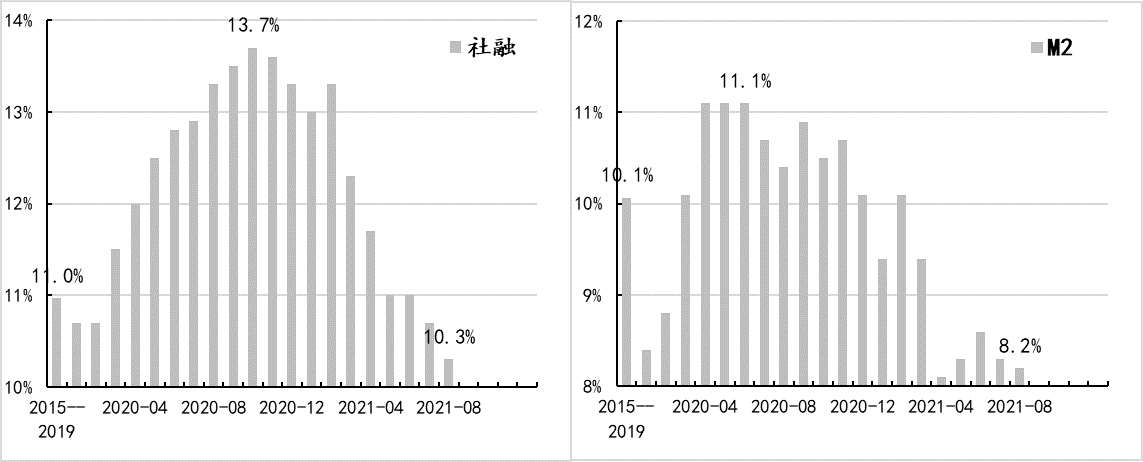

As stated in the last month’s review, “Under the premise of stabilizing the central bank’s balance sheet, the central bank is required to continue to take measures such as reducing RRR and increasing refinancing to hedge. With the implementation of these hedging operations, the money supply side has demand for financing. Before that, financing demand will hardly improve.“, the growth rate of social financing and M2 continued to fall in August, falling to 10.3% and 8.2%, respectively, which are already higher than those during the epidemic. The peak fell sharply and was also significantly lower than the level before the epidemic.

Figure 1: Social financing and M2 growth rate Source of trend data of Wind The debt financing rate has returned to below 30 trillion yuan/year for the first time, during which it reached a maximum of 34.9 trillion yuan/year (February 2021), that is, in the past 6 months, the physical debt financing rate has been significantly reduced by 5.5 trillion yuan /Year, of which entity companies contributed 3.2 trillion yuan/year, the government contributed 1.5 trillion yuan/year, and residents contributed 0.8 trillion yuan/year.

Figure 2: Changes in physical debt financing speed Data source: Wind

There are three main factors restricting financing demand, which correspond to the three categories of the real economy: one is The regulation of the real estate market and the policy of stabilizing the leverage ratio of residents have constrained the growth of residential mortgage loans; second, affected by the strict control of steel production capacity expansion and energy consumption targets, the investment and financing needs of entities have been very limited; third, Upstream price increases are conducive to the growth of fiscal and tax revenues, and to a certain extent alleviate the pressure on fiscal debt financing. Objectively speaking, monetary policy does not have many direct focus on alleviating these three types of constraints. Therefore, from the perspective of policy feasibility In other words, monetary policy is more about stabilizing the money supply side (for specific analysis, please refer to the previous monthly review “Financial Monthly Review|Improving financing demand requires the cooperation of the money supply side”), Try to implement the policy Focus on structural contradictions. On September 1st, the National Standing Committee proposed that “an additional 300 billion yuan of small re-loan lines will be added this year to support local corporate banks in granting loans to small and micro businesses and individual industrial and commercial households. “On September 9, the People’s Bank of China implemented this policy. It not only clarified that 300 billion small re-loans were issued in a “first-loan-after-borrow” model, but also guided the enthusiasm of local banks through better interest rates (the central bank clarified that the The loan interest rate is 2.25%, and the average interest rate for loans issued by banks is around 5.5%). It is roughly estimated that if human cost, capital occupation, tax and other factors are not taken into account, this small loan can bring a 2.25% interest margin to the bank Income, I believe that with such a good policy dividend, the enthusiasm of the bank can be mobilized.

Before the aforementioned three types of factors restricting financing demand are fundamentally reversed, no matter in terms of policy feasibility and effectiveness, monetary policy will focus more on structural contradictions. At the “Analysis Symposium on the Monetary and Credit Situation of Financial Institutions” on August 23, President Yi Gang emphasized “enhancing the stability of total credit growth” while also emphasizing “we must insist on advancing the adjustment of credit structure”. To increase support for key areas and weak links.” If this is used to predict the strength of the monetary policy in the later period, the central bank may also use tools such as refinancing and preferential deposit reserve ratios to promote the adjustment of the credit structure.

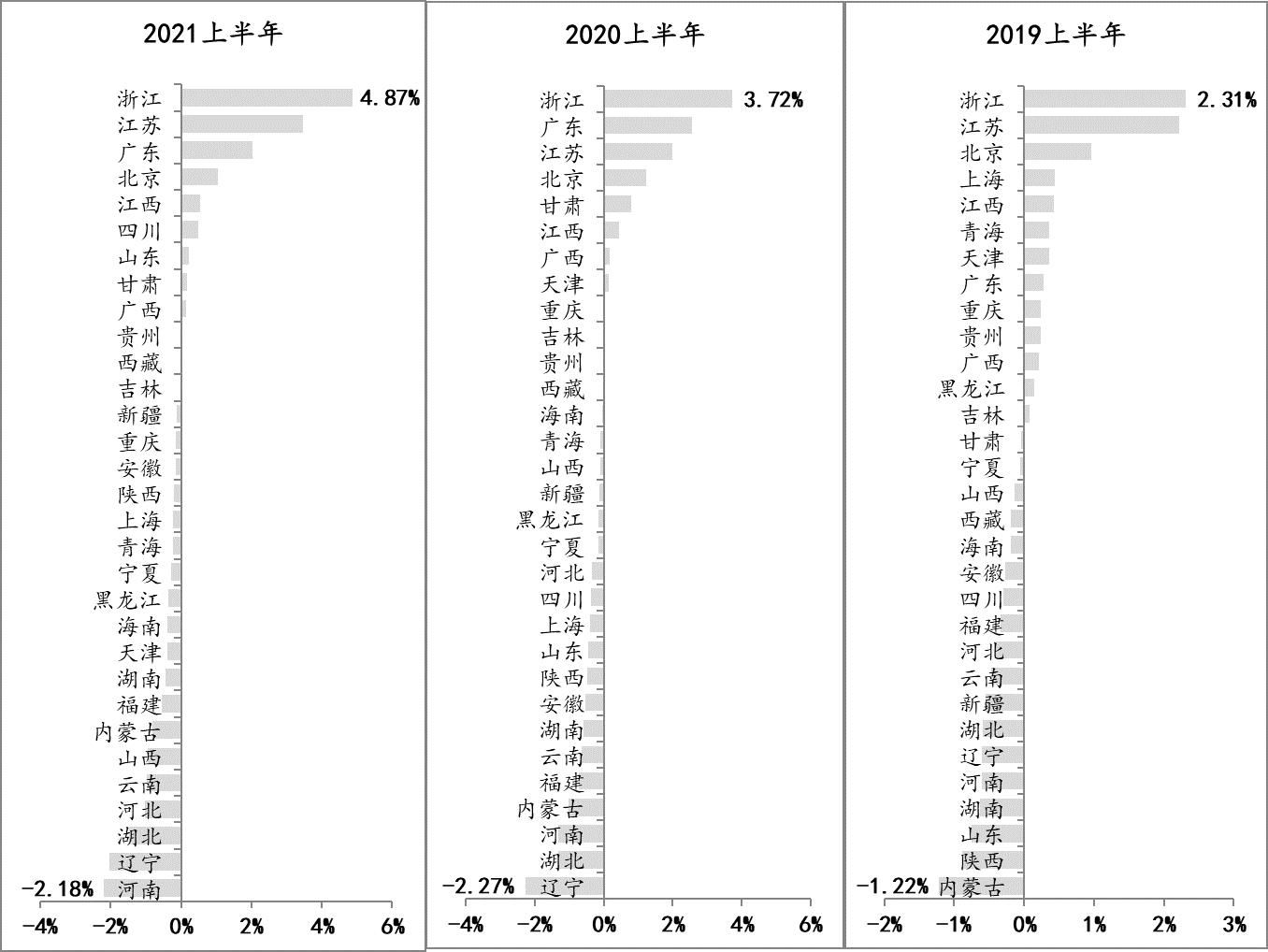

At present, in addition to small and micro, inclusive, incoordination and contradictions between regions are also very obvious. According to the regional social financing data released by the Central Bank, in the first half of this year, 20 of the 31 provinces, autonomous regions, and municipalities in the country had a lower share of social financing than their national GDP, while the other 11 regions’ GDPThe total national proportion is 51%, but the national proportion of social financing exceeds 64%. The difference between the two is as high as 13 percentage points. If you observe the data of the same period for the three years since 2019, the situation of inter-regional incoordination is In the process of continuous expansion, this contradiction is not conducive to the virtuous circle of the national economy and finance to a certain extent. Therefore, increasing credit support to areas with slow credit growth should be another force point for later monetary policy. This year, the central bank has added 200 billion yuan of re-loan lines to relevant regions. The Monetary Policy Implementation Report in the second quarter shows that as of the end of June, the People’s Bank of China has issued 160 billion yuan of re-loans, and the issuance progress reached 80%. It is not ruled out that the central bank will further increase this. Such tools as re-loan lines and preferential deposit reserve ratios.

Figure 3: National share of social financing and GDP by region The data source of the change in the difference of the national proportion: Wind