Discuss the structure and key considerations involved in employee option incentives involving the VIE structure.

Editor’s note: The authors of this article are Li Guanbao (Senior Partner) and Liu Jing (Partner) of Dacheng Law Firm. Original title “Incentive Structure and Key Points of Employee Option Incentives under VIE Framework”

Employee option incentives are an important way for companies, especially startups, to attract and maintain excellent talents. To a certain extent, they may also effectively reduce the company ’s cash expenditures. Employee option incentives under the VIE structure involve many specialities, including But it is not limited to architectural design, voting rights, fulfillment conditions, exercise arrangements, foreign exchange registration, etc.

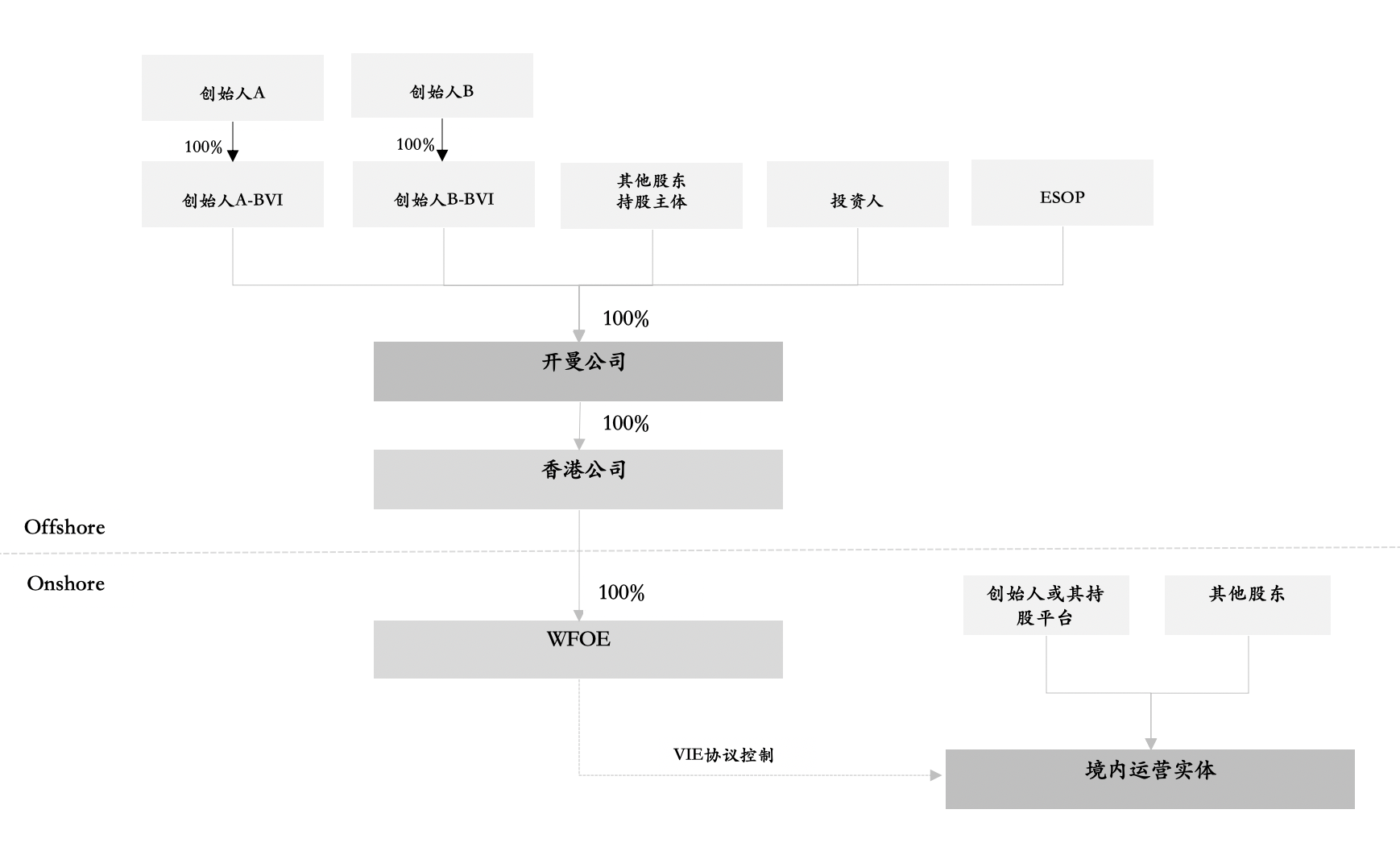

Typical VIE architecture

VIE (Variable Interest Entity, variable interest entity) structure exists in a large number of VC / PE dollar investment and financing transactions. The author summarizes several common considerations of adopting the VIE structure as:

Ÿ Businesses carried out by domestic operating entities (“VIE entities” or “OPCO”) fall within the category of foreign investment restrictions and / or prohibitions in accordance with Chinese laws; and / or

Ÿ The company hopes to obtain investment from foreign dollar investors more smoothly now or in the future; and / or

Ÿ The company hopes to list on the overseas capital market (usually US / Hong Kong) through the red chip structure.

Schematic diagram of typical VIE architecture

* The detailed discussion of the VIE architecture is not the focus of this article. The above typical VIE architecture diagram is used as a discussion of employee options Background reference for motivation related content.

The specific embodiment of the employee option incentive platform under the VIE structure

From the perspective of a startup company, it officially faces the need to set up an employee option incentive platform / employee option pool / employee option incentive plan (for convenience of expression, hereinafter referred to as “ESOP”), which usually occurs around the round A financing. In the early stages of company establishment, the founder may verbally promise to grant or grant some or all of the early employees a certain periodRights, and may also sign relevant grant documents that are not standardized or do not meet the requirements of investors;

When a startup company has passed a very early stage (seed round, angel round, etc.) and entered the Pre-A round or A round of financing, investors usually require the company to set up a certain percentage of employee option pools as a prerequisite for delivery (And a certain percentage must be maintained after the delivery), and within a certain period of time after the delivery (usually 6 months), a formal, in line with market practice employee option incentive plan (required by the board of directors and approved by the investor director) And if there has been an oral grant promise or signed some grant documents, it needs to be adjusted or perfected according to the formal employee option incentive plan.

Of course, the atypical enterprises that are supported by VC / PE and are already in the Pre-IPO stage may set up ESOP before listing. This situation is not within the scope of this article. The author will follow the proposed overseas listing How to deal with ESOP is discussed in a separate article.

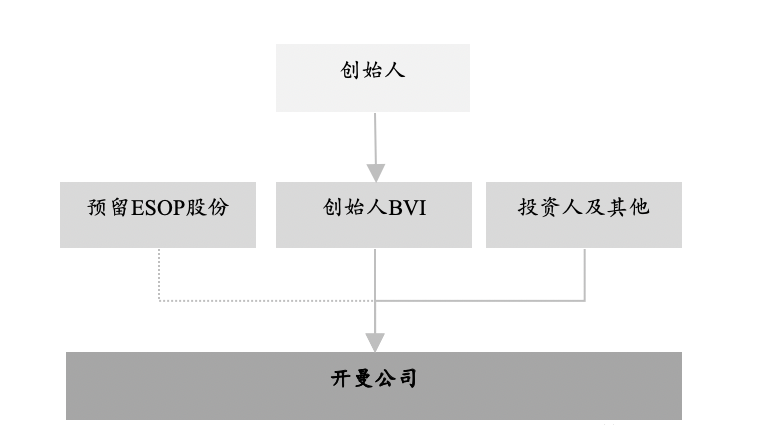

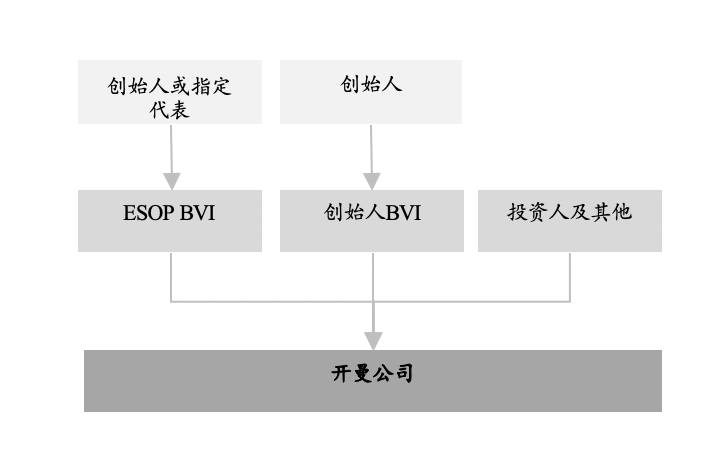

There are two main forms of ESOP under the VIE architecture:

A. Cayman reserved

The common shares reserved by the Cayman Company for a certain number of shares are used as ESOP (but not as shares issued (Issued and outstanding)), and will be awarded to the incentive objects in the future according to the employee option incentive plan; When the party ’s shareholding ratio is included, the proportion of ESOP is calculated accordingly, and the ratio of each party is diluted proportionally. Usually in the transaction documents, it is clearly stipulated that the investor ’s priority (such as priority subscription rights, anti-dilution rights, etc.) is less than the shares reserved for ESOP.

B. The ESOP shareholder holds it on behalf of

An ESOP shareholder is established by the founder alone (for example, a BVI company established by the founder in the British Virgin Islands (“BVI”), hereinafter referred to as “ESOP BVI”), which is first held in the name of the founder All of the BVI company’s issued shares are outside, and Cayman Company issues a certain percentage of shares to the ESOP BVI as an employee option pool.

It is worth noting that, if necessary, the Cayman company can adjust the total number of shares in the employee option pool by expanding the share or reducing the number of shares; if “BVI company is used as the ESOP shareholder, it will hold For the BVI company, the Cayman company will not increase the number of shares of the BVI company when it splits its shares. Of course, the BVI company itself can also split the shares to correspond to the Cayman company’s split.

BVI companies do not have the concept of “Authorized Share Capital”, and usually register with the number of authorized shares (50,000 shares) when registering. If you want to change the total number of treasury shares from 50,000 shares to 500,000 or 5 million or more The annual inspection fee also increases as the number of authorized shares increases. In addition, there are differences in voting rights, dividends, exercise rights, foreign exchange registration, etc. between the two methods.

From what angle does the founder consider the key terms of ESOP design?

commitment to employees before building a structure

Before formulating a formal employee option incentive plan, if the founder has made a commitment to the employee ’s work or signed an option grant document that relies on a domestic entity, it is necessary to fully communicate with the employee on how to convert the commitment made (including the cash cycle Rights price, number of shares and proportion, etc.).

In general, it is not recommended to promise a certain percentage to the incentive target, because the company ’s equity structure will continue to change with the adjustment of financing and capital structure, and the company ’s valuation will also continue to change. If you commit to the proportion, It may be that due to different understandings between the two parties, the founder cannot normally implement the “commitment”, so the best option to grant the target is clearly a certain number of shares or / registered capital. If it is indeed necessary to embody a certain proportion in the form of commitment, it should be clear that such proportion will be further adjusted and diluted as the company’s capital structure changes.

Voting rights

Under the domestic structure, if the employee option pool is set up in the form of a holding by the founder or another limited partnership, the founder usually has the right to vote for the ESOP. However, in the context of VIE structure, if the form of shares reserved by Cayman is used, these ESOP corresponding shares are not actually issued (Issued and outstanding) shares, and they do not correspond to the calculation of voting rights.Enjoy any voting rights. That is to say, when calculating the proportion of voting rights corresponding to the shares of each party, the reserved ESOP shares will be eliminated, so that the proportion of investors will be higher than the proportion set out in the Cap Table after settlement. The founder should anticipate this change in advance. For a small number of founders with a relatively low initial share ratio, it may be more advantageous to choose the above option B from the perspective of voting rights.

Proportion of Option Pool

Considering that the startup company will have multiple rounds of financing and multiple shares / shares diluted before listing, in the early stages such as the Angel round or the A round, 8% to 20% of the shares are generally reserved as employee option pools More common. From the perspective of the founder, if the proportion of the employee option pool is reserved before the closing of financing, it means that a higher proportion of the employee option pool will cause the company’s overall valuation to be lowered accordingly, so the ratio is not as high as possible, but If it is lower, it may affect the future incentive effect (that is, the options used for incentives may be exhausted soon), and it is necessary to maintain a moderate balance.

Option Cashing (Vest)

Similar to the shares held by the founders, employee options are also subject to redemption (Vest, Chinese or “release”, “belonging”, “mature”) terms. The cashing conditions are mainly considered from the perspective of other conditions such as time period or performance, and the time period is basically the standard configuration of the cashing clause.

(1) Time period considerations

Generally, 25% will be cashed out one year after the option grant date, thereafter 25% cashed every year, 1/36 cashed monthly or equal cashed quarterly, etc. It is common that the cashing is completed at a constant rate of four years. In addition, there may be some additional restrictions, for example, unpaid leave is not included in the cashing period and cannot exceed 30 days at most. If it is exceeded, it is regarded as the employee’s voluntary resignation. Combining the company’s business model and expansion speed, the founder can consider formulating different fulfillment schedules.

(2) Performance or other considerations

You can consider linking with the performance of the incentive object (different treatment of employees in different positions and categories), multiply the originally agreed redemption by the percentage of completed performance, and calculate the actual amount that can be redeemed. In the early stage, because the startup company’s model and performance evaluation method are not yet clear, there are few cases linked to performance; when the company’s financing round and / or business model and performance evaluation standards are clear in the middle and later stages (such as C round), Consider adding performance considerations.

Exercise Price

The incentive object needs to pay the consideration (“exercise price”), but there may be no consideration requirements (zero consideration), depending on the specific plan. Exercise prices are common in the following situations:

(1) Zero consideration

(2) Par Value (Par Value)

(3) Valuation or a certain percentage of valuation

* At a certain point (such as when the option is granted, the pre-option grant financing valuation, the previous round of financing before exercise, etc.), the company’s overall valuation or a certain discount ratio is the value corresponding to each share as the exercise price;

(4) Other reasonable fair prices

There are currently no mandatory or deterministic rules or practices on how exercise prices are set, and founders can consider exercise prices from several perspectives:

1. Cannot be too high. Excessively high exercise prices may cause employees to think that the expected return is low, which may affect the incentive effect;

2. Do n’t be too low, consider the problem of excessively high “share-based payment costs”, and it may also affect the incentive effect, because if you think that the drought and flood protection will be guaranteed from the perspective of employees, then you may not have enough motivation and company Work together to push up the valuation and stock price.

Regarding share-based payment costs, in other words, the company grants employees an option based on the labor or other services provided by the employee, promising that the employee can exercise at a price lower than the fair value at that time and obtain equity in the share as an incentive Employees serve the company better, so the company should pay for it, and the corresponding profit will decline.

From the perspective of share-based payment costs, the exercise price should not be set too low, otherwise it will bring greater pressure on the share-based payment costs to the company (especially the mature listed companies).

Exercise and Foreign Exchange Registration

Employee option incentives under the VIE framework are very special. Usually, the exercise of employees ’rights needs to be carried out after listing, which mainly hinders China ’s relevant foreign exchange management regulations and actual operations.

According to Article 6 of the “Notice Concerning Issues Concerning Foreign Exchange Administration of Overseas Investment and Financing and Return Investment of Domestic Residents Through Special Purpose Companies” (hereinafter referred to as “Circular 37”) issued by the State Administration of Foreign Exchange on July 4, 2014 According to the regulations of the non-listed special purpose company, the company ’s equity or options are the target, and the directors and supervisors of the domestic enterprise directly or indirectly controlled by the company and other employees with employment or labor relations are entitled to equity incentives. Before submitting materials, you can apply for foreign exchange registration procedures for special purpose companies.

First of all, the above Article 6 stipulates that the incentive object who accepts the option grant can “register” for option 37, and the understanding of this clause is “can be processed” rather than “must do”. However, based on practical experience, the foreign exchange department has reservations about this, mainly considering the issues involving cross-border payments, and it is actually not open for option 37 registration. In addition, it is not ruled out that there are some regions where the foreign exchange department considers it “should be handled” rather than “can be handled.” In this case, implement an option incentive plan and grantOptions granted to residents within China will likely fall into an indefinite loop that should be handled but cannot be handled and will be in a “non-compliant” state.

Secondly, if the employee exercises the option before listing, there will be a situation that “should be registered for Circular 37” and cannot be handled in practice, so it is usually before the listing, which hinders foreign exchange laws and practices Due to the restrictions, companies with VIE structure usually do not open the exercise of employee options. After the company is listed, the incentive object can exercise the right, and the foreign exchange registration is carried out in accordance with the “Notice on Issues Concerning Domestic Individuals Participating in Foreign Exchange Management of the Equity Incentive Plan of Overseas Listed Companies” (“Circular 7”) issued by the State Administration of Foreign Exchange in February 2012 .

About the author