The increase is super white wine, and the valuation is super semiconductor.

Editor’s note: This article is from the WeChat public account “Juchao Business Review” (ID: tide-biz), author: degree, editor: Wang Fangyu.

Since 2018, the stock prices of liquor and beer companies have continued to rise sharply. But if you compare the increase, Bairun shares (SZ: 002568) will surpass Maotai, Wuliangye, Luzhou Laojiao, Tsingtao Brewery, Chongqing Beer and other big-name companies.

Relying on the market performance of the pre-adjusted cocktail brand RIO, Bairun has been counting from mid-November 2018 until mid-May. In two and a half years, the stock price has increased by nearly 15 times. .

Bairun share price performance (November 2018 to present)

This is a report card that can be described as sensational. Not only are the leading companies in liquor, but even the semiconductor industry leaders with the most certain future market share in the past two years-including Weir shares, Zhaoyi Innovation, etc., have their cumulative gains far behind by Bairun shares.

In short, the stock price increase of Bairun shares in the past two or three years has far surpassed almost all historical-level big bull stocks in this market that investors can call their names.

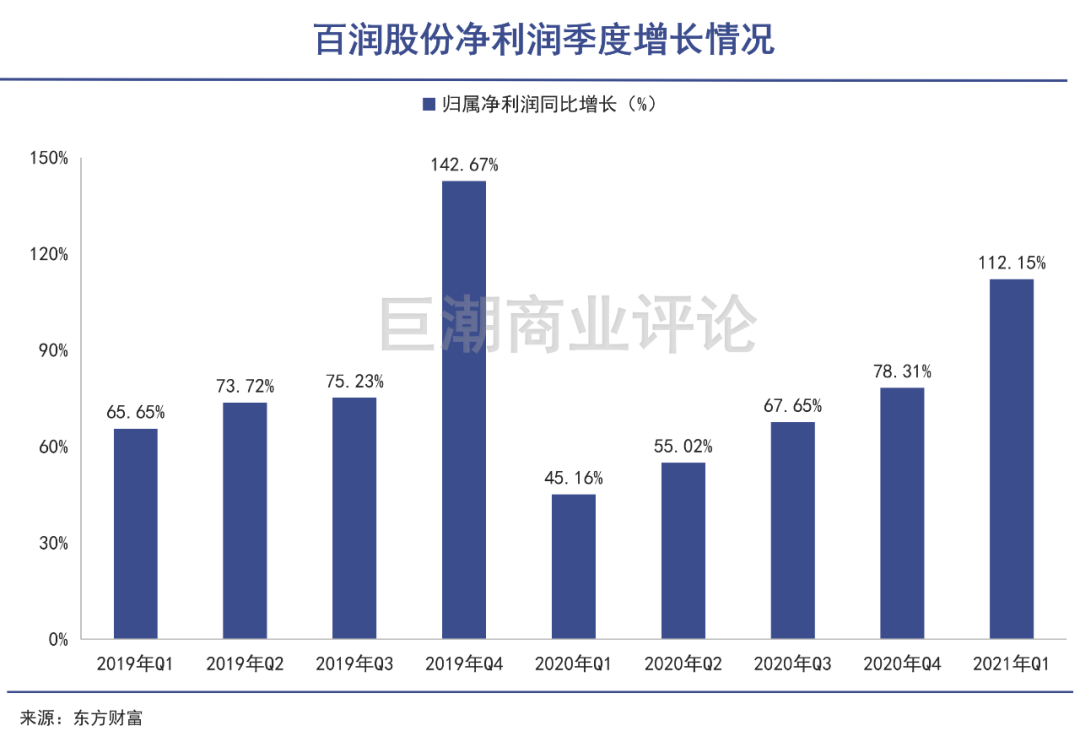

At the same time, under the promotion of marketing, advertising, and channel offensive, RIO branded cocktails appeared on more supermarket shelves. Observing its financial situation, we can also see that since 2019, Bairun’s revenue and net profit have been growing rapidly.

But simply relying on performance growth is simply not enough to drive the stock price to achieve such a scale increase. The valuation of Bairun shares has been continuously pushed up during the process of rising stock prices. At present, the dynamic price-earnings ratio has been above one hundred times for a long time. Whether it is liquor, beer or other consumer goods, there are rarely such highly valued varieties.

From the perspective of brand and product management, the RIO brand has been successful. However, the phenomenal stock price rises in the past two or three consecutive years still make people worry about whether this is a “micro-drunk” or a drunk?

Family Domination and “Davis Double Click”

Reviewing the development history of Bairun shares in recent years, like many industries, it interprets a story of industry reshuffle and “the leftover is king”.

It’s just that because the pre-modified cocktails it is in are still in the market cultivation period, the industry’s reshuffle is more intense and thorough than most industries. Bairun shares as the winner, also in the marketAfter the market was cleared, he fully enjoyed the market dividend.

The earliest pioneer in the domestic pre-mixed cocktail market is actually Bacardi, a foreign giant that entered the Chinese market in 1997. Its pre-mixed wine, Breezer, has been the number one brand of pre-mixed cocktails in China for a long time. . Bairun’s RIO brand is the main competitor.

But the performance of the pre-mixed wine market has been tepid. Until 2012, the domestic pre-mixed cocktail market entered a stage of rapid growth. The report of Boozdata shows that in 2013, the total market size of pre-mixed wine was only 1 billion yuan, but at the end of 2014 this figure had exceeded the 3 billion yuan mark.

In order to seize the market dividend period, Bacardi and Bairun used advertising campaigns to accelerate the introduction of pre-set cocktails to the market. In 2014, the RIO brand surpassed Bingrui and became the industry leader in pre-mixed cocktails, with a market share of over 40%.

But the crisis is also quietly gestating in the high boom of the market. The rapid growth of the preset cocktail industry soon attracted a lot of new players. Brands such as Yanghe, Gujinggong, Wuliangye, Shuijingfang, and even Hei Niu Food have stepped into the pre-mixing business, which eventually caused market saturation, sales difficulties, and inventory backlogs.

The industry then began to clear. In 2015, the production line of the pre-mixed wine business and the president of the Black Bull Food Auction resigned; in 2016, Bingrui, a subsidiary of Bacardi, was blasted and suspended, and layoffs. The pre-mixed cocktail projects of Luzhou Laojiao, Fenjiu, Gujing Gongjiu and other liquor giants have all been Pause or shrink.

Bairun has not gone bankrupt and ceased business, but it has also suffered a decline in sales and losses. In the fourth quarter of 2015, Bairun’s net profit loss reached more than 200 million yuan, while the first three quarters were all profitable. In 2016, Bairun’s revenue fell by more than 60% year-on-year, with a net profit loss of 147 million yuan.

After a crowd of players, especially the biggest rival Bacardi, withdrew from the market, Bairun, as the only remaining industry leader, fully enjoyed the dividends of the industry’s recovery and further consolidated its leading position in the industry.

Shanghai Brewing Professional AssociationThe data shows that RIO’s market share in the cocktail industry has increased year by year in terms of sales volume. In 2019, RIO’s market share in the cocktail industry has increased to 84%, which is already a dominant pattern.

It can be seen that starting from the industry trough in 2016, Bairun’s net interest rate has begun to continue to rise, and it has risen to 23.79% in 2020. Especially since 2019, Bairun’s net profit has continued to grow at a high rate, and in line with the continuous rise of stock prices, it has formed the “Davis Double Click”.

The industry has even shrunk

However, while net profit has soared and market share has soared, Bairun’s future growth remains in doubt.

On the one hand, the market space for pre-made cocktails is not as optimistic as expected. The actual industry growth is limited and slow, and even shrinking and regressing.

Pre-conditioned cocktails were predicted to be the next tens of billions of items during the frothy period of the last round of pre-conditioned cocktail market. Many authoritative organizations have even shouted that by 2020, the industry market will reach 10 billion yuan, 20 billion yuan, or even 30 billion yuan.

For example, in 2014, the China Brewing Industry Association predicted that the pre-conditioned cocktail market will continue to grow rapidly in 2015, and the sales volume in 2020 is expected to exceed 10 billion yuan. In fact, the scale of China’s pre-mixed wine market in 2014 was just close to 4 billion yuan;

But after more than 6 years of development, RIO, which has a market share of 84% in 2019, has only 1.712 billion yuan in revenue. This means that the scale of the industry is only about 2 billion. In other words, in the past few years, the market space for pre-made cocktails has not only not grown, but has shrunk by half.

Many institutions and investors are optimistic about the growth of the pre-made cocktail market because of the low penetration rate in the domestic market. However, there are huge differences in food culture between countries, and the mechanical benchmarking of the United States and Japan may not be appropriate.

According to Euromonitor International, the proportion of pre-mixed wines in Japan, Australia, and the United States in the sales volume of alcoholic beverages has reached 16.6 in 2019.%, 8.1% and 4.5%, and China’s pre-mixed wine sales accounted for only about 0.2%. If the domestic market is raised to the level of the United States and Japan, the market for cocktails will have great development prospects.

However, compared with foreign countries, the unique liquor culture in China will restrict the sales of cocktails in the entire alcohol market to a considerable extent. And the last round of prefabricated cocktail bubbles has proved that the penetration rate of domestic prefabricated cocktails is much slower than imagined.

On the other hand, because it is still in the market cultivation period, the domestic pre-mixing industry has not experienced sufficient competition, and Bairun’s leading position is not stable.

Because the pre-mixed cocktail can be prepared by adding auxiliary materials with high alcohol content, the threshold is not high, but the gross profit is considerable. This is not difficult to see from the previous round of liquor companies, beverage companies, and food companies entering the pre-adjusted cocktail market.

As a result of high gross profit and low threshold, the entire industry is easy to be copied and imitated, resulting in low prices and disorderly competition in the industry.

At present, in the context of the shrinking market size of the entire industry, Bairun shares a one-man show, and the gains from other players’ intervention are not large. However, if the industry resumes high growth, new players will enter the game very smoothly, and Bairun’s seemingly high market share will be quickly invaded.

Bairun obviously recognizes the limitations of the cocktail market. In recent years, it has also expanded its foreign spirits business. In addition to meeting its own raw material needs, it also hopes to occupy a place in the whiskey-based foreign spirits circuit.

However, this part of the business has not yet contributed performance in 2020, and it will still take some time to start production and expand the market, and it is too early to evaluate its future returns. It is also uncertain whether Bairun’s accumulated brand advantages in the cocktail field can be reused in spirits.

Super-growth stocks that don’t deserve their name

No matter how you look at it, the dynamic price-earnings ratio of a listed company of nearly 140 times is too high.

This level of price-earnings ratio generally occurs during the most frenetic period of the market. It is proportional to the bubble period of China’s Growth Enterprise Market and Internet technology stocks in 2015 when the masses started entrepreneurs and innovations, or the US Internet bubble in 2000.

In the consumer product field where the growth rate is relatively slow, and the supply chain, channels, and brand moat are tested, ultra-high valuation categories are even more rare. For example, Bairun shares are rare.

The author believes that for companies with a listed earnings ratio of more than 100 times, except for special circumstances that lead to untrue earnings data, most of the time the starting point for valuation is that this listed company can meet the following conditions at the same time:

1. High growth, annual net profit growth rate is above 50%;

2. High barriers, opponents basically can’t grab their market share, and there are strong moat barriers;

3The market space is huge, such as the level of the global Internet world around 2000.

Only companies that meet these three requirements at the same time are eligible to enjoy a valuation level of more than one hundred times the price-to-earnings ratio. Otherwise, investors may be knocked down by potential risks at any time.

According to the current performance growth of Bairun shares, there has indeed been a number of consecutive quarters of growth, and it seems that it has become a high-growth consumer company. Many public funds and well-known private equity institutions therefore hold firmly.

But if you look closely, you will find that under the sales expense investment of up to 922 million yuan in 2020, Bairun’s income and net profit will be 1.975 billion yuan and 536 million yuan respectively. In comparison, In 2015, revenue was 2.351 billion yuan and net profit was 500 million yuan.

This means that despite the past two years of continuous “high growth”, Bairun’s revenue and profits have only returned to the scale of 2015. In recent years, Bairun has gone through a process of recovery. Only after the exit of competitors, the industry structure has improved and Bairun’s sales expenses have decreased.

In addition, the current market size of only more than 2 billion means that pre-made cocktails are still a typical niche market, and there are many contradictions between the “large market space, high growth, and high barriers” implied by the price-earnings ratio of more than 100 times. . The former “tens of billions of single products”, after several years of development, the market size was cut in half, but a super-big bull stock whose stock price has risen 15 times is left behind, which is also a weird thing about A shares.

Write at the end

Opening the list of institutional shareholders of Bairun shares, a series of names like Leiguaner are listed impressively. E Fund, Dongfanghong, Huitianfu, Shenwanlingxin, Penghua, Nanfang…

Reported data for the first quarter of 2021, a total of 91 funds hold shares of Bairun, accounting for 23.83% of the total circulating shares. Going forward, there are more than 300 funds held in the 2020 annual report.

Some institutional investors, represented by public funds, have made a lot of profits on the 15-fold rise of Bairun shares. In the face of a price-earnings ratio of 140 times, these institutions sit calmly, and it seems that no one wants to leave this gorgeous stage before the music stops.