30 VC / PE background enterprises listed on the Hong Kong stock market performance of IPO eye-catching

Editor’s note: This article is from the micro-channel public number “Beyond the J-curve” (ID: beyondthejcurve), Author: Beyond the J curve.

Core discovery

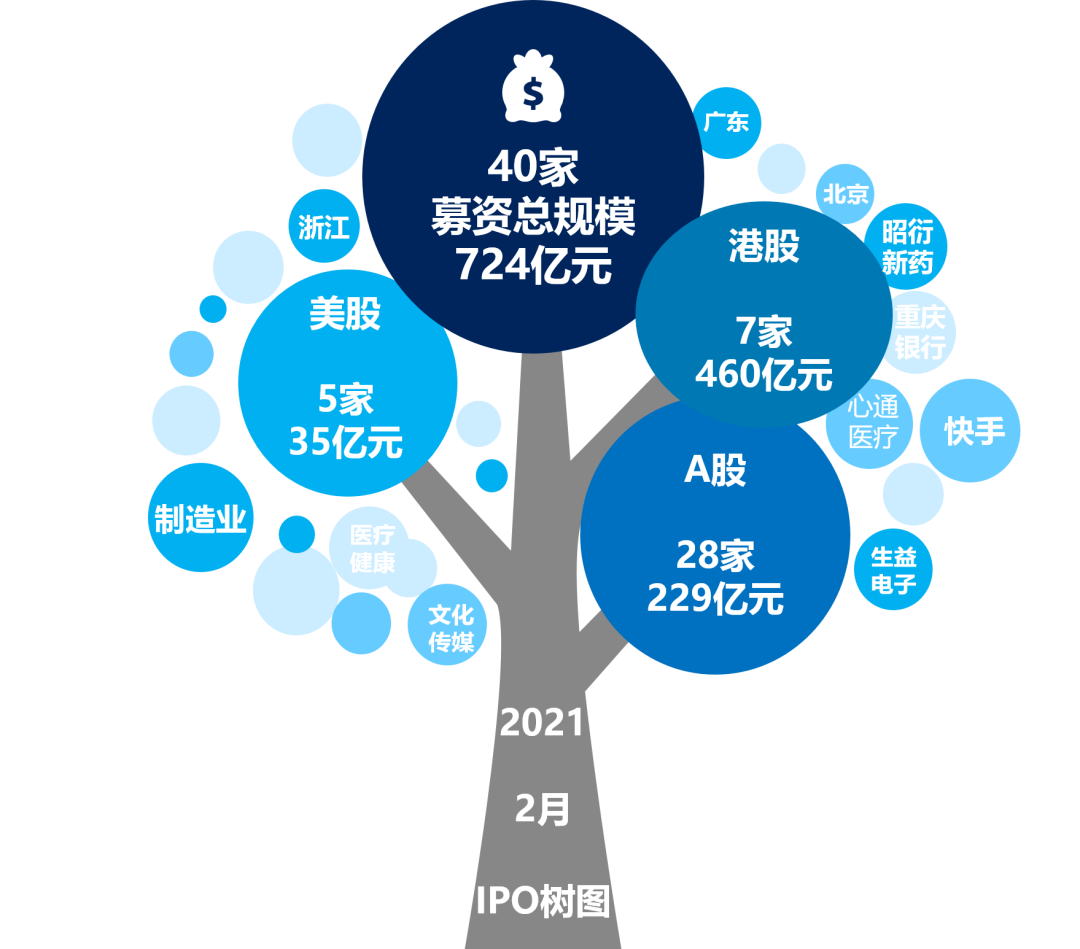

In February 2021, a total of 40 Chinese companies successfully IPO in A-shares, Hong Kong stocks and US stocks, and the number of IPOs in the global market increased year-on-year

The IPO penetration rate of VC/PE institutions reached 75%, and the IPO book exit return was as high as 238.7 billion yuan, of which kuaishou contributed nearly 90%, and the average book return doubled year-on-year

The top ten IPO projects of fundraising scale are all above 1.5 billion yuan, and the top ten IPO projects of the day’s market value are all above 10 billion yuan, and Kaishou has a daily market value of 1.028.684 billion yuan. Top of the list

Part 1: Analysis of IPO market by Chinese companies

In February 2021, a total of 40 Chinese companies successfully IPO in A-shares, Hong Kong stocks and U.S. stocks, raising a total of 72.4 billion yuan; the top 5 companies in terms of IPO funds raised this month are Kuaishou, Zhaoyan New Medicine, Bank of Chongqing, Xintong Medical and Shengyi Electronics; IPOs are concentrated in cultural media, medical and health, and manufacturing industries; IPOs are concentrated in Guangdong, Zhejiang, and Beijing. (See Figure 1)

Figure 1 Overview of the IPO in February 2021

▼The number of Chinese IPOs in the global market has increased year-on-year

In February 2021, a total of 40 Chinese companies successfully IPOs in A shares, Hong Kong stocks and US stocks. The number of IPOs increased by 33.33% year-on-year and decreased by 24.53% month-on-month; the total amount of funds raised was 72.4 billion yuan, and the IPO scale increased by 1.38 times year-on-year, month-on-month. An increase of 64.55%. A-share market-this month the Mainland has become the market with the largest number of IPOs in the global capital market, accounting for 70% of the global IPO volume this month; Hong Kong stock market-this month Hong Kong has become the market with the highest IPO fundraising scale in the global capital market this month, accounting for the global market this month 64% of the IPO scale, the largest fundraiser this monthProject-Kuaishou (01024.HK); US stock market-A total of 5 Chinese companies went public in the US this month. (See Figure 2, Table 1)

Figure 2 The scale and number of IPOs of Chinese companies in the global market from February 2020 to February 2021

Table 1 Statistics on the number and scale of IPOs in each trading sector in February 2021

▼A-share market slows down the issuance of new shares

In February 2021, a total of 28 Chinese companies made IPOs on the Shanghai and Shenzhen stock exchanges. The number of IPOs increased by 27.27% year-on-year and decreased by 15.15% month-on-month; the amount of funds raised totaled 22.9 billion yuan, and the IPO scale decreased by 13.26% year-on-year and 6.91 month-on-month. %. There were 10 IPOs on the Growth Enterprise Market of Shenzhen Stock Exchange this month, making it the largest IPO sector in the A-share market; the main board of the Shanghai Stock Exchange raised 9.292 billion yuan, making it the largest IPO sector in the A-share market. It is worth noting that the IPO review has become more stringent and the pace of issuance has slowed down significantly. On February 5, the China Securities Regulatory Commission issued the “Guidelines for the Application of Regulatory Rules-Disclosure of Information on Shareholders of Companies Applying for Initial Listings”, which focused on strengthening the supervision of shareholders of companies that intend to IPO .

This month, the China Securities Regulatory Commission reviewed and approved 18 IPO registrations on the Sci-tech Innovation Board, 1 suspended (other matters) audit, and 9 terminated audits. As of January, the number of listed companies on the Sci-tech Innovation Board reached 232. (See Figure 3 and Table 2)

Figure 3 February 2020-February 2021 A-share market Chinese companies IPO scale and number

Table 2 TOP5 Chinese companies’ A-share market fundraising in February 2021

▼The IPO medical and health stocks in the Hong Kong stock market performed well

In February 2021, 7 Chinese companies made IPOs in Hong Kong, all listed on the main board of the Hong Kong Stock Exchange. Medical and health companies accounted for 5 seats. The number of IPOs increased by 5 compared with the same period last year. The total amount of funds raised was 46 billion yuan. The IPO scale increased by 4.68 times from the previous month. Among them, the much-watched “short video first share” Kuaishou (01024.HK) has an absolute advantage with a fundraising scale of 35.056 billion yuan. In addition, medical and health companies have performed well, such as Zhaoyan New Drug (06127.HK). ) Became the fourth “A+H” CRO company in China. (See Figure 4, Table 3)

Figure 4 The scale and number of IPOs of Chinese companies in the Hong Kong stock market from February 2020 to February 2021

Table 3 TOP5 Chinese companies raising funds in the Hong Kong stock market in February 2021

▼The IPO boom of Chinese companies in the U.S. stock market continues

In February 2021, a total of 5 Chinese companies IPO in the US capital market, the number of IPOs decreased by 2 compared with the previous month; the total amount of funds raised was 3.5 billion yuan, and the IPO scale decreased by 7.89% year-on-year and 68.75% month-on-month. On the whole, although the number of IPOs has declined, popular companies such as Tuhu’s car, Dingdong Foods, and Didi Chuan have all reported IPOs in the United States, and the IPO boom of Chinese companies in the United States continues. (See Figure 5, Table 4)

Figure 5 The size and number of IPOs of Chinese companies in the U.S. stock market from February 2020 to February 2021

Table 4 TOP5 US stock market fundraising by Chinese companies in February 2021

Part 2 Analysis of IPO exit of Chinese companies

▼The IPO penetration rate of VC/PE institutions is as high as 75%

In February 2021, a total of 30 Chinese companies with VC/PE backgrounds will be listed. The IPO penetration rate of VC/PE institutions is 75%. Except for the Nasdaq exchange, the penetration rate of VC/PE in other trading sectors All are above 70%. VC/PE Institution I of the MonthHealth and manufacturing companies rank in the top three in IPO fundraising, accounting for 80.68% of the total funds raised in various industries. Among them, manufacturing companies have 11 corporate IPOs this month, which is the industry with the largest number of IPOs this month; cultural media Due to the outstanding performance of Kuaishou, the company has become the industry with the largest IPO scale this month, and the number of IPOs of medical and health companies ranks second. (See Figure 7, Table 7)

Figure 7 Industry distribution of IPO projects in February 2021

Table 7 IPO key industry segmentation statistics for February 2021

▼The most IPO attracting money in Beijing

In February 2021, the number of IPOs of Chinese companies in Beijing, Guangdong, and Zhejiang were all 7, and the number of IPOs ranked first; the scale of IPOs of Chinese companies in Beijing reached 44.652 billion yuan, accounting for 62% of the total IPO funds raised this month , Ranked first, Guangdong and Zhejiang ranked second and third respectively. (See Figure 8, Table 8)

Figure 8 The number of IPOs and the regional distribution of funds raised by Chinese companies in February 2021/p>

Note: The sum of IPO quantity distribution ratio (left) and scale ratio (right) are not due to rounding of “1”.

Table 8 The number of IPOs and the regional distribution of fundraising scale of Chinese companies in February 2021

Part 4 Key IPO cases of Chinese companies

In February 2021, the top ten IPO projects with fund-raising scale were all over 1.5 billion yuan, accounting for 78% of the total fund-raising in February. Among them, medical and health companies accounted for four seats. The top ten IPO projects with a market value of more than 10 billion yuan on the day of the IPO, and Kuaishou ranked first with a market value of 1.028.684 billion yuan on the day.

▼The IPO scale of Chinese companies and the TOP10 market value of the day

The table below shows the TOP10 IPO funds raised by Chinese companies in February 2021. (See Table 9, Table 10)

Table 9 TOP10 IPO scales of Chinese companies in February 2021

Table 10 2021 2TOP10 market capitalization on the day of IPO of Chinese companies in the month

▼Key Case: Kuaishou

Part 5 Review of policy hot spots

On February 5, Pi Liuyi, Deputy Director of the Market Department of the China Securities Regulatory Commission, stated that the merger of the Shenzhen Stock Exchange’s main board and the small and medium-sized board is an important measure to comprehensively deepen the reform of the capital market, as an important part of my country’s multi-level capital market system. The main board of the Shenzhen Stock Exchange and the SME board have played an active role in expanding direct financing, serving the real economy, and supporting small and medium-sized enterprises.

On February 5th, the China Securities Regulatory Commission issued the “Guidelines for the Application of Regulatory Rules—Regarding Application for Disclosure of Information Disclosure of Shareholders of Listed Companies”, requiring that issuers applying for initial public offerings or depositary receipts should follow these guidelines to fully complete shareholder information Disclosure and other related work.

1. The issuer shall disclose shareholder information in a true, accurate and complete manner. If the issuer’s history of stock holdings exists, it shall be terminated in accordance with the law before submitting the application, and the reasons for formation and evolution shall be disclosed in the prospectus , Dissolution process, whether there are disputes or potential disputes, etc.

2. The issuer shall issue a special undertaking when submitting the application materials, stating whether the issuer’s shareholders have the following circumstances, and disclose the undertaking to the public: (1) Laws and regulations prohibit the entity holding shares from directly or indirectly holding the issuance (2) The issuer’s shares are directly or indirectly held by the intermediary institution or its responsible persons, senior managers, and handlers of the issuance; (3) The issuer’s equity is used for improper transfer of benefits.

3. If the issuer submits an application for new shareholders within 12 months, it shall fully disclose in the prospectus the basic information of the new shareholder, the reason for the share purchase, the share price and the pricing basis, the new shareholder and the issuer’s other shareholders, Whether the directors, supervisors, and senior executives have an associated relationship, whether the new shareholder has an associated relationship with the intermediary institution and its responsible person, senior management, and handlers of the issuance, and whether the new shareholder has a proxy holding situation.

The above-mentioned newly-increased shareholders shall undertake that the newly-increased shares held by them shall not be transferred within 36 months from the date of acquisition.

4. If the transaction price of the issuer’s natural person shareholder’s share purchase is obviously abnormal, the intermediary institution shall check the basic information of the shareholder, the share purchase background and other information, and explain whether there is any situation in the first and second items of these guidelines. The issuer shall explain the basic information of the natural person shareholder.

5. If the shareholding structure of the issuer’s shareholder is two or more tiers and is a company or limited partnership with no actual business operations, if the shareholder’s share transaction price is obviously abnormal, the intermediary institution shall thoroughly check the shareholder’s level The final holder, explain whether there are any of the first and second items of this guideline. If the ultimate holder is a natural person, the issuer shall explain the basic information of the natural person.

6. Where financial products such as private equity investment funds hold the issuer’s shares, the issuer shall disclose the supervision of the financial products.

7. The issuer and its shareholders shall provide real, accurate and complete information to the intermediary in a timely manner, actively and fully cooperate with the intermediary in conducting due diligence, and fulfill the obligation of information disclosure in accordance with the law.

8. Sponsor institutions, securities service institutions and other intermediary institutions shall be diligent and responsible, and verify the shareholder information disclosed by the issuer in accordance with the requirements of these guidelines. The verification opinions issued by intermediary agencies cannot simply be based on the commitments of relevant institutions or individuals. They should comprehensively and in-depth verify objective evidence including but not limited to shareholder agreement, transaction consideration, source of funds, payment methods, etc., to ensure that the documents issued are true, accurate and complete .

9. Shareholders increased by the issuer through collective bidding and continuous bidding transactions during the period when the issuer is listed on the National SME Share Transfer System, listed on overseas stock exchanges, and because of inheritance, enforcement of court judgments or arbitration awards, and enforcement of national laws and policies Shareholders who require or are led by people’s governments at the provincial level and above to obtain the issuer’s shares may apply for exemption from the verification and share lock-up requirements of these guidelines.

10. If the issuer’s shareholders are suspected of illegal share purchases or obvious abnormal trading prices of the shares, the CSRC and stock exchanges may require relevant shareholders to report their basic information, background of the shareholding, etc., and require anti-money laundering management and anti-corruption requirements. Solicit opinions from relevant departments and jointly strengthen supervision.

11. These guidelines will be implemented from the date of issuance. Companies that have accepted the application before the date of publication do not apply to the share lock-up requirement in Item 3 of these Guidelines.