Whether Shentong can get investment optimism, need to analyze from multiple angles

Editor’s note: This article comes from WeChat public number “IPO knows early” (ID: ipozaozhidao), author Uncle C.

According to the IPO, I knew the news. On the evening of July 31, Shentong Express announced that the company’s controlling shareholder, Shanghai Deyin Investment Holdings Co., Ltd. (hereinafter referred to as “De Yin Investment”), the actual controllers Chen Dejun and Chen Xiaoying, and Ali Baba (China) Network Technology Co., Ltd. (hereinafter referred to as “Alibaba”) signed the “Share Option Agreement”, the agreement stipulates that De Yin Investment intends to grant Alibaba or its designated third party to purchase Shanghai Deyin Derun Industrial Development Co., Ltd. (hereinafter referred to as ” De Yin De Run”) 51% of the shares, and Shanghai Gongzhi Run Industrial Development Co., Ltd. (hereinafter referred to as “Kongzhi Run”) 100% of the shares or Christine Run at that time holding the shares of the listed company 16.1% of the shares (“share options”).

With regard to the amount involved in the share options, the announcement states that the total exercise price of the share options is RMB 9.982 billion in the case of Alibaba or its designated third party exercising all share options.

On August 1st, after the opening of Shentong Express (002468), the stock price opened slightly and then quickly dipped. After the closure, the turnover was 610 million yuan, and the turnover rate was 6.75%. On Monday, it continued to fall 6.72%.

With the above announcement, Shentong Express, which belongs to Chen Dejun and Chen Xiaoying’s brothers and sisters, has come to a close. Since then, Alibaba has been fully controlled and Shentong has officially become part of the rookie alliance.

For Ali, since the investment of 4.66 billion yuan in March, the network of the rookie alliance has been completed. However, since Chen Xiaoying’s brother and sister intends to give way and spend 10 billion yuan, it is not a big deal for Ali. After all, after fully controlling Shentong, many of the imaginations of intelligent logistics have room for free display.

For Shentong, the change of owner is a rescue for this company. The glory of Shentong dates back to 2014, when it once occupied the first place in the industry. Subsequent market share and business volume began to decline. From 2016 to 2018, the stock price was only 14.21 yuan, and the market value evaporated more than 45 billion yuan in two years.

For the logistics industry, Shentong’s original technical level has lagged behind, which is the original intention of this company to rely on the resources of rookie.

Interestingly, the announcement of Ali Holdings Shentong, the latter’s share price actually fell. However, this is not worthy of surprise, nothing more than profitThe effect of the good effect effect, after all, in March this year, Ali invested 4.66 billion to become the second largest shareholder, Shentong’s stock price limit for two consecutive days. In the following period, Shentong’s share price has doubled, which is fully reflecting the performance of Ali’s investment in Shentong.

Between the two, can you get the effect of adding positive and positive, whether Shentong can get investment optimistic, need to analyze from multiple angles.

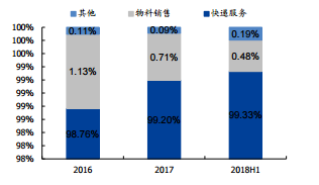

From a business perspective, Shentong’s main business is express delivery services, accounting for up to 99.33%. Since the company adopted the light asset model in the past few years, it has slowly fallen behind in the fierce market competition, but The company changed its previous strategy to increase capital expenditures. In May 2018, it bottomed out and the express business volume increased rapidly, which was 10% higher than the industry growth rate.

Shentong Express and the company’s business composition Source: Company Announcement

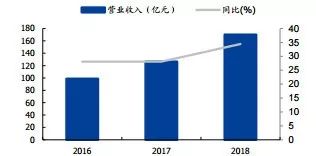

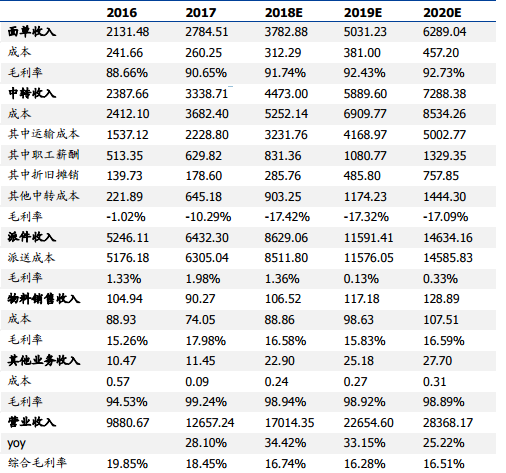

Shentong Express’s revenue has maintained rapid growth and its performance in terms of cost control is excellent. The company’s operating income is 2016-2018CAGR 31.22%, net profit at home is 2016-2018CAGR27.3%, operating income in 2018 is 17.014 billion yuan, up 34.42% year-on-year, net profit at home is 2.045 billion yuan, up 37.46% year-on-year. . Thanks to the stable management costs of the company, the sales expenses and financial expense ratios showed a downward trend, and the expense ratios were properly controlled, resulting in an increase in the net profit margin.

Shentong Express revenue and growth source: WIND

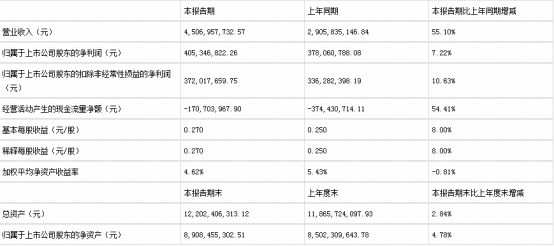

As of the financial report for the first quarter of 2019, the company’s revenue increased by 55.1% year-on-year, and the net profit of the mother returned by 7.22%.

Shentong Express 2019 First Quarter Financial Report Source: Company Announcement

After reading the company announcement, the determination of management change is firm. In 2018, 15 core city transshipment centers were completed, and the direct transfer rate reached 88%. On this basis, the company accelerated the progress of capacity production, and the original value of buildings and buildings increased by 89%. The market share also rebounded from the previous 9.3% to 10.7%, and the effect of marginal improvement was significant.

But the increase in share is a price to pay. Due to the overall price-sensitive nature of the e-commerce express industry, aggressive pricing strategies have led to Shentong’s short-term pressure.

If Alibaba exercises all the share options, it will indirectly hold 46% of the shares of Shentong Express. To achieve full control of the listed company, the overall acquisition cost price is about 20.80 yuan / share, lower than the current share price of 23.89 per share.

In recent years, Alibaba has continued to invest in logistics areas such as warehouse management and real-time distribution. The holding of Shentong will undoubtedly bring the synergy effect of Ali to the management and transportation network of the latter.

With this in mind, analysts believe that the 20/21 EPS dilution forecast should be appropriately raised, but the overall valuation of Shentong does not need to be adjusted significantly, and it is still within the reasonable stock price range.

E-commerce, led by Ali, JD.com and Jieduo, explored the new retail and drove the growth of the express delivery industry, and its market concentration was improved. The express delivery industry is divided into services, and e-commerce components are its main business. The growth rate of e-commerce components is linked to online retail sales.

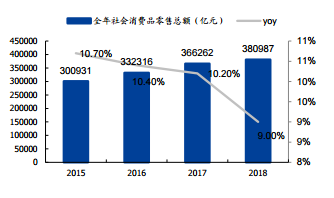

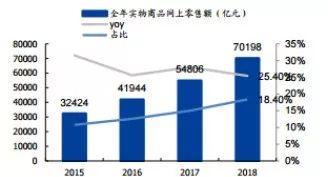

The total retail sales of consumer goods in the year of 2018 was 38.1 trillion yuan, a year-on-year increase of 9%. The online retail sales amounted to 7.02 trillion yuan, a year-on-year increase of 25.4%, accounting for 18.4%.

Annual Retail Total and Online Retail Total Source: WIND

Multiple e-commerce sinking markets have boosted the high growth of Internet users. Take a lot of examples. According to the trustdata data, the growth rate of mobile Internet users in third, fourth and fifth tier cities is much higher than that in first- and second-tier cities. The highest growth rate for fourth-tier cities is 61.1%. The proportion of four lines and below in the number of users is up to 38.4%, which is consistent with the level of Vipshop. With the high growth of Internet users in low-tier cities, the rapid growth of the market has been reflected in the increase in GMV. In 2018, it was 471.6 billion yuan, a year-on-year increase of 233.99%, and the number of orders was 11.1 billion, an increase of 158.14%.

The market concentration of the express delivery industry continues to increase

Data Source: Company Announcement WIND

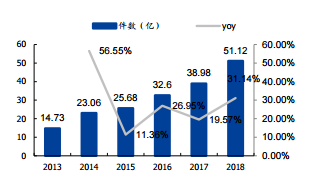

In 2018, the express delivery market share of the six major express delivery companies was 72.23%, which was an increase of 5.52% compared with the market share of 66.71% in 2017. The trend of the express service brand concentration index CR8 is rising, 2019 2 The month was 81.3, reflecting the further increase in the market share of the head express delivery companies, and the market share of small express delivery companies shrank rapidly. The first echelon express delivery companies have been listed in 2016, financing in the capital market, increasing capital expenditures, and further reducing the cost per piece.Improve service quality, enhance competitiveness and gain greater market share. In 2018, Shentong Express’s market share was 10.08%, and the number of express shipments for the year was 5.112 billion votes. Compared with 2017, it is in the first echelon of the industry.

From a proactive perspective, Shentong’s strategy is to increase capital expenditures and reduce transportation and transit costs.

Data Source: Company Announcement

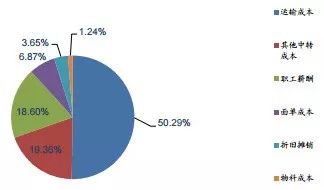

According to the 2018 data in the company’s announcement, transportation costs accounted for 50.29% of the cost structure, employee compensation accounted for 18.6%, and other transit costs accounted for 19.36%. After analysis, after eliminating the delivery cost, there is more room for the reduction of transportation costs and transit costs, which is the main direction for Shentong to reduce costs in order to achieve refinement.

Source: Shentong 2019 First Quarter Earnings

Increase capital expenditures into the transshipment center. In contrast to Shentong’s adoption of the light asset model in the past few years, since 2018, the company has changed its previous strategy to increase capital expenditures and to focus on asset lines. Data from the first quarter of 2019 showed that the investment reached 378 million, an increase of 132.93%.

However, the construction of the transshipment center is long-term. For short-term pressure, Shentong’s report shows that the pressure is released mainly by reducing the cost of transportation. The company gradually replaced the car (9.6 meters) with a big car (13.5 meters). Analyst estimates, assuming a loading rate of 70%, a transport distance of 1,300 kilometers, the driver’s wages are the same, a single piece of goods weighs 1.5 kilograms, regardless of depreciation costs, can be found a car single piece cost of 0.62 yuan, the cost of a single car 0.27 yuan, can achieve an effective reduction of 56.45%.

FromFrom the perspective of service quality, Consumers’ main complaints about Tongda’s express delivery are concentrated in delivery services, mail delays, and mail loss, which accounted for 33.3%, 26.7%, and 22.7% of the complaints, respectively.

The analyst believes that in addition to cost factors, service quality is a key competency. According to data released by the State Post Bureau, Shentong’s effective appeal rate dropped from 5.51 in January 2018 to 0.13 in December, ranking first among major express delivery companies.

Profit Forecast and Valuation Analysis

With the A-share company’s backdoor listing to open the first day of continuous daily limit, the market value of Shentong Express is 72.5 billion, which is ahead of the first day of Yuantong’s listing of 56.1 billion and Yunda’s 40.5 billion; but in October 16th, Zhongtong was listed, namely Tongda Department. On the whole listing day, the market value of Shentong has dropped to 53.4 billion, which is 55.1 billion behind Yunda, which is 9.3 billion behind Yuantong and 84.3 billion from Zhongtong. Since then, it has been lower than Yuantong and rhyme. As of February 22, the market value of Shentong 34.5 billion yuan, Yuantong 36.7 billion, rhyme reached 58.3 billion yuan.

In terms of PE(TTM), the valuation of Shentong fell from 35 times in the 17 years to the lowest 12.6 times in December 18, and Yuantong dropped from 35 times to 17 times in December, and rhyme started from 30 times. The high point has reached 40 times in 18 years, and the lowest has dropped to 20 times at the end of 18 years.

On average, rhyme is estimated at 30 times, Yuantong is 27 times, and Shentong is only 19 times.

If the changes discussed in the above section are successful, Shentong can successfully repair its valuation. Based on this prediction:

Source: Wind is forecasted by Aspirin

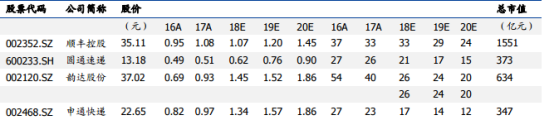

The comparable express delivery companies in A shares are SF Holdings, Yuantong Express, and Yunda. The average valuation of the above companies is 24 times in 2019. Analysts believe that the fundamentals of Shentong Express are improved and management efficiency is improved. Under the premise of the rapid development of the sinking market, a conservative 20-fold PE valuation can be assumed.

Used in the calculation Earnings forecast comes from WIND consensus expected source: WIND

The main risks take into account the possible failure of Alibaba’s shareholding, or improper integration; and the growth of major e-commerce customers is less than expected, which will affect the decline of the company’s business; it does not rule out that Shentong will not be able to resist market competition and slow down the growth. The share has fallen.