The vitality of Li Ziqi’s brand lies in the integration of culture and consumption at the bottom.

Editor’s note: This article is from the micro-channel public number “CPT Capital” (ID: MeridianCapital), Author: Ji Wei.

“Many people asked me: Is the Li Ziqi brand viable? If she doesn’t become popular, will the brand be worthless in the future? I can’t say that she must be valuable, but I say that this model is not new: A hundred years ago, there was Coco Chanel, and we also have Li Ning in China. In the same way, Li Ziqi represents the brand path of personal IP→cultural symbols→brand empire.”

Li Ziqi is a microcosm of culturally empowered consumption.

Where is the development of the cultural industry? What role do content and traffic play in the evolution of new consumption? How can cultural industry/consumer companies seize opportunities among them?

Recently, in the MBA cultural and creative industry practice course of Cheung Kong Graduate School of Business, Huaying Capital’s founding managing partner Ji Wei shared his observations on the cultural industry and new consumption, unlocking the development trends and brand opportunities of the cultural + industry.

Ji Wei pointed out that the current cultural industry market has entered a stage of recovery, and culture + has become a new growth point. Data and algorithms have become the “new production factors” and “new assembly lines” of the cultural industry, the circle-level consumption model is taking shape, various interactive forms of the cultural industry are emerging, and the interactive experience is upgraded.

The diversification of consumption scenes, crowd iteration, and other new changes in people and goods have accelerated the trend of integration of culture and consumption.

From the perspective of the empowering role of content and media on consumption, in the era of mobile Internet, online has become the main theme, and the digital economy has promoted the integration of media channels and promoted increasingly diversified marketing methods. The flow has entered the stock stage, and the pressure of platform realization promotes the diversification of channels and stimulates the rise of new online brands.

Media diversification and platform commercialization will jointly promote the arrival of the new domestic product era. Brands rely more on the driving force and innovation of content, and the brand ceiling continues to expand.

“Culture is becoming more and moreThe combination of other industries, like a spring rain nourishing everything, plays a silent role in moisturizing things. Culture and consumption are a relationship of harmony, symbiosis and co-existence”.

From culture to pan-culture, from traditional brands to emerging domestic brands, from digital content to consumption upgrade… Ji Wei believes that the penetration and integration of culture into other industries and fields is becoming more and more obvious. The current investment focus of new consumer brands is still to gain insight into the changes in the needs of the crowd through content and traffic; at the same time, with the help of consumption, supplemented by platform channels for marketing and promotion, the content of consumption is combined with the ecology of investment.

The following is the record of Ji Wei’s speech (after collation):

Good afternoon, fellow students, thank you for the invitation from Cheung Kong Graduate School of Business. Today, I want to focus on the empowerment effect of culture on other industries. Before starting, I would like to ask everyone to take a look at the three figures related to Li Ziqi: 15 billion, 14 million, and 6.7 million.

What do these three numbers represent? These are the milestones of Li Ziqi’s development from 2017 to the present:

Li Ziqi’s original video has accumulated more than 15 billion views on all content platforms;

Li Ziqi has 14 million followers on YouTube and can be said to be the most influential Chinese on YouTube;

Li Ziqi snail noodles became one of the hottest items in the “Double Eleven” last year, selling 6.7 million bags, a year-on-year increase of more than 4 times.

In just three to four years, Li Ziqi has grown from a short video celebrity to a globally influential Oriental IP, and has grown so rapidly, proving the potential of culture and content.

I want to use this as a microcosm to talk about culture and consumption. Nowadays, the cultural industry is more and more closely integrated with other industries. Culture is like a spring rain that nourishes everything, playing a silent role in moisturizing things. Culture and consumption are a relationship of harmony, symbiosis and coexistence.

From this perspective, first, I want to briefly summarize the development status of the cultural industry; second, I want to answer the role of concrete factors such as content and traffic in the development of new consumption, and how to affect the consumption field Development becomes a supplementary motive force; third, through some cases, specifically analyze how cultural and consumer companies seize opportunities in this process, and use culture and content to enhance their understanding of products and brands.

01 | Where is the cultural industry?

From economy to technology, the four driving forces of cultural industry development

The development of the cultural industry up to now is inseparable from the four major driving forces.

First, when the economy develops to a certain level, spiritual needs will be stimulated. Today, China’s per capita GDP has reached more than US$10,000 for two consecutive years; nearly 10% of per capita disposable income is cultural expenditure, which shows that the spiritual needs of the public are very strong.

Second, culture has become an important scene for the implementation of digital technology. For example, the Tang Palace Night Banquet during the Spring Festival out of the circle combined AR and VR related technologies, and another example is the teamlab digital art exhibition that has spread all over the world. Digitalization has played a very important role in promoting cultural development.

Third, Volkswagen touches the Internet. As network coverage becomes wider, culture can naturally reach everyone, and traffic brings the expansion of the entire industry.

Fourth, the epidemic has accelerated digitalization and onlineization. Not only the cultural industry, but the epidemic has promoted a general increase in people’s acceptance of online, such as digital office. Of course, in the short term, the epidemic has also had a certain negative impact on subdivisions such as movie performances.

Looking forward to the future trend of cultural development: data, people, patterns

The four major driving forces have promoted the development of culture, and the integration of culture and digitalization has become closer and closer. From the perspective of data, people and patterns, we observe the following trends:

1. Data becomes oil. Data and algorithms have become an important means of production for the cultural industry and penetrate into the entire process of the cultural industry. The content of culture is becoming more and more abundant, and it is inseparable from the accumulation and application of data.

2, circle-level consumptionThe rise of. With the help of platform private domain traffic and social traffic, it is easier for the Internet to reach the target group. The gathering of circles is getting easier, so the consumption of circles, vertical platforms and niche products are more and more prosperous. This is also an important reason why Gen Z culture can lead consumption, and culture and content can influence consumption.

3. The interactive/experience mode is upgraded. Consumer-oriented interactive experience is becoming more and more critical, especially in the field of culture and consumption, where offline formats require more interaction. Technology accelerates the interaction between content and people, and reshapes our perception mode.

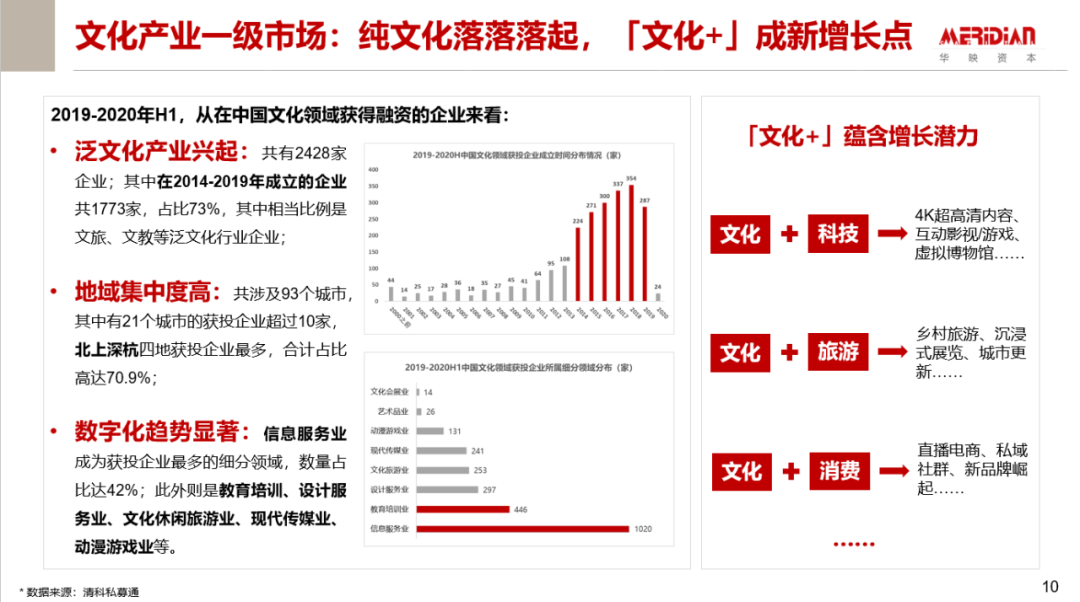

The primary market: pure cultural growth is sluggish, “culture +” has become a new growth point for the industry

The situation of the primary market can be seen by analyzing the companies that have obtained financing in the cultural field in recent years:

First of all, the pan-cultural industry has emerged. Many companies in the industry that have received financing are in cultural extension fields such as culture, education and cultural tourism. Although the cultural industry itself is still subject to many restrictions, but in the combination of culture and technology, tourism, consumption and other fields, the boosting force of culture is increasing.

Second, the geographical concentration is high. Only when the economy develops to a certain level, the spiritual life needs will be very important, so these enterprises are basically concentrated in Beishang, Shenzhen and Hangzhou.

Third, the trend of digitization is significant. The information service industry has taken the lead and has become the segment with the largest number of investment companies, with a high level of concentration at the head.

We often see investors saying that people are becoming more and more important, and that the top companies put people first. Now it’s not the 28th rule, but the 19th rule—the top players are more important, the so-called strong Hengqiang, the trend of digitalization is significant.

Secondary market: cultural media underperformed the market, there is still much room for boost

It must be admitted that from the perspective of rising and falling trends, the cultural media sector in the secondary market has basically underperformed the general trend in recent years.

There are 70 listed companies in the cultural field, accounting for 1.7% of the total number of A-share listed companies and 0.9% of the total market value. Cultural consumption accounts for nearly 10% of per capita disposable consumption—both Does not match. At the point of capitalization, the cultural industry still has a lot of room for growth.

The added value of China’s cultural and related industries exceeds 4 trillion yuan, but GDP accounts for less than 5%. The income of the cultural industry will drop significantly in 2020, and many areas will be greatly affected during the epidemic, especially the offline and experience-related sub-industries.

This is the status quo of the cultural industry. But on the other hand, I have full confidence in this industry. There are many potential opportunities in the industry. This opportunity lies not only in its own development, but also in the empowerment and integration of other industries.

02 | Convergence trend of content and consumption

The rapid development of consumption stems from the reconstruction of the relationship between people and goods

When it comes to the empowerment and integration of other industries, the most typical one is culture + consumption, which is also consistent with Huaying’s investment theme in recent years.

What are the opportunities in the consumer sector? Why is it so concerned? Why are consumer companies developing so well? There are several reasons:

First, scale dividends. China is about to become the world’s largest single consumer market, with total retail sales of consumer goods approaching 40 trillion yuan, and consumption has become the ballast stone for the stable operation of the Chinese economy.

Second, there is still great potential for China’s consumption upgrade. The total retail sales of consumer goods in China and the United States are both about 50 trillion yuan. But the market value of most listed companies in China’s consumer products is much lower than that of the United States, except for alcohol; the PE value given by China’s A-share market is much larger than that of the United States. On the supply side, China has an overall consumption capacity comparable to that of the United States, but there is still a big difference in the growth of consumption levels in sub-categories.

Third, the iteration of the crowd has become the main driving force of new consumption, such as singles, generation Z, pet circles and silver-haired people. New circles are developing, and we must always be aware of such changes.

Fourth, the consumption scene is more diversified. In the field of cultural content, from 2016 to 2020, short videos accounted for 41% of online time per capita. ChinaThe penetration rate of e-commerce is the highest in the world, and the segments that have accounted for an increasing proportion in recent years are community group buying and live broadcast e-commerce.

Fifth, content channels and media are increasingly integrated. Online, we used to grow grass on content platforms and pull weeds on Taobao; now, you can buy where you see it. What you see is what you get. This is a very important trend.

The same goes offline. The new consumption scenes are more interactive and increase the sense of experience. The new format attracts young people and also brings new business models and traffic sources to the business district.

Let’s summarize, why has consumption developed so fast in recent years? Why does content play such a big role in the consumer sector? This is caused by changes in the relationship between people and goods yards.

People: The increase in per capita disposable income, the prosperity of circle culture, and the different needs of different generations can reach every group.

Goods: China now has the most complete supply chain system in the world.

Field: Social media is a channel, and the diversification of media and channels has inspired changes in goods.

The Rise of New Consumer Brands: Potential Brands VS Kinetic Brands

The new changes in the human goods market have given birth to new consumer brands, one is the potential brand, and the other is the kinetic brand. The former cuts in from the needs of subdivided groups, focusing on the matching relationship between people and goods; the latter uses communication methods and uses traffic dividends to boost brand growth.

People have the potential to find goods at a premium. Potential brands such as Li Ziqi, first get to know her as a person and the lifestyle she represents, and through the content, the brand spirit is deeply rooted in the heart, thereby driving the consumption of related products.

The kinetic energy brand uses scale to force consumer perception. Like Yuanqi Forest, there are all over the world with its advertising and promotion, using its advantages in communication and channels to bring about high growth in the business, and then reuse it in other categories.

03 | How content and media empower consumption

How content and media empower consumption should be understood from the development context of the entire consumer industry. Since 2000From the beginning to the present, the digital economy has promoted the integration of media channels and promoted the diversification of marketing methods.

The history of media channel integration: from traditional media to mobile internet

Before 2000, the media was mainly graphics and text, single and monopolized; in the PC Internet era, digital marketing began to grow rapidly, online media gained a certain value, and user portraits began to be clear; in the mobile Internet era, video websites and social media With the rise of platforms, marketing began to shift to the mobile terminal, paying more attention to APP launching and advertising video.

In recent years, the emergence of mobile information, short videos, live broadcasts and other media has promoted the further integration of media and channels. The development of science and technology has made personalized recommendations of thousands of people a reality. Content platforms are e-commerce, and marketing methods are increasingly content and personalized. Planting grass, attracting fans, private domains, etc. have become standard keywords for consumer companies.

Brand rising power: platform monetization pressure + channel diversification

How to increase platform revenue? Here we have a basic formula: number of users x ARPU = platform revenue. Disassemble the variables to see——

From the perspective of user groups, since the increase in smartphones in the mobile Internet era has basically peaked, all platforms are now actively using content to obtain traffic, to obtain traffic outside the site, or to break the circle to obtain traffic.

From the ARPU value, the original monetization model of the content platform is advertising, games, live broadcast, etc. Why join the link of consumption and sales? In my opinion, one is the desire to increase user contribution value and seek new drivers of “income growth”; the second is ideological factors, and the pressure of content supervision is heavy, and it is necessary to hedge and use other methods to increase revenue.

It is much easier to do content ecology than consumption ecology. Building a business ecosystem requires not only infrastructure, but also a variety of service providers, and it needs to connect with advertisers, brand owners, MCNs, supply chains, and so on. Relatively speaking, it may only take 2-3 years for the content ecology to be established, while the consumption ecology takes longer to establish.

Brand Evolution Theory: From Traditional Brands to New Domestic Brands

Media diversification and platform commercialization have expanded the brand ceiling.

The traditional brand era is inseparable from the re-launch of mainstream media, such as radio and television. The media is a very important development boost for consumer brands; in the era of the Tao brand, brands have begun to use mobile Internet traffic dividends to expand marketing channels and continue Introduce the old and bring forth the new. But the problem with the Tao brand is that it relies too muchTaobao should operate through multiple channels and develop through multiple channels, and the current development trend should also prove this point.

The current era of new domestic products is driven by content and product innovation, which is reflected in the diversification and integration of media and channels.

The new generation of consumers is also different. Generation Z is a very confident generation of the country. They grew up in an affluent environment, with a globalized structure and a high aesthetic level. Consumers’ confidence in the national tide is also increasing. We will recommend new brands of domestic products in our life circle and are willing to use them.

04 | Let’s start with Li Ziqi: Huaying Capital’s investment logic

Li Ziqi: From cultural output to a world-renowned oriental gourmet brand

Li Ziqi is an excellent benchmark for the integration of content and consumption. In the field of food content, short videos like Li Ziqi are rare until now.

Where is the advantage? First, it is everyone’s instinct to yearn for poetry, pastoralism, and a better life. Everyone likes this kind of content. Second, eating is a common demand, whether it is a front-line white-collar worker or a small town youth.

“Maintaining the original intention” is an important reason for the strong vitality of Li Ziqi’s IP. She chose a long-term path. Many people ask me: Does Li Ziqi have vitality? What if she doesn’t become popular anymore? Will this brand be worthless in the future?

I can’t say that she must be valuable, but I say that this model is not new: a hundred years ago there was Coco Chanel, and we also have Li Ning in China. Similarly, Li Ziqi represents personal IP→cultural symbols→brand empire. path.

Hefu Lao Noodles: Digital Barriers + Modern Food and Beverage Leveraging Traditional Culture

The most standardized categories in China are rice, noodles, hot pot, and barbecue. Among these four categories, I think investment can only be invested in standardized catering around these categories. Hefu Lo Noodles is very earlyThe central factory in Wanping was established, and the digital capability of the entire supply chain was a moat.

Another opportunity is productization. Hefulao Noodles is a catering company, but like a company, it can quickly digest and retail catering products in the future, follow the route of supermarkets, and accumulate advantages in the supply chain and brand. Productization is a good opportunity for catering companies to open up the second curve.

Zi Hei Pot: Grasp the intergenerational dividends, and flow to strengthen the minds of the crowd

Zihai Pot has seized the demand of singles, and has become the third choice besides instant noodles and takeaways with lower prices, convenient and abundant scenes, and high-end ingredients. We believe that eating for one person is a track with great potential in the future and can define new categories.

Bai Xiao T: Omni-channel content marketing

Baixiaot is a functional menswear brand that only makes basic styles. It is a T-shirt in summer and a down jacket in winter. With the help of the platform bonus, we have seized the opportunity of Douyin’s wave of category launches. The private domain operation is particularly good and its growth is very fast. In February, it just became the No. 1 in JD T-shirt category, and the brand ranked in the top five.

05 | Conclusion

Finally, I want to say that, in the final analysis, consumption is a business of “people”, and it always starts with insights into the crowd.

The original intention of Huaying was to use content and traffic to keenly perceive who, where, and what changes the user is. At the same time, it uses the experience of traffic and delivery efficiency as the entry point for consumption and investment. Empower enterprises.

“Follow the situation, act accordingly, and follow the trend.” These capabilities match the development trend of the industry, and it is precisely that we can seize the opportunity in the big consumer track and make a good investment in the leading companies. And the reason for finally occupying a place.

This is what Huaying is doing now. It is also hoped that in this way, content and consumption can be integrated with the entire investment ecology. That’s all I am talking about today, thank you all.