Nuggets of enterprise service vendors sink the market

Author | Wang Yutong

Edit | Shi Yaqiong

The corporate service track is undergoing an unexplored battle for the sinking market.

Last year, Perfect World released the perfect mailbox, through which the non-company-form collaborative office process can be completed;

After the epidemic, Jinshan Document found that 60% of its users are from traditional manufacturing and e-commerce;

Start-up companies fly missions and Ji Gongjia clearly want to serve the B-end market, which is dominated by construction/manufacturing workers;

Cloud computing vendor Ucloud began to serve the township and county governments;

Huawei’s Chinese government and enterprises have launched a strategy of “sinking cities and cities” for many years;

The field of no-code is constantly lively, BI manufacturer FanRuan released a no-code product Jian Daoyun, Ronglian Qimo has MoPower, and low-code manufacturer Orzhe also released new products without code;

In April 2021, Chanjet, a subsidiary of UFIDA that specializes in small and micro enterprises in the sinking market, plans to go public on the A-share market;

On January 14 and 15, 2021, Alibaba DingTalk and Tencent Cloud Development respectively released new versions of low-code development tools. The creation process is realized through drag and drop, and the scope of use will further sink.

They belong to different tracks, use different technologies, and reach different groups of people, but their commonality is that they are targeting the same piece of land—the sinking market of enterprise service.

The optimistic outlook has attracted capital’s favor. Since 2020, VForms, treelab, Heipayun and other tools have successively obtained financing through code-free process/system construction tools; blue-collar talent service provider Youlan International, blue-collar employment platform immediately report to labor management service provider Gaiya Workshop, flexible Companies that focus on blue-collar employment, such as China Service Cloud, the employment service platform, also received financing in the same year.

After a year of follow-up and observation in this field, we try to answer the following questions for you:

1. What is the sinking market in the field of corporate services?

2. Why has the market been sinking in the past year and has been sought after?

3. At what stage is it now?

4. As the Nuggets sink into the market, what problems will companies encounter?

5. What direction will the sinking market of corporate services take in the future?

01 Nuggets moment

What attracts these companies and capital is a large market that is close to a trillion dollars.

Why do you say that?

First of all, sinking markets should not be called “sinking markets” at all, they should be called “mainstream markets”. Its placeThe trend represented is not “declining consumption” but “upgrading consumption”, that is, groups with lower incomes begin to learn to “spend money”, corresponding to tob is to learn to “purchase.”

Pinduoduo’s sinking market refers to the low-income consumer groups in third- and fourth-tier cities. The national population with a monthly income of less than 5,000 yuan accounts for 70% of the total population, which is a real “mainstream market” (data for 2020). Correspondingly, these 70% of the population whose monthly income is less than 5,000 yuan are generally covered by the sinking market that we define. By analogy, 70% is “enterprise service sinking the market.” This means that enterprise service companies serving the sinking market have the opportunity to serve 70% of the user base, which is more than twice the current 30%.

Take cloud computing as the representative of China’s current mid-to-high-end enterprise service market. In 2020, the scale of China’s IaaS+PaaS+SaaS will be 300 billion yuan, and the cloud computing market will sink 700 billion yuan. Coupled with other types of tracks such as platforms, the size of the entire sinking market is approaching trillions and will gradually expand.

The huge market represents a huge temptation.

Secondly, the popularity of smart phones provides the possibility of digital penetration.

Before and after 2015, the popularization of 4G and the blowout of mobile Internet: China’s Internet users have reached 688 million, and the Internet penetration rate has reached 50.3%, which is 3.9% higher than the global average; rural Internet users have reached 195 million, and urban Internet users have a total of 493 million . At this time, the network and e-commerce have penetrated into the sinking market, but Pinduoduo, an e-commerce platform dedicated to serving the sinking market, has just been established. In the sinking market of enterprise services, it can be said that everyone knows how to use a mobile phone.

Finally, but looking at the corporate service track, the threshold for sinking the market is lower, which is a major benefit for new players.

Take no-code technology as an example, its technical threshold is not high, which makes the cost of trial and error for manufacturers extremely low; moreover, since the service targets are mostly small and micro enterprises, traditional enterprises, and long-tail enterprises, its characteristics are Selling standard products does not need to formulate solutions to the individual needs of enterprises like manufacturers serving mid-to-high-end markets, and the marginal cost is low. This is a low-cost production and asset-light model in technology entrepreneurship.

In this way, the sinking market is very good, and it will naturally attract a lot of players to enter.

02 What are the opportunities for dismantling the sinking market of 70% of the Chinese population?

On a macro level, the sinking market of corporate services refers to companies with relatively low IT literacy.

First of all, its users are mainly blue-collar groups. Blue-collar workers are not just laborers who do heavy physical tasks. With the adjustment of the economic structure, the blue-collar population is also changing-including low-skilled office workers.

Secondly, in addition to the overall enterprise composed of blue-collar groups, individual project teams and loose organizations are also covered in the category of sinking markets.

Again, the long-tail industry and the long-tail companies in the industry may have digital needs, but due to their low attention and no specific digital tools, their IT literacy is not high.

These three groups can be independent of each other, or they can overlap. For example, a construction company outsources a construction team for a certain project. First of all, this group is a blue collar. Secondly, they are not a complete company, but a project team, and their company may belong to a long-tail company, not all corporate services. Manufacturers are competing for the top enterprise.

The enterprise service demand of this kind of users is that the enterprise service sinks the market.

Who are the companies that want to make money in the sinking market? I want to explain here that in fact, there have always been companies that serve the sinking market. For example, the outsourcing construction team mentioned above can also be regarded as providing services to the company. However, this kind of purely manual “enterprise service” without IT content is not in the scope of this article. This time I will focus more on the “enterprise service” in the digital wave.

Classification from application scenarios

If the application scenario is used as the classification standard, the classification of the sinking market is not much different from the mid-to-high-end market, which is the main market classification of enterprise service vendors before, mainly in general scenarios and segmented scenarios in different fields.

1. General scenarios, such as process, management, collaborative office, etc.

In this type of scenario, the biggest difference between the mid-to-high-end market and the sinking market is that the usage habits of the users are different, that is, the working habits of white-collar people and blue-collar people lead to differences in processes, management, and collaboration. White-collar workers are more accustomed to using OA systems (computer terminals), and office software such as Dingding and Feishu, while blue-collar people have their specific needs in general scenarios, that is, the functions should not be too complicated and simple to use.

On this basis, around the different users of the sinking market, several groups are divided:

The first group is manual laborers, their usage habits have the following problems:

1. I don’t want to use new apps such as corporate WeChat and DingTalk. New apps have certain learning and training costs, and there are certain thresholds for users with low education levels. In these areas, task management is not It must be high frequency, and the usage rate of downloading APP will not be very high, which will result in low task transmission efficiency;

Second, it is best not to use the system on the computer side, because traditional industries are often not like Internet companies with a computer, and the workplace is not necessarily equipped with a wireless network;

Three. On a one-two basis, work tasks are often uploaded and issued through WeChat, butThe transmission format and file size of WeChat are limited, and omissions are prone to occur in many information streams.

In summary, if you want to enter the manual labor market, such as building construction, takeaway express delivery, maintenance and cleaning, etc., in addition to companies capable of self-developed systems, the best way is to establish process management through WeChat applets Collaboration tools.

The second group is low-tech office workers, the typical representatives are small e-commerce, intermediaries, etc. They have better IT literacy than manual workers, but their business model determines the simplicity of the tool. In this scenario, form tools that are networked and capable of collaboration are often the best choice.

The other faction is loosely organized. The internal use of DingTalk and corporate WeChat needs to be built on the basis of a “company”, but for loose organizations, this is not conducive to their management and collaboration. The epidemic has catalyzed the trend of flexible employment, and more and more freelancers have appeared, and they are more to complete a project, not long-term management and coordination; organizations represented by university associations are also facing the same problem. At this time, web-side tools can become a good carrier.

(to loosely organized tool)

Perfect Email is a typical collaborative tool for loose organizations. It does not need to download multiple apps such as IM, video conference, or install the system on the computer. You only need to open a mailbox page on the web to work together. , The training cost is low, and the threshold for use is low.

The user community of Kingsoft Documents combines the above three factions. 60% of its users are from traditional manufacturing and e-commerce users. These users manage and undertake production tasks through the form function in the Kingsoft Docs applet. Its habit is to use QQ and WeChat for communication, and it is also difficult to apply for DingTalk and corporate WeChat certification. Between personal communication tools such as QQ and WeChat and corporate IM such as corporate WeChat and Dingding, there is an opportunity for collaboration tools such as Kingsoft Docs.

Wang Dawei said that the table form is a very good management vehicle for many sinking users. For example, a Taobao store with four or five people only has customer service, shipping and warehousing management, and sales parts, and often one person has multiple roles. At this time, there is no need to introduce complex systems such as ERP and CRM. Forms can be used. Resolved; but all of the sameForm, Excel does not have the ability to collaborate in real time, so form tools will have new opportunities.

2. Focus on different subdivision scenes

In addition to general scenarios, different fields and industries have their own scenarios, and they also have different requirements for digital service providers.

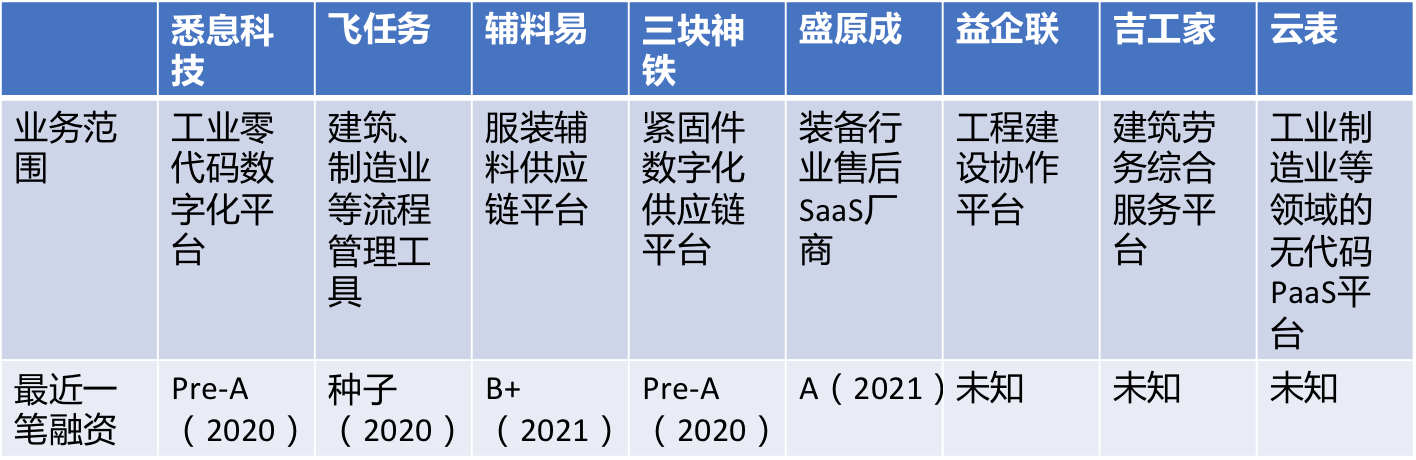

Manufacturing, construction and other scenarios

Manufacturing and construction are typical scenarios where blue-collar workers gather. At present, there are about 100,000 construction and engineering construction companies in the market, of which 8% are leading companies; and the number of manufacturing industries is even greater. According to the National Bureau of Statistics in 2018, there are 3 million factories in China with annual revenues of more than 20 million , The annual income is less than 20 million yuan, including small workshops.

(Part of the list of related vendors that have recently obtained financing)

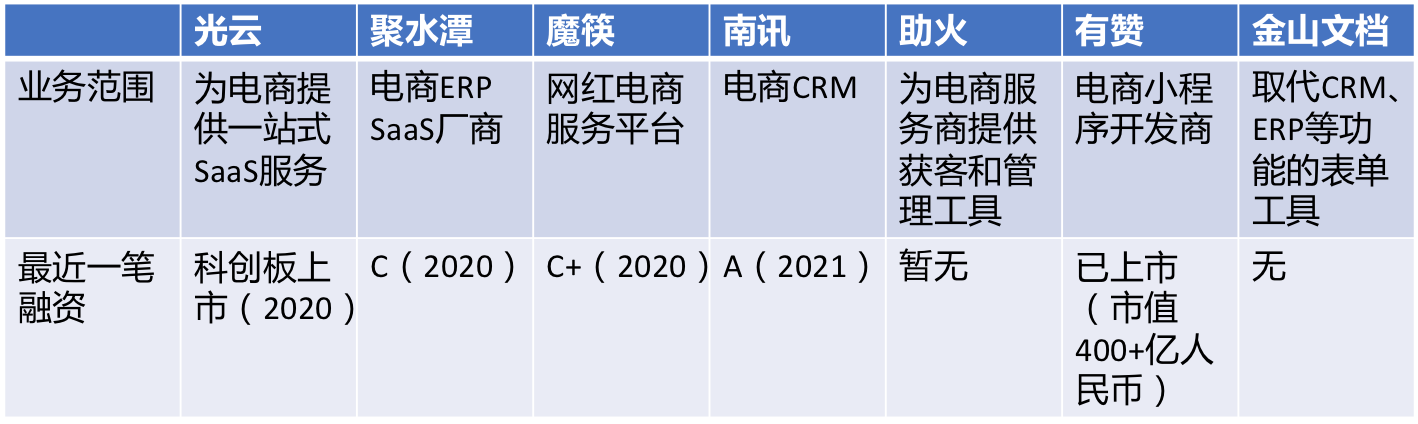

E-commerce scenario

China’s e-commerce is developing rapidly. By 2019, the scale of e-commerce has exceeded 30 trillion. According to statistics, in 2018, the number of active sellers on the four major e-commerce platforms of Ali, JD, Pinduoduo, and Weidian exceeded 10 million.

E-commerce merchants are often small in scale, with 1-10 people mainly, and their staff do not need to have complex work abilities.

(Part of the list of related vendors that have recently obtained financing)

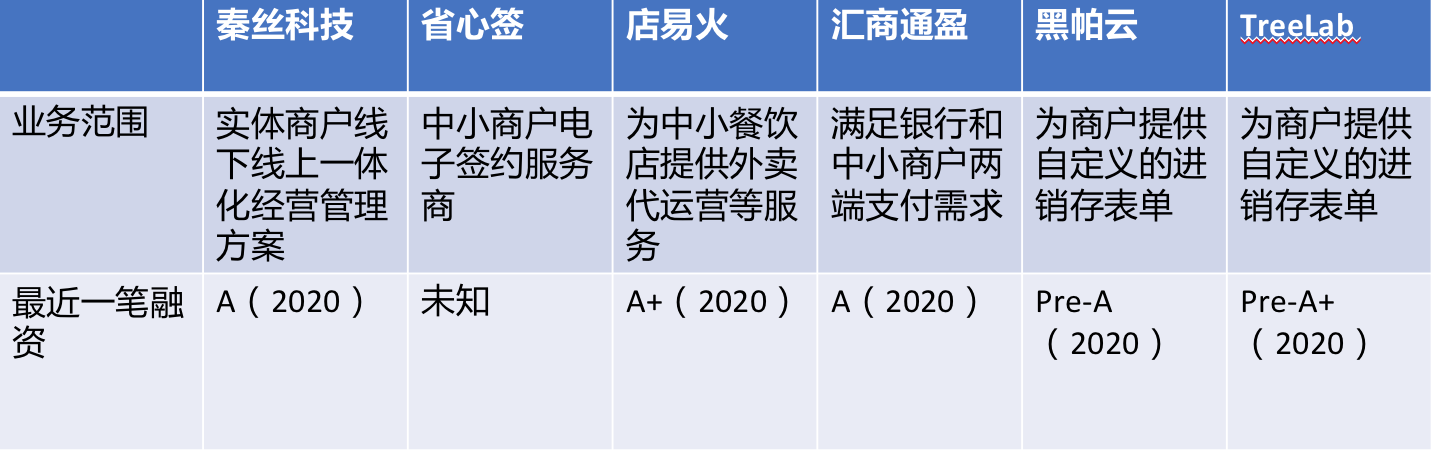

Physical merchant scenario

China’s small and medium-sized merchants are the foundation of economic development. There are more than 80 million individual domestic businesses with 230 million employees, accounting for 30% of China’s labor force, and most of them are couples and wives shops.

(Part of the list of related vendors that have recently obtained financing)

Blue collar employment scenario

According to public data from the National Bureau of Statistics and other public data, there are more than 400 million blue-collar people in China, of which about 120 million are blue-collar in the service industry, about 290 million are migrant workers, about 100 million are in the manufacturing industry, and nearly 8,000 are in the construction industry. Million. These blue-collar workers change jobs frequently, changing jobs every 6 months on average, and many projects cannot meet all salary and welfare guarantees. Therefore, tools and platforms around blue-collar management, recruitment, salary and welfare services are very important. This is also a scene where new players have been entering the game since the Internet era.

(Part of the list of related vendors that have recently obtained financing)

3. No code tool that does not distinguish between scenes

Since the sinking market is an emerging market and many of them belong to long-tail demand, many scenarios cannot be covered. And because the IT literacy of the sinking market is low and the threshold for digitalization is high, a “no/zero code platform/tool” that can realize the self-built process may be able to solve the problem of scenario coverage.

In 2020, 13 zero-code vendors were reported.

(Partial list of manufacturers)

Compared with the concept of zero code/no code, low code/light code is more familiar. The low-code concept was also introduced from the United States, which refers to the rapid generation of applications through a small amount of light-weight programming, and is more used to serve long-tail industries and long-tail applications where digital tools have not yet appeared. Previously, this track has ran out of the unicorn OutSystems with a valuation of more than 1 billion US dollars in the United States. Giants such as AWS, GOogle, Microsoft, Oracle, etc. have also laid out low code.

Since 2019, the domestic low-code trend has gradually become clear. Apart from the influx of startups, on January 14 and 15, 2021, Alibaba Dingding and Tencent Cloud Development respectively released new Versions of low-code development tools can also implement the creation process through drag and drop, which is more biased towards the category of zero code.

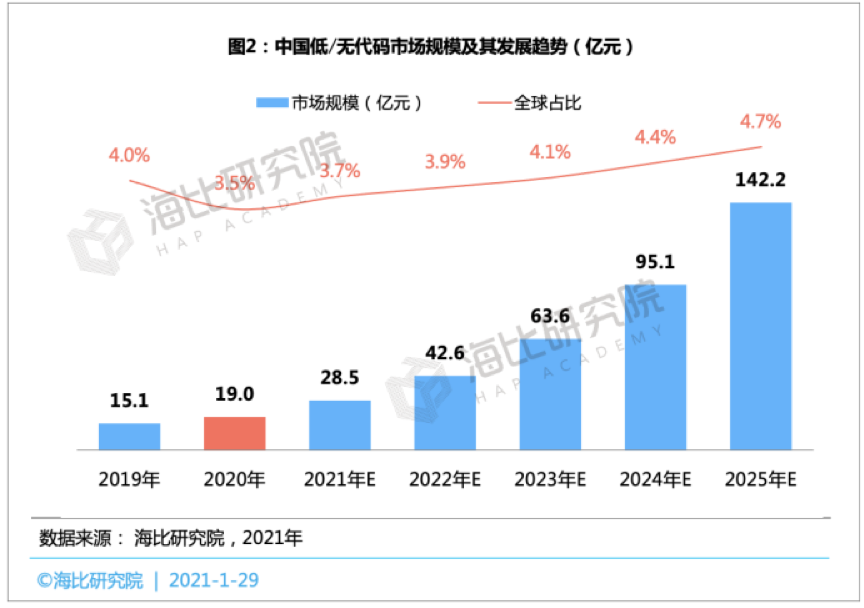

China’s no-code/low-code market is developing rapidly

Classification from play style

According to the play style of the incoming vendors, it can be divided into two categories

One category is dedicated to sinking markets. These companies are divided into two batches. One is SaaS, which are mostly established or marketed around 2020, and the other is platform. With the rise of Internet platforms, most of them are blue-collar recruitment platforms.

Take flying missions as an example in the SaaS category. The main goal of the no-code tool established in 2019 is to help the sinking market achieve mission management. Task management is just needed, but in traditional industries such as manufacturing and construction in third- and fourth-tier cities, because they are too far away from digitalization, most of them still use manual and verbal task management. Flying missions can be adapted to their usage habits. Process management tools can be created by dragging and dropping on small programs. Users can complete related mission claims and execution feedback without using other apps or web systems.

Of course, there are also SaaS tools that saw the development of the sinking market a few years ago, such as the labor management system Gaia Workshop. However, its play style is different from ordinary sinking tools. Although the users are mainly blue-collar labor, the payers are mostly large enterprises, and their paying awareness is higher.

The platform business model is simple, such as “Youlan International” established in 2014. As a blue-collar service platform, on the one hand, it improves the quality of talents through vocational education and training, and improves the quality of blue-collar talent supply; on the other hand, it improves through Internet technology Service efficiency improves the efficiency of matching blue-collar talents.

The other is to develop more user groups in order to find the second curve. Enterprise services in the mid-to-high-end market have been the main market for manufacturers to break through since SaaS sprouted in China in 2014. In recent years, old manufacturers continue toWith development, new manufacturers continue to appear. This market is becoming saturated, and some manufacturers serving the mid-to-high-end market have begun to sink the market and make efforts to make customer groups more diverse.

MOKA, a manufacturer of ATS (recruitment management platform), originally served more companies in new economic industries such as the Internet, but found that there are too many competitors in this field, and is currently considering more traditional industries Transformation.

A lot of toG’s business is even sinking. Wei Bo, the deputy dean of Ucloud Research Institute, found that in recent years, he and many other big cloud computing companies have met in the township and county government bidding. With the support of policies, the township and county governments have also continued digital transformation, which attracts more Enterprise service vendors serve them.

There is also a type of sinking play, which does not distinguish between markets, but is just to serve customers. A typical case is Huawei’s Chinese government and enterprise. Since 2017, it proposed the “prefecture-city sinking” strategy, starting from the provincial capital city and gradually going down, not only has it cultivated internal city managers who are “going to the countryside”. Also gathered external partners such as channel vendors. The sinking strategy has achieved remarkable results. In 2020, the revenue of the regional market has accounted for more than 40% of the total revenue. And their purpose is not to serve customers in the sinking market, but many traditional companies in third- and fourth-tier cities with low IT literacy. In order to serve them well, they can only make their play “more grounded.”

In summary, entering 2021, there will be more and more start-up manufacturers specializing in the sinking market, and there will be more and more “old guns” manufacturers who are originally considering sinking in the mid-to-high-end market. There will also be more and more new models and technologies for market development, and the trend of enterprise service manufacturers entering the sinking market will become more and more obvious.

03 Although the prospect is good, it is not easy to do it

But after entering the game, players will find that the road to sinking is not easy, and they will even face obstacles from both technical and business models.

The obstacle first comes from its advantages-low barriers to entry. The technical threshold is low, in other words “no technical barriers”, it is more prone to homogenized competition. Taking no-code tools as an example, it can be seen that there is not much difference in the use pages and functions of dimension tables, treelab, and Hepa Cloud currently on the market. A tob investor clearly told that tools without technical thresholds such as no code and low code have no investment value.

However, a non-code manufacturer put forward his own view on the fact that there is no technical threshold: “Even if this capital does not invest, other capital will invest in us.”

Other related entrepreneurs believe that when technology is difficult to play tricks, they can use the “stupid bird to fly first” method to enter the game early to seize the window period.

Another disadvantage, these groups do not have the awareness of paying, and the second is that they do not have the ability to pay.

In the sinking market, it is difficult to pay. Take form tools as an example. This type of tool is often free to use for a period of time before charging, but the trial-paid conversion rate is mostly between 20% and 50%.

The lack of the ability to pay is because this group has low income, and it is often difficult for the person in charge of purchasing for them to have the ability to pay. The customer unit price of products in the sinking market is basically below 2w, and many are even at the level of 1,000 yuan.

The premise of paying awareness and paying ability is to find these clues first, that is, “acquiring customers.” The sinking market is huge, but the industry and geographical location are scattered, and it is difficult to find and contact through the Internet. More customers can only be obtained through local push. However, the road to ground push is difficult, which makes these manufacturers unable to achieve large-scale replication.

Also, even if the tool is used, in the process of using it, some customers will still find it difficult to trust the tool. A manufacturer of textile digitization found when serving some family workshops in the south that they refused to upload their warehouse data anyway, thinking it was a “commercial secret.” This will bring difficulties to subsequent services.

But these business model problems are not unsolvable.

One way is to use the high-end market approach to sink the market. Gaia Factory, which entered the labor management market in the early years, adopted the method of cooperating with large labor-intensive companies to solve the payment problem. Although the user group is still blue-collar, they do not deal directly with blue-collars, but cooperate with large groups that employ a large number of blue-collars.

The second idea for solving the problem is to develop on a small scale first, polish the product and deepen the understanding of the industry, and occupy a market position. Wei Mingzhi, the financial consultant of the mission, told that the existence of these problems is still related to the inadequate infrastructure, but the infrastructure can only be spread by major manufacturers, and now the start-up manufacturers have to occupy the seat first.

The third idea for solving the problem is to sink directly to the bottom without worrying about it. You can start from the mid-market first. For example, Ucloud cannot touch the township government at once. You can start with the second and third-tier urban government.

There are two customer-acquisition tips: Those who sink the market to purchase software and tools often do not have too strong digital capabilities, and they cannot distinguish the differences between different software. Therefore, when acquiring customers, one can use the C-end customer acquisition method, place advertisements where they can see, and try them out. Even if the conversion rate is only 30%, but the base number is large, they can naturally have considerable revenue; second, you can When pushing on the ground, your mouth is sweeter. The local pushing staff of a certain manufacturer told me that when acquiring customers on the ground, many mom-and-pop stores do not use function evaluation tools, but to see whose local pushers are sweet.

But the more important question is: What will big manufacturers do if they want to enter the sinking market in the future?

Although it has not yet appeared, but must notThe obstacle of not worrying is. Entrepreneurs have a different view-it is not a bad thing if you enter the game now. As mentioned by Wei Mingzhi above, the entry of a large factory can help the sinking market complete infrastructure construction and market education; the sinking market of the enterprise service track is originally scattered, and the large factory may not take away all the space.

Of course, looking at it now, there will always be more or less uncertainty about the future. Whether it is the financing rounds of startups or the maturity of their products, the industry is at a relatively early stage, and the prospects are not completely clear. The trillion-dollar market is growing, and those who want to share the pie are naturally endless. Perhaps under the constant running-in of the industry and manufacturers, products, and capital, the market development route and business model will gradually become clear.

Whether the sinking of the Nuggets can rescue the bottlenecked Chinese corporate service industry, we will wait and see.

——————————————-

“Enterprise Service Review” (36dianping.com) has now included nearly 10,000 products. You can choose software and services suitable for your company based on the evaluation of real users, independent and objective product ratings and rankings. Scan the code immediately and pay attention to find solutions that make work easier and more efficient.

Comments on Enterprise Service