With the outbreak of the new coronary pneumonia epidemic in major countries around the world, the world economy is facing a new round of recession. Although the current epidemic situation in China is under initial control, it is difficult for production and life to return to normal in the short term under the background of “foreign defense import and internal defense rebound”.

The service industry, especially the industry with the characteristics of consumer aggregation, will inevitably suffer huge economic losses. Although most other industries have the conditions to resume normal production and operation, the demand (orders) has been greatly reduced due to the global economic downturn. To save economic growth and avoid a hard landing, many economic revitalization plans are on the horizon.

Among the many proposed economic revitalization policies, the “new infrastructure” represented by artificial intelligence, cloud computing, industrial Internet, 5G network, UHV, etc Very high, and received the most criticism and doubt at the same time.

Advocates believe that the new infrastructure represents the future direction of industrial development and can solve the problems of current economic difficulties and the driving force of future economic development in one fell swoop. However, the doubters believe that the problem of huge capital sources for new infrastructure cannot be solved, the role of employment promotion is limited, and the investment benefits cannot be guaranteed, making it difficult to effectively resolve the current economic difficulties. Some people even think that from the perspective of stimulating employment and investment, the stimulus effect of the new infrastructure is still far less than the traditional infrastructure represented by “Tie Gongji”.

When controversy is difficult to divide, we might as well learn from history.

At the end of 2008, in response to the risk of a hard landing that our country might face under the impact of the global financial crisis, China launched a “four trillion” investment plan. This is a large-scale, far-reaching large-scale infrastructure investment plan. According to the estimates of the National Development and Reform Commission, the construction of major infrastructure such as railways, highways, airports, water conservancy and other major infrastructures and urban power grids in China is about 1.5 trillion yuan. In other words, the main capital investment of the “Four Trillion” investment plan is the traditional infrastructure represented by “Tie Gongji”. After that, China successfully took the lead out of the shadow of the global financial crisis.

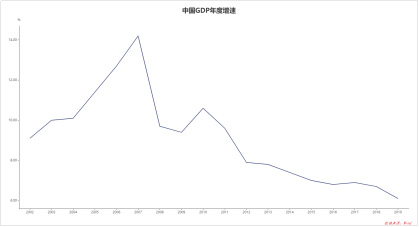

From the perspective of China ’s GDP growth rate, the economic growth rate in 2009 avoided a linear decline similar to that in 2008, and there was a wave of rapid recovery in the economic growth rate from 2010 to 2011 . Although the economic growth rate then re-entered the “new normal” that slowly declined, the short-term downward volatility of the economy was successfully smoothed (see

Figure 1 ).

Figure 1: China ’s annual GDP growth rate The “100 million” investment plan has also significantly increased housing prices, but many people agree that it has effectively hedged the impact of the global financial crisis to a certain extent and prevented large-scale migrant workers from returning to their hometowns. After that, once the economic growth rate fell, people would inevitably think of using increased infrastructure investment to hedge. This new infrastructure is also related to this historical experience.

However, the “successful historical experience” of using large-scale infrastructure investment to hedge the risk of economic recession may only be a historical superficial phenomenon and does not represent historical facts. We have another version of the story of how China quickly emerged from the shadow of the global financial crisis.

Infrastructure investment is generally a project with high investment, low return, and extremely long payback period. Although it may be beneficial to long-term development, it has limited short-term pulling effect on the economy, and may even cause blood loss to the short-term economy and increase macroeconomic risks. From an economic point of view, large-scale government investment may have a “crowding-out effect”, pushing up private investment and consumption costs, thereby reducing private investment and consumption.

Why do other developed countries rarely launch large-scale infrastructure investment plans when facing the same situation? Why does China’s “four trillion” investment plan work first in the world? Is the level of infrastructure development in developed countries too high and there is no need to repeat construction? Did “Tie Gongji” successfully absorb large-scale employment? Not exactly. The Chinese economy is able to quickly get out of the global financial crisis, probably because we have missed an important role that we do not want to be publicly mentioned in our previous analysis. This important role is real estate.

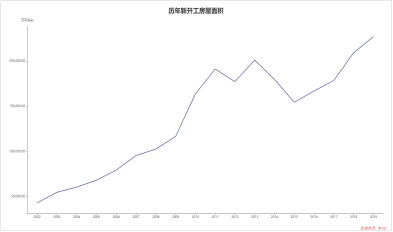

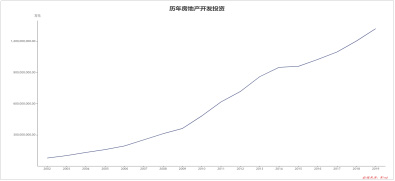

The “Tie Gongji” invested in the “Four Trillion” investment plan may be able to provide sustained momentum for long-term economic development, but it is also true that the short-term economic pulling capacity is insufficient . The reason for the rapid economic situation after the large-scale infrastructure investment, without fear of the shadow of the financial crisis, is only because the real estate industry has been resurrected quickly under the double stimulus of the capital policy (see

Figure 2, Figure 3 ).

Figure 2: Floor area of newly started housing over the years

Figure 3: Real estate development investment over the years Not only that, the large-scale infrastructure investment plan itself also indirectly plays a role in investment and financing for real estate development and sales. Typical examples include large-scale demolition and large-scale construction, and various types of funds flowing into real estate in disguise. Although the “Tie Gongji” has limited effect on short-term employment and economic growth, the real estate industry is an indisputable short-term economic “stimulant”.

This can also explain from another aspect, why developed countries rarely use large-scale infrastructure investment as a short-term economic stimulus. The urbanization process in Western countries has long been over, the living conditions of citizens are relatively high, and there is no real estate at the same time.

New infrastructure investment is not an effective way to save short-term economic growth, nor is the traditional infrastructure “iron public foundation” that can absorb relatively more employment, not real estate. A newly built expressway may not have many cars in three to five years. A new home needs constant decoration, maintenance, and purchase of furniture and appliances from the date of delivery. Not to mention that housing is closely related to marriage and human reproduction.

The fixed parking spaces matching the housing is an important condition for facilitating the use of new energy vehicles. The real estate industry and its directly connected Jian’an decoration industry not only can absorb a lot of employment itself, the real estate industry also has a huge leading role in many important upstream and downstream industries. More importantly, the recovery of the real estate industry can lift local financial difficulties, thereby prompting the regional economy on the verge of shock to quickly return to normal operation.

Back to the original discussion, leaving real estate, not only is the new infrastructure difficult to save the economy, but the traditional infrastructure is also not good, they are not very good to smooth out short-term economic cycle fluctuation Policy tool. The infrastructure represented by “Tie Gongji” since 2008 seems to be effective as a tool for short-term economic cycles, only because people are reluctant to mention real estate as “behind the scenes”.

From this perspective, some proponents of new infrastructure may only use the new infrastructure as a means of financing real estate, and the opportunity to activate real estate is the ultimate goal.

However, to the destinationAt this stage, is real estate still a big deal? The answer is both negative and positive.

Nowadays, house prices are at historically high levels, residents are generally burdened with mortgages for decades, and those with multiple suites are not rare. High. The low level of the city brought about by the real estate bubble simply cloned outwards, which also greatly damaged the quality of the city.

Most people know clearly that our country can no longer afford a new round of real estate bubbles. Once again, real estate is stimulated, and once the price of houses rises and falls and the market collapses, the consequences will be disastrous. In recent years, the central government has repeatedly emphasized that “no housing, no speculation,” one of its main purposes is to avoid systemic economic risks caused by speculation.

Although China ’s real estate industry has a greater bubble risk, it also has greater development potential. This argument seems contradictory on the surface, but it is not.

Although China has always been troubled by the real estate bubble problem, the urbanization of China like this has not ended and real estate has been characterized by a large bubble, which is not in the development history of countries around the world. common. One of the very important reasons is the rigid constraint of the dual land development system on the development of the real estate industry. Urban land is taken exclusively by the local government, creating artificial scarcity. When people’s housing needs are far from being met, real estate bubbles have already accumulated.

Clothing, housing and transportation are the most basic needs of people. Improving living conditions is not only one of people ’s upward motivations, but also an important part of people ’s longing for a better life. China is still in the background of urbanization. In the future, there will be tens of millions of farmers who need to live in cities every year. . The overall housing quality of urban residents in China is not high. Non-complete housing, tube houses, etc. also occupy a large proportion of the stock, and the need for improved housing needs to be stimulated. Trying to meet these basic needs while suppressing bubbles can not only solve the real estate industry ’s development potential, but also partially resolve the current economic development dilemma.

Although due to the constraints of the land system, the traditional real estate development model has entered a dead end, and bubbles and real estate speculation will rebound faster as the industry recovers. However, if we can break the land monopoly, we can significantly increase housing investment and improve the living conditions of residents, and at the same time, we can suppress the reduction of the real estate bubble, and we can achieve more than one benefit. We need to develop a new real estate model, and the key to the new real estate model is the reform of the land system.

At present, we have taken the first step of reform. Article 63 of the newly amended Land Management Law, which came into effect on January 1, 2020, stipulates,” The overall plan for land use, Urban and rural planning is determined to be for industrial, commercial and other operational purposes, and collectively registered construction land that has been legally registered. The landowner can use it by units or individuals through transfers, leases, etc. “This is actually to break the monopoly on land supply, It has created certain legal conditions to promote the direct entry of operating collective construction land into the market.

Unfortunately, the scale of collective operating construction land planned for industrial and commercial operating purposes Very small, the main construction land in rural areas is homesteads. The practical application of this reform is extremely limited, and it is difficult to shake the traditional monopoly real estate development pattern.

If we can go further , To explore the direct transfer of non-operating collective construction land such as homesteads, a new real estate model will be born. We can let go of real estate development and improve residential housing The conditions can also inhibit the expansion of the real estate bubble, and can also solve the current economic difficulties and play the role of one stone with many birds.

Under the new real estate model, with the block Coordinating the system and opening up and supporting residents to purchase land and build their own houses under the premise of meeting the planning will further inspire residents ’enthusiasm for improving living conditions and promote diversification of the city ’s style. The pattern of urban singular expansion can also be further improved. It is a major development for urban architectural culture and art.

In short, new infrastructure and traditional infrastructure as an essential part of a long-term development strategy, still need to increase investment.

< div class = "contheight"> But in the short term, funds can easily flow into the real estate sector, forming a new round of real estate bubbles. Simply adopting a plugging strategy to strongly prevent funds from flowing into the real estate sector may result in less success. And left real estate , New infrastructure and traditional infrastructure can only exist as a long-term strategy, can not quickly pull the economy, solve the current real economic difficulties, this is a paradox.

The way out of the historical circle is to open a new real estate model through land reform and guide the rational flow of funds into the real estate field. While deconstructing the real estate bubble, the housing conditions of residents have been greatly improved, and short-term economic growth momentum The problem has also been solved.

(Author Zou Linhua, leader of the big data project team of the Institute of Finance and Economics of the Chinese Academy of Social Sciences, Chinese Academy of Social Sciences Competitiveness Simulation Laboratory Deputy Director, Founder of Weifang Index)