Hotels in Mainland China may not return to pre-epidemic levels until 2022.

Editor’s note: micro-channel public number article from the “Global Travel Weekly” (ID: Traveldaily) , Author: Li Jiayong.

After a long cold winter, the Chinese hotel industry began to pick up gradually.

Many domestic hotel groups have published their occupancy data. For example, Global Travel News once reported that as of March 26, the occupancy rate of China Lodging has returned to 62%. According to official data from Yaduo, the occupancy rate of the entire group exceeded 70% on April 14.

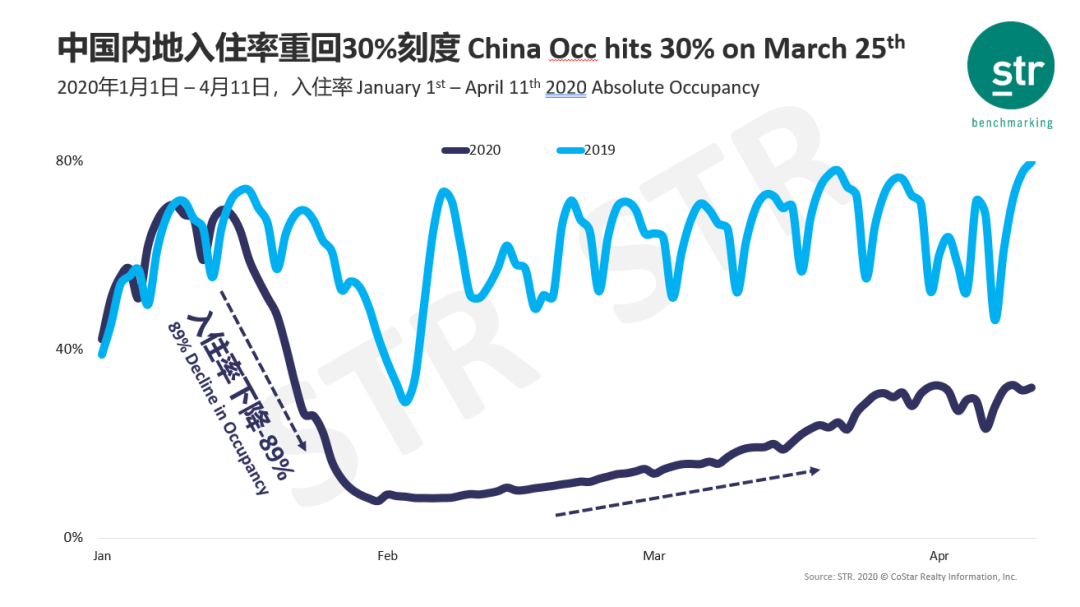

Data source: STR

According to STR’s historical trend of hotel occupancy in Mainland China, from January 1 to April 11 last year, the occupancy rate before the Spring Festival showed a short V-shaped bottoming out. After the Spring Festival travel recovery, the occupancy rate rose rapidly again.

And this year, the first half of January still showed an upward trend, but after reaching the highest point in mid-January, it plummeted all the way to the lowest 7% on February 1. During this period, it was the outbreak of the new crown Critical period. Since February, with the resumption of production in non-epidemic cities, the hotel occupancy rate has slowly recovered, but there is still a large gap from the same period last year. Until March 25, the occupancy rate of hotels in Mainland China exceeded 30%. From April 1 to April 11, the occupancy rate of hotels in Mainland China basically fluctuated between 20% and 40%.

However, with the global outbreak of the epidemic, markets outside of mainland China are also repeating the old path of the Chinese market.

In the beginning of April, the world ’s top 10 hotel orders plummeted by more than 80% year-on-year

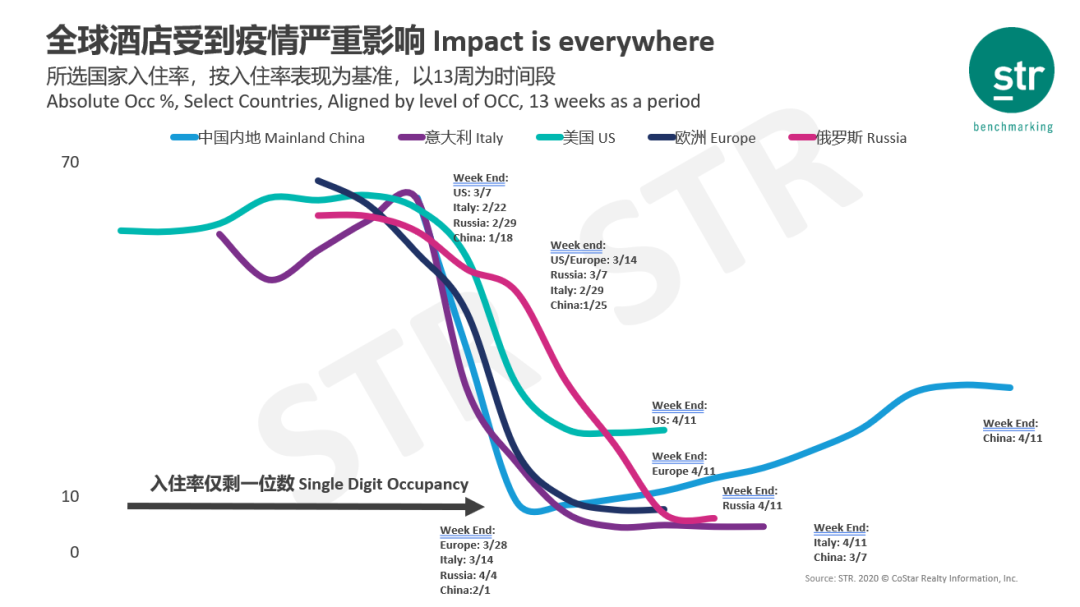

Data source: STR

Comprehensive hotel data of different grades, according to STR data, since mid-March, the occupancy rate of Asian markets except China has dropped significantly. In the United States, Italy, Russia, Europe and other countries and regions further away from us, the hotel was severely affected by the epidemic. Hotel occupancy rates in Italy, Russia, and Europe fell to the bottom on March 14, April 4, and March 28, respectively. As of April 11, the occupancy rates of the above three countries and regions are still less than 10%.

The United States is both an important destination and the country with the worst epidemic. Judging from Dr. Clove’s newly diagnosed trend chart, the number of new cases in the United States has exceeded 100 since March 9 and has been rising ever since. Judging from the historical trend graph of STR, from March 7, the hotel occupancy rate in the United States has ushered in a turning point of decline. It can be seen that the two transition periods are about the same.

In addition to the first blowout of US stocks on March 9, three more blowouts ushered in the next 10 days. On March 18, Global Travel News reported that several industry executives from Marriott, MGM, Disney and Hilton visited the White House to apply for $ 250 billion in emergency assistance from the authorities. Around March 20, Ohio, Louisiana, Delaware, Philadelphia and Dallas successively issued “closure orders”. It can be seen from the trend graph of STR that the occupancy rate of the hotel industry also fell to the bottom at the end of March.

In addition, Italy has been fully closed from March 10th, and STR’s historical trend chart shows that the occupancy rate of Italian hotels fell to the bottom on March 14. Russia began to seal the country on March 30, STR’s historical trend chart shows that the occupancy rate of Russian hotels fell to the bottom on April 4. It can be seen that the spread of the epidemic, the closure of the country and the economic recession have had a huge impact on the hotel occupancy rate.

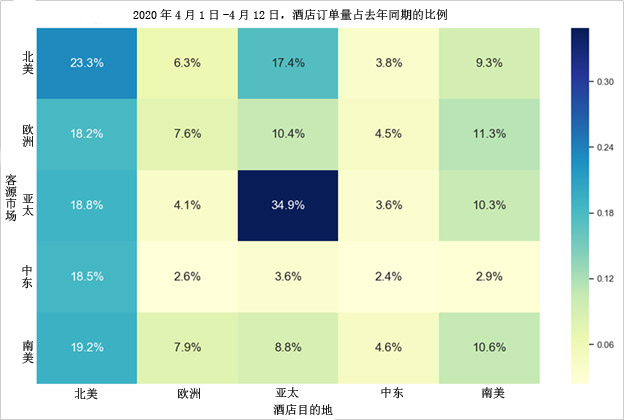

Data source: Derby software

Data from Derby Software, a global hotel distribution technology service provider, showed that in the first 12 days of April, the number of hotel orders from different destinations in the global source market compared to the same period last year, the proportion of guests in the Asia Pacific region booking hotels in the Asia Pacific The highest was 34.9% in the same period last year. North America as a destination, orders from customers from South America, the Middle East, Asia-Pacific, Europe and North America were more than 18% of the same period last year. Zepu in other regionsLess than 10% of the same period last year.

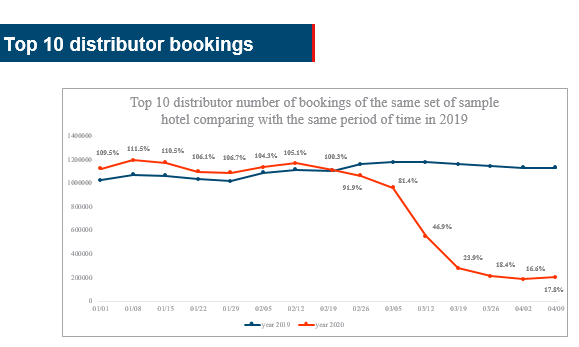

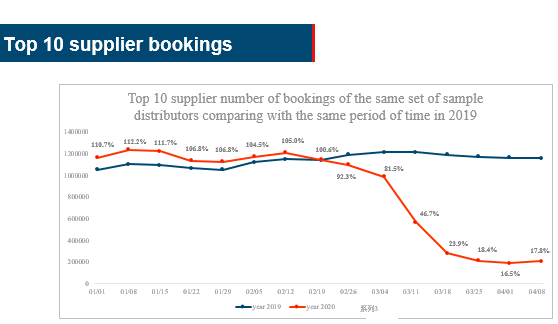

Based on its own data, Derby Software also outlined the overall trend of the world ’s top 10 hotel distributors and supplier orders before April 9 this year.

The top 10 hotel distributors in the world have changed orders, the above picture is provided by Derby Software

The top 10 hotel supplier orders in the world have changed, the above picture is provided by Derby software

As you can see from the above two figures, the booking trends of hotel distributors and suppliers are basically the same. Before February 19, the number of hotel orders this year has been higher than the same period last year. The highest point occurred on January 8, when hotel distributors and suppliers had orders of around 1.2 million, more than 10% higher than the same period last year.

After February 19, the order volume began to decline, and the largest decline occurred on March 11. On the same day, the World Health Organization announced that the 2019 coronavirus epidemic has constituted a global pandemic, and it is not difficult to understand the sudden drop in global hotel orders.

After March 25, global hotel distributors and supplier orders have basically stabilized at around 200,000, less than 20% of the same period last year. The orders of the top 10 global hotel suppliers on April 8 and the orders of the top 10 global hotel distributors on April 9 decreased by 82.8% compared to the same period.

The future is difficult to predict, and it will be difficult for hotels in Mainland China to return to pre-epidemic levels next year

In February and March of this year, Expedia, Booking Holdings and Ctrip, the world’s three major OTA groups, have successively released their 2019 financial reports.

In the performance outlook, Ctrip expects net operating income to decline by 45% -50% year-on-year in the first quarter of 2020. In response to questions from analysts, Ctrip CEO Sun Jie revealed that Ctrip expects to receive accommodation reservations in the first quarter of 2020It fell 60% -65%.

As for Booking Holdings Group and Expedia, the former stated in the earnings outlook that it expects the number of nights between bookings to drop by 5% to 10% year-on-year in the first quarter of 2020, after which the first-quarter performance outlook was withdrawn due to worsening epidemics . Expedia did not provide performance outlook in the financial report due to the impact of the epidemic.

On the other hand, International Hotel Group also reflects its concerns about the development of the hotel industry.

Marriott recently announced that preliminary estimates for global RevPAR in the first quarter of this year have dropped by 23% year-on-year. Global RevPAR is expected to fall by 60% year-on-year in March, and RevPAR in Greater China has fallen by more than 80% year-on-year. In comparison, the RevPAR of Marriott hotels in Greater China fell by nearly 90% year-on-year in February this year. At present, about 25% of the more than 7,300 hotels of the Marriott Group are temporarily closed. Marriott expects that more hotels will be closed next, further affecting the performance of RevPAR.

Recently, Glenn Fogel, CEO of Booking Holdings, said that the number of newly booked room nights has fallen by more than 85% compared with the same period in 2019.

In mid-March, Hilton ’s potential negative impact due to the new crown epidemic will be greater than previously estimated, canceling previously announced performance expectations. Hilton had previously expected earnings per share for the first quarter to be between US $ 0.85 and US $ 0.91, with adjusted EBITDA between US $ 520 million and US $ 540 million, lower than US $ 586 million in Q4 2019. Annual earnings per share are expected to be between US $ 4.08 and US $ 4.21, and adjusted EBITDA is between US $ 2.42 billion and US $ 2.47 billion.

According to Reuters reports, many analysts believe that the InterContinental Hotel Group, headquartered in the United Kingdom, is one of the European companies most directly affected by the epidemic. Before February 19, 160 hotels at InterContinental China had closed or suspended some passenger services. It is expected that in February of this year, the epidemic will affect Intercontinental in mainland China by about US $ 5 million, while Intercontinental ’s annual franchise management business revenue in mainland China is about US $ 100 million.

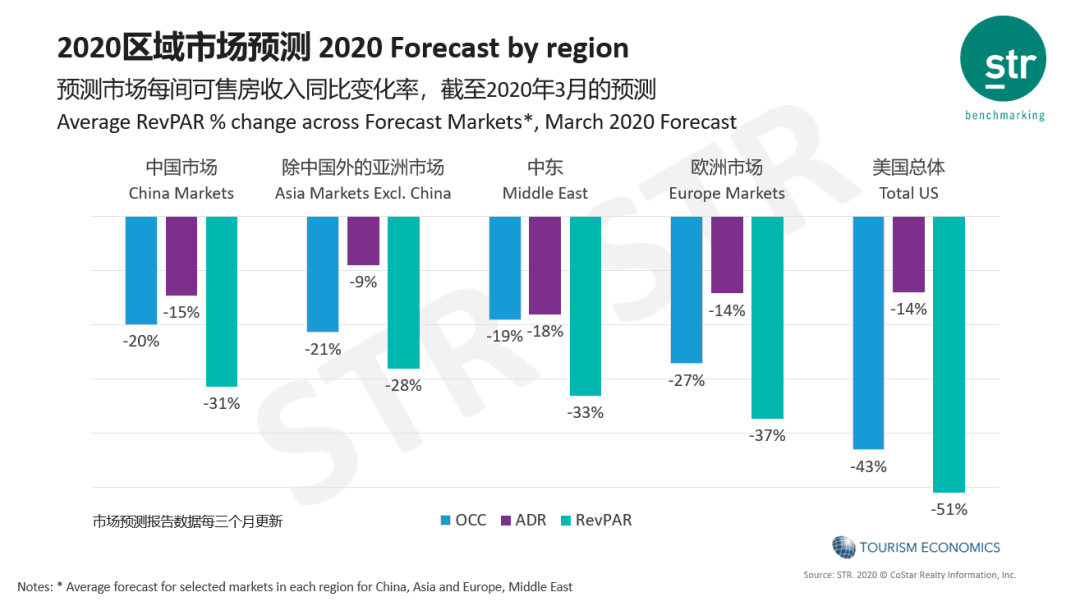

Data source: STR

As of March 2020, STR has made some predictions for some global markets in 2020.Among them, hotel occupancy rates in the Chinese market (based on Beijing Shangguang, Chengdu, and Hangzhou hotel market forecast data) will decline by 20%, ADR by 15%, and RevPAR by 31%. At present, the United States has the largest number of confirmed cases. The predicted occupancy rate will decline by 43%, ADR by 14%, and RevPAR by 51%.

Based on data from the Beijing, Shanghai, Chengdu and Hangzhou hotel markets in March, STR predicts that the hotel market in Mainland China will still not return to 2019 levels in 2021, and the recovery rate of occupancy rate, ADR and RevPAR will be about 90% in 2019 Around 2022, RevPAR is predicted to return to 2019 levels, and occupancy rate will exceed 2019, but ADR is still slightly lower.