One clue is the spread of the epidemic worldwide. According to the statistics of the Johns Hopkins University System Science and Engineering Center, as of 10 a.m. Beijing time on April 12, more than 1.77 million people have been infected with new coronary pneumonia worldwide, and it has been confirmed that the number of deaths exceeded 108,000 people. Before effective vaccines and treatments were developed, the current effective measure to contain the epidemic was isolation to reduce the spread of the virus. Therefore, many countries around the world have adopted increasingly strict isolation measures. Before the outbreak is contained, the isolation measures It will continue forever, so the economies of all countries must withstand the direct damage of viruses and the double blow of isolation measures to interrupt the economy.

Another clue is the progress of China’s economic resumption. According to the statistics of CICC ’s daily “start index”, the current national average rate of resumption of work is 85%, and Guangdong, Shanghai, Beijing and Hebei and other regions plan to allow students to return to school in the first half of May. It shows that China is not only advancing the resumption of work in an orderly manner, but also prudently relaxing the isolation measures.

The first uncertainty factor is , since the closure of Wuhan on January 23, China has adopted the most stringent isolation measures, the corresponding short-term impact on the economy is undoubtedly huge, and the first two Monthly economic data also confirmed the severity of the shock. CICC ’s daily “start index” shows that the national average rate of resumption of work at the end of February was 61%, that is, the rate of resumption of work in March increased by 24 percentage points. At this rate, economic operations should return to normal in April, with a rate of 100 %, But CICC data shows that since April, the national recovery rate has basically stabilized at 85% -87%, so when the economic operation will return to normal is still uncertain .

The second uncertain factor is The spread of overseas epidemics and the continued isolation measures of various countries have spillover effects on the Chinese economy from the supply and demand sides, respectively. For example, the change in the operating conditions index of the Chinese enterprises of the Yangtze River Business School shows that potential external attacks and the double impact of demand cannot be underestimated. In March, the company’s sales and employment prospect index was higher than that in February.The rebound, but only 56% and 72% of the average level, and although the inventory forward index fell from February, it is still 1.2 times the average level. The Standing Committee meeting of the Political Bureau of the CPC Central Committee held on April 8 also emphasized “ Be prepared for a longer time to respond to changes in the external environment and prepare for work “, which shows that the spillover impact of external supply and demand on the Chinese economy has been obtained Confirmation at the decision-making level.

Figure 1 Yangtze Business School China Enterprise Operating Index Data Source: Wind The financial data and the policy signal released by the People ’s Bank of China in the first quarter of 2020 financial statistical data press conference may conclude that the layout of the first stage of the response to the epidemic at the monetary and financial level has been completed, that is, “emergency “End of task .

First of all, According to the rule of empirical data that the growth rate of social financing stocks leads GDP growth by one quarter, the cumulative year-on-year growth rate of social financing stocks in the past four quarters was 11.2%, 10.7%, 10.7%, and 11.5%, from this from the perspective of financing, the economy has rebounded in the second quarter, and it has been deployed in advance .

Figure 2 Source of data on social growth and GDP growth: Wind

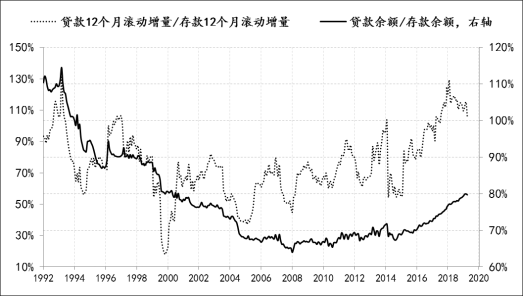

Second , as of the end of March, the deposit-loan ratio of the banking system fell from 79.94% last month to 79.71%, the first decline in seven months, indicating that the mechanism for creating deposits in the first quarter of loans has been improved , And the cumulative net increase in RMB loans in the first quarter of this year was 7.1 trillion, which is the highest value in the first quarter of the calendar year. In other words, Credit issuance is synchronized, and financial idling is converging. This change is conducive to the transmission of monetary policy .

To sum up the three points, in response to the impact of the epidemic, the financial emergency response has been laid out in advance, followed by the short-term bottom of the economic growth in the first quarter and the policy hedge against the economy in the second quarter The focus of financial assistance to entities should also be shifted from “emergency” to “save poverty”, but the problem of “save poverty” is far more complicated than “emergency”. As mentioned above, the two clues to the global economy Under the circumstances, the two uncertainties facing the Chinese economy, how to achieve “saving the poor”, I am afraid that the central bank alone can not afford.

To sum up the three points, in response to the impact of the epidemic, the financial emergency response has been laid out in advance, followed by the short-term bottom of the economic growth in the first quarter and the policy hedge against the economy in the second quarter The focus of financial assistance to entities should also be shifted from “emergency” to “save poverty”, but the problem of “save poverty” is far more complicated than “emergency”. As mentioned above, the two clues to the global economy Under the circumstances, the two uncertainties facing the Chinese economy, how to achieve “saving the poor”, I am afraid that the central bank alone can not afford.