Baidu’s short-term receipt of YY is a short-term capital story, long-term or AI

Editor’s note: This article is from the WeChat public account ” Science and Technology said “(ID: kejishuo) , author: old iron 007.

I believe that many people are just like us, right Baidu This acquisition was initially confusing: as Why does a company that continues to increase AI investment need to acquire YY Live at a price of 3.6 billion US dollars at this time? The discerning people know that the acquisition may bring about revenue growth, but is this in line with Baidu’s current core interests? Or at what point is Baidu now?

Since Baidu announced that it will acquire YY, the above questions have been entwining me. Combining Baidu’s historical data and current development rules, this article tries to answer the above questions.

As an Internet company that has been in business for more than 20 years, “mature” should be one of the most important labels given to Baidu by the capital market. In this cycle, companies need to have: huge cash flow support, stable revenue and profit growth, right The valuation method of such companies will also be biased from the P/S ratio model of the growth company to the P/E ratio.

In the past few years, Baidu has fallen behind Tencent and Alibaba in terms of total market value management. Recently, it has also been lost to Weilai, Pinduoduo, JD.com, and Shell is surpassed by the representative emerging companies. The reason for the above-mentioned capital market’s valuation of mature companies is not difficult to find, that is: as an Internet company with a dominant domestic search, after the rise of the mobile Internet, with Weibo, headlines and the rise of WeChat, Baidu has not copied the control of traffic in the PC era to the new era, and the status of online advertising has been continuously diluted In addition, after focusing on the AI strategy, it is more radical in terms of R&D expenditure. All this shows that if Baidu is viewed by the standards of a “mature” company, its market value is indeed unstable and lacks storytelling.

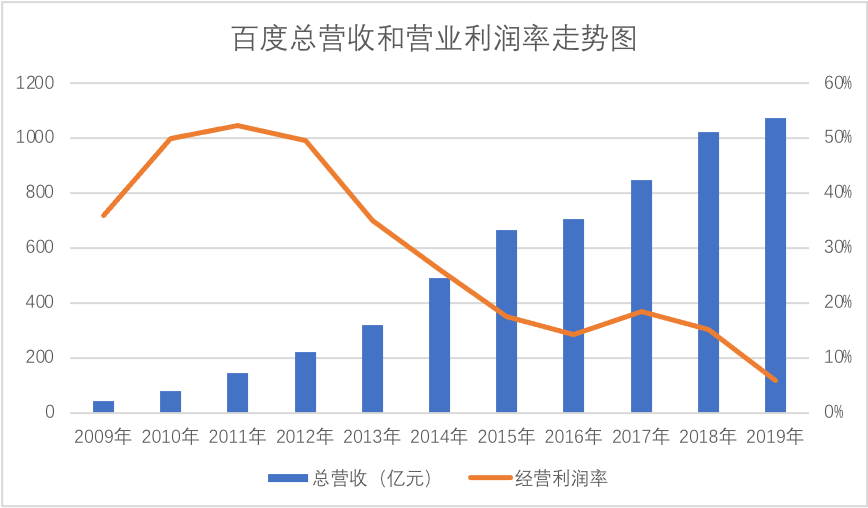

For an objective comparison, we take Baidu’s revenue and operating profit margin over the past ten years and draw the following chart.

Before 2013, both total revenue and operating profit margin were in the best cycle in history. It is not an exaggeration to say that this is Baidu’s best time, but as mentioned in our opening hypothesis, With the rise of the mobile Internet, the total revenue has become more and more sluggish. Especially in 2014-2016, when the O2O business represented by Baidu Waimai invested heavily in 2014-2016, Baidu almost used online marketing revenue to feed the loss-making food, which lowered the total operating profit margin. Of course, this also includes the early losses of innovative businesses.

After the sale of Baidu Waimai in 2017, the operating profit rate was immediately reflected. Since then, Baidu has become a big player and re-enter the online marketing market with the combination of “search + information flow”. In 2018, the total revenue has been faster Growth, but due to