The latest interpretation of Ping An Bank, Suning and Gome’s supply chain financial model pigeon target “(ID: nigeba77) , author: clay pigeon.

What is supply chain finance

Supply chain finance refers to the financial services provided to upstream and downstream enterprises in the industry chain based on core enterprises, relying on core enterprise credit, and using real transactions as the background.

In the traditional supply chain finance business model, business entities include suppliers (upstream companies), distributors (downstream companies), core companies, banks, warehousing agencies, and logistics companies. The business models mainly include three types , Respectively, account receivables financing model, confirmed warehouse financing model and financing warehouse financing model. Innovations at the technical level include blockchain, and innovations in invoice transaction data counterparty information include Lian Yirong.

The model of supply chain finance is generally referred to as “1 + N”. The bank will support the financing and credit support of a large number of small and medium-sized enterprises “N” based on the credit support of the core company “1”. The domestic supply chain finance 3.0 “N + N” has evolved from the “1 + N” business model of supply chain finance 1.0. Supply Chain Finance 1.0: It mainly focuses on human credit approval, and discusses it on a case-by-case basis. Supply Chain Finance 2.0: With the direct link between banks and enterprises as the core, banks can not only rely on the core company’s credit to grant credit to upstream suppliers and downstream distributors, but also achieve the purpose of acquiring customers in batches. Supply Chain Finance 3.0: With the three-in-one platform as the core, integrating business flow, logistics, and capital flows into the three-in-one information platform, the bank broke the 28 rule.

A detailed explanation of the supply chain financial model

1. Accounts receivable model

Upstream small and medium-sized enterprises will transfer the credit vouchers (receivables for the small and medium-sized enterprises) to the financial institution for financing to carry out their own operations. Financial institutions, the financial institution may collect the receivables from the core enterprise.

2. Prepayment model

Downstream SMEs pay a certain deposit to financial institutions and rely on the credit of core enterprises to lend to financial institutions. The loans obtained can be purchased from core enterprises.

3. Movable property pledge financing

Movable property pledge financing mode may not involve core enterprises, but the business involves the control of cargo rights and the management of logistics supervision enterprises, so it is still considered as one of the models of supply chain finance.

4. Factoring mode

The bank assigns the account receivable formed by the domestic seller (customer) to sell goods or provide services to another buyer who is also in the country. Based on this, it provides the seller with account management of the account receivable. Receivables financing, collection of receivables collection and risk of bad debts of receivables, and other comprehensive financial services. During the transfer of accounts receivable, the act of the bank assigning the seller’s accounts receivable without notifying the buyer to buy a house is called undercover factoring; otherwise, the buyer’s notification is called clear factoring. For customers, the transfer of accounts receivable can achieve the realization of sales repayment in advance and accelerate the turnover of liquidity. In addition, customers are not required to provide collateral and other guarantees required for traditional liquidity loans. Risk points: the authenticity of the buyer and seller’s trade background. The existence and achievability of accounts receivable. Legality and validity of accounts receivable transfer procedures. Lock-in of rebate customers.

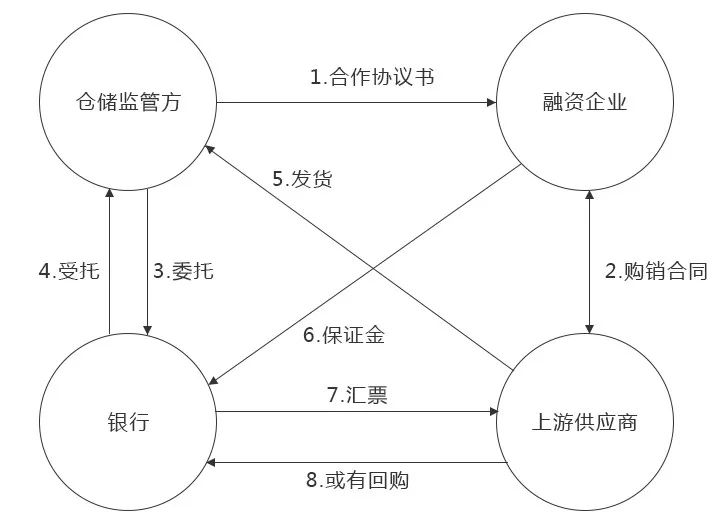

5. Confirmed position financing model

Enterprises that are downstream in the supply chain often need to pay in advance to upstream suppliers in order to obtain the raw materials and finished products required by the enterprise for continuous production and operation. For companies with short-term capital flow difficulties, they can use the confirmed warehouse business to finance a special prepayment of their accounts to obtain short-term credit support from the bank.

In addition to the participation of upstream suppliers, downstream manufacturers (financing companies) and banks in the supply chain, the confirmed warehouse business also requires the participation of warehousing supervisors, mainly responsible for the evaluation and supervision of pledged goods; Confirmed warehouse business requires upstream companies to commit to repurchase, thereby reducing the bank’s credit risk. Financing companies obtain the right to pay for goods in batches and withdraw goods in batches through confirmed warehouse operations, so they do not have to pay the full amount of the goods at one time, which is effective. Alleviated short-term funding pressure for enterprises.

Confirmed warehouse business realizes leveraged procurement of financing companies and bulk sales of suppliers. At the same time, it also brings benefits to banks and achieves a win-win situation. It provides financing facilities for small and medium-sized enterprises at the nodes of the supply chain and effectively solves the financial dilemma of their full purchases. In addition, from the perspective of the bank, the confirmed warehouse business not only further tapped the customer resources for the bank, but the bank acceptance bills issued at the same time can not only provide joint and several liability guarantees by the supplier, but also can be secured by property rights, further reducing Risk assumed.

Supply chain model innovation

Technical Innovation: Blockchain

Blockchain is a fundamental technology-it has the potential to create a new technological foundation for the economy and trading systems of the supply chain finance industry. It is of great significance to solve many problems in the field of supply chain finance.

1. In terms of network structure : The blockchain is based on a peer-to-peer network structure, enabling participants to collaborate peer-to-peer and mesh. This facilitates cross-agency coordination between participants without significant hierarchy or affiliation, without the need to negotiate on the organizational structure, and facilitates the need to negotiate on the organizational structure, as long as the business rules are solidified toThe initial setting of the blockchain is simple and quick.

2. System stability aspects : Blockchain has highly stable characteristics, and can be used as a basic platform for supply chain finance operations to meet supply chain finance The basic requirements of the business for system stability.

3. Trust system : Each node can conduct secure transactions without trust. The biggest role of the blockchain is to effectively solve the problem of trust. The data on the blockchain is highly secure and transactions cannot be withdrawn. At the same time, supply chain financial systems that use blockchain technology often carry out stricter identity authentication and anti-money laundering authentication, which constitutes the blockchain’s trust system.

4. Storage technology : The distributed and collectively maintained storage method allows traders to be anonymous and the transaction information is completely transparent. Participants jointly maintain a ledger with visible data. Through distributed encrypted storage of data, data cannot be tampered with, and integrity is effectively guaranteed.

Blockchain-based supply chain financial solutions: (1) Transparency of supply chain information: Participants in the supply chain ecosystem jointly maintain a public ledger according to the agreement, and each transaction is recorded after all consensus Account. The data on the public ledger is all visible, which can effectively ensure the data subjects’ access rights and data portability rights, and give the data subjects more flexible handling capabilities of their own data. (2) Credit transfer. Due to the consensus mechanism design of the blockchain, the data on the chain cannot be tampered with, traceable, and can carry value. The endorsement utility of core companies can be transmitted along credible financing links, thereby solving the difficulty of transmitting core corporate credit To the end of the supply chain. (3) Smart contract manages performance risks. The smart contract-based performance form not only guarantees the smooth execution of the contract in the absence of third-party supervision, but also eliminates the risk of default that may be caused by manual operations. (4) The convenience of supervision is improved, and the information of supply chain finance is encrypted on the chain and traceable, ensuring the authenticity and accuracy of the data. At the same time, the electronicization of paper documents and the application of smart contracts through the blockchain can effectively obtain regulatory information, analyze and warn capital flows, and analyze and verify the authenticity of trade backgrounds in a timely manner. (5) Reduce financing costs and improve financing efficiency. The combination of blockchain technology and supply chain finance enables upstream and downstream SMEs on the chain to conduct trade authenticity reviews and risk assessments more efficiently. At the same time, because core enterprises can pass credit, the cumbersome verification procedures that have been added due to the crisis of trust in the traditional process can be greatly reduced, and the phenomenon of financial institutions’ prudence and refusal to lend can also be improved.

Blockchain technology advantages: (1) end-to-end information transparency. All relevant parties share information and conduct transactions through a public ledger, improving the efficiency and accuracy of decision-making. (2) Smart contracting of transactions. All transactions are realized through smart contracts, and only transactions that meet the conditions will be executed, reducing the counterparty risk. (3) Electronic paper documents. All paper documents are made electronic, improving process efficiency and reducing operational risks. (4) Information encryption can be traced. All on-chain information is encrypted and traceable, ensuring the authenticity and accuracy of the data, while reducing the difficulty and cost of the audit. (5) Participant operation coordination. All relevant parties jointly maintain process nodes to ensure information synchronization. (6) Distributed data storage. Distributed storage of information and data ensures data integrity.

Although the “blockchain + supply chain finance” solution eliminates many problems, there are also many problems and deficiencies that need to be paid enough attention to: (1) supply chain finance is not suitable for core enterprises The degree of dependence is very high, and companies need to assume additional responsibilities and risks transferred from banks, which is often difficult for companies to accept. (2) The degree of informatization is relatively low. The information related to chain financial business is on the chain, which depends on the informatization of all enterprises in the entire supply chain. For small and medium-sized enterprises, the cost of informatization is relatively high, and the conditions for comprehensive informatization are lacking. (3) Data privacy. The company uploads all transaction data in the business to the chain. In the process of data distribution, preventing data leakage and protecting the privacy of the company is a very serious problem.

Suggestions for strengthening the implementation of blockchain: (1) Strengthen the innovation of blockchain technology, and promote the innovation of key blockchain technologies such as consensus mechanisms, cryptographic algorithms, cross-chain technology, and privacy protection. At the same time, we must learn from the industry’s leading experience and cooperate with banks, colleges, research institutions, etc. to create a technology platform. (2) Exploring the nature of supply chain finance and focusing on business innovation. Before applying blockchain technology to supply chain finance, you need to fully understand the nature and logic of each business in supply chain finance. You should not use a hammer to find nails everywhere. Each business has an essential understanding to find the right path to practice. Supply chain finance also needs to innovate with mature technology under the blessing of blockchain technology to create new business models and promote another qualitative leap in the supply chain finance industry. (3) Constructing a complete blockchain supply chain financial ecology. At present, the application of blockchain to supply chain finance does not yet have a complete ecosystem. In addition to designing a reasonable incentive mechanism to attract participants, blockchain technology is The practice in the field of supply chain finance requires a comprehensive layout, including technology research, business model exploration, landing scenarios, standardization work, supporting facilities, financial supervision and regulations.

Combination analysis of invoice counterparty information

Taking Lianyirong as an example, first sort out the industry, automobile industry, manufacturingManufacturing industry, medical industry, modern agriculture, etc., in each industry will find well-qualified companies, around the core companies in these industries to understand upstream and downstream who do business with it. Modeling and data analysis of small and micro enterprises in these ecosystems. And this kind of data analysis and modeling, taking the tax invoice as an example, the amount is huge, and it deals with the data of billions of tax invoices, which cannot be achieved by traditional manual methods. Use AI technology and big data analysis technology to help small and micro enterprises make a real picture of their operating conditions. The richer the data source, the more complete the historical data collection of small and micro enterprises, and the more accurate the portrait of the business unit. The results of the portraits and the results of the scoring cannot be given to financial institutions as your only tool for risk judgment, but they will complement the good risk judgment of financial institutions before, during, and after lending. We have gone a long way on this road. We think that you have a model that can enforce power, and another model is that you do not need core companies to enforce power or are unwilling to enforce power. Using supply data to expand supply chain finance Will be a more complete solution.

Lian Yirong is to build an ecosystem and serve as a service platform for Fintech supply chain finance. One end connects core enterprises, and connects small and micro enterprises through core enterprises. The other end is connected capital, including capital markets, capital securitization, including industrial funds, and so on. The bottom layer is a variety of modern advanced technologies, including blockchain, including AI. Including big data analysis, but also cloud.

Lian Yirong cooperates with the industry to fully develop the six capabilities of this platform. For example, the digital risk control platform cooperates with financial institutions. The supply chain asset consolidation platform is very efficient. The supply chain financial platform treats the underlying assets very transparently. The asset packages bought by financial institutions are not only spot checks of the underlying package’s asset status and overall analysis. Financial institutions can be allowed to spot check the development of the underlying real-time and keep abreast of changes in underlying assets. The ABC platform is now fully open to financial institutions and core enterprises. The other is a microservices platform. MBS is a platform that uses data and microservices to help financial institutions to solve the problems of opaque information in the market, long operating processes, and high operating costs.

Combined with e-commerce data analysis

1. Analysis of Ping An Orange e-net supply chain financial model

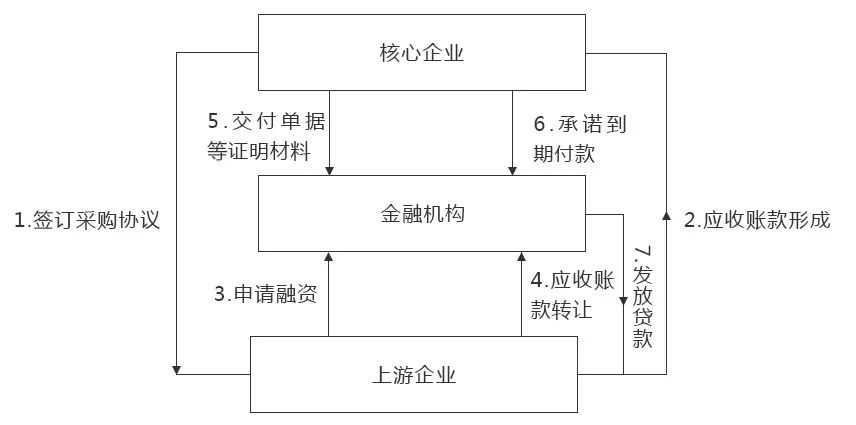

Ping An Bank innovatively launched an e-commerce and financial model, that is, a bank establishes a free business management platform to help customers who have not been effectively improved during the process of industrial Internetization to manage efficiently, conveniently, and at zero cost. The business process from order to warehousing, transportation, and payment. On this basis, the bank is based on the information such as the order, logistics, and payment left by the supplier and the dealer on the bank’s business steward, based on their corresponding credit limit. The purpose of this function isTherefore, it solves the problem of transaction management confusion and inefficiency due to the low level of informationization of some customer groups, and solves the problem of financing difficulties and expensive financing caused by light assets and small scale.

With the Orange e-Net, the orders, freight orders, and receipts generated by companies and upstream and downstream businesses around the transaction are all settled on the platform. These data are used by Ping An Bank to judge an enterprise, especially a SME. The operating conditions provided the basis, thereby changing the information asymmetry between banks and enterprises under the traditional model in the past, the cost of acquiring bank information and the risk of taking too much. At the same time, Ping An Bank, while developing its supply chain finance business, can focus on core companies as the core of risk control in the past, and gradually become a data basis to judge whether the company often operates as the core of risk control.

The financial services in the supply currently being provided are shifting from traditional banking to supply chain finance based on organizational ecology. From the perspective of organizational ecology, Ping An Bank has achieved the precipitation and management of transaction information and data in the entire process of supply chain finance through the construction and operation of the Orange e-net. In order to ensure the integrity and authenticity of these information data, it is also external Collaborators’ platform docking, thus playing the role of a trading platform provider.

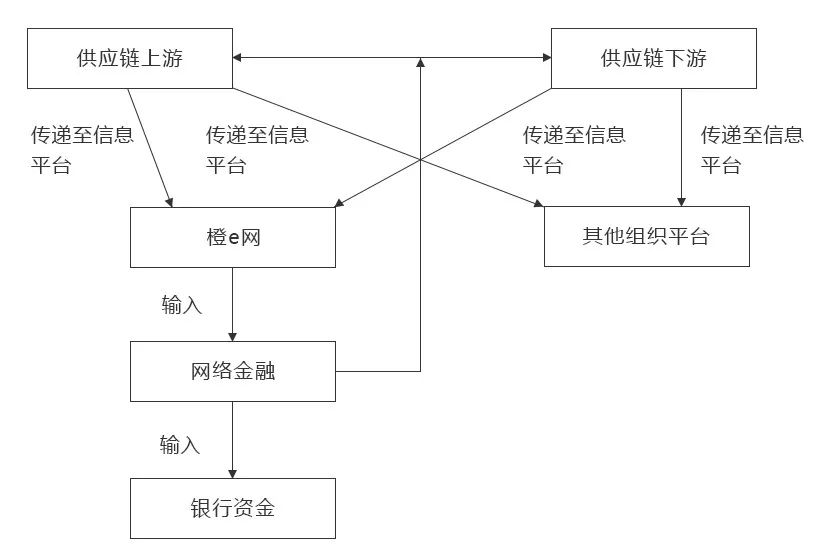

The ecological structure of Ping An Bank’s supply chain financial organization is shown in Figure :

2, Analysis of Suning Financial Supply Chain Financial Model

In terms of participants. As a commercial transaction platform, Suning has established its own financial service company based on the accumulated financial strength of retail entities over the years. Based on the platform, it has established appropriate risk control standards to provide financing services to suppliers in a targeted manner. In the process, Suning’s self-built financial services company has reduced its dependence on banks and gradually replaced the position of commercial banks. At present, Suning’s self-operated supply chain financial business is also trying to establish Suning Bank or access P2P Feng Gao sources its funds. Therefore, Suning’s self-employed e-commerce supply chain finance can directly provide loans to small and medium-sized suppliers on the chain without the need for other topics to participate.

Loan technology. With the help of big data technology and visualization tools, Suning e-commerce platform can retrieve a large amount of different types of data in the platform database as required and output it in the required format.Fully grasp the real data of supply chain companies’ commodities, transactions, and finances, which greatly reduces the cost of identifying investment information, thereby increasing the probability of financing companies obtaining loans.

In terms of financing services. From the perspective of financing objects, Suning is a retail-type e-commerce. The platform itself is a link in the supply chain. The main financing object is upstream brand suppliers. From the perspective of financing quota and frequency, Suning’s supplier financing quota is related to the transaction amount, so the single financing quota is high and the financing frequency is low. All processes of Suning’s supply chain finance are operated electronically and financing is efficient. For financing costs, Suning used its own database system to conduct pre-loan review, which greatly reduced the work of loan officers and reduced the pre-loan costs; the supplier’s sales account was used to settle the loan and reduce the post-loan supervision costs.

3. Analysis of Gome account cloud loan model

Account loan is a factoring product under Gome Financial Holdings, and it is also Gome Financial’s first landing product. The supplier transfers the accounts receivable to Gome Electrical Holdings to Gome Financial Holdings, and from Gome Financial Holdings’ commercial factoring company conducts financing. Compared with banks, the main advantages of commercial factoring companies are market segmentation, data processing and customer service. Based on this, they are more targeted in the selection of target customers, and Credit methods are relatively flexible.

Account Cloud Loan Flowchart:

4. Analysis of CITIC Bank’s Supply Chain Finance Model

The receivables pledge financing that CITIC Bank can provide has the following two methods:

One is the credit guarantee of accounts receivable: CITIC Bank determines the loan amount based on the accounts receivable produced by the loan applicant. For the credit of the loan applicant, this model applies to the account receivables. Low frequency and large single amount; Second, cyclical credit of receivables pledge: CITIC Bank checks and approves applicants based on the continuous and stable number of accounts receivable balances in the previous period. Maximum credit limit for receivables pledged.

For the debtor of the account receivable, because the creditor obtains credit approval by pledged the account receivable to CITIC Bank, the result will reduce the sensitivity of the corresponding account period. Sex, providing more competitive buyers in the long runPay to improve the efficiency of fund use. The upstream supply channels are stable at the same time without having to pay extra fees.

5. Analysis of the Mobil-Bank-Enterprise Communication Model

Mobike has launched supply chain financial strategic cooperation with professional financial institutions such as Ping An Bank, China Merchants Bank, Guangfa Bank, etc., and launched the “Bank-enterprise link” financial cooperation project. Under this model, banks, enterprises, and Mobi platforms work closely together. Based on the online transaction data of corporate customers on Mobi platforms, banks and other financial institutions use Mobi Financial’s pre-risk control and credit evaluation as the basis to provide target companies with Financing through financial cooperation to achieve a trilateral win-win situation.

Bank-enterprise communication is to broaden corporate financing channels and help solve difficult financing problems; second, to use funds flexibly and reduce actual financing costs; third, to provide buyers with competitive raw material procurement channels The fourth is the docking of the Mobike platform system with the bank, and the enterprise receives financing support in real time; the fifth is the early cooperation phase of the project, customers can enjoy Mobbe financial margin and rate discounts; the sixth is to enjoy the transaction management, Value-added services such as sales promotion and derivative finance.

Bank-enterprise communication operation process:

1. Accounts receivable model

Upstream small and medium-sized enterprises will transfer the credit vouchers (receivables for the small and medium-sized enterprises) to the financial institution for financing to carry out their own operations. Financial institutions, the financial institution may collect the receivables from the core enterprise.

2. Prepayment model

Downstream SMEs pay a certain deposit to financial institutions and rely on the credit of core enterprises to lend to financial institutions. The loans obtained can be purchased from core enterprises.

3. Movable property pledge financing

Movable property pledge financing mode may not involve core enterprises, but the business involves the control of cargo rights and the management of logistics supervision enterprises, so it is still considered as one of the models of supply chain finance.

4. Factoring mode

The bank assigns the account receivable formed by the domestic seller (customer) to sell goods or provide services to another buyer who is also in the country. Based on this, it provides the seller with account management of the account receivable. Receivables financing, collection of receivables collection and risk of bad debts of receivables, and other comprehensive financial services. During the transfer of accounts receivable, the act of the bank assigning the seller’s accounts receivable without notifying the buyer to buy a house is called undercover factoring; otherwise, the buyer’s notification is called clear factoring. For customers, the transfer of accounts receivable can achieve the realization of sales repayment in advance and accelerate the turnover of liquidity. In addition, customers are not required to provide collateral and other guarantees required for traditional liquidity loans. Risk points: the authenticity of the buyer and seller’s trade background. The existence and achievability of accounts receivable. Legality and validity of accounts receivable transfer procedures. Lock-in of rebate customers.

5. Confirmed position financing model

Enterprises that are downstream in the supply chain often need to pay in advance to upstream suppliers in order to obtain the raw materials and finished products required by the enterprise for continuous production and operation. For companies with short-term capital flow difficulties, they can use the confirmed warehouse business to finance a special prepayment of their accounts to obtain short-term credit support from the bank.

In addition to the participation of upstream suppliers, downstream manufacturers (financing companies) and banks in the supply chain, the confirmed warehouse business also requires the participation of warehousing supervisors, mainly responsible for the evaluation and supervision of pledged goods; Confirmed warehouse business requires upstream companies to commit to repurchase, thereby reducing the bank’s credit risk. Financing companies obtain the right to pay for goods in batches and withdraw goods in batches through confirmed warehouse operations, so they do not have to pay the full amount of the goods at one time, which is effective. Alleviated short-term funding pressure for enterprises.

Confirmed warehouse business realizes leveraged procurement of financing companies and bulk sales of suppliers. At the same time, it also brings benefits to banks and achieves a win-win situation. It provides financing facilities for small and medium-sized enterprises at the nodes of the supply chain and effectively solves the financial dilemma of their full purchases. In addition, from the perspective of the bank, the confirmed warehouse business not only further tapped the customer resources for the bank, but the bank acceptance bills issued at the same time can not only provide joint and several liability guarantees by the supplier, but also can be secured by property rights, further reducing Risk assumed.

Supply chain model innovation

Technical Innovation: Blockchain

Blockchain is a fundamental technology-it has the potential to create a new technological foundation for the economy and trading systems of the supply chain finance industry. It is of great significance to solve many problems in the field of supply chain finance.

1. In terms of network structure : The blockchain is based on a peer-to-peer network structure, enabling participants to collaborate peer-to-peer and mesh. This facilitates cross-agency coordination between participants without significant hierarchy or affiliation, without the need to negotiate on the organizational structure, and facilitates the need to negotiate on the organizational structure, as long as the business rules are solidified toThe initial setting of the blockchain is simple and quick.

2. System stability aspects : Blockchain has highly stable characteristics, and can be used as a basic platform for supply chain finance operations to meet supply chain finance The basic requirements of the business for system stability.

3. Trust system : Each node can conduct secure transactions without trust. The biggest role of the blockchain is to effectively solve the problem of trust. The data on the blockchain is highly secure and transactions cannot be withdrawn. At the same time, supply chain financial systems that use blockchain technology often carry out stricter identity authentication and anti-money laundering authentication, which constitutes the blockchain’s trust system.

4. Storage technology : The distributed and collectively maintained storage method allows traders to be anonymous and the transaction information is completely transparent. Participants jointly maintain a ledger with visible data. Through distributed encrypted storage of data, data cannot be tampered with, and integrity is effectively guaranteed.

Blockchain-based supply chain financial solutions: (1) Transparency of supply chain information: Participants in the supply chain ecosystem jointly maintain a public ledger according to the agreement, and each transaction is recorded after all consensus Account. The data on the public ledger is all visible, which can effectively ensure the data subjects’ access rights and data portability rights, and give the data subjects more flexible handling capabilities of their own data. (2) Credit transfer. Due to the consensus mechanism design of the blockchain, the data on the chain cannot be tampered with, traceable, and can carry value. The endorsement utility of core companies can be transmitted along credible financing links, thereby solving the difficulty of transmitting core corporate credit To the end of the supply chain. (3) Smart contract manages performance risks. The smart contract-based performance form not only guarantees the smooth execution of the contract in the absence of third-party supervision, but also eliminates the risk of default that may be caused by manual operations. (4) The convenience of supervision is improved, and the information of supply chain finance is encrypted on the chain and traceable, ensuring the authenticity and accuracy of the data. At the same time, the electronicization of paper documents and the application of smart contracts through the blockchain can effectively obtain regulatory information, analyze and warn capital flows, and analyze and verify the authenticity of trade backgrounds in a timely manner. (5) Reduce financing costs and improve financing efficiency. The combination of blockchain technology and supply chain finance enables upstream and downstream SMEs on the chain to conduct trade authenticity reviews and risk assessments more efficiently. At the same time, because core enterprises can pass credit, the cumbersome verification procedures that have been added due to the crisis of trust in the traditional process can be greatly reduced, and the phenomenon of financial institutions’ prudence and refusal to lend can also be improved.

Blockchain technology advantages: (1) end-to-end information transparency. All relevant parties share information and conduct transactions through a public ledger, improving the efficiency and accuracy of decision-making. (2) Smart contracting of transactions. All transactions are realized through smart contracts, and only transactions that meet the conditions will be executed, reducing the counterparty risk. (3) Electronic paper documents. All paper documents are made electronic, improving process efficiency and reducing operational risks. (4) Information encryption can be traced. All on-chain information is encrypted and traceable, ensuring the authenticity and accuracy of the data, while reducing the difficulty and cost of the audit. (5) Participant operation coordination. All relevant parties jointly maintain process nodes to ensure information synchronization. (6) Distributed data storage. Distributed storage of information and data ensures data integrity.

Although the “blockchain + supply chain finance” solution eliminates many problems, there are also many problems and deficiencies that need to be paid enough attention to: (1) supply chain finance is not suitable for core enterprises The degree of dependence is very high, and companies need to assume additional responsibilities and risks transferred from banks, which is often difficult for companies to accept. (2) The degree of informatization is relatively low. The information related to chain financial business is on the chain, which depends on the informatization of all enterprises in the entire supply chain. For small and medium-sized enterprises, the cost of informatization is relatively high, and the conditions for comprehensive informatization are lacking. (3) Data privacy. The company uploads all transaction data in the business to the chain. In the process of data distribution, preventing data leakage and protecting the privacy of the company is a very serious problem.

Suggestions for strengthening the implementation of blockchain: (1) Strengthen the innovation of blockchain technology, and promote the innovation of key blockchain technologies such as consensus mechanisms, cryptographic algorithms, cross-chain technology, and privacy protection. At the same time, we must learn from the industry’s leading experience and cooperate with banks, colleges, research institutions, etc. to create a technology platform. (2) Exploring the nature of supply chain finance and focusing on business innovation. Before applying blockchain technology to supply chain finance, you need to fully understand the nature and logic of each business in supply chain finance. You should not use a hammer to find nails everywhere. Each business has an essential understanding to find the right path to practice. Supply chain finance also needs to innovate with mature technology under the blessing of blockchain technology to create new business models and promote another qualitative leap in the supply chain finance industry. (3) Constructing a complete blockchain supply chain financial ecology. At present, the application of blockchain to supply chain finance does not yet have a complete ecosystem. In addition to designing a reasonable incentive mechanism to attract participants, blockchain technology is The practice in the field of supply chain finance requires a comprehensive layout, including technology research, business model exploration, landing scenarios, standardization work, supporting facilities, financial supervision and regulations.

Combination analysis of invoice counterparty information

Taking Lianyirong as an example, first sort out the industry, automobile industry, manufacturingManufacturing industry, medical industry, modern agriculture, etc., in each industry will find well-qualified companies, around the core companies in these industries to understand upstream and downstream who do business with it. Modeling and data analysis of small and micro enterprises in these ecosystems. And this kind of data analysis and modeling, taking the tax invoice as an example, the amount is huge, and it deals with the data of billions of tax invoices, which cannot be achieved by traditional manual methods. Use AI technology and big data analysis technology to help small and micro enterprises make a real picture of their operating conditions. The richer the data source, the more complete the historical data collection of small and micro enterprises, and the more accurate the portrait of the business unit. The results of the portraits and the results of the scoring cannot be given to financial institutions as your only tool for risk judgment, but they will complement the good risk judgment of financial institutions before, during, and after lending. We have gone a long way on this road. We think that you have a model that can enforce power, and another model is that you do not need core companies to enforce power or are unwilling to enforce power. Using supply data to expand supply chain finance Will be a more complete solution.

Lian Yirong is to build an ecosystem and serve as a service platform for Fintech supply chain finance. One end connects core enterprises, and connects small and micro enterprises through core enterprises. The other end is connected capital, including capital markets, capital securitization, including industrial funds, and so on. The bottom layer is a variety of modern advanced technologies, including blockchain, including AI. Including big data analysis, but also cloud.

Lian Yirong cooperates with the industry to fully develop the six capabilities of this platform. For example, the digital risk control platform cooperates with financial institutions. The supply chain asset consolidation platform is very efficient. The supply chain financial platform treats the underlying assets very transparently. The asset packages bought by financial institutions are not only spot checks of the underlying package’s asset status and overall analysis. Financial institutions can be allowed to spot check the development of the underlying real-time and keep abreast of changes in underlying assets. The ABC platform is now fully open to financial institutions and core enterprises. The other is a microservices platform. MBS is a platform that uses data and microservices to help financial institutions to solve the problems of opaque information in the market, long operating processes, and high operating costs.

Combined with e-commerce data analysis

1. Analysis of Ping An Orange e-net supply chain financial model

Ping An Bank innovatively launched an e-commerce and financial model, that is, a bank establishes a free business management platform to help customers who have not been effectively improved during the process of industrial Internetization to manage efficiently, conveniently, and at zero cost. The business process from order to warehousing, transportation, and payment. On this basis, the bank is based on the information such as the order, logistics, and payment left by the supplier and the dealer on the bank’s business steward, based on their corresponding credit limit. The purpose of this function isTherefore, it solves the problem of transaction management confusion and inefficiency due to the low level of informationization of some customer groups, and solves the problem of financing difficulties and expensive financing caused by light assets and small scale.

With the Orange e-Net, the orders, freight orders, and receipts generated by companies and upstream and downstream businesses around the transaction are all settled on the platform. These data are used by Ping An Bank to judge an enterprise, especially a SME. The operating conditions provided the basis, thereby changing the information asymmetry between banks and enterprises under the traditional model in the past, the cost of acquiring bank information and the risk of taking too much. At the same time, Ping An Bank, while developing its supply chain finance business, can focus on core companies as the core of risk control in the past, and gradually become a data basis to judge whether the company often operates as the core of risk control.

The financial services in the supply currently being provided are shifting from traditional banking to supply chain finance based on organizational ecology. From the perspective of organizational ecology, Ping An Bank has achieved the precipitation and management of transaction information and data in the entire process of supply chain finance through the construction and operation of the Orange e-net. In order to ensure the integrity and authenticity of these information data, it is also external Collaborators’ platform docking, thus playing the role of a trading platform provider.

The ecological structure of Ping An Bank’s supply chain financial organization is shown in Figure :

2, Analysis of Suning Financial Supply Chain Financial Model

In terms of participants. As a commercial transaction platform, Suning has established its own financial service company based on the accumulated financial strength of retail entities over the years. Based on the platform, it has established appropriate risk control standards to provide financing services to suppliers in a targeted manner. In the process, Suning’s self-built financial services company has reduced its dependence on banks and gradually replaced the position of commercial banks. At present, Suning’s self-operated supply chain financial business is also trying to establish Suning Bank or access P2P Feng Gao sources its funds. Therefore, Suning’s self-employed e-commerce supply chain finance can directly provide loans to small and medium-sized suppliers on the chain without the need for other topics to participate.

Loan technology. With the help of big data technology and visualization tools, Suning e-commerce platform can retrieve a large amount of different types of data in the platform database as required and output it in the required format.Fully grasp the real data of supply chain companies’ commodities, transactions, and finances, which greatly reduces the cost of identifying investment information, thereby increasing the probability of financing companies obtaining loans.

In terms of financing services. From the perspective of financing objects, Suning is a retail-type e-commerce. The platform itself is a link in the supply chain. The main financing object is upstream brand suppliers. From the perspective of financing quota and frequency, Suning’s supplier financing quota is related to the transaction amount, so the single financing quota is high and the financing frequency is low. All processes of Suning’s supply chain finance are operated electronically and financing is efficient. For financing costs, Suning used its own database system to conduct pre-loan review, which greatly reduced the work of loan officers and reduced the pre-loan costs; the supplier’s sales account was used to settle the loan and reduce the post-loan supervision costs.

3. Analysis of Gome account cloud loan model

Account loan is a factoring product under Gome Financial Holdings, and it is also Gome Financial’s first landing product. The supplier transfers the accounts receivable to Gome Electrical Holdings to Gome Financial Holdings, and from Gome Financial Holdings’ commercial factoring company conducts financing. Compared with banks, the main advantages of commercial factoring companies are market segmentation, data processing and customer service. Based on this, they are more targeted in the selection of target customers, and Credit methods are relatively flexible.

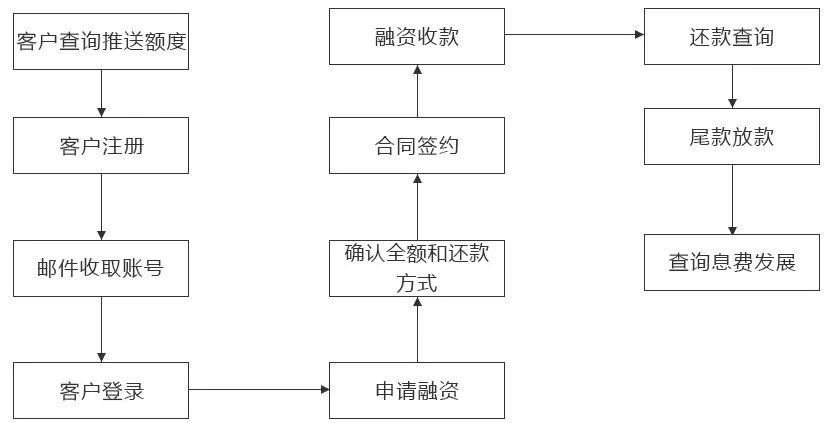

Account Cloud Loan Flowchart:

4. Analysis of CITIC Bank’s Supply Chain Finance Model

The receivables pledge financing that CITIC Bank can provide has the following two methods:

One is the credit guarantee of accounts receivable: CITIC Bank determines the loan amount based on the accounts receivable produced by the loan applicant. For the credit of the loan applicant, this model applies to the account receivables. Low frequency and large single amount; Second, cyclical credit of receivables pledge: CITIC Bank checks and approves applicants based on the continuous and stable number of accounts receivable balances in the previous period. Maximum credit limit for receivables pledged.

For the debtor of the account receivable, because the creditor obtains credit approval by pledged the account receivable to CITIC Bank, the result will reduce the sensitivity of the corresponding account period. Sex, providing more competitive buyers in the long runPay to improve the efficiency of fund use. The upstream supply channels are stable at the same time without having to pay extra fees.

5. Analysis of the Mobil-Bank-Enterprise Communication Model

Mobike has launched supply chain financial strategic cooperation with professional financial institutions such as Ping An Bank, China Merchants Bank, Guangfa Bank, etc., and launched the “Bank-enterprise link” financial cooperation project. Under this model, banks, enterprises, and Mobi platforms work closely together. Based on the online transaction data of corporate customers on Mobi platforms, banks and other financial institutions use Mobi Financial’s pre-risk control and credit evaluation as the basis to provide target companies with Financing through financial cooperation to achieve a trilateral win-win situation.

Bank-enterprise communication is to broaden corporate financing channels and help solve difficult financing problems; second, to use funds flexibly and reduce actual financing costs; third, to provide buyers with competitive raw material procurement channels The fourth is the docking of the Mobike platform system with the bank, and the enterprise receives financing support in real time; the fifth is the early cooperation phase of the project, customers can enjoy Mobbe financial margin and rate discounts; the sixth is to enjoy the transaction management, Value-added services such as sales promotion and derivative finance.

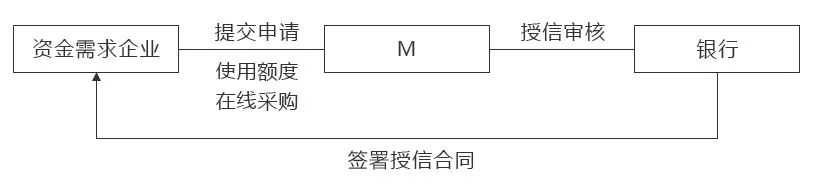

Bank-enterprise communication operation process:

Downstream SMEs pay a certain deposit to financial institutions and rely on the credit of core enterprises to lend to financial institutions. The loans obtained can be purchased from core enterprises.

3. Movable property pledge financing

Movable property pledge financing mode may not involve core enterprises, but the business involves the control of cargo rights and the management of logistics supervision enterprises, so it is still considered as one of the models of supply chain finance.

4. Factoring mode

The bank assigns the account receivable formed by the domestic seller (customer) to sell goods or provide services to another buyer who is also in the country. Based on this, it provides the seller with account management of the account receivable. Receivables financing, collection of receivables collection and risk of bad debts of receivables, and other comprehensive financial services. During the transfer of accounts receivable, the act of the bank assigning the seller’s accounts receivable without notifying the buyer to buy a house is called undercover factoring; otherwise, the buyer’s notification is called clear factoring. For customers, the transfer of accounts receivable can achieve the realization of sales repayment in advance and accelerate the turnover of liquidity. In addition, customers are not required to provide collateral and other guarantees required for traditional liquidity loans. Risk points: the authenticity of the buyer and seller’s trade background. The existence and achievability of accounts receivable. Legality and validity of accounts receivable transfer procedures. Lock-in of rebate customers.

5. Confirmed position financing model

Enterprises that are downstream in the supply chain often need to pay in advance to upstream suppliers in order to obtain the raw materials and finished products required by the enterprise for continuous production and operation. For companies with short-term capital flow difficulties, they can use the confirmed warehouse business to finance a special prepayment of their accounts to obtain short-term credit support from the bank.

In addition to the participation of upstream suppliers, downstream manufacturers (financing companies) and banks in the supply chain, the confirmed warehouse business also requires the participation of warehousing supervisors, mainly responsible for the evaluation and supervision of pledged goods; Confirmed warehouse business requires upstream companies to commit to repurchase, thereby reducing the bank’s credit risk. Financing companies obtain the right to pay for goods in batches and withdraw goods in batches through confirmed warehouse operations, so they do not have to pay the full amount of the goods at one time, which is effective. Alleviated short-term funding pressure for enterprises.

Confirmed warehouse business realizes leveraged procurement of financing companies and bulk sales of suppliers. At the same time, it also brings benefits to banks and achieves a win-win situation. It provides financing facilities for small and medium-sized enterprises at the nodes of the supply chain and effectively solves the financial dilemma of their full purchases. In addition, from the perspective of the bank, the confirmed warehouse business not only further tapped the customer resources for the bank, but the bank acceptance bills issued at the same time can not only provide joint and several liability guarantees by the supplier, but also can be secured by property rights, further reducing Risk assumed.

Supply chain model innovation

Technical Innovation: Blockchain

Blockchain is a fundamental technology-it has the potential to create a new technological foundation for the economy and trading systems of the supply chain finance industry. It is of great significance to solve many problems in the field of supply chain finance.

1. In terms of network structure : The blockchain is based on a peer-to-peer network structure, enabling participants to collaborate peer-to-peer and mesh. This facilitates cross-agency coordination between participants without significant hierarchy or affiliation, without the need to negotiate on the organizational structure, and facilitates the need to negotiate on the organizational structure, as long as the business rules are solidified toThe initial setting of the blockchain is simple and quick.

2. System stability aspects : Blockchain has highly stable characteristics, and can be used as a basic platform for supply chain finance operations to meet supply chain finance The basic requirements of the business for system stability.

3. Trust system : Each node can conduct secure transactions without trust. The biggest role of the blockchain is to effectively solve the problem of trust. The data on the blockchain is highly secure and transactions cannot be withdrawn. At the same time, supply chain financial systems that use blockchain technology often carry out stricter identity authentication and anti-money laundering authentication, which constitutes the blockchain’s trust system.

4. Storage technology : The distributed and collectively maintained storage method allows traders to be anonymous and the transaction information is completely transparent. Participants jointly maintain a ledger with visible data. Through distributed encrypted storage of data, data cannot be tampered with, and integrity is effectively guaranteed.

Blockchain-based supply chain financial solutions: (1) Transparency of supply chain information: Participants in the supply chain ecosystem jointly maintain a public ledger according to the agreement, and each transaction is recorded after all consensus Account. The data on the public ledger is all visible, which can effectively ensure the data subjects’ access rights and data portability rights, and give the data subjects more flexible handling capabilities of their own data. (2) Credit transfer. Due to the consensus mechanism design of the blockchain, the data on the chain cannot be tampered with, traceable, and can carry value. The endorsement utility of core companies can be transmitted along credible financing links, thereby solving the difficulty of transmitting core corporate credit To the end of the supply chain. (3) Smart contract manages performance risks. The smart contract-based performance form not only guarantees the smooth execution of the contract in the absence of third-party supervision, but also eliminates the risk of default that may be caused by manual operations. (4) The convenience of supervision is improved, and the information of supply chain finance is encrypted on the chain and traceable, ensuring the authenticity and accuracy of the data. At the same time, the electronicization of paper documents and the application of smart contracts through the blockchain can effectively obtain regulatory information, analyze and warn capital flows, and analyze and verify the authenticity of trade backgrounds in a timely manner. (5) Reduce financing costs and improve financing efficiency. The combination of blockchain technology and supply chain finance enables upstream and downstream SMEs on the chain to conduct trade authenticity reviews and risk assessments more efficiently. At the same time, because core enterprises can pass credit, the cumbersome verification procedures that have been added due to the crisis of trust in the traditional process can be greatly reduced, and the phenomenon of financial institutions’ prudence and refusal to lend can also be improved.

Blockchain technology advantages: (1) end-to-end information transparency. All relevant parties share information and conduct transactions through a public ledger, improving the efficiency and accuracy of decision-making. (2) Smart contracting of transactions. All transactions are realized through smart contracts, and only transactions that meet the conditions will be executed, reducing the counterparty risk. (3) Electronic paper documents. All paper documents are made electronic, improving process efficiency and reducing operational risks. (4) Information encryption can be traced. All on-chain information is encrypted and traceable, ensuring the authenticity and accuracy of the data, while reducing the difficulty and cost of the audit. (5) Participant operation coordination. All relevant parties jointly maintain process nodes to ensure information synchronization. (6) Distributed data storage. Distributed storage of information and data ensures data integrity.

Although the “blockchain + supply chain finance” solution eliminates many problems, there are also many problems and deficiencies that need to be paid enough attention to: (1) supply chain finance is not suitable for core enterprises The degree of dependence is very high, and companies need to assume additional responsibilities and risks transferred from banks, which is often difficult for companies to accept. (2) The degree of informatization is relatively low. The information related to chain financial business is on the chain, which depends on the informatization of all enterprises in the entire supply chain. For small and medium-sized enterprises, the cost of informatization is relatively high, and the conditions for comprehensive informatization are lacking. (3) Data privacy. The company uploads all transaction data in the business to the chain. In the process of data distribution, preventing data leakage and protecting the privacy of the company is a very serious problem.

Suggestions for strengthening the implementation of blockchain: (1) Strengthen the innovation of blockchain technology, and promote the innovation of key blockchain technologies such as consensus mechanisms, cryptographic algorithms, cross-chain technology, and privacy protection. At the same time, we must learn from the industry’s leading experience and cooperate with banks, colleges, research institutions, etc. to create a technology platform. (2) Exploring the nature of supply chain finance and focusing on business innovation. Before applying blockchain technology to supply chain finance, you need to fully understand the nature and logic of each business in supply chain finance. You should not use a hammer to find nails everywhere. Each business has an essential understanding to find the right path to practice. Supply chain finance also needs to innovate with mature technology under the blessing of blockchain technology to create new business models and promote another qualitative leap in the supply chain finance industry. (3) Constructing a complete blockchain supply chain financial ecology. At present, the application of blockchain to supply chain finance does not yet have a complete ecosystem. In addition to designing a reasonable incentive mechanism to attract participants, blockchain technology is The practice in the field of supply chain finance requires a comprehensive layout, including technology research, business model exploration, landing scenarios, standardization work, supporting facilities, financial supervision and regulations.

Combination analysis of invoice counterparty information

Taking Lianyirong as an example, first sort out the industry, automobile industry, manufacturingManufacturing industry, medical industry, modern agriculture, etc., in each industry will find well-qualified companies, around the core companies in these industries to understand upstream and downstream who do business with it. Modeling and data analysis of small and micro enterprises in these ecosystems. And this kind of data analysis and modeling, taking the tax invoice as an example, the amount is huge, and it deals with the data of billions of tax invoices, which cannot be achieved by traditional manual methods. Use AI technology and big data analysis technology to help small and micro enterprises make a real picture of their operating conditions. The richer the data source, the more complete the historical data collection of small and micro enterprises, and the more accurate the portrait of the business unit. The results of the portraits and the results of the scoring cannot be given to financial institutions as your only tool for risk judgment, but they will complement the good risk judgment of financial institutions before, during, and after lending. We have gone a long way on this road. We think that you have a model that can enforce power, and another model is that you do not need core companies to enforce power or are unwilling to enforce power. Using supply data to expand supply chain finance Will be a more complete solution.

Lian Yirong is to build an ecosystem and serve as a service platform for Fintech supply chain finance. One end connects core enterprises, and connects small and micro enterprises through core enterprises. The other end is connected capital, including capital markets, capital securitization, including industrial funds, and so on. The bottom layer is a variety of modern advanced technologies, including blockchain, including AI. Including big data analysis, but also cloud.

Lian Yirong cooperates with the industry to fully develop the six capabilities of this platform. For example, the digital risk control platform cooperates with financial institutions. The supply chain asset consolidation platform is very efficient. The supply chain financial platform treats the underlying assets very transparently. The asset packages bought by financial institutions are not only spot checks of the underlying package’s asset status and overall analysis. Financial institutions can be allowed to spot check the development of the underlying real-time and keep abreast of changes in underlying assets. The ABC platform is now fully open to financial institutions and core enterprises. The other is a microservices platform. MBS is a platform that uses data and microservices to help financial institutions to solve the problems of opaque information in the market, long operating processes, and high operating costs.

Combined with e-commerce data analysis

1. Analysis of Ping An Orange e-net supply chain financial model

Ping An Bank innovatively launched an e-commerce and financial model, that is, a bank establishes a free business management platform to help customers who have not been effectively improved during the process of industrial Internetization to manage efficiently, conveniently, and at zero cost. The business process from order to warehousing, transportation, and payment. On this basis, the bank is based on the information such as the order, logistics, and payment left by the supplier and the dealer on the bank’s business steward, based on their corresponding credit limit. The purpose of this function isTherefore, it solves the problem of transaction management confusion and inefficiency due to the low level of informationization of some customer groups, and solves the problem of financing difficulties and expensive financing caused by light assets and small scale.

With the Orange e-Net, the orders, freight orders, and receipts generated by companies and upstream and downstream businesses around the transaction are all settled on the platform. These data are used by Ping An Bank to judge an enterprise, especially a SME. The operating conditions provided the basis, thereby changing the information asymmetry between banks and enterprises under the traditional model in the past, the cost of acquiring bank information and the risk of taking too much. At the same time, Ping An Bank, while developing its supply chain finance business, can focus on core companies as the core of risk control in the past, and gradually become a data basis to judge whether the company often operates as the core of risk control.

The financial services in the supply currently being provided are shifting from traditional banking to supply chain finance based on organizational ecology. From the perspective of organizational ecology, Ping An Bank has achieved the precipitation and management of transaction information and data in the entire process of supply chain finance through the construction and operation of the Orange e-net. In order to ensure the integrity and authenticity of these information data, it is also external Collaborators’ platform docking, thus playing the role of a trading platform provider.

The ecological structure of Ping An Bank’s supply chain financial organization is shown in Figure :

2, Analysis of Suning Financial Supply Chain Financial Model

In terms of participants. As a commercial transaction platform, Suning has established its own financial service company based on the accumulated financial strength of retail entities over the years. Based on the platform, it has established appropriate risk control standards to provide financing services to suppliers in a targeted manner. In the process, Suning’s self-built financial services company has reduced its dependence on banks and gradually replaced the position of commercial banks. At present, Suning’s self-operated supply chain financial business is also trying to establish Suning Bank or access P2P Feng Gao sources its funds. Therefore, Suning’s self-employed e-commerce supply chain finance can directly provide loans to small and medium-sized suppliers on the chain without the need for other topics to participate.

Loan technology. With the help of big data technology and visualization tools, Suning e-commerce platform can retrieve a large amount of different types of data in the platform database as required and output it in the required format.Fully grasp the real data of supply chain companies’ commodities, transactions, and finances, which greatly reduces the cost of identifying investment information, thereby increasing the probability of financing companies obtaining loans.

In terms of financing services. From the perspective of financing objects, Suning is a retail-type e-commerce. The platform itself is a link in the supply chain. The main financing object is upstream brand suppliers. From the perspective of financing quota and frequency, Suning’s supplier financing quota is related to the transaction amount, so the single financing quota is high and the financing frequency is low. All processes of Suning’s supply chain finance are operated electronically and financing is efficient. For financing costs, Suning used its own database system to conduct pre-loan review, which greatly reduced the work of loan officers and reduced the pre-loan costs; the supplier’s sales account was used to settle the loan and reduce the post-loan supervision costs.

3. Analysis of Gome account cloud loan model

Account loan is a factoring product under Gome Financial Holdings, and it is also Gome Financial’s first landing product. The supplier transfers the accounts receivable to Gome Electrical Holdings to Gome Financial Holdings, and from Gome Financial Holdings’ commercial factoring company conducts financing. Compared with banks, the main advantages of commercial factoring companies are market segmentation, data processing and customer service. Based on this, they are more targeted in the selection of target customers, and Credit methods are relatively flexible.

Account Cloud Loan Flowchart:

4. Analysis of CITIC Bank’s Supply Chain Finance Model

The receivables pledge financing that CITIC Bank can provide has the following two methods:

One is the credit guarantee of accounts receivable: CITIC Bank determines the loan amount based on the accounts receivable produced by the loan applicant. For the credit of the loan applicant, this model applies to the account receivables. Low frequency and large single amount; Second, cyclical credit of receivables pledge: CITIC Bank checks and approves applicants based on the continuous and stable number of accounts receivable balances in the previous period. Maximum credit limit for receivables pledged.

For the debtor of the account receivable, because the creditor obtains credit approval by pledged the account receivable to CITIC Bank, the result will reduce the sensitivity of the corresponding account period. Sex, providing more competitive buyers in the long runPay to improve the efficiency of fund use. The upstream supply channels are stable at the same time without having to pay extra fees.

5. Analysis of the Mobil-Bank-Enterprise Communication Model

Mobike has launched supply chain financial strategic cooperation with professional financial institutions such as Ping An Bank, China Merchants Bank, Guangfa Bank, etc., and launched the “Bank-enterprise link” financial cooperation project. Under this model, banks, enterprises, and Mobi platforms work closely together. Based on the online transaction data of corporate customers on Mobi platforms, banks and other financial institutions use Mobi Financial’s pre-risk control and credit evaluation as the basis to provide target companies with Financing through financial cooperation to achieve a trilateral win-win situation.

Bank-enterprise communication is to broaden corporate financing channels and help solve difficult financing problems; second, to use funds flexibly and reduce actual financing costs; third, to provide buyers with competitive raw material procurement channels The fourth is the docking of the Mobike platform system with the bank, and the enterprise receives financing support in real time; the fifth is the early cooperation phase of the project, customers can enjoy Mobbe financial margin and rate discounts; the sixth is to enjoy the transaction management, Value-added services such as sales promotion and derivative finance.

Bank-enterprise communication operation process:

The bank assigns the account receivable formed by the domestic seller (customer) to sell goods or provide services to another buyer who is also in the country. Based on this, it provides the seller with account management of the account receivable. Receivables financing, collection of receivables collection and risk of bad debts of receivables, and other comprehensive financial services. During the transfer of accounts receivable, the act of the bank assigning the seller’s accounts receivable without notifying the buyer to buy a house is called undercover factoring; otherwise, the buyer’s notification is called clear factoring. For customers, the transfer of accounts receivable can achieve the realization of sales repayment in advance and accelerate the turnover of liquidity. In addition, customers are not required to provide collateral and other guarantees required for traditional liquidity loans. Risk points: the authenticity of the buyer and seller’s trade background. The existence and achievability of accounts receivable. Legality and validity of accounts receivable transfer procedures. Lock-in of rebate customers.

5. Confirmed position financing model

Enterprises that are downstream in the supply chain often need to pay in advance to upstream suppliers in order to obtain the raw materials and finished products required by the enterprise for continuous production and operation. For companies with short-term capital flow difficulties, they can use the confirmed warehouse business to finance a special prepayment of their accounts to obtain short-term credit support from the bank.

In addition to the participation of upstream suppliers, downstream manufacturers (financing companies) and banks in the supply chain, the confirmed warehouse business also requires the participation of warehousing supervisors, mainly responsible for the evaluation and supervision of pledged goods; Confirmed warehouse business requires upstream companies to commit to repurchase, thereby reducing the bank’s credit risk. Financing companies obtain the right to pay for goods in batches and withdraw goods in batches through confirmed warehouse operations, so they do not have to pay the full amount of the goods at one time, which is effective. Alleviated short-term funding pressure for enterprises.

Confirmed warehouse business realizes leveraged procurement of financing companies and bulk sales of suppliers. At the same time, it also brings benefits to banks and achieves a win-win situation. It provides financing facilities for small and medium-sized enterprises at the nodes of the supply chain and effectively solves the financial dilemma of their full purchases. In addition, from the perspective of the bank, the confirmed warehouse business not only further tapped the customer resources for the bank, but the bank acceptance bills issued at the same time can not only provide joint and several liability guarantees by the supplier, but also can be secured by property rights, further reducing Risk assumed.

Supply chain model innovation

Technical Innovation: Blockchain

Blockchain is a fundamental technology-it has the potential to create a new technological foundation for the economy and trading systems of the supply chain finance industry. It is of great significance to solve many problems in the field of supply chain finance.

1. In terms of network structure : The blockchain is based on a peer-to-peer network structure, enabling participants to collaborate peer-to-peer and mesh. This facilitates cross-agency coordination between participants without significant hierarchy or affiliation, without the need to negotiate on the organizational structure, and facilitates the need to negotiate on the organizational structure, as long as the business rules are solidified toThe initial setting of the blockchain is simple and quick.

2. System stability aspects : Blockchain has highly stable characteristics, and can be used as a basic platform for supply chain finance operations to meet supply chain finance The basic requirements of the business for system stability.

3. Trust system : Each node can conduct secure transactions without trust. The biggest role of the blockchain is to effectively solve the problem of trust. The data on the blockchain is highly secure and transactions cannot be withdrawn. At the same time, supply chain financial systems that use blockchain technology often carry out stricter identity authentication and anti-money laundering authentication, which constitutes the blockchain’s trust system.

4. Storage technology : The distributed and collectively maintained storage method allows traders to be anonymous and the transaction information is completely transparent. Participants jointly maintain a ledger with visible data. Through distributed encrypted storage of data, data cannot be tampered with, and integrity is effectively guaranteed.

Blockchain-based supply chain financial solutions: (1) Transparency of supply chain information: Participants in the supply chain ecosystem jointly maintain a public ledger according to the agreement, and each transaction is recorded after all consensus Account. The data on the public ledger is all visible, which can effectively ensure the data subjects’ access rights and data portability rights, and give the data subjects more flexible handling capabilities of their own data. (2) Credit transfer. Due to the consensus mechanism design of the blockchain, the data on the chain cannot be tampered with, traceable, and can carry value. The endorsement utility of core companies can be transmitted along credible financing links, thereby solving the difficulty of transmitting core corporate credit To the end of the supply chain. (3) Smart contract manages performance risks. The smart contract-based performance form not only guarantees the smooth execution of the contract in the absence of third-party supervision, but also eliminates the risk of default that may be caused by manual operations. (4) The convenience of supervision is improved, and the information of supply chain finance is encrypted on the chain and traceable, ensuring the authenticity and accuracy of the data. At the same time, the electronicization of paper documents and the application of smart contracts through the blockchain can effectively obtain regulatory information, analyze and warn capital flows, and analyze and verify the authenticity of trade backgrounds in a timely manner. (5) Reduce financing costs and improve financing efficiency. The combination of blockchain technology and supply chain finance enables upstream and downstream SMEs on the chain to conduct trade authenticity reviews and risk assessments more efficiently. At the same time, because core enterprises can pass credit, the cumbersome verification procedures that have been added due to the crisis of trust in the traditional process can be greatly reduced, and the phenomenon of financial institutions’ prudence and refusal to lend can also be improved.

Blockchain technology advantages: (1) end-to-end information transparency. All relevant parties share information and conduct transactions through a public ledger, improving the efficiency and accuracy of decision-making. (2) Smart contracting of transactions. All transactions are realized through smart contracts, and only transactions that meet the conditions will be executed, reducing the counterparty risk. (3) Electronic paper documents. All paper documents are made electronic, improving process efficiency and reducing operational risks. (4) Information encryption can be traced. All on-chain information is encrypted and traceable, ensuring the authenticity and accuracy of the data, while reducing the difficulty and cost of the audit. (5) Participant operation coordination. All relevant parties jointly maintain process nodes to ensure information synchronization. (6) Distributed data storage. Distributed storage of information and data ensures data integrity.

Although the “blockchain + supply chain finance” solution eliminates many problems, there are also many problems and deficiencies that need to be paid enough attention to: (1) supply chain finance is not suitable for core enterprises The degree of dependence is very high, and companies need to assume additional responsibilities and risks transferred from banks, which is often difficult for companies to accept. (2) The degree of informatization is relatively low. The information related to chain financial business is on the chain, which depends on the informatization of all enterprises in the entire supply chain. For small and medium-sized enterprises, the cost of informatization is relatively high, and the conditions for comprehensive informatization are lacking. (3) Data privacy. The company uploads all transaction data in the business to the chain. In the process of data distribution, preventing data leakage and protecting the privacy of the company is a very serious problem.

Suggestions for strengthening the implementation of blockchain: (1) Strengthen the innovation of blockchain technology, and promote the innovation of key blockchain technologies such as consensus mechanisms, cryptographic algorithms, cross-chain technology, and privacy protection. At the same time, we must learn from the industry’s leading experience and cooperate with banks, colleges, research institutions, etc. to create a technology platform. (2) Exploring the nature of supply chain finance and focusing on business innovation. Before applying blockchain technology to supply chain finance, you need to fully understand the nature and logic of each business in supply chain finance. You should not use a hammer to find nails everywhere. Each business has an essential understanding to find the right path to practice. Supply chain finance also needs to innovate with mature technology under the blessing of blockchain technology to create new business models and promote another qualitative leap in the supply chain finance industry. (3) Constructing a complete blockchain supply chain financial ecology. At present, the application of blockchain to supply chain finance does not yet have a complete ecosystem. In addition to designing a reasonable incentive mechanism to attract participants, blockchain technology is The practice in the field of supply chain finance requires a comprehensive layout, including technology research, business model exploration, landing scenarios, standardization work, supporting facilities, financial supervision and regulations.

Combination analysis of invoice counterparty information