Land market have risen overall heat

Editor’s note: This article is from the micro-channel public number “Dingzu Yu assessment of the property market” (ID: dzypls), Author: Dingzu Yu.

“

Affected by the epidemic and the three red lines, the land market has been ups and downs this year. Land transactions fell to a trough at the beginning of the year. Since the second quarter, most cities have increased the supply of high-quality land to stabilize the economy and financial stability. The total land supply has steadily increased, and it has cooled again at the end of the third quarter.

As the end of the year is approaching, the supply and demand of the land market in 2020 is coming to an end. As of December 22, data shows that this year’s land supply is basically the same as last year, and the transaction scale has exceeded that of last year. At the same time, 16 cities have land transfer fees of more than 100 billion yuan, and the overall market fever has risen compared with 2019. With the convening of the Central Economic Work Conference, the structure of land supply may undergo major changes in the future. The scale of land transactions under the “three stability” target will continue to be high, and land prices are expected to remain stable under tight financing.

It is worth mentioning that the current hot land market in many cities means that real estate companies are generally optimistic about the city’s market development in the short term, but such cities also have the risk of high land prices leading to higher housing prices. ; In the short-term development prospects of cities are not promising, land transactions are relatively poor, and market pressure will also be greater. In fact, the investment intensity also represents the developer’s professional judgment on the city’s property market, which in turn is an indicator that can be used as a reference for home buyers.

“

01

The annual land transaction scale will exceed that of 2019

In the third quarter of 2020, affected by the pace of land supply in various cities, the transaction volume of the land market dropped significantly compared with the second quarter. Superimposed on the impact of the policies of “housing and housing, no speculation” and the “three red lines”, the land transaction market has cooled, but all The land supply side remained the same as last year. According to CRIC monitoring data, as of December 22, there were about 160 thousand hectares of land listed in 300 cities across the country and a construction area of about 3.53 billion square meters.

From the perspective of transactions, CRIC data shows that the land transaction area of 300 cities across the country is about 121,000 hectares, an increase of 5% compared to the same period last year; the transaction building area is about 2.64 billion square meters, an increase compared to the same period last year 4%. Judging from the land supply in November, it is expected that the total land market in 2020 will exceed the level of 2019, and the annual transaction volume will increase more than 4% year-on-year.

Picture: 300 cities nationwide in 2019 and 2020

Comparison of land supply and demand (100 million square meters)

Note: The statistical time period for 2019 and 2020 are both from January 1st to December 22nd, the same below.

Data source: CRIC collation

02Differentiation of land supply, Guangzhou-Shenzhen supply “exceeds the standard”

The completion of land supply in each city is basically the same, basically showing a differentiation pattern of “exceeding standards” in the central and western cities, and insufficient land supply in the downward cities of the property market.

In terms of specific cities, the ratio of land listings to planned land supply (hereinafter referred to as “listing completion”) in central and western cities such as Taiyuan, Wuhan, and Lanzhou all exceeded 140%, and the supply scale was obviously “exceeded.” Among them, Taiyuan is the most typical, with the listing volume of residential land reaching 684 hectares, while the planned supply of residential land in the city in 2020 is only 304 hectares, and the listing completion rate is as high as 225%. The reason is that this year, Taiyuan City’s old reforms continued to make efforts, and 257 hectares of homes were listed in the Xiaodian District alone, an increase of 160% compared to 2019. Similarly, in order to stimulate economic vitality, Wuhan has also increased its land supply, with a listing completion rate of 161%.

In the first-tier cities, Shenzhen and Guangzhou have completed 152% and 133% of listings respectively, and the supply side continues to exert strength. The reason is that the two cities are affected by national policies.

On the 40th anniversary of the construction of the Shenzhen Special Economic Zone in 2020, the central government supports Shenzhen to build a “first demonstration zone”, and its construction land approval has been further expanded, the pace of land supply has been significantly accelerated, and the amount of land has increased significantly.

Under the favorable planning and implementation of the Guangdong-Hong Kong-Macao Greater Bay Area, the land market in Guangzhou is very hot, especially Nansha District has become a hot spot for real estate companies to chase after. Many parcels of land have reached the highest price limit and entered the lottery link. Record-breaking, the price is close to “20,000+”. On November 30, Kaisa acquired a land parcel in Nansha Bay with a maximum land price of 2.018 billion yuan and an additional construction of 12,150 square meters, which was equivalent to a floor price of 22,700 yuan per square meter, setting the highest land price record in Nansha again.

Picture: From the perspective of land supply and transaction

Completion of land supply plan in typical first- and second-tier cities

Note: Affected by the listing time of the land, the listed plots in 2020 have not yet been completed.

Data source: CRIC collation

Jinan, Zhengzhou and other property markets are under great downward pressure. Under the influence of this, the completion of urban land listings is relatively low, all below 70%. According to the “Sales Price Index of Newly Built Commercial Residential Buildings in 70 Large and Medium-sized Cities in November 2020” released by the National Bureau of Statistics, the prices of commercial residential buildings in the two cities showed a downward trend year-on-year in November, especially in Jinan. By 1.7%.

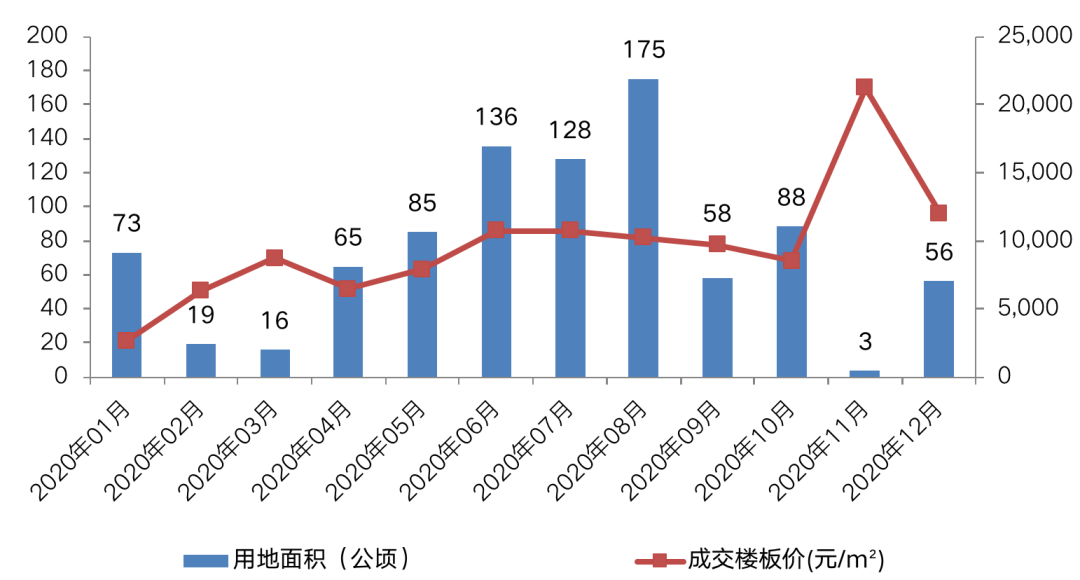

Ningbo, Hefei, Nanjing, Dalian and other cities have not completed their listings well, all below 90%. Mainly due to the control of market enthusiasm, such as Ningbo, due to the unusually high commercial housing and land market in the second and third quarters, repeated adjustments and interviews, the real estate market has entered a policy sensitive period, and the number of land listings in the fourth quarter has been significantly reduced. As of December 22 In the fourth quarter of Ningbo, the number of residential land listings was less than one million cubic meters, which was less than 30% of the second and third quarters. Therefore, Ningbo, which has a higher market popularity, has a relatively low level of completion of residential land listings and transactions this year.

Picture: Ningbo Shezhai Land in 2020

Monthly changes in volume and price

Note: The data for December is as of December 22.

Data source: CRIC collation

03The heat of the land has increased,Some cities have become “severely hit areas”

From the perspective of the supply-demand ratio indicator reflecting the heat of the land market, the supply-demand ratio of land in 300 cities across the country in 2020 is 1.34, which is a decrease of 0.05 from 2019. The overall land flow in 2020 is better than in 2019. This data is consistent with the unsold rate of key cities monitored by CRIC. The land unsold rate in 2020 is 10.7%, a drop of nearly 3 percentage points from 2019. In general, the land market has become more popular than 2019.

In terms of different cities, 30% of the 24 key first- and second-tier cities have a supply-demand ratio exceeding 1.3. Among them, cities such as Taiyuan, Jinan, and Hefei have outstanding performance, with the supply-demand ratio exceeding 1.35, and the proportion of land unsold is relatively large. high.The key cities monitored by CRIC’s data of unsold auctions (by number of frames) show that the three cities are all TOP10 cities with unsold rates, and the unsold rate exceeds 12%, all of which are “severely hit areas” for unsold auctions. Even for land transactions, the premium rate is relatively low. Take Jinan, which has a poor performance in the commercial housing market this year, as an example. The premium rate of residential land is only 4%. Many land transactions are sold at the reserve price and the land market is very depressed.

Picture: Typical first- and second-tier cities in 2020

Supply and demand area ratio of Shezhai plots

Data source: CRIC collation

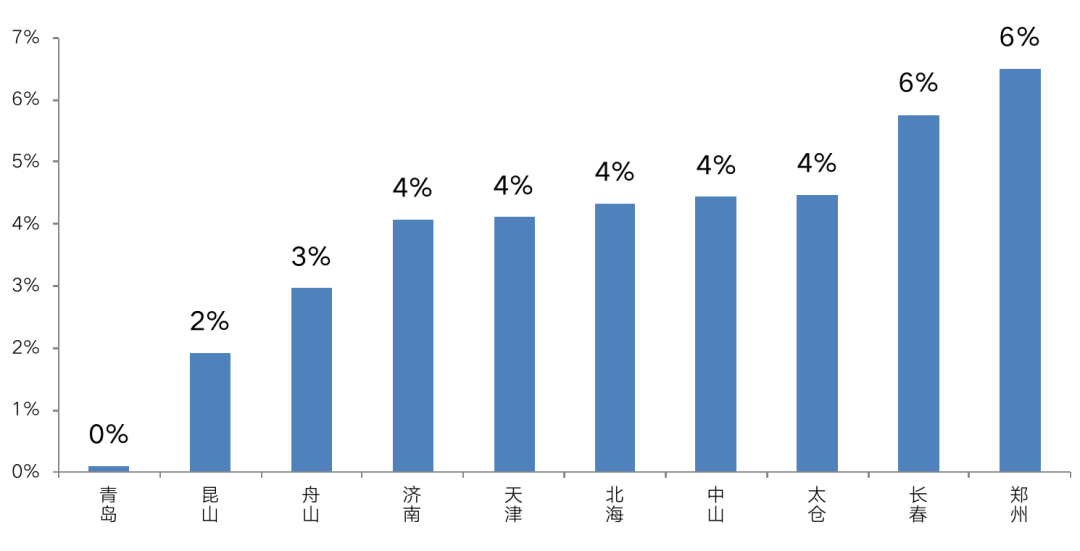

In contrast, Hangzhou, Ningbo, Nanchang and other cities with relatively balanced supply and demand (the ratio of supply and demand is 1.1 and below) have a relatively low rate of unsold auctions and a relatively high premium rate. A typical example is Hangzhou. In 2020, the unsold rate of residential land (by number of lots) is only 2%, but the premium rate is as high as 21%. The land market is significantly hotter than cities with high supply and demand.

Picture: TOP10 cities with pass rate

Data source: CRIC collation

Picture: TOP10 cities with the lowest premium rate

Data source: CRIC collation

The overall pace of land supply in each city shows a pattern of “policies in accordance with the city”. With favorable policies, the supply of land in Shenzhen and Guangzhou has increased significantly, and the supply in cities such as Taiyuan and Lanzhou, where the demand for old reforms is greater, has also increased significantly; commercial housing inventory pressure is greater Big cities such as Jinan and Zhengzhou are obviousThe land supply has been reduced, and the actual transaction of housing land accounts for only half of the annual housing land supply plan.

The Central Economic Work Conference set the tone. Next year, the macro policy should maintain continuity, stability, and sustainability, and continue to adhere to the main tone of the policy of “housing, housing, no speculation”. Against the background of the expected regulation of the “three stability”, land supply will remain moderately abundant, and it is expected that the scale of land transactions in 2021 will continue to be high.

It is worth noting that this year’s Central Economic Conference listed “solving the outstanding housing problems in big cities” as one of the eight key tasks to be grasped next year. For these first-tier and second-tier cities, next year, land supply will be tilted towards the construction of rental housing under the premise of “policy by city” and reasonable abundance next year, especially for larger populations, higher housing prices, and comparison of housing contradictions. In the prominent first-tier cities of Beijing, Shanghai and Shenzhen, the supply of affordable housing will increase significantly.

From a corporate point of view, the “three red lines” are overwhelming, and the financing environment for real estate companies will be tight for a long time. Under the background of “money tight”, real estate companies will be more cautious in acquiring land, and land supply will continue to be high next year. , Land heat is difficult to rise again, and the maintenance of land prices is also a high probability event.