Try to use the “contrast quantification” method to outline the basic face of Huawei’s fast-growing technology elephant, and then deduct how it will be if it is listed.

Editor’s note: This article is from WeChat public account “Alpha Workshop” (ID: alpworks), the author is my.

In the past half a year, Huawei has almost become a topic of the whole nation. As a non-listed company, Huawei is even more attractive than the entire A-share listed company.

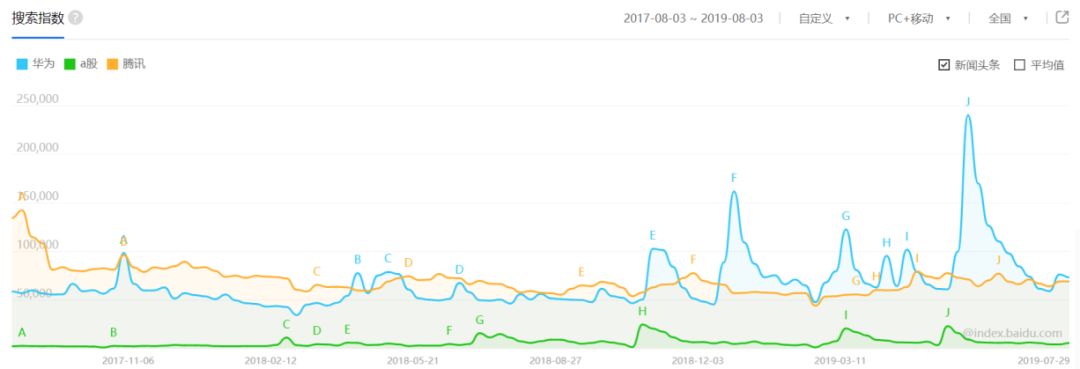

Taking the Baidu Index from August 2017 to August 2019 as an example: Before November 2018, Huawei basically had the same level of attention as another Internet giant in Tencent (HK:00700) in Shenzhen;

But since December 2018, Huawei’s attention has increased rapidly, and the topic heat often forms a very high peak. Figure 1: Huawei’s attention has increased rapidly in the past six months

Source: Baidu

For Huawei, everyone is familiar with it, but after careful calculation, it feels very strange – “entity list”, “Hong Meng”, “Huawei Haisi”, “mate series”, “5G base station”… …these words that are overwhelming, each of which corresponds to a huge amount of information.

Huawei has a large volume and involves a wide range of businesses. At the same time, because it is a high-tech enterprise and has a frontier field of layout, it often makes people deeply think that it is “the monk of Zhang Er can’t figure it out.”

I want to use an article to make Huawei clearly clear that it is a fantasy. The author tries to use the “contrast quantitative” approach to try to outline the basic face of Huawei’s fast-growing technology elephant, and then deduct if it will be listed. What kind of volume will it be.

01.Horizontal contrast, clarify history

Look at Huawei horizontally and use it as a single individual to understand the history of its growth.

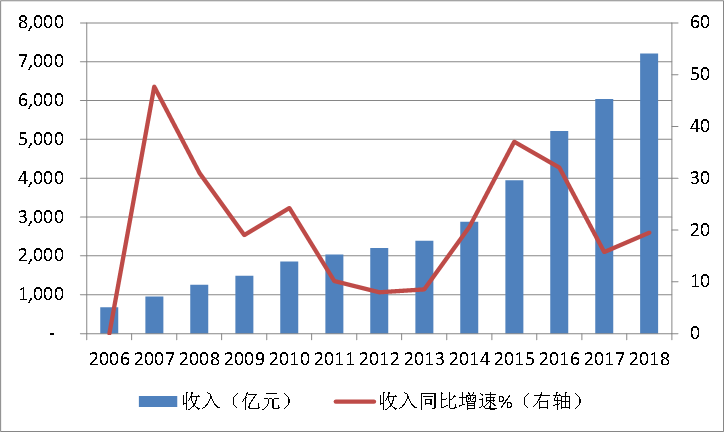

[1] Income growth: The compound growth rate in the past 13 years is 22%.

On the afternoon of July 30, Huawei issuedThe 2019 semi-annual report was published: the revenue was 401.3 billion yuan, a year-on-year increase of 23.2%, which was very eye-catching. In fact, since 2006, Huawei has continued to grow at a compound annual growth rate of 22% from 2018, and has grown into a giant one step at a time.

Figure 2: Huawei’s revenues maintain a stable growth trend

Source: Huawei Annual Report

After refining the income structure: According to the 2018 financial report, Huawei’s consumer business accounted for 48% (the first time that the carrier business became the company’s largest revenue source), after the largest carrier business decreased by 41%. These two businesses have become the main source of revenue for Huawei.

In addition, Huawei’s key business development in recent years has also accounted for 10% of revenue in 2018.

-

Huawei’s business is a communication device. Currently, Huawei, Ericsson, Nokia, and ZTE are in the global communications main equipment market. In 2018, Huawei’s global market share reached 30%, and it has maintained the number one position in the world for four consecutive years. Market position.

-

Huawei’s follow-on consumer business products cover mobile phones, PCs and tablets, wearables, mobile broadband terminals, home terminals and consumer clouds. In 2018, Huawei shipped 208 million smartphones, with a global share of 14.7%, while Samsung and Apple shipped 314 million and 225 million units respectively.

-

Huawei is the world’s third-largest smartphone manufacturer. With more than 30 years of deep integration in the communications industry and global network and operational advantages, Huawei’s consumer business has grown rapidly in recent years, 2018 The realized income was 348.9 billion yuan, accounting for 48.4% of the company’s total revenue.

Summary in one sentence: Huawei gradually expanded its enterprise-level consumer terminal business from its initial equipment provider business, and achieved rapid growth in the company’s revenue scale.

Figure 3: Huawei’s three major business components

Source: Huawei Annual Report

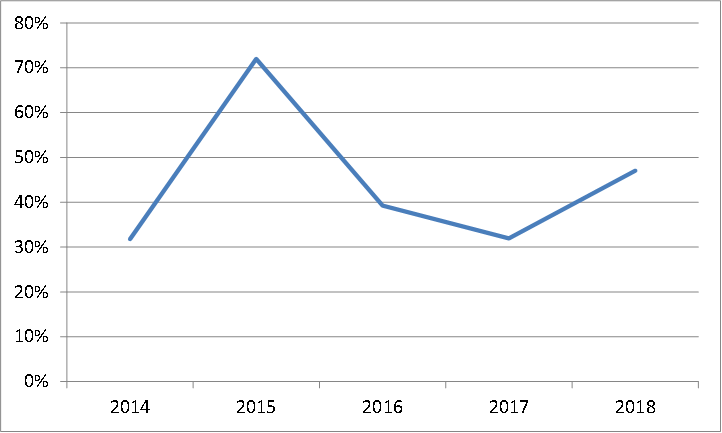

The most worth mentioning is Huawei’s consumer business.

In 2009,Consumer business accounted for only 16.5% of Huawei’s revenue; in recent years, especially in 2017 and 2018, in the case of the mobile phone industry competing in the Red Sea, Huawei’s consumer business revenue growth has remained at a high level of more than 30%. Complete the contrarian expansion.

In fact, Huawei Mobile Terminal Company was established as early as 2003. As the predecessor of the later consumer business group (BG), the development story of Huawei mobile phone is also very legendary.

If you look back at the elements of its success, it is mainly because Huawei insists on independent research and development of processor chips, and has completed catching up with the intergenerational difference through ten years. Huawei’s mobile phone camera is the world’s leading camera, based on chip and camera functions. Huawei’s P series and Mate series have achieved great success and become the first mobile phone factory in China to break through to mid- to high-end models.

According to Huawei’s latest semi-annual report, in the first half of 2019, the consumer business realized revenue of 220.8 billion yuan, and once again successfully became the sector with the largest revenue contribution, and the proportion exceeded 55% for the first time.

In the first half of 2019, Huawei’s smartphones (including glory) shipped 118 million units, a year-on-year increase of 24%, and officially surpassed Apple, ranking second in the world. Even Huawei is likely to complete its surpassing of Samsung in terms of shipments in 2019 and become the world’s number one.

Figure 4: Consumer business revenue continues to grow at a high rate

Source: Huawei annual report, click to see the big picture.

[2] Globalization Genes: The proportion of overseas income is always high.

Different from the development path of the general company, the first is to become a large local, and then to expand internationally; Huawei has a globalized gene since its birth, and its overseas income has been relatively high.

In 2009-2016, the company’s overseas revenues accounted for more than 50%; only in 2017-2018, due to the popularity of Huawei’s mobile phones in China, domestic revenues in the past two years exceeded overseas revenues.

Figure 5: Huawei has the strength and gene of globalization

Source: Huawei Annual Report

[3] Profitability: The accumulated net profit for the past 13 years was 314.9 billion yuan.

In terms of profitability, Huawei is also very worthy of the audience.

Source: Huawei Annual Report, Guosen Securities

02. Vertical contrast, the ceiling is far away

Another way to quantify Huawei is to reflect Huawei’s position by comparing with other technology companies at home and abroad.

In this regard, the author has chosen three perspectives:

(1) Comparison between Huawei and A-share overall communication and electronic listed companies;

(2) Huawei and domestic Internet giant AT (Ali and Tencent) comparison;

(3) Contrast with US technology giants Apple and Amazon (NASDAQ: AMZN).

[1]Compared with the A-share electronic communication industry: Huawei’s profit is equal to 2/3 of the A-share electronic communication industry.

The reason why the A-share electronic communication industry was chosen is because Huawei’s largest revenue comes from these two industries.

Huawei’s revenue accounts for only 30% of the 345 listed companies in the communications electronics industry, but its profit share is 77%. What is particularly impressive is that Huawei is slightly higher than the combined R&D investment of these 345 companies.

Another data, Huawei’s overseas income is also much higher than these companies.

In this way, the current valuation of the A-share communications industry more than 160 times, the electronic 47-fold valuation is clearly overestimated. Of course, due to the existence of a loss-making company, it will obviously raise PE (price-earnings ratio). In view of this, the author removed the loss-making enterprises in the communications and electronics industries, and obtained static PE at the end of 2018 for the communications industry 36 times and the electronics industry 31 times.

Figure 9: Huawei vs. A-share listed companies (2018 data)

Source: Huawei Annual Report, Wind, click to enlarge.

[2]Compared with global technology giants:

Huawei is far from the ceiling.

(1)Compared with domestic Tencent and Alibaba (NYSE:BABA).

The domestic public opinion has changed the “BAT” to “HAT” for a long time. The author also chose AT for comparison:

In terms of revenue, Huawei is basically the same as AT, but since Huawei is a manufacturing company after all, its profitability is far away, and the R&D expense ratio close to 14% also reduces the net profit margin. Therefore, Huawei’s net profit Both are lower than AT.

Another point worth noting is that Tencent’s overseas revenue is only 3%, and Alibaba is slightly better, accounting for 20%. They are far lower than Huawei and lower than Amazon and Apple. That is to say, Tencent and Alibaba are still mainly making domestic money at this stage.

(2) Contrast with Apple and Amazon.

If compared with the US technology giant Amazon and Apple, Huawei’s current volume is still not large.

In terms of revenue, Huawei is only less than half of Amazon’s revenue. It also likes Amazon, which has a large amount of research and development. The net profit is only 66.7 billion yuan, which is consistent with Huawei’s size. Although Amazon’s profits have not yet been released, the US market has clearly given a lot of tolerance. In 2018, the static PE multiples exceeded 70 times.

As one of Huawei’s largest competitors in its consumer business, Apple’s revenue is 2.4 times that of Huawei and its profit is 6.6 times that of Huawei. Such a big gap also shows that there is still a distance from Huawei’s ceiling.

Figure 10: Huawei and the entire technology giants

Source: Company Annual Report

03. If listed, Huawei’s market value geometry?

Although Ren Zhengfei, Huawei is not clear that the lack of money, there is no listing of the program, and now Huawei’s unique ownership structure can not be listed. but it does not prevent us “on paper” Huawei If listed, how much can be achieved under market value to deduce?

first estimate of 2019 earnings at Huawei, Huawei simple assumption that 2019 full-year revenue growth of 20%, net profit rate remained 8.7% in the first half of 2019, the corresponding profit of about 75 billion yuan.

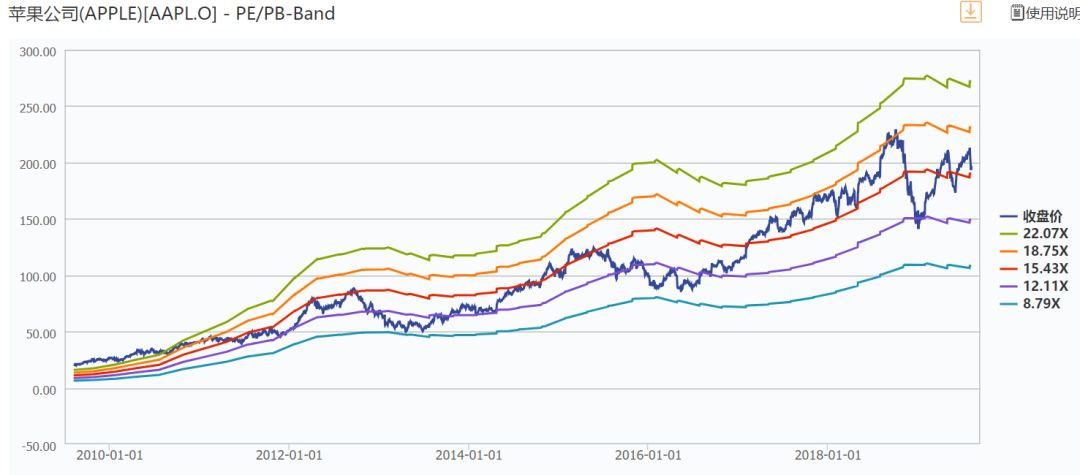

I believe that Apple’s valuation, as Huawei valuation limit. This is so set, due to the highest degree of overlap both the business and the growth of Huawei better, and non-consumer business can give a higher valuation.

For a period of time, Apple’s median price-earnings ratio is basically more than 15 times, which means that Huawei’s valuation lower limit can be set to 15 times.

Figure 11: Apple valuation

The vertical axis is the stock price

Source: Wind

Look at the valuation ceiling: If you refer to the median valuation of the entire A-share electronics and communications sector, the theoretical upper limit can be 35 times; if you refer to the current median valuation of the board, as of On August 8, 2019, the theoretical upper limit can be given 100 times (see the figure below).

Figure 12: List of stocks in the stock market (as of August 8, 2019)

Source: Chioce Financial Terminal

In other words, if US stocks, Hong Kong stocks, and A-share mains are listed, according to Huawei’s 2019 net profit of 75 billion yuan and PE multiples of 15-35 times, the corresponding market value should be 1.125 trillion yuan – 2.6 trillion. In the yuan interval, the central market value is about 1.86 trillion yuan.

If Huawei landed on the board, the current price-to-earnings ratio of China’s Tonghao (SH:688009) is 28 times, and the price-to-earnings ratio of the median of all 27 companies is 100 times. According to Huawei’s 2019 net profit of 750. In terms of billions of dollars, the corresponding market value should be between 2.1 trillion and 7.5 trillion, and the central market value is about 4.8 trillion.

Of course, it must be pointed out that although the science and technology board is the current “most awkward” in the A-share market, it is full of imagination for Huawei to land on the board. But this proposition is actually not very meaningful at present:

One Huawei is too large, and the water level of the science and technology board that has just opened the door is limited. At present, “the small temple is difficult to accommodate the big Buddha”;

The second section of the board has been open for more than 3 weeks and has been in a state of speculation. As of the latest trading day (August 8th), the China No. with the lowest P/E ratio (28 times), its Hong Kong stocks (HK: 03969) The price-earnings ratio is only 13 times; while the semiconductor industry chain company Micro-Company (SH:688012), the price-earnings ratio has reached 458 times – it can be seen that the valuation bubble is still very impressive.

Three because of the well-known reasons, Huawei’s business development in the future is uncertain.Qualitative.

But in any case, looking at the aforementioned market value range – whether it is 1.125 trillion yuan – 2.6 trillion yuan, or 2.1 trillion – 7.5 trillion, is enough to make Huawei the largest market capitalization company in China. Therefore, “HAT” can be described as deserved.