Judging from the amount of financing, coffee ultimately lost out on tea.

Editor’s note: micro-channel public number “One look at the business’ from this article (ID: yilanshangye), Author: Xue, Editor: One view king.

The development of tea and coffee in the beverage industry can be regarded as a pair of enemies. In the past three years, with the rapid rise of new-style tea drinks in the country, coffee has not given way. With the blessing of capital, the country is staking a race.

2020 is a year of growth and change for the enemy. After a short pause at the beginning of the year, tea and coffee quickly recovered through different means and ushered in growth.

In 2020, various new coffee brands will emerge in coffee, and a series of foreign coffee brands such as Tims and Y’s will be launched in China. In terms of tea, Michelle Ice City will open thousands of stores, and the local brand Cha Yan Yue Se will begin. With a national layout, Nayuki’s tea and hi tea are preparing to hit the first share of tea.

According to Tmall data, from November 1-3, 2020, the coffee category increased by 1900% year-on-year. Similarly, the “2020 New Tea Drinks White Paper” released by CBNData shows that online orders for new tea drinks from Ele.me in August 2020 are five times that of February 2020, and the number of stores has also shown a significant growth trend. The beverage industry ushered in “compensatory consumption.”

Behind the vigorous development of tea and coffee, it is inseparable from the continuous attention of capital. According to the incomplete statistics of “One View Business”, in 2020, there will be 22 financing incidents in the coffee and new-style tea circuit, and the total amount of disclosed funds exceeds 2 billion yuan. Among them, the amount of financing for tea drinks exceeded RMB 1.2 billion. In terms of the amount of financing, coffee ultimately lost out on tea.

One View Business believes that after nearly three years of rapid development, the new tea and coffee industry is ushering in new changes.

Coffee is still growing, tea will welcome the market trend

Although coffee is booming, from the current point of view, Chinese coffee brands are mostly in the start-up growth period. Among the 11 financings in the coffee industry in 2020 calculated by “One View Business” are in the seed round, angel round, and A round of coffeeBrands accounted for six, and the financing amount was mostly tens of millions.

In terms of turnover, except for three and a half meals and even coffee, most of them are relatively small. For example, Yongpu Coffee’s sales in 2019 are 26 million yuan, and the goal for 2020 is 100 million yuan; Shicui was established in 2019, and the monthly sales in 2020 are only in the order of one million, and the annual sales only hover around 100 million. .

Of course, although coffee brands are small in size, they are all in a period of rapid development. For example, Yongpu Coffee, sales on Double 11 in 2020 will be 10 times that of the same period last year. Fan Ruoyu, the founder of another brand of Shicui Coffee, revealed that the quarterly repurchase rate of Shicui Coffee’s Tmall store remained at about 25%, while the original applet renewal rate remained above 50%.

Compared with the start-up and growth period of coffee brands, after several years of rapid development, the pattern of new tea brands has basically taken shape.

On the one hand, the top brands of Hey Tea, Naixue’s Tea, Michelle Ice City, and Chali in tea are still the sweet pastries in the eyes of capital. Naxue’s tea completed two rounds of financing in June and December, B and C, with a total amount of up to 200 million US dollars; Chali, the leading brand of tea bags, also completed a round of B round of financing of 100 million yuan.

On the one hand, capital has also begun to target mid-waist brands. Waist brands such as Shanghai Auntie, 7 Fen Tian, Gu Ming Tea Drink and other waist brands have all received financing in 2020.

With the formation of the brand structure, the top players of the new tea brands have also reached the harvest period. Most investors told “One View Business” that the new tea industry will usher in a wave of listings in 2021.

In fact, there were reports in September 2020 that Heytea plans to go public in Hong Kong before the end of 2021, and it is expected to raise US$400 million to US$500 million. On the other hand, Naixue’s tea valuation, which has undergone 5 rounds of financing, will be close to US$2 billion, or approximately RMB 13 billion, and the time to go public is basically ripe. Another net red tea drink Michelle Ice City reported that it raised 2 billion yuan in early 2021, with a post-investment valuation of more than 20 billion yuan, and it is preparing to list on A shares.

Instant coffee rises, tea market sinks

In the coffee market, while chain coffee shops with scenes as their selling points are booming, instant coffee, which was originally at the bottom of the coffee contempt chain, is also beginning to rise.

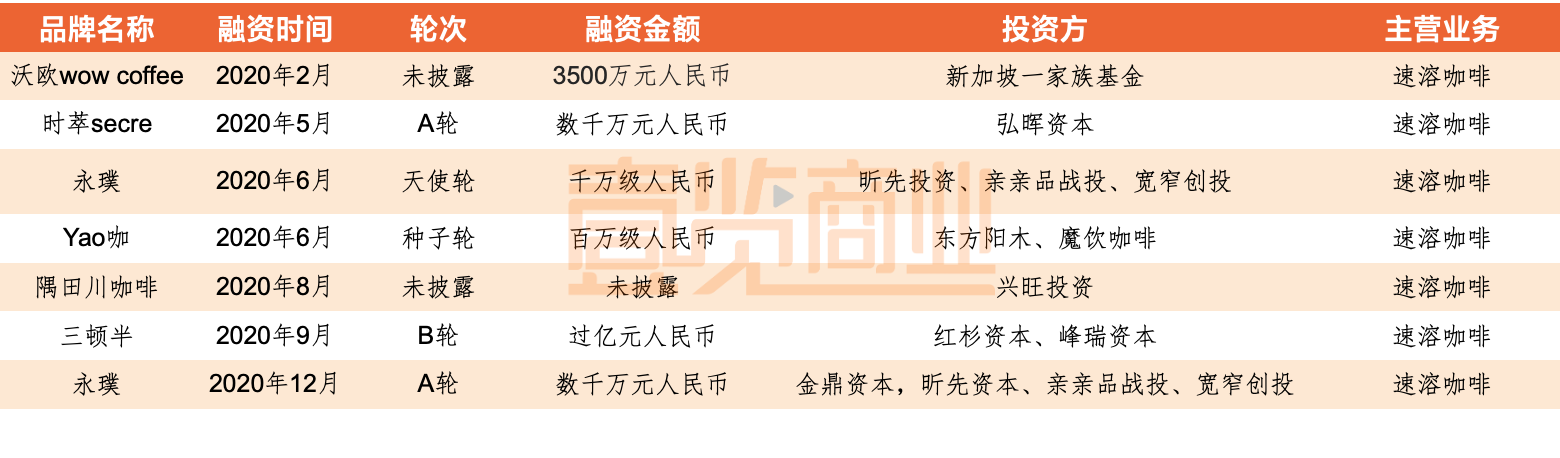

At the end of December 2020, after half a year, the instant coffee brand “Yongpu” announced that it has once again completed a tens of millions of A round of financing. In September, it also focused on three and a half meals of boutique instant coffee, and also announced the completion of a round of financing of more than 100 million yuan. .

According to incomplete statistics from “One View Business”, since January 2020, a total of 6 boutique instant coffee brands including Yongpu and Sandunban have completed a new round of financing. Among them, Woou Coffee was established in 2016, and its main products are instant three-in-one coffee (white coffee) and instant black coffee; Shicui secret coffee was established in 2019, focusing on premium instant coffee; yao coffee was established in 2019, focusing on melting coffee powder.

Take Sandunban as an example. Its main body is Changsha Sandunban Coffee Co., Ltd., established in 2015. Its signature product is ultra-instant coffee, which is quickly dissolved in ice milk, ice water and soda water, and its taste is close to that of freshly ground coffee. Relying on instant coffee, Santon quickly became famous in the instant market and obtained multiple rounds of financing. According to Tianyan Check, as of the end of 2020, three and a half years have completed five rounds of financing in less than five years, with an overall valuation of more than 800 million yuan. It is evident that instant coffee is affected by capital intimacy.

In terms of sales volume, instant coffee also performed very well. When Yongpu received its second financing at the end of December 2020, its sales had achieved a five-fold increase in sales compared to the previous June when the first round of financing of tens of millions of dollars occurred; 3. In 2019, the sales volume of Double 11 surpassed Nestle in one fell swoop, and reached the top of Tmall coffee category. In 2020, Double 11 continued to win the championship, with sales exceeding 100 million yuan.

In fact, although instant coffee is at the bottom of the coffee contempt chain, in terms of market share, instant coffee has always accounted for the majority. According to Tao data, as of 2018, my country’s instant coffee market is about 70 billion yuan, accounting for about 72% of the entire coffee consumer market. Among them, Nescafe ranks first with a market share of 28.5% and has a solid position, making it difficult for instant coffee to innovate for a long time.

The reason why the boutique instant coffee represented by Three and a half and Yongpu can rise under the strong pressure of Nestlé is that the new retail business review special commentator He Yi stated that they are largely due to their accuracy. Cut into the segmented field, seize the opportunity of the blank market with innovative products, and meet the needs of users in the immediate scene.

The latest Kantar Consumer Index report shows that in 2020In the 52 weeks before September 11, the online shopping channels of the instant coffee market increased by 15% year-on-year, mainly due to the significant expansion of the consumer base buying instant coffee from e-commerce companies, and the rate of new recruitment was faster than the same period last year.

Different from the breakthrough of coffee varieties, new teas are sinking into the channel.

As of the end of 2020, there are close to 500,000 tea shops nationwide. According to iiMedia Consulting’s data, from 2016 to 2019, the growth of the tea market in third-tier and lower cities reached 138%, surpassing the growth rate of 120% in Beijing, Shanghai, Guangzhou and the new first-tier cities; at the same time, the closing rate of tea drinks in third-tier and lower cities 15%, which is far lower than the 55% closing rate of tea shops in first-tier cities.

Because of the new-style tea market, the top brand has been stable, so no matter from the capital or market perspective, the new-style tea market in first- and second-tier cities is almost saturated.

Therefore, sinking to the lower-tier market has become a new choice for new-style tea. In fact, in 2020, the sinking market of new-style tea drinks is also changing, and many excellent brands such as Michelle Ice City, Tea Yanyue Se, and Gu Ming are emerging.

Michelle Ice City was founded in 1997 and is headquartered in Zhengzhou. It is the first tea brand and the first tea player to focus on the third and fourth tier markets. According to the data of the narrow door dining eye, Michelle Ice City has achieved a national layout with 11,926 existing stores. Among them, there are only 388 first-tier cities, accounting for only 3.3%. Michelle Ice City has only 60 stores in Shanghai, 44 stores in Anhui prefecture-level city Fuyang, and 65/49 stores in Baoding/Handan, Hebei.

In addition, Michelle Ice City also opened stores around various university cities to conquer student consumer groups. On January 13, according to “LatePost” news, the new tea brand Michelle Bingcheng completed the first round of financing of 2 billion yuan. Dragon Ball Capital and Hillhouse Capital jointly led the investment. It is reported that the two parties invested 1 billion yuan each. After the financing is completed, Michelle Ice City is valued at more than RMB 20 billion. In addition, Michelle Ice City plans to list on the A-share market. The preparations for the listing have reached the final stage and the listing process is expected to be completed within this year.

Guming, which received financing in July 2020, is also a typical tea brand rooted in third- and fourth-tier cities. According to China Business News, as of April 2020, Guming has opened more than 3,000 stores across the country. . Tea Yanyue, which originated in Changsha, will gradually expand outward in 2020.

You want coffee and milk tea

As more and more people enter the game, the competition becomes more and more fierce. In order to compete for the market, both coffee and tea drinks are no longer just staring at their own three-acre land.

In April 2020, Hey Tea launched a low-key coffee single product, jumping out of its inherent milk tea category. Coffee’s competitors, the coffee brand “Xixiaoka” is also registered;

On November 25, Naixue’s new tea shop “Naixue PRO” opened in Shenzhen. This type of store added specialty coffee products and launched 7 specialty coffees. The product is positioned as “daily specialty coffee” and the pricing range is 15-24 yuan;

In 2019, the coffee brand Luckin launched the milk tea brand Xiaolu Tea to compete with the milk tea brand for the tea market. Starbucks started selling tea in stores as early as 2018.

The first coffee maker was CoCo, an old tea brand. As early as 2014, it had cooperated with coffee service organizations to open CoCo Cafe offline stores. Currently, the number of stores exceeds 1,500, accounting for half of CoCo stores nationwide.

Michelle Ice City launched a sub-brand “LuckyCup”, which is consistent with the main brand positioning. Except for the lower price of latte, which is 8 yuan, other drinks are basically between 10-15 yuan.

Nowadays, under the wave of consumption upgrades, coffee and new tea drinks have developed rapidly in recent years. With the blessing of capital, competition in the current nearly trillion coffee and tea market has long been heated up, and the Matthew effect has become prominent.

In the face of rising costs and fierce competition, the pressure to survive increases. Therefore, breaking through the development of a single category seems to be the best choice for the brand. Today, Hi Tea’s application for the “Hi Xiao Ka” trademark and its entry into the coffee field are similar to Luckin’s “Little Deer Tea” in the past. There is a category ceiling, try to find more growth possibilities in new areas.

Finally, it is worth noting that in the coffee and tea race track, many entrants, such as brand marketing, store digitalization, product health, and packaging environmental protection, are trying. This will also be the future trend. In 2021, we will continue to pay attention to how the coffee and new tea-drinking track will expand and what kind of waves the market will cause.