It’s still a woman’s money to make money.

Editor’s note: This article is from the micro-channel public number “far Chuan Business Review” (ID: ycsypl), Author: Huang Xiangpeng / high wing, Editor: Yao Shuheng.

The A-shares in the first four trading days of this week can be described as miserable, and everyone’s faces are green. However, Huadong Medicine is “a little red among the ten thousand green bushes”, rising by nearly 20% in 4 days. If you start after the Spring Festival, the increase will be even greater.

What made Huadong Medicine stand out was an acquisition announcement. On February 17, this veteran pharmaceutical and drug selling company announced that it would acquire Spanish medical beauty company High Tech at a price of 65 million euros. This is a company that manufactures cryo-fat and laser hair removal equipment. Based on the transaction price, the valuation is about 13 times the price-earnings ratio and 3 times the price-to-sales ratio.

Under the environment where A-share Amerco and Huaxi Biologics are frequently valued at two to three hundred times, this valuation level is simply horribly cheap.

In fact, this is not the first time Huadong Medicine has acquired a medical beauty business/company. From acquiring the agency rights of Ewan Hyaluronic Acid and Jetema Botox in China to acquiring manufacturers in the UK and Sweden, I have already stocked a relatively complete product pipeline without knowing it.

After the epidemic raged, the entire medical aesthetics industry in Europe and the United States was hit, and it also gave Chinese capital the opportunity to go overseas to purchase high-end medical aesthetics equipment that is currently in short supply in China at a low price. Huadong Medicine’s acquisition of High Tech is an example.

Then the question is here:

1. Why does Huadong Medicine frequently acquire medical beauty projects?

2. What is the current status of Huadong Medicine’s medical aesthetics pipeline?

3. From generic drugs to medical beauty, how to price Huadong Medicine?

Failed to benchmark Hengrui

Huadong Medicine and Hengrui were two big white horses recognized by the pharmaceutical industry in the past. From 2008 to 2018, the share prices of the two companies have increased by nearly 20 times in the past 10 years. The company has also become the most enthusiastic comparison object in the market.

However, in the following years, East China gradually declined. The essential reason was the misalignment of revenue and profit.

Huadong Medicine was established in 1993. Compared with Hengrui, Huadong is a comprehensive pharmaceutical company. The so-called comprehensiveness means that you can produce it yourself, sell it yourself, and distribute it yourself. This is a bit too decentralized for a pharmaceutical company. In recent years, the pharmaceutical industry has increasingly focused on specialized division of labor, and this “want everything” business layout has given this company a lot of historical burden.

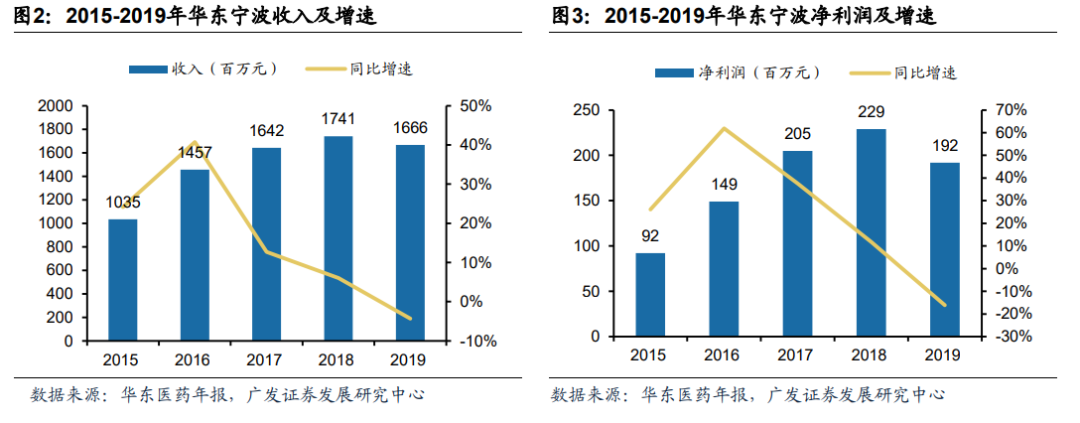

From the financial report of the past few years, its pharmaceutical business revenue accounted for nearly 70%, which is an important source of revenue for the company, and the second largest source of revenue is pharmaceutical manufacturing, which accounts for nearly 30%. However, revenue accounted for only 30%However, its pharmaceutical manufacturing business contributed 70% of the profits, and the rapid growth of 20% of the company’s performance in recent years is also dependent on the growth of the pharmaceutical business.

The commercial sector is the drug distribution, earning the same money as the courier brother; and a large part of the pharmaceutical business that contributes the bulk of the profit comes from an ancient magical medicine-Cordyceps sinensis. East China is based on Bailing capsules, that is, Cordyceps fungus powder. This product still contributes more than 2 billion yuan in revenue to East China every year.

In addition, East China first imitated the German pharmaceutical company Bayer’s diabetes drug, Acarbose. This drug is a stepping stone for Bayer to enter China, and it provides Bayer with a steady stream of cash flow all year round. In addition to the brand effect of foreign companies, East China also considers the influence of channels-Diabetes and Bailing Capsules are all prescribed from the endocrinology department of the hospital. In this way, the company’s original sales team can continue to reuse and achieve two goals.

So, driven by these two large single products, the company’s revenue and net profit compound growth rate in recent years has been maintained at more than 20%, ROE has also reached more than 20%, and the market value has been rising all the way. With several new products plugged into its product pipeline, it has become a big white horse on par with Hengrui.

However, Hengrui outperformed market changes, but Huadong did not keep up.

Large single-product companies are most afraid of price reductions. After 18 years of centralized procurement, more than 90% of the price drops were suppressed, and the company’s revenue soon became a negative growth. Hengrui spends more than one billion yuan in research and development expenses each year, allowing it to quickly take out new products as substitutes after price reductions. On the other hand, many medicines bought by East China still remain in the laboratory.

Pharmaceuticals are a livelihood industry, and the state’s policy of lowering prices remains unchanged for a long time. Centralized procurement pressure and the company’s own transformation have been slow, making Huadong Medicine’s generic drug product business become the “enemy of time” after 2018, and it also allowed the capital market to vote with its feet. The stock price fell endlessly. Swiss Medicine is in sharp contrast.

But if you are in the pharmaceutical business, the cash flow can be very high, which gives the company the opportunity to buy on a large scale. When Huadong found that it was difficult to make money for patients, it began to make money for women.

Pharmaceuticals are not as good as medical beauty

In fact, at the beginning, Huadong Medicine also wanted to honestly be a “pharmaceutical master”, dedicated to helping the wounded.

In 2019, the company began to continuously develop innovative drugs and generic drugs with high-tech barriers. Judging from the company’s 19-year financial report, the annual R&D expenditure was 1.055 billion yuan, an increase of 49.14% year-on-year, accounting for 10% of the pharmaceutical industry’s revenue. It is important to know that the company’s annual net profit is only 3 billion yuan, and the R&D personnel has rapidly expanded from 550. To 1078.

In October last year, the company announced an exclusive cooperation with Immuno Gen, obtaining the right to develop and sell its ADC products under research in Greater China.. Recently, the company announced that it has signed a strategic cooperation agreement with Provention Bio of the United States to introduce the exclusive clinical development and commercial rights of the bispecific antibody PRV-3279 in Greater China.

Whether it is the ADC at the front or the double antibodies at the back, this is a very cutting-edge thing for the capital market and the people who eat melons. These actions at least prove that Huadong Medicine is catching up with the world’s leading pharmaceutical companies.

In addition, Huadong Medicine has also recently cleaned up and eliminated some generic drugs with low barriers and low commercial value, including projects such as erlotinib and imatinib in the field of anti-tumor, as well as those in the field of super antibiotics. Fidaxomycin tablets and dalbavancin freeze-dried powder injection projects, etc. These are all the “star products” of the past, cutting off innovative drugs that allow East China to focus on high-profit and high-tech content.

However, these are the things that pharmaceutical companies nowadays will do. Huadong Medicine’s advantage is that it has stable business in the past and there is more room for trial and error. From the results, there is no difference in Huadong Medicine. . On the other hand, even for innovative drugs, the situation is not optimistic when medical insurance prices have been reduced in recent years.

Therefore, even though the company’s recent innovative drug transformation actions have continued and the R&D expenses have been continuously increasing, in the short term, its own innovative drug pipeline has slowed down the company’s profit growth rate, and the capital market has not recognized it. However, Huadong’s layout in the field of medical aesthetics has been progressively advanced.

Under the background of the gradual prevalence of the beauty economy, Huadong Medicine won the agent right of Ewan Hyaluronic Acid in China in 2013, and the company began to enter the medical beauty circuit. This product has also brought gratification to the company. In return, in 2018 and 2019, the sales scale and value of the Yiwan Hyaluronic Acid brand ranked first in the domestic market for two consecutive years. The company’s medical beauty business has grown rapidly, with sales reaching 500 million yuan in 2019. Turned nearly five times.

After tasting the sweetness of the golden track of medical beauty, the company immediately accelerated the layout of its medical beauty map.

In 2018, the company acquired Sinclair, a British company that focuses on beauty lines, long-acting microspheres and hyaluronic acid. In 2019, it became a shareholder of R2, an American international medical company. In 20 years, it signed a Chinese agent for botulinum toxin products with Jetema, a listed South Korean company. And acquired the Swedish hyaluronic acid company Kylane. Recently, the company announced the acquisition of Spanish medical equipment company High Tech once again pushed the company to the forefront of the medical aesthetics track.

And these mergers and acquisitions on the medical beauty track have allowed East China to complete the transparency of multiple SKUs.Sodium injections (Perfectha, MaiLi), microsphere-containing injections (Ellánse), embedding thread (Silhouette), botulinum toxin (Jetema The Toxin) and instrument products (pigment regulation) multi-medical product line, comprehensive production This allows the company to have stronger product integration capabilities.

In November last year, the leading medical beauty company, Amic, announced the launch of a clinical plan for a weight-loss drug, liraglutide, and the stock price increased by 14 points that day. But in fact, Huadong Medicine’s similar products had already progressed to clinical phase III at that time, nearly two years faster than Amic, but at that time the company was still hovering in the low-pressure atmosphere brought about by centralized procurement. Until now, the popularity of medical aesthetics is burning. Enough, everyone’s recognition of this company has changed from “East China Medicine” to “East China Medical Beauty”.

The joys and worries of the transformation of medical beauty

Although medical beauty is good, every family has opportunities, but the competition is fierce, and no one has a moat.

On the one hand, the company’s medical aesthetics transformation strategy is still in its infancy, and its revenue share has always been in single digits and its contribution to performance is limited. On the other hand, most of the medical aesthetics businesses acquired by the company are located overseas, and they can be acquired at low prices because their operations have been severely affected under the impact of the epidemic. Last year, the international medical aesthetics business in East China also experienced a decline. The company’s medical aesthetic transformation has actually just started.

Is the path of medical beauty in East China good?

The upstream of medical aesthetics is the pharmaceutical consumables and equipment industry, which has high barriers and strong profitability. At present, overseas companies account for a large market share, and there is a large domestic substitute space; the midstream is a service organization with low concentration, fierce competition, large information gaps, and low profitability, mainly relying on channels; while downstream channels mainly rely on drainage organizations , Incline to the medical beauty vertical platform, and the head company has a rapid growth rate.

So although the domestic medical beauty market is advancing rapidly at a compound growth rate of 24.2% every year, the majority of profits are on the one hand in front-end equipment production and on the other hand in terminal brands. As a manufacturer, Huadong Medicine barely occupies a good industrial position.

On the other hand, the beauty of medicineSo it is called medical beauty because it still operates in the system of pharmaceutical products.

Hyaluronic acid, thread embedding, etc. belong to three types of medical devices, and botulinum toxin is a biological product. These are all managed by the Food and Drug Administration of the China Food and Drug Administration, and have strict clinical trials and approval systems. In addition to the company’s technical strength, there are clinical resources that are tested behind this: the company needs doctors from all regions to lead the clinical trials of its own products and endorse their products.

This requires the company’s long-term clinical accumulation, which is one of the basic skills of pharmaceutical companies, which can determine the speed of product launch and market share changes. As a long-established pharmaceutical company, Huadong Medicine has a more mature pharmaceutical industry system compared to other medical beauty companies, making it easier to run through the entire process and carry out large-scale replication.

For channel vendors, the circulation logic of medical aesthetics products is similar to that of medicines: hold product launch meetings, recruit experts for product use training, regularly visit doctors to collect product use feedback, and continue to promote them. This is the mainstream circulation method that the pharmaceutical industry has been advocating for more than 30 years.

Therefore, East China has the background that other medical beauty companies do not have, and it also has the first-mover advantage that other medical companies do not have. This is the unique place in East China’s transformation of medical beauty.

Ending

After 2015, when innovative drugs were on fire, East China was actively deploying new product pipelines. In recent years, the beauty economy has prevailed, and East China has also set foot in the field of medical beauty. The same is pursuing new concepts, but the former is still at least making medicine, and no matter how exaggerated its medical properties are, the latter is still a bit unfair. In the future, how the medical beauty business and the pharmaceutical industry will allocate energy and resources, and whether they can collaborate with each other is an unknown.

Although historically, there have been many pharmaceutical companies that “do not do business properly”. Among them, the highest status is Allergan, a medical empire created by the Chinese through acquisitions. Before it was acquired by the pharmaceutical giant AbbVie, it was once ranked. It has reached the 18th place among the world’s TOP pharmaceutical companies, leaving a dozen streets behind Hengrui Fosun.

Looking at domestic listed pharmaceutical companies, Yunnan Baiyao is also not doing business properly. After not wanting to sell medicines at ease, Yunnan Baiyao began to deploy in the daily chemical industry, launching toothpaste, shampoo and even wanted to get a share of the tourism and vacation industry.

Although Yunnan Baiyao’s business development strategy does not have many successful products except toothpaste, band-aids and other products, at least it caused a sensation when the transformation was announced at that time, and it was considered a good result (in fact, Yunnan Baiyao). Baiyao is now the industry leader), and whether it is Yunnan Baiyao or Allergan, it is a development strategy of the company to do business properly.

As for Huadong Medicine, both the generic drug business and the innovative drug business are affected by the price reduction policy to varying degrees. Transformation of medical beauty is more of a helpless choice under the unprecedented pressure of an increasingly aging population and the unprecedented pressure of medical insurance control fees.

Pharmaceutical companies do because of revenue pressureThere is nothing wrong with the consumer business, but if more and more pharmaceutical companies come to make consumer products, who will produce good medicines that are affordable and useful to the people in the future is a question that everyone has to consider after the market heats away.

References:

[1] The layout of the non-surgical product line is complete, and the medical beauty business needs to take off urgently. GF Securities

[2] The era of “value economy” is coming, medical beauty business stimulates the company’s new vitality, Huachuang Securities