2021, who will “kick the hall”?

Editor’s note: This article is from the public micro-channel number “to win business cloud Intelligence” (ID: sydcxy2014), Author: Liang Chu Tong.

Compose丨Liang Chutong

Edit丨Fu Qingrong

On the first floor, the shopping mall’s “facade” is a place where powerful brands are competing for a position-decent and attracting customers, but the rent is high, not everyone can earn it back.

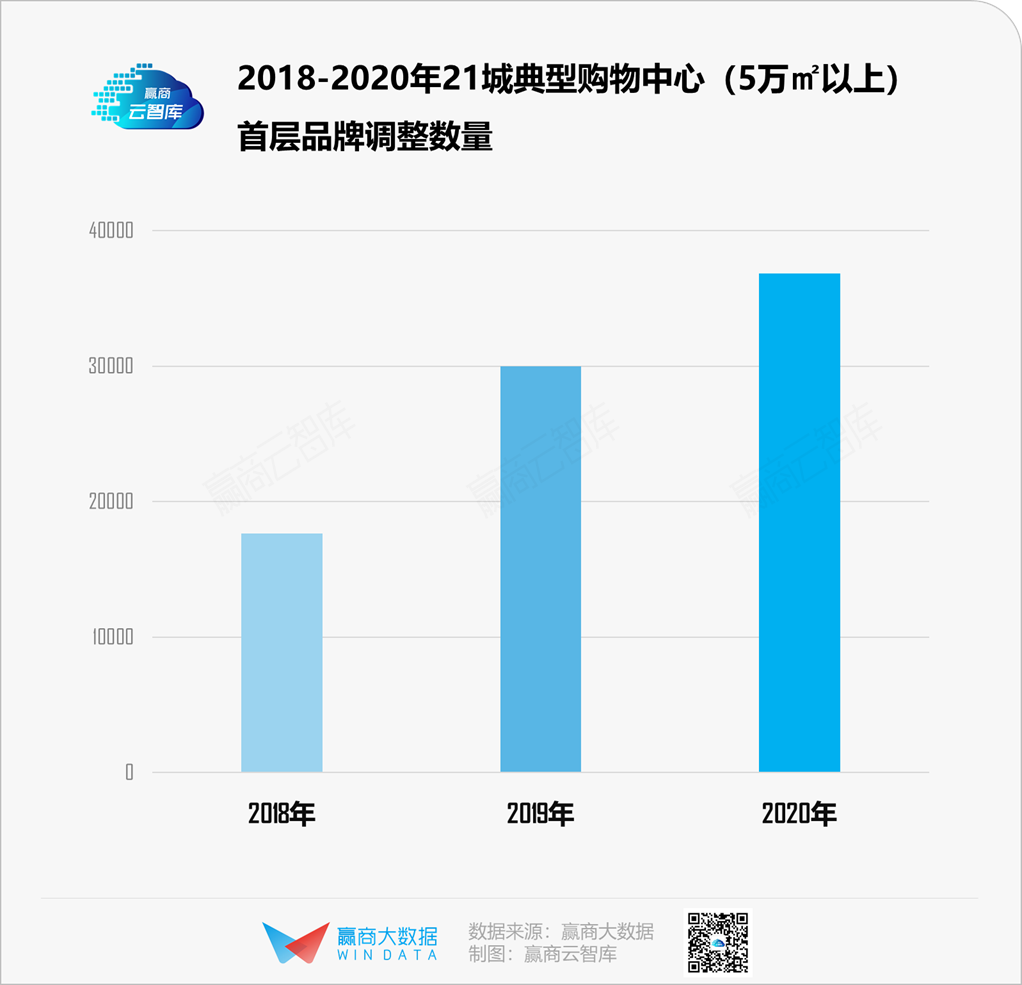

According to the statistics of Winshang Big Data, in 2020, there will be 1,080 shopping centers in 21 cities with more than 50,000 square meters. The first-level brand “big exchange”, the number of adjustments is nearly 37,000 (including transfers in and out) ), the brand opening and closing ratio of 0.85, slightly higher than the overall shopping center opening and closing ratio (0.78).

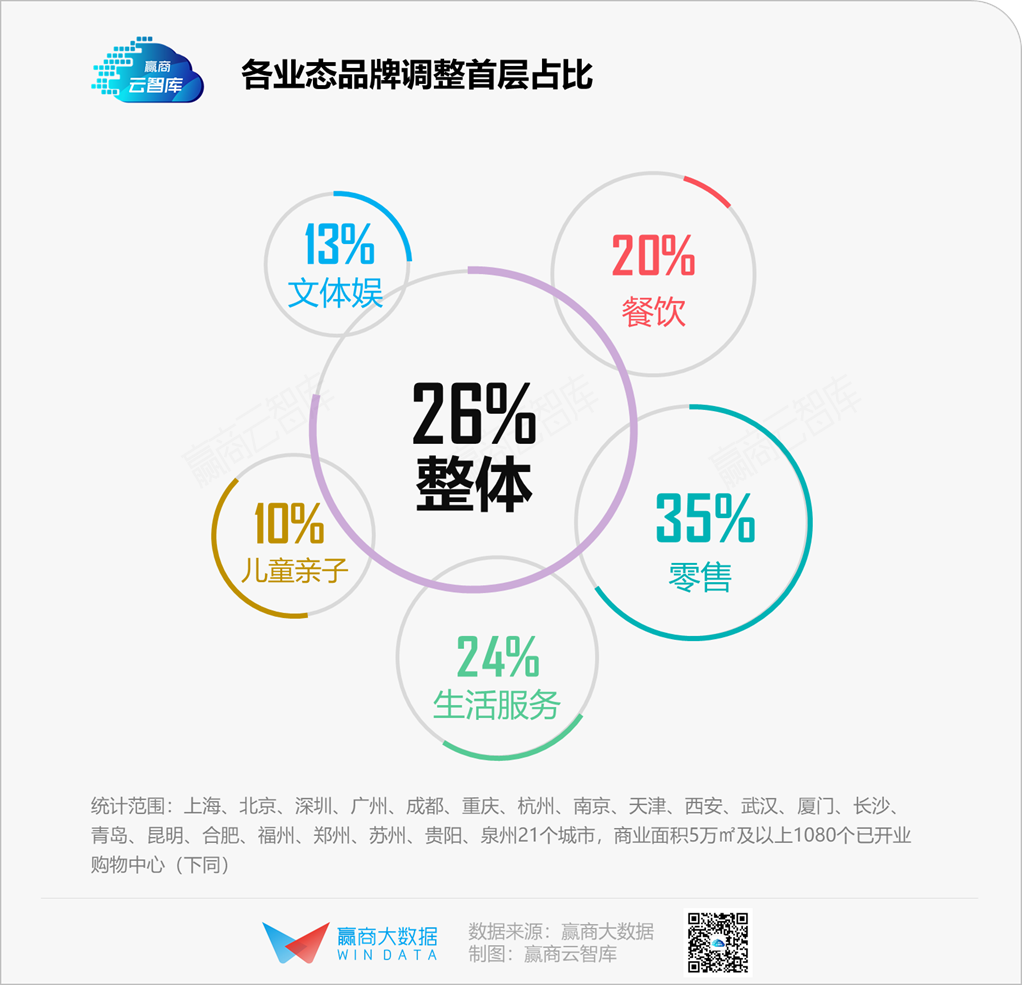

These 37,000 brands have been adjusted on the first floor, accounting for about 26% of the total brand adjustments of 1,080 malls, ranking the most among all floors. According to the format, 35% of the adjustment of retail brands occurred on the first floor. New faces came and went quickly.

Long-term perspective, from 2018 to 2020, first-tier retail productsThe ratio of brand opening and closing stores is less than 1, and the overall trend is shrinking. However, in 2020, the ratio of opening and closing stores is basically the same as that of other formats. The ability of powerful brands to “hold the ground” cannot be underestimated; while catering, children’s parent-child, life services, cultural and sports stores The numbers have all changed from expansion to contraction.

It’s also worth mentioning that compared with 2019, In 2020, local brands will show up more frequently on the first floor of shopping malls. They cater to new consumer trends, seize the minds of young consumers, and become shopping malls.” “Fragrant steamed buns”; while the proportion of emerging brands has shrunk to 8.75%. Under the impact of the epidemic, the rentability is weak, and the future challenges in the battle for the first store will be even greater.

01

First-story “protagonist” retail, undersea waves

In the stores occupying 70% of the first floor, the new arrivals and exits of retail brands affect the “big market” of the changes in the first floor of shopping malls. Some are coming aggressively, while others are leaving the market sadly. The segments with the largest number of net increase and decrease in stores all come from retail.

▶ Apparel: Women’s wear meets a bottleneck, sportswear comes to “fill in the blanks”

The women’s clothing business with the largest market scale and the largest number of brands is the main force at the first level of shopping malls. However, the market has become saturated and performance has encountered bottlenecks. There is an urgent need to seek brand rejuvenation and differentiation. It is more prudent to enter the first floor.

Women’s clothing, men’s clothing, and footwear have shrunk sharply than <1 on the first floor of the opening and closing stores for three consecutive years. The "empty" they dug is filled by sportswear. Among the TOP10 brands with net increase in the number of stores on the first floor, sportswear has jumped from 4 in 2018 to 8 in 2020, accelerating its entry into the first floor. Young people in the product and marketing circle, new concept stores, The flagship store is eye-catching and has become a trend checkpoint.

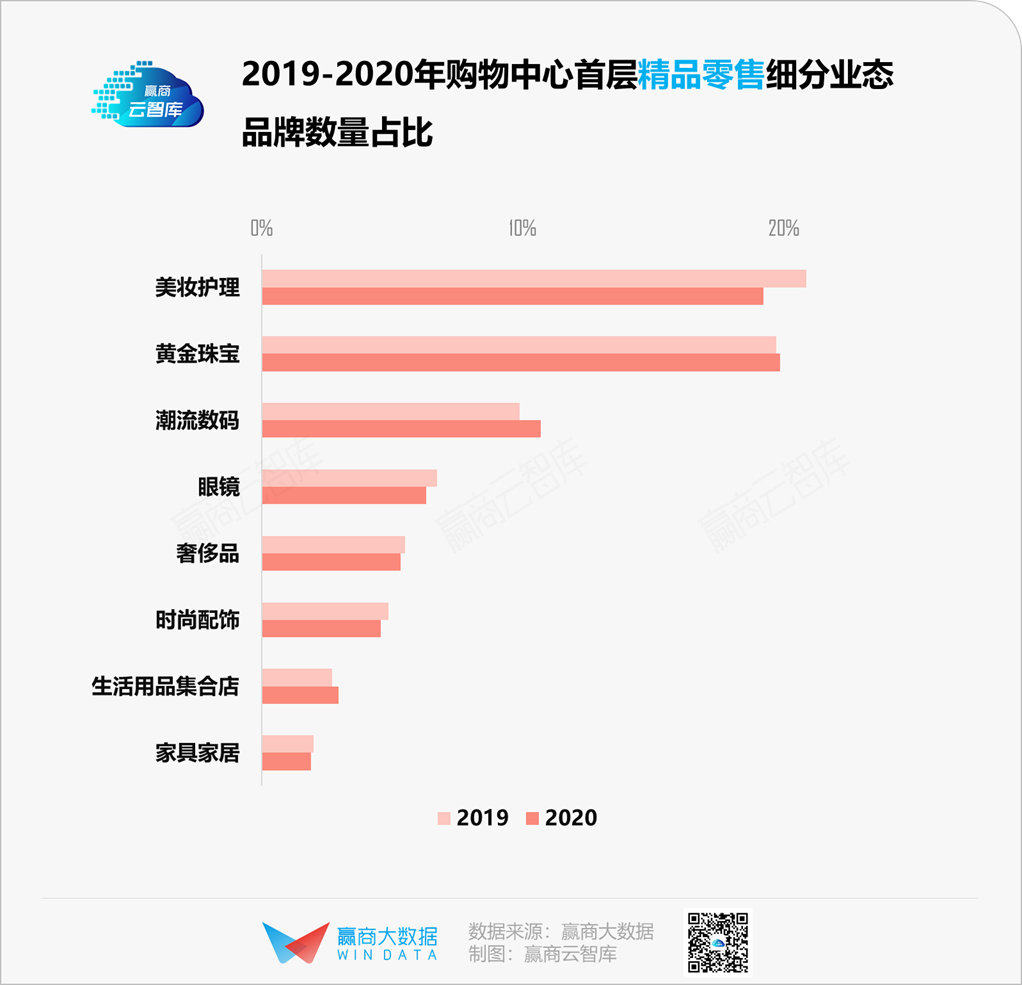

▶ Boutique retail: beauty reshuffle, digital top, luxury advancement

With large demand elasticity, high profits, and strong renting power, beauty care brands are often the “standard equipment” at the door of shopping malls. However, at present, the proportion of this format in the first-level boutique retail has fallen to insufficient 20% and undergoing a round of shuffling. On the one hand, emerging local beauty brands such as THE COLORIST, WOW COLOUR, Perfect Diary, etc. are influx, and international beauty brands such as Lancome and YSL are adding more; on the other side are the low-end brands such as Innisfree, Maybelline, Herborist, etc., which are weak in innovation and attract young customers. The strength is reduced, and he evacuates frequently.

The domestic digital brands represented by Huawei, OPPO, and Xiaomi have not only moved their stores into shopping malls one after another, but also aimed at the first-floor facade and opened experience stores full of technological sense. This brings consumers closer.

Luxury consumption continues to return to China, stimulating their continued increase in the occupancy rate on the first floor of shopping malls. In 2020, the ratio of opening and closing stores will reach 1.48. For every 10 new luxury stores opened, 8 homes will be in the first place. Layer. In contrast, brands such as gold jewellery, fashion accessories, glasses, and home furnishings frequently exit the first floor.

02

“Best supporting role” dining, tea is the most popular

The proportion of first-tier branded stores has risen to 22%, and the presence of the catering business in the first-tier business has continued to increase, but the changes in its segmented business have been relatively stable.

Casual catering, Chinese catering, and exotic catering occupy 90% of the first-tier catering categories. The ratio of opening and closing stores of the three in 2020 is <1, showing a shrinking trend. The "Qi" barbecue category, the compound catering that focuses on the scene, and the light meals that cater to the trend of healthy consumption have made room for expansion.

Casual dining, which accounts for nearly half of the number of stores, is the focus of shopping malls. Among them, the “most grabbing show” is the tea-drinking track that has been popular with the market and capital in recent years..

“Buy a cup and drink slowly when you enter the door” has become a standard feature for young people to visit the mall nowadays. Aiming at the first floor with the largest passenger flow, the competition for beverage brands is getting more and more intense. The top brands of Heycha and Naixue’s tea will continue to open 90+ and 40+ first-floor stores respectively in 2020 under the gloom of the epidemic.

03

Children’s parent-child, cultural and sports entertainment, life services:

There are not many “parts”, “face changing” is the fastest

For children’s parent-child, cultural and sports entertainment, and life service formats with clear consumption purposes, large area and weak rentability, the first floor of shopping malls is often not its main battlefield. Brands that dare to enter the first floor are mostly strong in business.

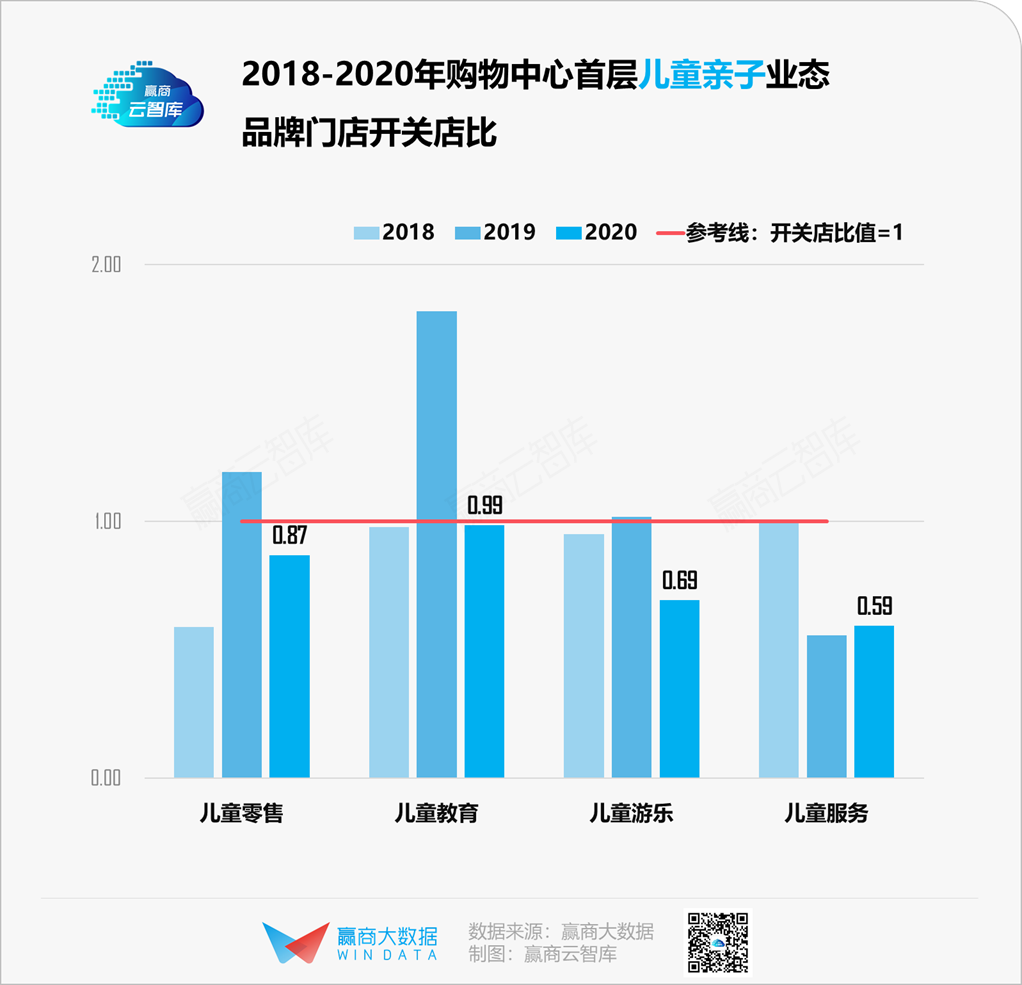

▶ Children’s parenting: children’s retail reshuffle, children’s education or the trend

The first-tier layout of children’s retail, which accounts for 60% of brands, is shrinking. Although the top brands with stable operations are still actively deploying, more brand stores are facing elimination due to inadaptability to market changes; children’s education has a good momentum, and the number of first-floor opening and closing stores in 2020 will be basically the same, except for common English and art training , Robots, technology, dance music training are also becoming first-tier “frequent visitors”.

Lego Toys continues to rank as the largest number of net increase in children’s stores from 2018 to 2020, and other brands have not continued to actively deploy the first tier.

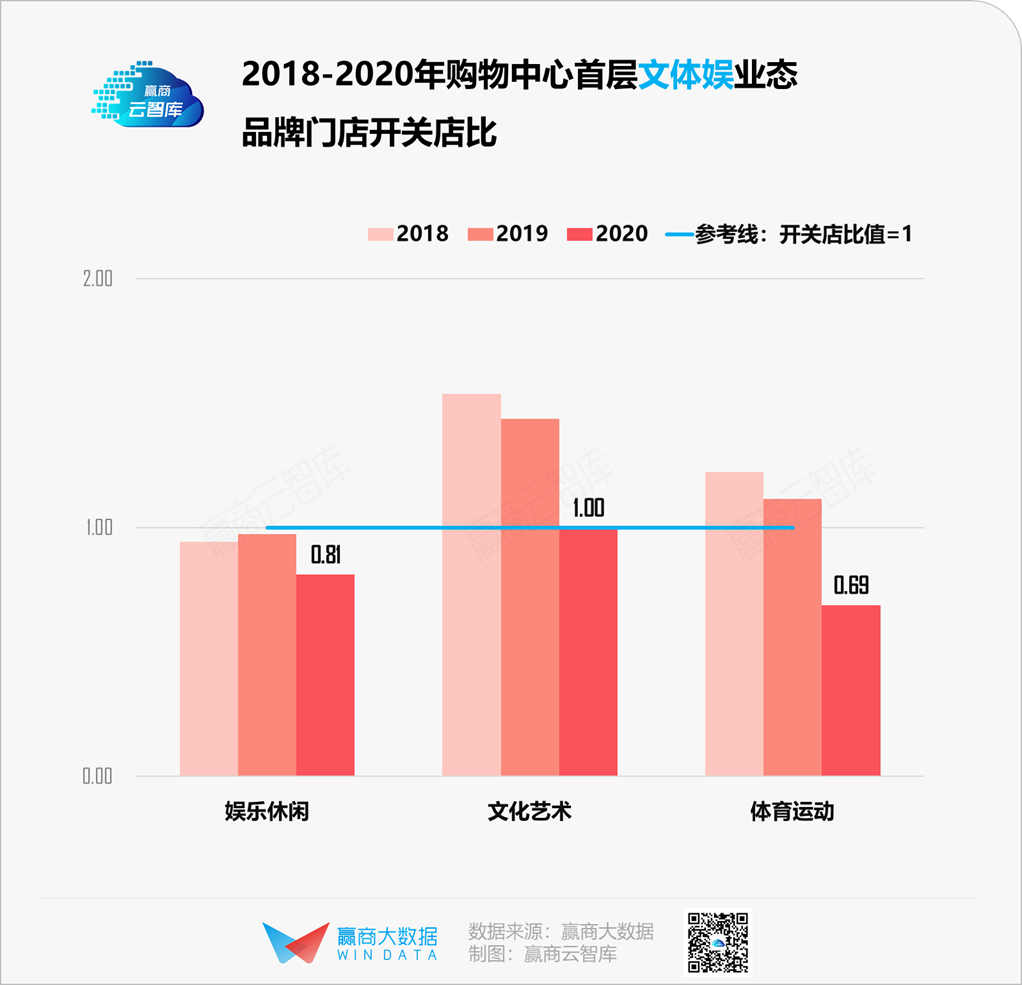

▶ Culture, sports and entertainment: entertainment and leisure, cultural and artistic expansion, sports contraction

Although it only accounts for less than 2% of the number of first-floor stores, there are indispensable scenes of “playing coffee” and “artistic coffee” in shopping malls, which stimulate young consumers with diverse interests. The proportion of entertainment and leisure, culture and art formats has increased, while sports have further narrowed.

Looking at it concretely, the number of first-floor stores in the past three years has seen a large increase in the number of cultural and sports entertainment brands that have hardly replicated, such as VR, claw machines, car showrooms, bars, and bookstores.……Multi-category gradually expanded the first