Intelligence will certainly become an important direction for the development of the global wealth management industry in the next decade.

Editor’s note: This article is from the micro-channel public number “Zero One Finance” (ID: Finance_01) , Author: Yang Ya.

Under the epidemic, traditional enterprises have once again felt the inevitability of “online” transformation, as have the financial and wealth management industries.

BCG and Lufax recently released the “Global Digital Wealth Management Report 2019-2020” forecasting that intelligence will definitely become an important direction for the development of the global wealth management industry in the next decade and bring new opportunities to the wealth management market. And huge market potential, “Let various institutions achieve 15-30% revenue increase and 25-50% profit, and the entire wealth management market asset management scale to achieve 25-50% growth.”

The biggest trend in the future financial industry is that “financial services will be everywhere, that is, not at bank outlets.” The report pointed out that the application of various intelligent technologies will allow all types of financial services including deposits, loans, and remittances to go out of outlets and even out of financial institutions, integrate into various online and offline ecological scenarios, and contact and serve more closely. client.

Facing the opportunities and challenges brought by intelligence, how do traditional wealth management institutions make up for their shortcomings? Is there only one way to build self-built capacity? In the future benign competition ecosystem, how can traditional institutions achieve industry ecological co-prosperity with many participants in the market, and maximize the release of business value brought by the intelligent era?

I. New Opportunities: Millennials and Mass Customers Expand Wealth Management Market

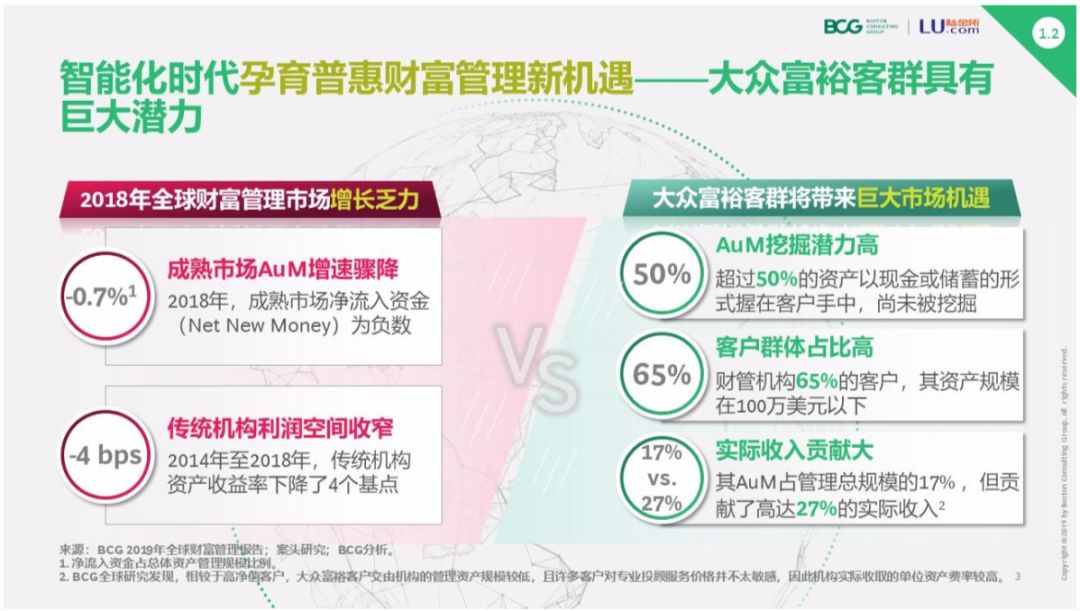

From 2018, the global wealth management market has entered a turning year. According to the calculations reported by BCG and Lujin, the growth rate of the global wealth market in 2018 has fallen to the lowest point in the past half century, and the global wealth market will continue to grow slowly at an average annual rate of 5.7% in the next five years.

At the same time, a number of new “wealth users” entered the market-“Millennials” after 8090 and “Digital Natives” after 00 officially became the main customers group. These “born online” users are not enthusiastic about traditional counter-type financial services such as banks, but they are a future incremental market that cannot be ignored and are expected to become the largest contributors to institutional profits.

Figure 1: Global Treasury Management Market in 2018 and Market Opportunities Brought by the Masses and Rich Clients

Source: BCG & Lufax Global Digital Wealth Management Report 2019-2020

Using traditional offline services, it is difficult to capture this huge customer base: On the one hand, the setting of high thresholds and high rates makes it difficult for traditional wealth management to effectively cover the masses of wealthy people; on the other hand, online The fragmentation and personalization of catalysts brought by the transformation of mobile and mobile terminals make customers become more and more familiar with financial services. From the past waiting for customers to come to the branch in the past, to capture moments of customer demand in real time in different scenarios.

These two changes need to be solved through intelligent means, and at the same time bring a broad market space. According to the report, the intelligent technology represented by AI can bring 25% -50% AUM growth and 15% -30% revenue increase to the entire wealth management market. At the same time, by improving the efficiency and effectiveness of the entire value chain of wealth management institutions, it can bring about a profit improvement of 7-12bps per unit of AUM, that is, a 25% -50% profit margin increase.

Take Lufax as an example. Based on a large amount of user investment, credit and behavioral data accumulated by online wealth management services, Lufax has continuously upgraded the KYC (Know your customer) system. Trillion-dollar products are properly matched, more than 3 million risky transactions are blocked, and higher-quality product security risk control is performed at lower operating costs.

In 2019, Lufax upgraded the KYI (Know your intention) customer intention recognition system, further predicting customer intentions based on behavioral data, realizing timely and timely services, and accurately matching products and services. With the assistance of KYC and KYI, the frequency of user service interactions on the Lufax platform has increased five times over the past, greatly improving the user service area and response speed.

Second, in the face of opportunities and challenges, how do traditional institutions act?

Facing new requirements in the age of intelligence, what actions will traditional institutions take? The report is pleased to find that traditional institutions have reached the incremental market through intelligent applications such as mobile channel innovation, accurate KYC of big data, and intelligent investment advisors to meet the digital and personalized needs of customers in the new era. Even many traditional institutions realize their own disadvantages and quickly acquire and iterate intelligent capabilities through external cooperation.

1. Innovative mobile channel

Under the trend of mobile, mobile terminals and scenarios have become the new battlefield of channels, and mobile APPs have become the platform foundation for promoting intelligent wealth management. In recent years, traditional institutions have also paid more attention to the construction of mobile channel and bottom-level capabilities.

At present, many banks have implemented “mobile”Priority” strategy, and constantly upgrading and iterating on mobile terminal channels, online and intelligent wealth management functions are also embedded in mobile terminal apps. From the perspective of mobile banking user scale, in addition to the Bank of Communications, The number of mobile banking users has reached the level of 100 million households, which has greatly facilitated the promotion of smart wealth management services based on mobile clients.

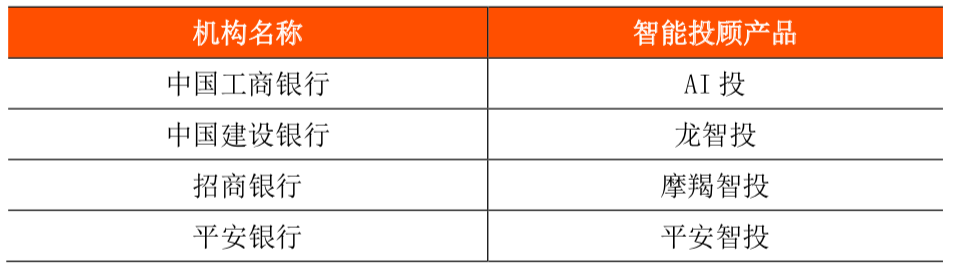

2. Create smart investment advisory products

Intelligent investment consulting, also known as robotic investment consulting, its core lies in the unmanned and intelligent operation of the entire process in the investment management value chain. It is an important intelligent tool covering the wealthy customer base of the public. The report also mentioned that for the mass affluent customer base, intelligent investment advisory services based on technology and algorithms can reduce the cost of traditional manual investment advisory and provide “light advisory services” based on specific wealth management goals.

Table 1: Intelligent investment advisory products launched by some traditional institutions

Source: Public information, ZeroOne Think Tank

Since China Merchants Bank launched “Capricorn Intelligent Investment” in 2016, many traditional institutions have launched intelligent investment advisory products and set up intelligent investment advisory circuits. At present, the banking department has become a force that cannot be ignored in the intelligent investment advisory market, and many banks have launched intelligent investment advisory products.

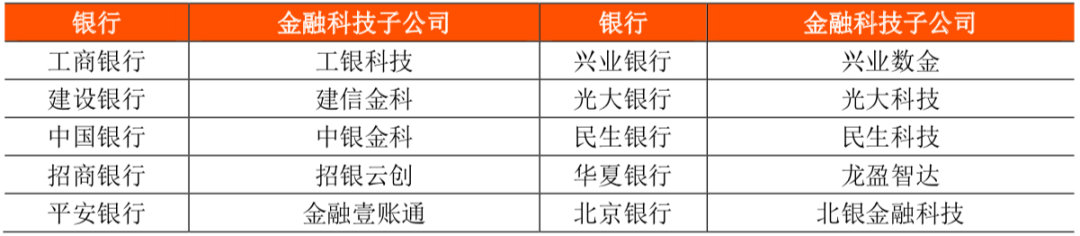

3. Establishing a Fintech subsidiary

The report believes that traditional institutions generally face constraints in terms of organization, talent, culture, and institutional mechanisms. High-level department walls, fragmented data and IT systems, scarce embedded IT resources, and technical personnel, etc. It severely restricts the potential of traditional financial institutions to move towards data-driven and release intelligent value. In order to break through the shackles of institutional mechanisms and cultivate a corporate culture that supports innovation, many traditional institutions in the industry have established fintech subsidiaries to focus on the development and innovation of fintech and underlying technologies.

Table 2: Banking Fintech subsidiaries

Source: Public information,Zero One Think Tank

4. Seeking external cooperation and empowerment

In addition to self-built capabilities, major traditional institutions have also begun to choose to cooperate with fintech companies and Internet giants to quickly acquire and iterate intelligent capabilities to make up for their own system constraints and iterative speed disadvantages in technological breakthroughs and innovations.

Table 3: Wealth management modular applications and intelligent solutions provided by some domestic and foreign fintech companies

Source: Public information, ZeroOne Think Tank

With their own traffic advantages and technical capabilities, Internet giants have launched many cooperations with traditional institutions. There are also many fintech companies that provide modular applications and intelligent solutions to traditional institutions. These fintech companies are also important targets for traditional institutions to seek cooperation.

The report points out that these products or solutions can generally be divided into two categories: one is to start from a pain point in the value chain of intelligent interaction, investment research, and risk control; the other is to provide front, middle, and back-end End-to-end intelligent overall solution.

III. In the future benign competition and cooperation ecology, the advantages will complement each other to realize the co-prosperity of the industry

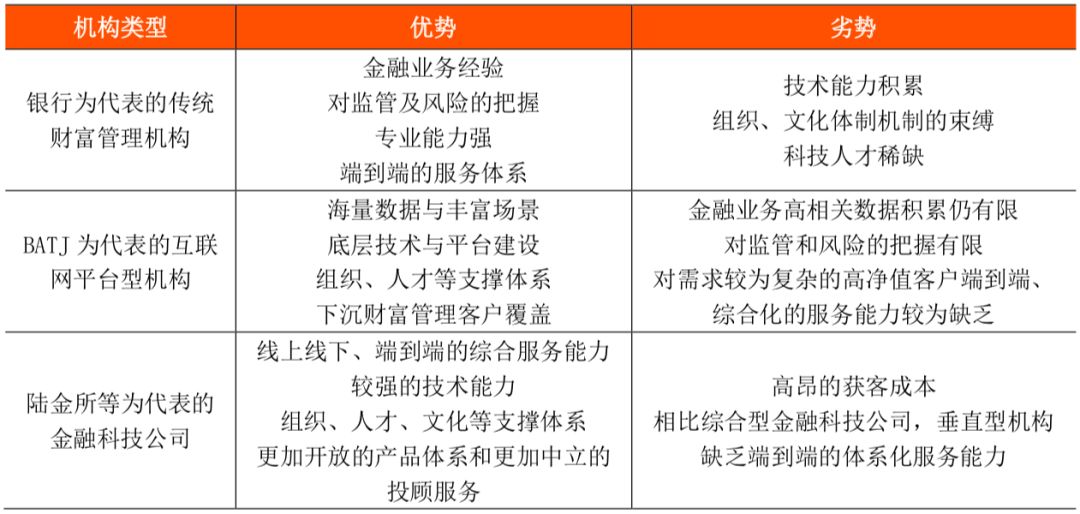

It can also be seen from the intelligent actions of traditional institutions that the relationship between traditional institutions and emerging technology and Internet companies has changed from “not fearful” and “strong threats” to “win-win cooperation”. The report believes that traditional institutions, fintech companies and Internet companies have fully recognized their own advantages and shortcomings, and found their own ecological place in the process of intelligent wealth management, and gradually formed a benign competition ecosystem with innovation as the core. .

Table 4: Advantages and weaknesses of different types of wealth management institutions

Source: “Global Digital Wealth Management Report 2019-2020” by BCG & Lufax, Zero One Think Tank

In this benign competition and cooperation ecosystem, different players on the supply side of the marketIn addition, we are also cooperating in various aspects such as professional knowledge, data and scenes, algorithms and technologies to achieve common prosperity in the industry.

Traditional institutions rely on their professional capabilities and service capabilities to reach cooperation with fintech companies in a more open attitude and in a variety of ways to make up for shortcomings in technology and support systems. Internet platform institutions represented by BATJ have gradually focused on the technology layer and infrastructure layer to build the bottom core of the financial ecosystem. Fintech companies such as Lufax have also undergone a change in model and role: from a single 2C model to a 2B2C model, from a market disruptor to a collaborator and enabler of traditional institutions, providing a certain field for traditional institutions Or end-to-end solution.

Figure 2: Traditional financial management institutions, fintech companies, and platform-based institutions promote each other and promote ecological prosperity.

Source: BCG & Lufax Global Digital Wealth Management Report 2019-2020

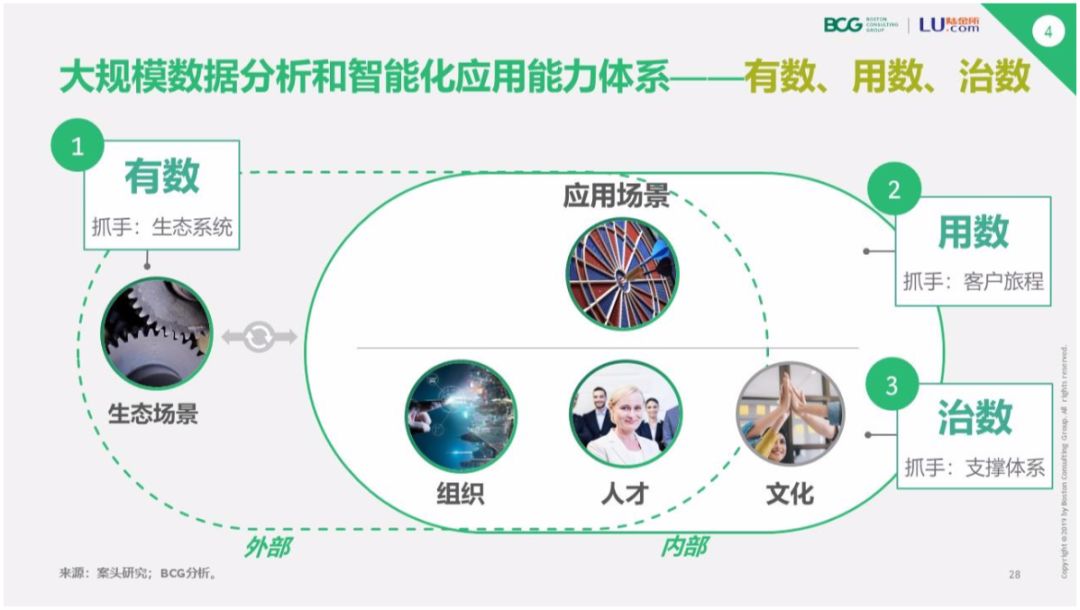

In the future, no matter for traditional or emerging institutions, to seize new opportunities and build moats in the era of intelligence, the report believes that institutions need to build an intelligent system around the three aspects of “numeracy, use, and rule” to build the core ability.

Figure 3: “Number, use, rule” intelligent system

Source: BCG & Lufax Global Digital Wealth Management Report 2019-2020

“Having a number” means building more scenarios and connecting scenes, and gaining more massive, multi-dimensional, highly relevant data through the creation of an open ecology; “Using numbers” needs to start from examining customer value propositions and carry out end-to-end A comprehensive customer journey remodeling; and “Governance” puts forward new requirements for institutional support systems.

As a result, for traditional institutions, in addition to the existing intelligent actions, the core capabilities need to be structured more systematically in the future. The report suggests that, first, data and scenarios