid cloud since its establishment and insisted on independent research and development of core codes. Manufacturers that directly replace the computing platform with localization are currently listed on the Science and Technology Innovation Board.

According to the official website of Kingsoft Cloud, it is still inseparable from the support of shareholders on the hybrid cloud. Currently, there are three hybrid cloud customers, namely Xiaomi Technology, Giant Network and Kingdee Software.

Generally speaking, the future direction of Kingsoft Cloud is difficult to reproduce the glory of Xiaomi and Kingsoft Office. It is likely to be similar to Xishanju, that is, although it cannot be the industry leader, it can occupy a place by virtue of its differentiated model. Just how long this “seat” can occupy depends on whether the giants are willing to eat this piece of cake, and how much technical advantage Kingsoft Cloud can build.