Don’t let the fruits of entrepreneurship go to waste.

Editor’s note: This article is from the micro-channel public number “to bet Practice” (ID: duidushiwu) , Author: Liu Xinbo Ding Shan.

Since the outbreak, many entrepreneurs have consulted us. If the ongoing gambling fails or the transaction defaults, will the result affect the property of themselves and their families?

This is not unfounded. In business practice, examples of entrepreneurs who suffer a major impact on family wealth due to gambling failure and the rights and interests of spouses, parents, and children are not uncommon. For example, Pony Pentium Li Ming Due to an accidental death, the court sentenced his spouse Jin Yan to bear the joint debt of 200 million yuan.

As a result, if the entrepreneur fails to make good property planning, in the event of a sudden incident, the assets of the company, individuals and families may be seized, frozen, insolvent or even confiscated. In addition, there is currently no personal bankruptcy system in the Mainland, and if the debt cannot be paid off, it may become a disaster.

If entrepreneurs can make reasonable property planning before signing the gambling agreement, they can greatly avoid the risk of family wealth shrinkage due to gambling failure. To this end, we use the judicial practice in the mainland as a background to introduce the following four available property isolation methods to provide effective suggestions for entrepreneurs participating in gambling.

Set up a company: isolate the target company from the entrepreneur

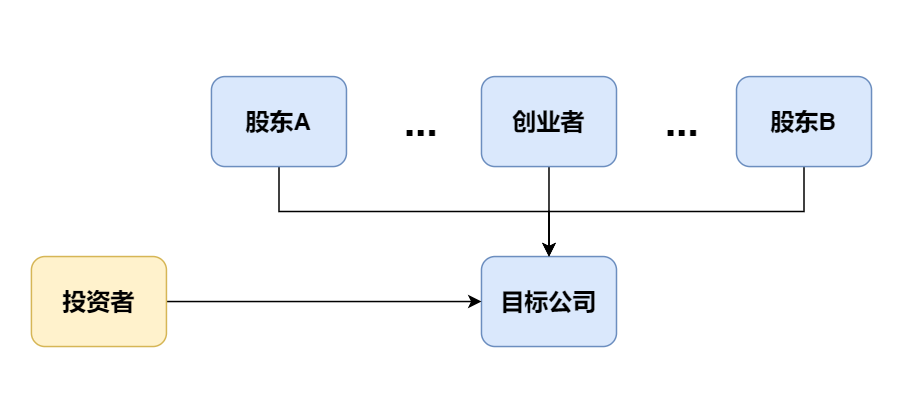

1. Common target company shareholding structure in gambling

When an entrepreneur sets up a target company, he often holds the equity of the target company in his own name (see the figure below). In this common target company’s shareholding structure, entrepreneurs often directly participate in the operation and management of the target company. If the gambling fails, the entrepreneur usually needs to direct the investor to take responsibility according to the agreement on the gambling agreement.

Shareholding structure of the target company common in gambling

When an entrepreneur introduces an external investor, the investor chooses to increase the capital to become a shareholder, transfer the equity of the old shareholder of the target company, or both to become the new shareholder of the target company. Regardless of the method of shareholding, investors will generally sign a gambling agreement with the shareholders of the target company, commonly known as “gambling with shareholders”; at the same time, investThe person may also require the target company to directly bear the debts related to the failure of the gambling in the gambling agreement, or assume the guarantee responsibility for the debts of the target shareholders.

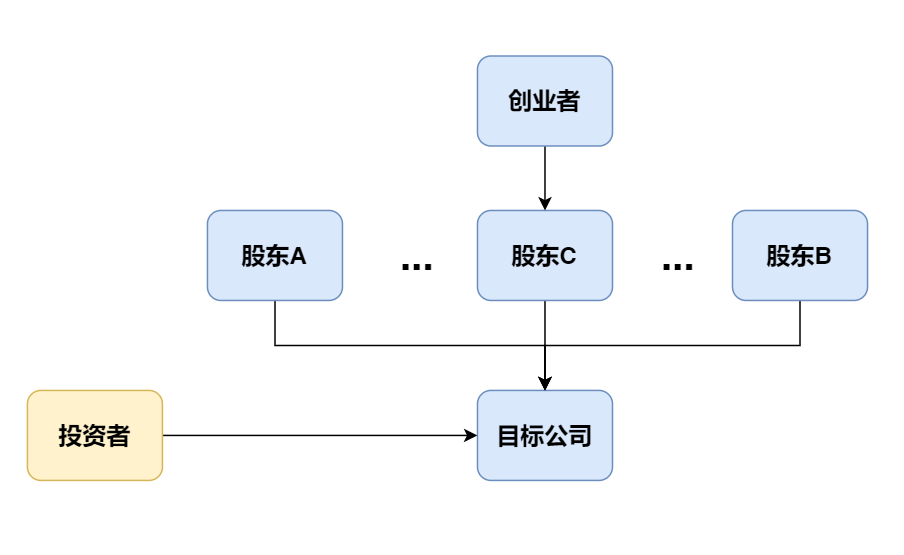

2. The company ’s shareholding structure that isolates the target company from the entrepreneur

Entrepreneurs become parties to gambling, often because entrepreneurs directly hold equity in the target company, so they should be responsible for the gambling commitments of the target company such as performance and listing, so entrepreneurs often cannot isolate individuals from target companies. Furthermore, the risk cannot be isolated when the bet fails.

We suggest that when establishing a target company or before gambling, entrepreneurs further optimize the target company ’s shareholding structure (see the figure below), establish a new company to hold the target company ’s equity, and indirectly hold the target company ’s equity to achieve The effect of property segregation.

Proposed shareholding structure of the target company

As mentioned above, the gambling agreement is usually signed by the investor and the target company ’s shareholders (or the original shareholders). Holding shares, it is possible to isolate the risk of gambling failure.

So how to choose the “isolated subject” between the target company and the entrepreneur?

Some entrepreneurs will choose to set up a limited partnership, the core reason is to save tax. Limited partnerships do not need to bear corporate income tax, while limited liability companies do. In fact, we do not recommend the use of limited partnerships as “isolated subjects”, because the general partners of the partnership should bear unlimited joint and several liabilities for the debts, and the company ’s shareholders only assume limited liability to the company ’s capital. Natural persons invest in the company 1. The use of companies for commercial activities can, to a certain extent, achieve the separation of personal and company property.

If the entrepreneur indirectly holds the target company through the establishment of the company, the entrepreneur is no longer a shareholder of the target company, but becomes the actual controller of the target company. In the case where the investor has not agreed that the actual controller assumes responsibility for gambling, If entrepreneurs fail to gamble, investors generally can only claim responsibility from the shareholders of the target company (that is, the company established by the entrepreneur). Even if the company is insolvent or even bankrupt, investors usually have no right to claim rights from the entrepreneur. To a certain extent, the effect of property isolation is achieved.

In addition, the isolated body can be designed with multiple layers of nesting, and it does not even exclude the construction of overseas structures.

3. Feasibility analysis of establishing a company to isolate risks

Setting up companies to isolate entrepreneurs from target companies is not an innovative method. In practice, we learned that some entrepreneurs even design very complicated shareholding structures and use multiple layers of nesting to make the actual holdings of the target company’s actual controller less clear. The purpose is to hide the target company’s actual controller. But in this way to isolate risks, there are mainly the following two risks.

(1) Realistic risk: Investors “lock” entrepreneurs to take responsibility for gambling

In the practice of gambling, the most common gambling commitment is the entrepreneur, whether or not it is a direct shareholder of the target company.

When investors sign a gamble agreement, the target company will be directly or indirectly controlled by the entrepreneur. Whether the target company can achieve performance, listing and other goals depends on the entrepreneur ’s diligent management. In order to urge entrepreneurs to continue to manage the target company, investors often require investors to assume responsibility for gambling, that is, to “lock” the entrepreneur, regardless of whether the entrepreneur is a shareholder or executive of the target company, he should bear debts after gambling failure . In this case, the establishment of a company to isolate risks will not work.

(2) Legal risk: Denial of corporate personality leads to “penetration” of the shareholding structure

In the gambling transaction, some entrepreneurs have a misunderstanding: the company ’s “shell” is for their own use, and the company ’s assets and investors ’investment can be freely controlled. Once the gambling fails, the company ’s own assets will be repaid. However, personal assets will not be affected. The behavior in this view is a typical shareholder’s abuse of the company’s independent legal person status. In China’s company law, such shareholders will be jointly and severally liable for company debts. This legal system is the company’s personality denial system.

Abuse of a company ’s independent personality is very common in corporate governance. The Supreme Court listed in the “Minutes of the National Court of Civil and Commercial Trial Work Conference” (hereinafter referred to as “Nine Minutes Minutes”) three situations regarding the denial of the company’s independent personality: mixed personality, excessive domination and control, and significant capital shortage . In these three situations, “mixed personality” is more common, and it is reflected in corporate governance. It is usually manifested as a mixture of property and finance between shareholders and companies. Personal debt, etc.

If the entrepreneur abuses the independent status of the company ’s legal person and the limited liability of the shareholders, to evade debts, such as the use of a controlling advantage to transfer assets, unauthorized withdrawal of company assets for their own use, etc. If the company is denied company personality by the people ’s court, the company ’s independent status is abused Of entrepreneurs will be jointly and severally liable for the company ’s debt, and the goal of setting up a company to achieve the separation of the company ’s property from individuals (and their families) will be difficult to achieve.

《People ’s Republic of ChinaParagraph 3 of Article 20 of the Heguo Company Law. If a company shareholder abuses the independent status of the company’s legal person and the limited liability of the shareholder to evade debt and seriously damage the interests of the company’s creditors, it shall bear joint and several liability for the company’s debt.

Another note is that although a one-person limited liability company also has the form of a company, it has only one natural or legal shareholder. The Company Law of the People ’s Republic of China (hereinafter referred to as the “Company Law”) Such companies have special regulations in terms of registration, articles of association, resolutions of shareholders ’meetings, etc., in order to prevent one-person shareholders from abusing the company ’s independent legal person status, resulting in a mixture of shareholders and company property. Article 63 of the “Company Law” specifically stipulates that the shareholders of a one-person limited liability company shall independently bear the burden of proof for the company and the property of the shareholders, otherwise they shall bear joint and several liability for the company. Therefore, if the entrepreneur chooses to establish a company to achieve the effect of property isolation, it is recommended to avoid the establishment of a one-person limited liability company.

Article 63 of the Company Law of the People ’s Republic of China. If the shareholders of a one-person limited liability company cannot prove that the company ’s property is independent of the shareholders ’own property, they shall be jointly and severally liable for the company ’s debt.

4. Summary

Setting up companies to isolate risks is very common in business practice. In gambling, we recommend that entrepreneurs rationally design the target company ’s shareholding structure and isolate the target company from the entrepreneur as much as possible. If the investor does not require the entrepreneur to bear the responsibility for gambling, and the entrepreneur manages the company reasonably and avoids the denial of the personality of the held company, the risk can be effectively isolated, and the goal of property isolation can be achieved.

The couple of entrepreneurs agreed in advance: segregate family property

Question 1: Whether the entrepreneur ’s debt to the gambling failure is the joint debt of the husband and wife

In the gambling transaction, a question that entrepreneurs often consult is: Entrepreneurs sign a gambling agreement in their own name. If the gambling fails, can they only use the entrepreneur ’s personal property to repay? Furthermore, if a couple of entrepreneurs divorces during the gambling period, will they be able to retain part of their family assets? The essence of these two questions is: whether the debt owed by the entrepreneur in the name of the individual in the gambling is the joint debt of the husband and wife, and whether the spouse of the entrepreneur is obliged to repay. The story of Li Ming and Jin Yan, the real controller of Pony Pentium, can give a footnote to this question.

Pony Pentium ’s actual controller Li Ming and the investor signed a gambling agreement. After the failure of the gambling, Li Ming unfortunately passed away. The investor filed a lawsuit and demanded that Jin Yan, as the joint debtor of Li Ming ’s husband and wife, bear the responsibility for gambling. Jin Yan believes that he is unaware of the gambling agreement and the debt should not be regarded as a joint debt of the husband and wife. In the judgment, the court of first instance determined that this was based on the relevant provisions in Article 24 of the Interpretation of the Supreme People ’s Court on Several Issues Concerning the Application of the “Marriage Law of the People ’s Republic of China” (hereinafter referred to as “Interpretation of Marriage Law 2”). The debt is Li MingyuJin Yan’s husband and wife share debts.

Interpretation of the Supreme People ’s Court on Several Issues Concerning the Application of the Marriage Law of the People ’s Republic of China (2) Article 24, paragraph 1 Creditors claiming rights over debts incurred by a spouse in their own name during the marriage Treated as a joint debt of husband and wife. However, except for a spouse who can prove that the creditor and the debtor have clearly agreed to be personal debt, or can prove that they belong to the circumstances specified in Article 19, paragraph 3, of the Marriage Law.

Jin Yan refused to accept the judgment of the first instance and appealed. At this time, the Supreme People’s Court issued the “Interpretation of the Supreme People’s Court on the Issues Concerning the Application of Law in the Trial of Disputes Concerning Couples’ Debt” (Fa Shih [2018] No. 2, implemented on January 18, 2018) (hereinafter referred to as “” Debt Disputes “Judicial Interpretation” stipulates that the debt of one spouse exceeding the family ’s daily needs in the name of the husband and wife shall not be regarded as the joint debt of the husband and wife. Jin Yan even forwarded the news released by the judicial interpretation in the circle of friends, and the attachment believes that he has been liberated .

Article 2 of the Interpretation of the Supreme People ’s Court on Applicable Laws in the Trial of Disputes Concerning Couples ’Debts The people’s court shall support the claim for rights.

However, the court of second instance ruled in accordance with Article 3 of the Judicial Interpretation that Jin Yan was aware of the share repurchase obligations stipulated in the gambling agreement. He was the chairman of Pony Pentium and participated in the joint operation of the company. After Li Ming’s death, Jin Yan’s series of acts confirmed that Li Ming and Jin Yan’s husband and wife jointly operated the company, and the debt involved in the case belonged to the husband and wife’s joint debt.

The Interpretation of the Supreme People ’s Court on Issues Relevant to the Application of Law in the Trial of Disputes Concerning Couples ’Debts The people’s court will not support the claim for the right, but the creditor can prove that the debt is used for husband and wife living together, joint production and operation or expressing based on the common intention of the husband and wife.

In judging the common debt of husband and wife, the law first takes the principle of good faith and “common sense of life” as the basic judgment and presumption standards, supplemented by exceptions. Once the debt caused by the failure of the entrepreneur is determined as the common debt of the husband and wife, the husband and wife of the entrepreneur must jointly assume the obligation of repayment, even if the husband and wife divorce or even one party dies.

In the gambling transaction, the entrepreneur ’s debt to gambling failure is usually beyond the daily life of the family. According to the provisions of the “Judicial Interpretation of Marital Debt Disputes”, it should not be regarded as a joint debt of the entrepreneur ’s husband and wife, but if If the investor can prove that the husband and wife are co-producing and operating (such as the “marriage shop model” in the Pony Pentium case) or that the husband and wife both express their intentions (such as the investor requiring the spouse of the entrepreneur to sign an informed letter / consent letter), then the debt should be deemed Entrepreneur couple debt.

In the Pony Pentium case, Jin Yan believed that he was unaware of Li Ming ’s gambling debt and the debt exceeded the family ’s daily life needs. Investors believed that Jin Yan served as the chairman of Pony Pentium. The debt was caused by the joint production and operation of Li Ming and Jin Yan’s husband and wife. The court finally determined that the pair of gambling debts were the husband and wife’s joint debt.

The enlightenment given to us by this case is that in order to avoid the risk that the entrepreneur ’s debt to the gambling failure is recognized by the court as the joint debt of the husband and wife, it is recommended that the spouse of the entrepreneur should not become a shareholder of the target company and related company established by the entrepreneur Do not hold directors, supervisors, senior executives or even employees in related companies, and should not participate in the operation and management of the target company.

Question 2: Can the entrepreneur ’s husband and wife agree on the distribution of debt and property in advance, can they segregate property?

The entrepreneur ’s debt to gambling failure may be deemed to be the joint debt of the husband and wife, so some entrepreneurs have new problems: if the husband and wife notarize the property before marriage, or during the marriage, the husband ’s debt Can the agreement or notarization of property and property not prevent the entrepreneur from seriously damaging family property when the gambling fails? The answer to this question is also uncertain. It is necessary to judge whether the debt and debt agreement is known and agreed by the investor, whether the investor requires the spouse of the entrepreneur to sign an informed / consent letter, and whether the debt constitutes a joint debt of the spouse.

According to the provisions of the “Marriage Law of the People’s Republic of China” (hereinafter referred to as the “Marriage Law”), both spouses can make a written agreement on the ownership of property before marriage and during the marriage, which is binding on both spouses.

Paragraph 1 of Article 19 of the Marriage Law of the People ’s Republic of China. The husband and wife may agree that the property acquired during the marriage relationship and the property before marriage shall be owned, jointly owned, or partly owned or partly owned. The agreement shall be made in writing. If there is no agreement or the agreement is not clear, the provisions of Articles 17 and 18 of this Law shall apply.

Article 19, paragraph 2 The agreement between the husband and wife on the property acquired during the marriage relationship and the property before marriage is binding on both parties.

Therefore, some entrepreneurs consulted, if couples agreed on family property in writing before the gambling or by a more credible notarization method, can they retain part of the family property when the entrepreneur fails the gambling and avoid the use of all family property Yu assumes the obligation to gamble. However, the Marriage Law also stipulates that the spouse ’s agreement on property only binds the spouse and the spouse can only use one of the property to pay off the debt in accordance with the agreement if the third party (creditor) knows it.

Article 19, paragraph 3, of the Marriage Law of the People ’s Republic of China The property owned by the husband or wife is paid.

According to the above regulations, ifIn order to save part of the family property, the entrepreneur and the spouse can agree to isolate the spouse ’s property and the couple ’s joint debt during the marriage, and disclose and agree to the investor when signing the gambling agreement. Then the agreement is binding on investors. Even if the gambling fails, the entrepreneur can pay off the debt within the scope of the originally agreed property.

But this solution is not always realized. In the practice of gambling, some entrepreneurs transfer property to their spouses in various ways, divorce themselves to “purify themselves”, and then evade the debts resulting from the failure of gambling; or some entrepreneurs cause personal changes due to marriage Property is affected. In order to avoid such risks, investors usually require the spouse of the entrepreneur to sign an informed letter / consent letter, clearly stating that he knows the entrepreneur ’s gambling arrangements and recognizes that the debt is the joint debt of the entrepreneur ’s husband and wife. If the entrepreneur fails gambling, Agree to use family property (or spouse’s personal property) to pay off debts.

This kind of informed letter / consent letter belongs to the commitment between entrepreneur couples and investors (potential creditors) about the debt settlement method of entrepreneurs, if there is no “Civil Law of the People’s Republic of China” and other relevant civil laws and regulations Regarding fraud and coercion, the agreement should be valid. The content of the informed letter / consent letter conflicts with the agreement of the entrepreneur ’s husband and wife, and the signing time is later than the agreement of the entrepreneur ’s husband and wife. Therefore, regarding the settlement of the failed debt of gambling, the content of the informed letter / consent letter should prevail .

Based on the above analysis, the entrepreneur couple can agree on the property of the couple ’s joint or personal property, but in order to achieve the effect of property isolation, it should be disclosed to the investor when signing the anti-gambling agreement. If there is evidence to prove that the investor knows, If there is no clear objection, when the entrepreneur fails to gamble, the spouse of the entrepreneur may save part of the family ’s property according to the agreement. However, if the investor expressly disagrees with the agreement of the entrepreneur ’s spouse, and further requires the entrepreneur ’s spouse to sign an informed letter / consent letter, then the entrepreneur ’s spouse ’s agreement is not binding on the investor, and the entrepreneur cannot implement the individual by this means Separated from family property.

3. Application in betting

Debt during the marriage of husband and wife should generally be regarded as the common debt of the husband and wife, but in a special transaction such as gambling, the entrepreneur ’s debt when the gambling fails is likely to exceed the family ’s daily needs, according to The relevant provisions of the “Judicial Interpretation of Marital Debt Disputes” should be regarded as personal debts of entrepreneurs. However, if the investor can prove that the debt to the gambling is expressed by the husband and wife living together, producing or operating, or the entrepreneur ’s husband and wife, then the debt can be regarded as the joint debt of the entrepreneur ’s husband and wife. Some family property. It is worth noting here that investors bear the burden of proof.

Therefore, it is still recommended that entrepreneur couples agree / notarize their debts and property before marriage or before gamblingInsurance premiums are the entrepreneur ’s own property, so buying life insurance has no effect of isolating the property. Similarly, if the spouse of the entrepreneur is the beneficiary, a similar problem to the beneficiary of the designated trust is that if the gambling debt is regarded as the common debt of the spouse of the entrepreneur, the insurance money obtained by the spouse as the beneficiary may still be invested by the investor carried out. According to the current recommended insurance structure design, entrepreneurs are recommended to designate family members other than their spouses as beneficiaries.

Finally, entrepreneurs should insure before signing a bet.

Some policyholders purchase high amounts of life insurance for “debt avoidance” and designate beneficiaries as other family members. Although the “Insurance Law” does not specifically specify the problem of “malicious insurance”, if the insured maliciously insures in order to avoid debt, if the debt occurs first, the insurance is later, and the insurer’s creditor can prove that the insurer maliciously insured to avoid debt It can then claim that the act of insurance is invalid in accordance with the provisions of Article 52 of the “Contract Law” on “covering illegal purposes in a legal form” and then be compensated for the returned property. Therefore, in order to avoid the risk that the life insurance invested by the entrepreneur is deemed invalid, it should purchase life insurance before the gambling fails. Furthermore, if an entrepreneur buys life insurance after signing a gambling agreement and before the gambling fails, is there still a risk of being deemed to be maliciously insured? At this time, there is a problem of determining whether the entrepreneur has malicious intentions. Entrepreneurs and investors (entrepreneur’s creditors) need proof of proof, so if the entrepreneur wants to avoid the burden of proof after the dispute, we recommend that the entrepreneur try to sign the gambling Purchase life insurance before the agreement.

2. The risk of failing to achieve property segregation when purchasing insurance: the cash value of insurance is enforced

Although the life insurance premium is the property of the beneficiary, investors cannot claim the enforcement of the beneficiary ’s insurance premium after the gambling failure. Judicial practice of insurance cash value. The cash value of insurance is feasible to be executed, so there is still a risk that property isolation cannot be achieved when purchasing life insurance.

The cash value of insurance is different from the beneficiary ’s insurance premium. It refers to the value of personal insurance policies with a savings nature (such as two-insurance insurance, life insurance, universal insurance, etc.). The cash value can be regarded as the surrender money that can be received when the policyholder surrenders the policy, so the cash value of the policy belongs to the policyholder. According to this principle, if an entrepreneur is insured, its cash value can be enforced by investors.

Although the current law does not clearly stipulate whether the policy can be enforced, according to the public cases inquired and documents issued by provinces such as Jiangsu and Zhejiang, it can be seen that the cash value of life insurance products can be enforced by the people’s court.

For example, the “On Strengthening and Regulating the Implementation of Property Benefits of Life Insurance Products Owned by the Executioned Persons” issued by the Zhejiang High Court in 2015The Notice clearly stipulates that the “cash value of the policy after surrender” belongs to the property that can be enforced by the people ’s court; The Notice clearly stipulates that the “cash value (account value, unexpired premiums) available for surrender” belongs to the property that the people ’s court can enforce.

Zhejiang High Court, “Notice on Strengthening and Regulating the Implementation of Property Benefits of Life Insurance Products Owned by the Executed” (Zhegao Fazhi [2015] No. 8) Type, universal life insurance products, survival insurance funds available under the policy agreement, or policy dividends paid in cash, or the cash value of the policy after surrender, all belong to the property rights of the insured, the insured or the beneficiary. When the insured, the insured or the beneficiary is the person to be executed, the property right belongs to the responsible property and the people’s court can enforce it.

Jiangsu High Court, “Notice on Strengthening and Regulating the Implementation of Property Rights of Life Insurance Products Owned by the Enforced Person” The people’s court may execute the case if it belongs to the person being executed. The property rights and interests of life insurance products include the survival insurance money, cash dividends, cash value (account value, unexpired premiums) that can be received according to the insurance contract, and the insurance money that can be confirmed according to the insurance contract but has not been paid. , And other property rights with clear ownership.

Some district courts, such as those in Beijing, Fujian, and Shandong, have made adjudicative documents in support of the enforcement of the property rights and interests of the enforced life insurance. For example, Shandong Higher Court held in an executive objection review ((2015) Lu Zhifu Zi No. 108) that the cash value of the policy belongs to the insured ’s liability property and is not legally personally dependent and specific, It is also not a living item and living expenses necessary for the person subject to execution and his dependents, so it can be executed.

Another question about the cash value of the enforced policy is: only the surrender can obtain the cash value of the policy. Can the court force the policyholder to surrender the policy to enforce the cash value of the policy? China has no clear regulations on this issue, and courts in different regions have different approaches.

For example, the Beijing High Court stated in the “Beijing Court Implementation Work Rules” that the people ’s court shall not compulsorily terminate the insurance contract legal relationship, that is, if the policyholder does not agree to terminate the insurance contract legal relationship, the people ’s court Cash value.

Article 449 of “Beijing Court’s Rules of Enforcement Work” (revised in 2013) [Enforcement of Rights and Interests Enjoyed in Commercial Insurance] The People’s Court may freeze and dispose of commercial insurance invested by the person subject to execution. The executor is based on the rights and interests enjoyed by the insurance contract, but may not forcibly terminate the legal relationship of the insurance contract. …

And some provincial high schools (such as Zhejiang High School, Jiangsu High SchoolIn the execution documents issued by the court, etc., it is believed that the people’s court may issue an execution ruling and an assistance execution notice to the insurance company, and request the insurance company to terminate the insurance contract.

Zhejiang High Court, “Notice on Strengthening and Regulating the Implementation of Property Benefits of Personal Insurance Products Owned by the Executed” (Zhegao Fazhi [2015] No. 8) V. The People’s Court requires insurance institutions to assist in deducting insurance product refunds When the property benefits can be obtained after the guarantee, the surrender application signed by the insured should generally be provided, but if the executor’s whereabouts are unknown, or the refusal to sign the surrender application is signed, the enforcement court may issue an enforcement ruling to the insurance institution and assist the enforcement of the notice The book requires assistance in deduction of insurance products to obtain property benefits after surrendering insurance, and insurance institutions have the obligation to assist.

Jiangsu High Court “Notice on Strengthening and Regulating the Implementation of the Property Rights and Interests of Life Insurance Products Owned by the Executor”

V. … If the insured or the beneficiary fails to deliver the property equivalent to the cash value of the policy after surrender to the people ’s court, the people ’s court may require the policyholder to sign the surrender application and issue an assistance deduction to the insurance company Notice. If the insured person ’s whereabouts is unknown or refuses to sign the surrender application, the people ’s court may directly issue an execution ruling and assistance execution notice to the insurance company, request the insurance company to terminate the insurance contract, and assist in deducting the available property after the insurance product has been surrendered. Insurance companies have the obligation to assist.

After the insurance applicant has not signed the application for surrender, the insurance company will cancel the insurance contract according to the execution of the people ’s court and assist the execution. If the relevant person sues the insurance company for this reason, the people ’s court will not support it.

As for whether the people ’s court has the right to compulsorily terminate the enforceable person ’s insurance contract, the Jiangsu High Court provides an alternative method of enforcement: the beneficiary and other interested parties pay the creditor of the policyholder the equivalent of the cash value The amount is paid off on behalf of and involved in the insurance contract to maintain the continuity of the contract. This approach is also in line with the legislative spirit of the Supreme People’s Court’s “Interpretation of Several Issues Concerning the Application of the Insurance Law of the People’s Republic of China (3).”

Jiangsu High Court “Notice on Strengthening and Regulating the Implementation of Property Rights and Interests of Life Insurance Products Owned by the Executor” When a planned insurance product can obtain property benefits after surrendering, it shall notify the insured and the beneficiary. If the insured or the beneficiary agrees to accept the contract status of the insured, maintain the validity of the insurance contract, and deliver to the people’s court property equivalent to the cash value of the policy after surrender, the people’s court may no longer enforce the cash value of the policy.

Article 17 of the “Interpretation of Several Issues Concerning the Application of the” Insurance Law of the People’s Republic of China “(3)” The policyholder terminates the insurance contract, and the parties claim that the termination of the contract is invalid without the consent of the insured or the beneficiary , The people ’s court does not support it, but the insured or the beneficiary has paid the insuredExcept for the payment of gold value and informing the insurer.

Some provinces and cities in China have issued regulations to implement the cash value of policies, but such regulations are only applicable within the provinces and cities where regulations are promulgated, and are not uniform national implementation standards. If investors apply for the execution of entrepreneurs in the people ’s courts of the above provinces and cities, there is a risk that the execution court may execute the cash value of the policies held by the entrepreneurs.

3. Suggestions

First, pay attention to the structural design of life insurance.

First, entrepreneurs with a high probability of indebtedness or their spouses should not be insured, and the parents of entrepreneurs with a low likelihood of indebtedness are selected as policyholders; second, if the entrepreneur is an insured, avoid When the insured person dies, the insurance money becomes the insured ’s inheritance, and the insured person should designate one or more other persons other than the entrepreneur as the beneficiary; finally, because the entrepreneur ’s creditor may claim that the entrepreneur ’s debt is the entrepreneur ’s couple The common debt of the insurance company, so when the insured person is designated as the beneficiary in the insurance contract (subject to the insured ’s consent), it is recommended that the parent or child of the entrepreneur be designated as the beneficiary.

If entrepreneurs wish to achieve property isolation through insurance planning, they need to design within the scope of insurance-related laws and regulations, combined with the characteristics of insurance architecture, so as to achieve a proactive effect.

Second, choose insurance outside the mainland.

Although life insurance in the mainland has the possibility of property segregation, the cash value of the insurance still has the risk of being enforced in certain provinces and cities, so we recommend that entrepreneurs learn more about insurance companies outside the mainland to apply for insurance .