Fintech startups are beginning to become more like traditional financial companies, using economic thinking to focus on indicators that are more closely linked to “money” such as risks, returns, and losses.

Editor’s note: This article from the micro-channel public number “Silicon rabbit race” (ID: sv_race), of: Lexie, Editor: Lu.

In January this year, the US “Huabe” Affirm went public, and it closed up 98.45% on the first day of listing, to US$97.24, with a market value of US$23.6 billion. As of press date, Affirm’s stock price is close to $105.

In early February, Robinhood received a total of US$3.4 billion in financing from investors within a week, surpassing its total financing since its establishment in 2013.

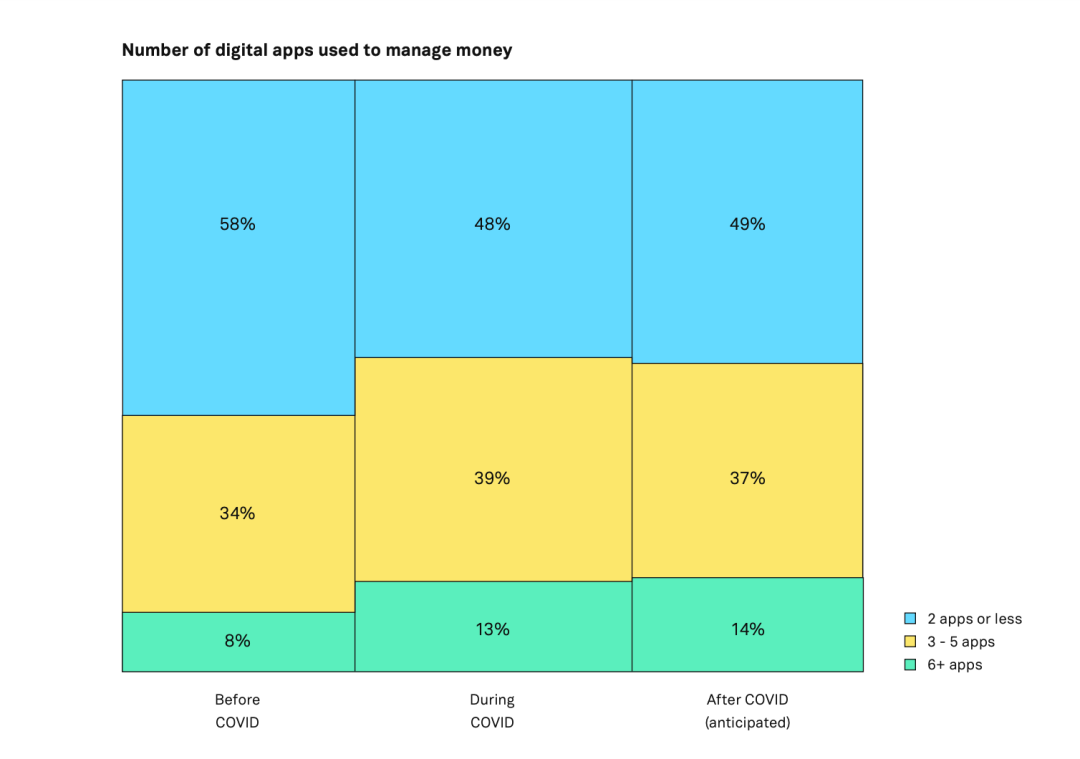

The new crown epidemic has accelerated people’s acceptance of digitalization in various industries, and financial technology is no exception. According to a survey by financial technology startup Plaid, 73% of the respondents said that using financial technology for financial management has become a “new routine”, 80% Of people say that they can complete all financial management tasks without going to the bank. 69% of people say that fintech has played a role in saving time, money, and stress, which is more than “life-saving”. Generally speaking, it has become people’s financial management The best choice.

As people’s demand for financial technology increases, funds are also flocking to this field. In the environment of the 2020 Black Swan Year, financial technology companies have performed well.

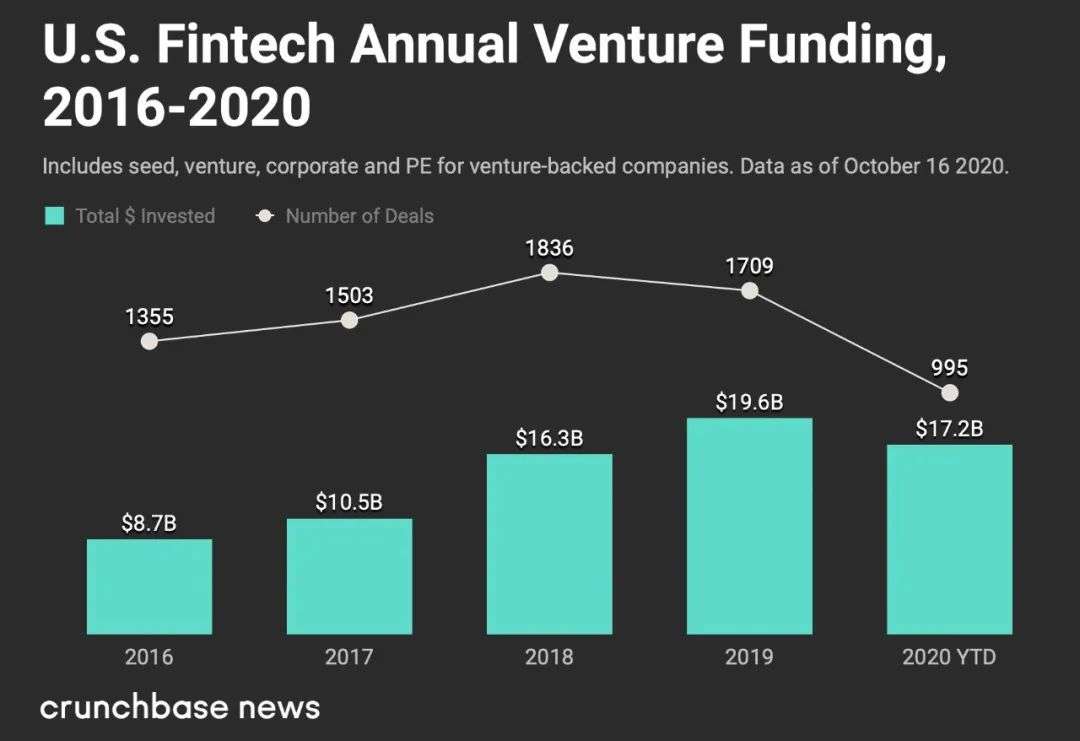

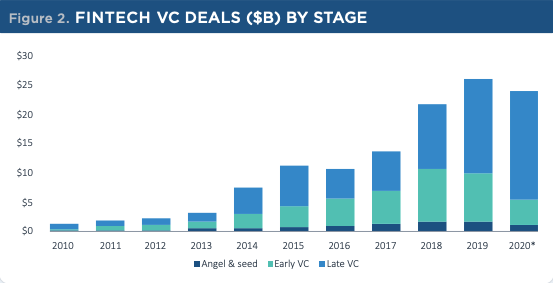

According to data from the financial software company Tipalti, a total of 76 new unicorn companies will be created worldwide in 2020, of which 17% will come from the FinTech track. At the same time, data from Crunchbase News as of the end of October last year shows that the total financing of the global financial technology sector in 2020 is approximately 26.5 billion US dollars, accounting for 14% of the total global investment.

In 2020, a total of 995 transactions in the financial technology sector in the United States were completed, with a total financing of US$17 billion. Compared with the US$19.6 billion under 1709 transactions in 2019, it presents the characteristics of a larger financing amount, and most of them are concentrated in A later company.

PitchBook’s data also shows that in recent years, the investment allocated to angel/seed rounds and early stages in the financial technology field has decreased, and the investment allocated to later stages has increased.

This means that it is more difficult for early-stage startups to break through in the field of financial technology. Early-established startups are constantly increasing their products, financial institutions are improving their technological level, and the original Companies that have nothing to do with it also want to join. This is the trend of “every company will become a financial company” that will be discussed below.

Currently, the hottest investment areas of financial technology include insurance, banking, lending, and of course, essential electronic payments.

Plaid: Almost “married” with Visa, with a 60% increase in users last year

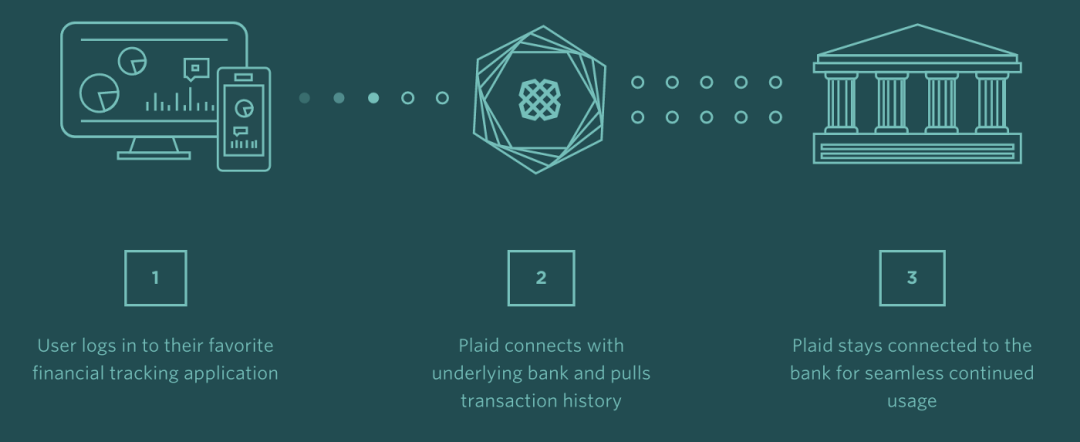

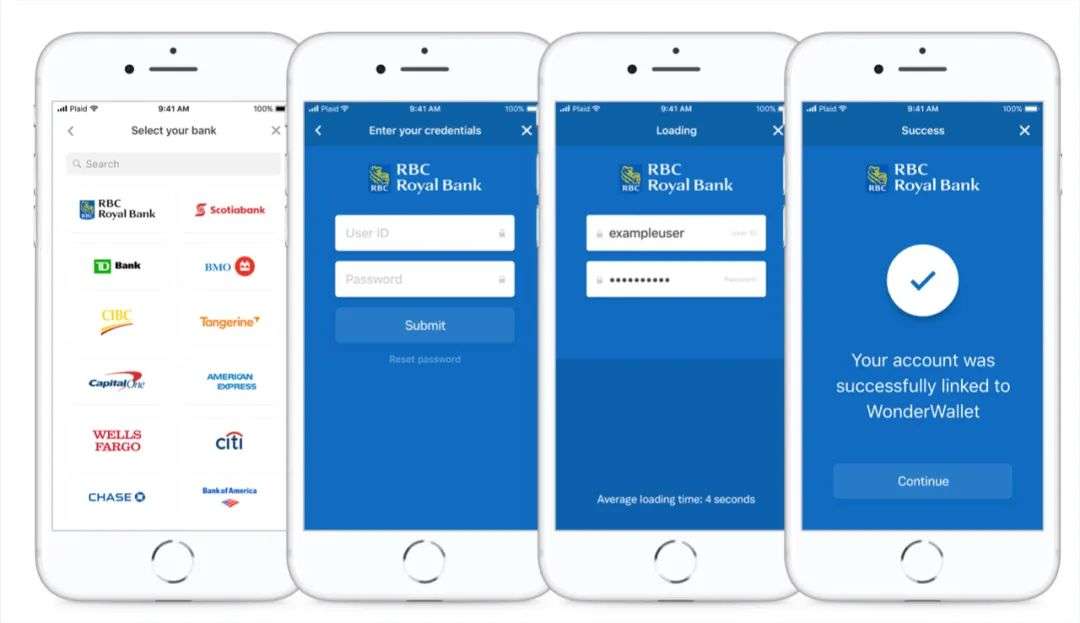

Plaid is growing into a strong force in the field of financial technology. Plaid was established in 2013. Its core product is API (application programming interface) software in the direction of financial services. It empowers software infrastructure and allows the main financial The software development team of the technology app can obtain information and data from financial institutions, and smoothly create the digital financial products we love, so that users can easily connect their financial institutions to the app. It is said that four out of the people in the United States have bank accounts. One of them is using Plaid.

Plaid’s clients include mobile bank Varo, Venmo for payment, Robin for investmentHood, Credit Karma for tax filing, Affirm for lending, and robo-advisor platform Personal Capital and other “net celebrity” apps.

Another point of Plaid’s attention is that its core technology will also play an important role in DeFi (decentralized finance).

Currently, Plaid’s service only involves payment accounts. The same principle can also be applied to encrypted assets. Plaid is currently working with DeFi startups such as Dharma and Teller Finance to study how to take this development further.

Plaid has completed 4 rounds of financing so far, with a total financing of 309 million US dollars. The investors behind it include Index Ventrues, Kleiner Perkins, Goldman Sachs Investment Partners, Spark Capital, etc.

Plaid also experienced great ups and downs last year and the beginning of this year. The “rising” stems from the news that came out in January last year that Visa will acquire Plaid for US$5.3 billion, young consumers represented by millennials. More and more are embracing the trend of digital finance and using fintech apps for financial management. As a credit card giant, Visa is also catering to the needs of consumers. It would have been a good combination of strengths, but…

The U.S. Department of Justice filed an antitrust lawsuit in November. After about a year, Visa announced that it would abandon the acquisition of Plaid. This once-preferred marriage “falls” to the end. Plaid’s seemingly sad result It’s not too sad. Founder Zach Perret said that Plaid itself is growing very fast. Even if it is not included in Visa, it will not lose anything. In an interview with TechCrunch, Plaid revealed that Plaid’s users have increased by 60% in 2020 and have With 4,000 new customers, revenue increased by about 3 digit percentage.

However, this hammer from judicial policy has smashed many financial technology companies’ dreams that they may successfully exit through M&A in the future. Apart from this, the industry’s response is mostly happy for Plaid.

For example, Amy Cheetham from Costanoa Ventures believes that “Such results will allow Plaid to acquire new products and develop products faster, and the final valuation will be higher.”.

Investors such as Allen Miller from Oak HC/FT and Sri Muppidi from Sierra Ventures hold similar attitudes. They pay more attention to the development potential of API software companies represented by Visa’s acquisition intention. Fiery is not a flash in the pan, but will change the future of the software industry.

Affirm: There are risks behind the rapid growth

In terms of electronic payment, financial technology in Europe and the United States has not developed as fast as domestically. Start-up companies and traditional financial industries have been late in the deployment of this field, and this year has gradually become popular in this field.

The first to bear the brunt was Affirm, which was just listed on the Nasdaq in mid-January. It was founded in 2012 by Max Levchin, known as the “Paypal Mafia”, to provide users with small purchases before paying. Loan services are often referred to as “Huabei” in the United States. Users can make monthly payments, with interest lower than the high interest rates of traditional credit cards and no compound interest.

Affirm currently cooperates with more than 6,500 merchants, including Walmart, Adidas, Nordstrom and other well-known brands. The e-commerce dividends brought by the new crown epidemic have played a certain role in the development of Affirm, such as home furnishings and home exercises. , Home office supplies and other companies themselves have benefited from the epidemic, and Affirm has also benefited from it.

One of the things I have to mention is the spinning bike Peloton. The revenue of this business alone accounts for 28% of Affirm’s revenue in 2020. This arrangement makes many people feel a bit “virtual” because Peloton itself can be behind. It is hard to say that it will maintain the momentum of growth in the era of the epidemic, which makes Affirm more risky to obtain stable income.

In addition to this weakness, Affirm is currently improving as a whole. The closing stock price rose 98.45% on the first day of listing to close at $97.24, with a market value of $23.6 billion. It has become the “darling” of Wall Street, so its growth and financial How is the situation?

In fiscal year 2019, Affirm’s revenue reached US$264.4 million, and this figure reached US$509 million in fiscal year 2020, achieving a 93% growth, while its losses are also decreasing. The annual loss of US$120 million was reduced to US$112 million in 2020.

User activity and total transaction volume (GMV) are also growing positively. Its GMV for fiscal year 2019 was US$2.62 billion. In 2020, this figure reached US$4.64 billion. The number of active users in 2020 has increased from 2019. Of 2.38 million rose to 2.88 million, and the average number of active users in the third quarter of 2020 was 2.Two times, compared with the two times in the same period in 2019, there was also an increase.

At the same time, Affirm currently has sufficient funds and has now completed $1.5 billion in financing. The most recent round occurred in September last year and completed the $500 million Series G financing led by GIC and Durable Capital Partners LP.

50% of shoppers around the world have begun to use electronic payment more due to the impact of the epidemic. Major companies in the electronic payment field also benefited from contactless payment and e-commerce dividends last year: Paypal ranked second in 2020 Quarterly revenue increased by 22%; Square data shows that in February 2020, only 5.4% of Square sellers used cashless transactions, and by April this number had risen to 23.2%.

Affirm is not only competing with payment giants such as PayPal and Square, but also other industry giants who want to share a slice of the electronic payment track and are preparing to enter the game.

Tech giants are competing: every company will become a fintech company

Just in early January, Walmart issued a statement on its website, announcing that it has reached a strategic partnership with financial investment company Ribbit Capital to establish a new financial technology startup to create innovative and cost-effective financial products for customers and employees. The details have not been disclosed, but Wal-Mart has already started testing financial services.

For example, the launch of the “layaway program” allows customers to pay the down payment first to own the product and then make up the balance, and the prepaid debit card “Moneycard” allows customers to deposit money in the card for consumption, get cash rebates, etc. This is considered a formal entry into the financial technology field. Wal-Mart’s strong user base in the retail industry and Ribbit Capital’s experience in successfully investing in Robinhood, Credit Karma, Affirm and other companies are worth looking forward to.

There is no doubt that the battle in the payment field has already started, and Amazon is also one of the participants.

From the launch of Pay with Amazon in 2007, to the acquisition of mobile payment startup GoPago in 2013, to accessing Worldpay, the world’s largest payment operator in 2019, to the development of Amazon Go unmanned stores and possible sweeping payments in the future. Amazon has made a lot of efforts in payment in the past few years.

Not only payment, but Amazon is also active in SME loans, cash, and insurance. It is also actively deploying financial infrastructure. What is its intention? Through financial technology services, Amazon can gain more merchants and users, improve the consumer experience, and expand Amazon’s overall ecology.

This trend is also in response to the speech theme of a16z investor Angela Strange at the a16z Summit “Every company will become a fintech company”. This trend is happening.

We used to think of it as a “computer” Apple launched its own credit card in 2019; Shopify, while providing online e-commerce services for thousands of merchants, also launched allowing merchants to allow users in batches Payment technology and Shopify Balance bank account; Debit card services provided by shared platforms such as Uber and Lyft allow its profits on financial services to subsidize the large cost of recruiting drivers, with an additional value proposition. It is easier to retain the driver.

According to the survey, only 28% of millennials and Generation Z trust the financial services of banks, and more than 50% of people in the United States have no deposits. Traditional financial institutions are not likable, and the speed of the emergence and growth of fintech startups It’s not fast enough. What we lacked before was not the needs of consumers, but the enabling infrastructure.

At present, the innovation of “infrastructure as a service” is happening rapidly in the financial field. Just like Amazon’s aws provides people with cloud computing and storage infrastructure, Plaid allows startups to quickly acquire users in financial institutions In the next few years, we will see more companies like Plaid create a smooth and stable 2B infrastructure in multiple fields including user interface, data, supervision, payment, fraud prevention, etc., so that these segments More 2C services have emerged on the track.

Plaid founder and CEO Zach Perret also said in an interview with TechCrunch that software is swallowingTo eat the world, financial service companies must arm themselves with technology, and every company will eventually become a financial technology company. There are still vacancies in the 2C field, but there is even more potential for financial technology to empower infrastructure like Plaid.

While Amazon is launching a war against financial institutions and wants to disintegrate it piece by piece, we have also seen financial technology startups begin to transform from small and sophisticated to large and comprehensive.

From small and sophisticated to large and complete

The first batch of fintech companies were born in the early 2000s. Although banks provided a full range of financial services at that time, they did not provide sophisticated services in every part. Therefore, many fintech start-ups held that “one skill can gain the world.” “The original intention was to show off their talents. A few years later, a group of segmented track leaders such as Robinhood, SoFi, and Chime emerged in fields including robo-advisory, lending, and financial management.

Robinhood has become synonymous with American retail investors challenging Wall Street since its inception. In late January and early February, due to the fluctuation of the Gamestop market, it still closely completed two rounds of financing totaling 3.4 billion US dollars. However, retail investors are prohibited Investors buying certain stocks have become the target of public criticism, and they may be “revenged” by users after the IPO, which makes its future more unknown.

SoFi, which provides users with loan and wealth management services, is currently valued at US$8.65 billion. At the beginning of this year, there was news that it was going to be listed through SPAC.

After the digital bank Chime completed a $485 million financing in September last year, its valuation reached $14.5 billion, surpassing Robinhood to become the most valuable financial technology company in the US consumer sector.

Although these apps have their own strengths, the result is that users who want to manage their own finances have to download more than 10 software on their mobile phones, which is complicated and cumbersome; for these companies, as more and more players Entering the fintech track, a single core product cannot win, so we see more and more start-ups begin to expand their product lines and strive to become an integrated platform with multiple financial products.

For example, M1 Finance, which has a history of 5 years so far, was mainly engaged in robo-advisory business when it was established. Today, it is positioned as a super app that integrates investment, lending, and spending. Users can complete the app for free. Build investment portfolios, check credit, and make regular repayments.

M1 Finance completed two financings in succession last year, including $33 million in Series B financing in June and $45 million in Series C financing in October. The investors behind it include LeftLaneCapital, Jump Capital, and Clocktower Technology.Ventures, etc., the additional funds will be used to develop this goal of becoming a “super app”.

For example, Credit Karma, which was acquired by Intuit for $7 billion in February last year, was originally designed to provide consumers with credit scores and credit reports. In recent years, the product line has been continuously expanded, such as the introduction of tax preparation The service “Credit Karma Tax®” allows users to judge whether they can apply for “Karma Drive” for auto insurance and high-yield current savings accounts based on their driving level.

For another example, Revolut, headquartered in the United Kingdom, has frequently added new features since last year. First, the main app interface is divided into two major sections. In the Home section, users can manage and analyze their own income and expenses. In the Wealth section, users can Investing in stocks and bitcoin; launched the “perks” function for British users so that they can get cash back and discounts when using Revolut cards; also launched a gold transaction function for VIP users; even launched a teaching child money A separate app “Revolut Junior” managed by the company.

Revolut has so far completed 16 rounds of US$917 million in financing. The most recent round occurred in July last year, with an investment of 80 million US dollars led by TSG Consumer PartnersUSD Series D financing.

These companies’ efforts to launch more product lines and become “super apps” like WeChat and Alipay are mostly driven by the pressure of profitability. Since last year, science and technology companies have been following the “growth first. The belief that “profitability will be discussed later” is no longer true in the field of financial technology.

Profit>A year of growth

If there are no natural and man-made disasters, every company will follow its own steps to achieve growth goals, and the variables brought by the epidemic have made many companies find that just looking at growth data at this time seems to be “vanity metrics”, because especially many 2C companies The survival depends on the user’s behavior on the app, and this is a very fickle style of play.

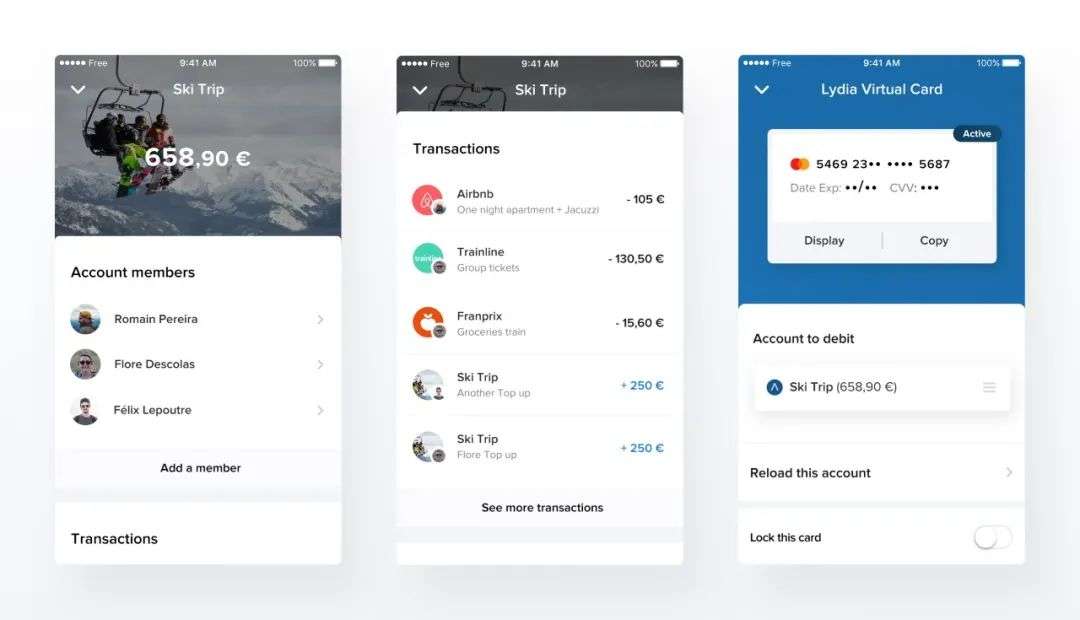

For example, Lydia, a mobile payment startup from France, was founded 7 years ago and has become a one-stop financial service application including bank accounts, payment cards, instant loans, insurance and other applications. It currently has 3 million users in France , 25% of people aged 18-30 in France have a Lydia account. However, because its service relies heavily on transfers between users, during the period of severe epidemics in European home quarantine, user usage was greatly reduced, and the transaction volume on the entire app in April decreased by 70%.

Lydia completed a US$45 million Series B financing led by Tencent at the beginning of last year. At this juncture, Tencent also gave suggestions based on domestic home isolation experience. Lydia quickly began to provide contactless payments and virtual bank cards. Wait for service transformation, and make profit as the main goal.

In the field of financial technology, there are three main income channels for consumers:

1. Debit card

When users register, they will get a debit card issued by the platform to complete future payment tasks. When users use this card for transactions, the commission fee paid by Visa or Mastercard is the income of the financial service company, such as Digital banks such as Chime and Varo use this model. Each transaction fee is not high, but if the number of users is large enough, it is also a good income channel, but this premise greatly depends on the number of users and the number of user transactions.

2. Financial products

????Many of the startups mentioned are developing more product lines. The ways to become super apps fall into this category. The wide range of financial service products they provide do not all belong to their own, such as Paypal in Last year, it reached a cooperative relationship with Paxos, allowing users to buy and sell Bitcoin on Paypal, and the fees charged became the main income.

3. Subscription service

Subscription service is the most stable of these sources of income, and it is also the model adopted by many apps at present. For example, the three “easy, personal, and family” membership systems of the micro-investment platform acorns provide different Investment service level:

Robinhood launched Robinhood Gold with a monthly fee of $5. Users can enjoy exclusive features such as market data under professional research, twice the purchasing power, and extended transaction duration:

Because many people usually adopt a “subscribe and forget” attitude towards subscription services, even when the number of users and transactions decreases, the income from the membership system will suffer less, and the membership system under a fixed fee It also allows these companies to work hard on the included functions to adjust their needs to retain members. For example, digital banks N26 and Monzo adjusted their membership subscription system last year, taking into account the current situation of the tourism industry that has been hit by the epidemic, reducing The proportion of travel insurance in financial services.

In the turbulent environment of last year, financial technology did not regard growth as its main goal, but collectively reflected on how to strengthen its product portfolio and create more resistant income channels. At this point, Fintech startups are beginning to become more like traditional financial companies, using economic thinking to focus on indicators that are more closely linked to “money” such as risks, returns, and losses.

If it is really like what Angela Strange and Zach Perret of a16z said, every company will become a financial technology company, and infrastructure as a service will redefine the speed and scope of the emergence of financial technology. Players such as Wal-Mart and Amazon have entered the game, small startups have begun to transform to integration and are also working towards profitability goals. In addition, sometimes policy c has the ups and downs of the plot. It is not yet known who will win on the financial technology circuit, but this battle is a big deal. There is absolutely no shortage of wonderful things.

Reference:

1. Affirm files to go puclic (Tech Crunch)

2. Survey finds that fintech has been a lifeline during COVID-19; consumers say it’s the “new normal”(Plaid)3. Fintech Startups Broke Apart Financial Services. Now The Sector Is Rebundling(Crunchbase)4. Venture capitalists react to Visa-Plaid deal meltdown(TechCrunch)

5. increasingly Fintech startups are focusing on profitability(TechCrunch)

6. State of the Fintech Industry with Infographic (Finance)7. Every Company Will Be a Fintech Company(a16z)8. Fintech VC keeps getting later, larger and more expensive(TechCrunch)9. Everything You Need To Know About What Amazon Is Doing In Financial Services(CBInsights)