After the European debt crisis, the euro zone is retaking the path of German structural adjustment after the Internet bubble in 2000, but it is based on global imbalances.

The euro area after the European debt crisis = Germany after the IT bubble?

After 2000, Germany entered a time of balance sheet recession, domestic demand growth stagnated, savings rate increased, investment rate fell, fiscal consolidation, current account surplus and The scale of capital outflows has expanded, and its conflicts with the balance sheet cycles of other countries in the euro area have exacerbated the imbalances in the balance of payments within the euro area-Germany is a surplus country, other countries are deficit countries; German capital providers, other countries’ capital needs Fang; superimposed on loose monetary policy and capital inflows, the trend of economic bubbles in peripheral countries has intensified. With the outbreak of the American financial crisis, the European real estate bubble burst.

After the financial crisis, the German authorities recognized the imbalances caused by the German model. At the same time, they also recognized that the response to the economic crisis requires concerted action, otherwise the situation of beggar-thy-neighbor may occur, repeating itself The tragedy during the Great Depression led to the disintegration of the Eurozone and the rise of extremist forces, and even triggered geopolitical disputes.

In May 2010, the euro zone realized the importance of fiscal coordination and decided to promote “fiscal consolidation” and reached a fiscal treaty in 2012 (Fiscal Compact), to extend Germany’s debt break mechanism to the entire Eurozone. It stipulates that in almost any case, the governments of the euro zone should maintain a fiscal balance. The issuance of public debt requires the consent of other countries, and countries that violate the regulations will be punished. Since then, the fiscal deficit rate of the Eurozone countries has continued to decrease, and has been reduced to less than -1% in 2018. Greece, the initiator of the European debt crisis, even turned into a surplus in 2016.

The euro zone government leverage ratio reached its peak in 2013 and then slowly declined. At the same time, residents and non-financial companies still maintain surpluses, and deleveraging continues to advance. Corresponding to this is the net outflow of the capital account and the current account surplus.

Germany is still the largest trade surplus country in Europe, but its trade balance with other countries in the Eurozone has been balanced. In the first quarter of 2009, Germany’s trade surplus fell to a trough (US$360), and then continued to rebound. In the second quarter of 2016, it rose to 80 billion, which was the same as the 820 billion before the 2008 financial crisis.100 million flat. Later, under the influence of reverse globalization, it has fallen to US$62 billion in the fourth quarter of 2019. Since the beginning of 2012, the euro zone’s contribution to Germany’s trade surplus has fallen below 10%. The average contribution rate from 2012 to 2019 was only 2%. Since the third quarter of 2018, there has even been a deficit.

Developed economies are still the main source of Germany’s trade surplus. The United States, the United Kingdom and France are at the forefront, and Germany’s trade with other eurozone countries is basically balanced. Before the financial crisis, the quarterly peak of Germany’s trade surplus with the United States was about 15 billion U.S. dollars. It broke the previous high in 2012, and the quarterly average from 2015 to the present is about 19 billion U.S. dollars, with a contribution rate of about 30%. Germany’s trade surplus with emerging and developing economies has been rising as a whole, with a quarterly average of approximately US$20 billion. Among them, the surplus with emerging and developing economies in Europe is declining, and the surplus with emerging and developing economies in Asia turned from negative to positive in 2011. The most important change comes from China. If China is deducted, Germany’s trade balance with other emerging and developing economies in Asia is in deficit.

Before the 2008 financial crisis, the balance of payments in the Eurozone was generally balanced, but the internal structure was basically that Germany’s surplus was affected by the European debt crisis. The deficit is offset. After the financial crisis, Germany’s total surplus decreased slightly, and more importantly, the source of the surplus has shifted from the Eurozone to the United States. At the same time, after fiscal consolidation and social welfare system reforms, the countries in which the debt crisis occurred in Europe have turned from deficits to surpluses. As a result, the Eurozone’s international balance of payments has shifted from a basic balance to a large surplus. In 2011, it was close to 100 billion euros, the peak of this century; it has been above 200 billion since 2012, and it has exceeded 300 billion for four consecutive years since 2016. It accounts for more than 3% of Eurozone GDP (Figure 1).

Figure 1: The balance of payments in the Eurozone has improved significantly. Data: IMF, CEIC; Orient Securities

All turn to positive values. Since the end of 2017, the GDP growth rate in the Eurozone has slowed down. One of the reasons is the significant decline in net exports. As a buffer, government departments have expanded countercyclical adjustments. The German government’s surplus has narrowed, and other Eurozone countries have had deficit rates. Improved. Affected by the new crown pneumonia epidemic, external demand and domestic private sector demand plummeted, the European Commission passed a 750 billion euro fiscal stimulus package, which boosted market expectations for European economic recovery. Not only because of the fiscal stimulus itself, but also because of the speed of action and consistency of opinions of EU member states. It opens up imagination space for future integration prospects such as finance.

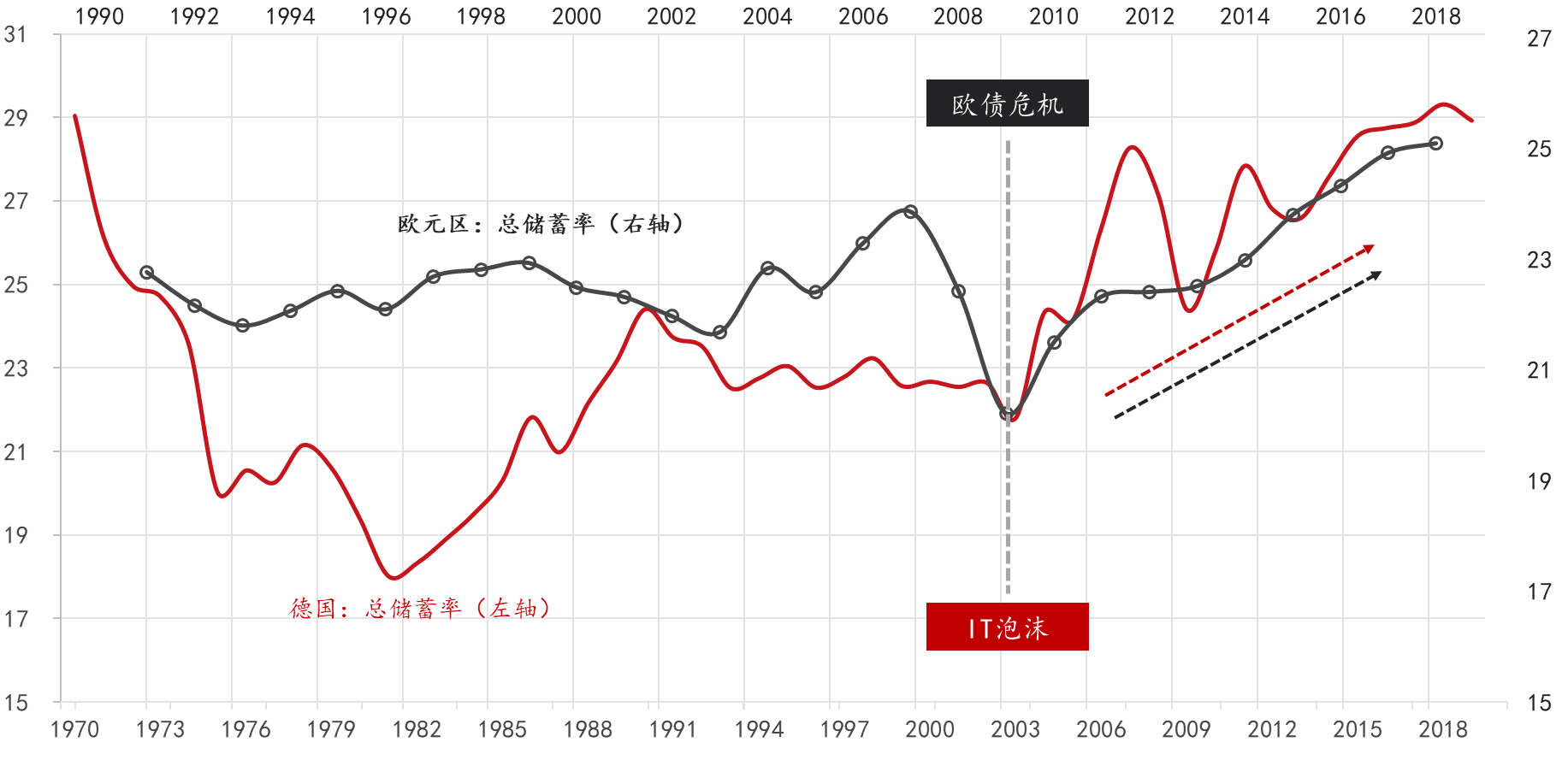

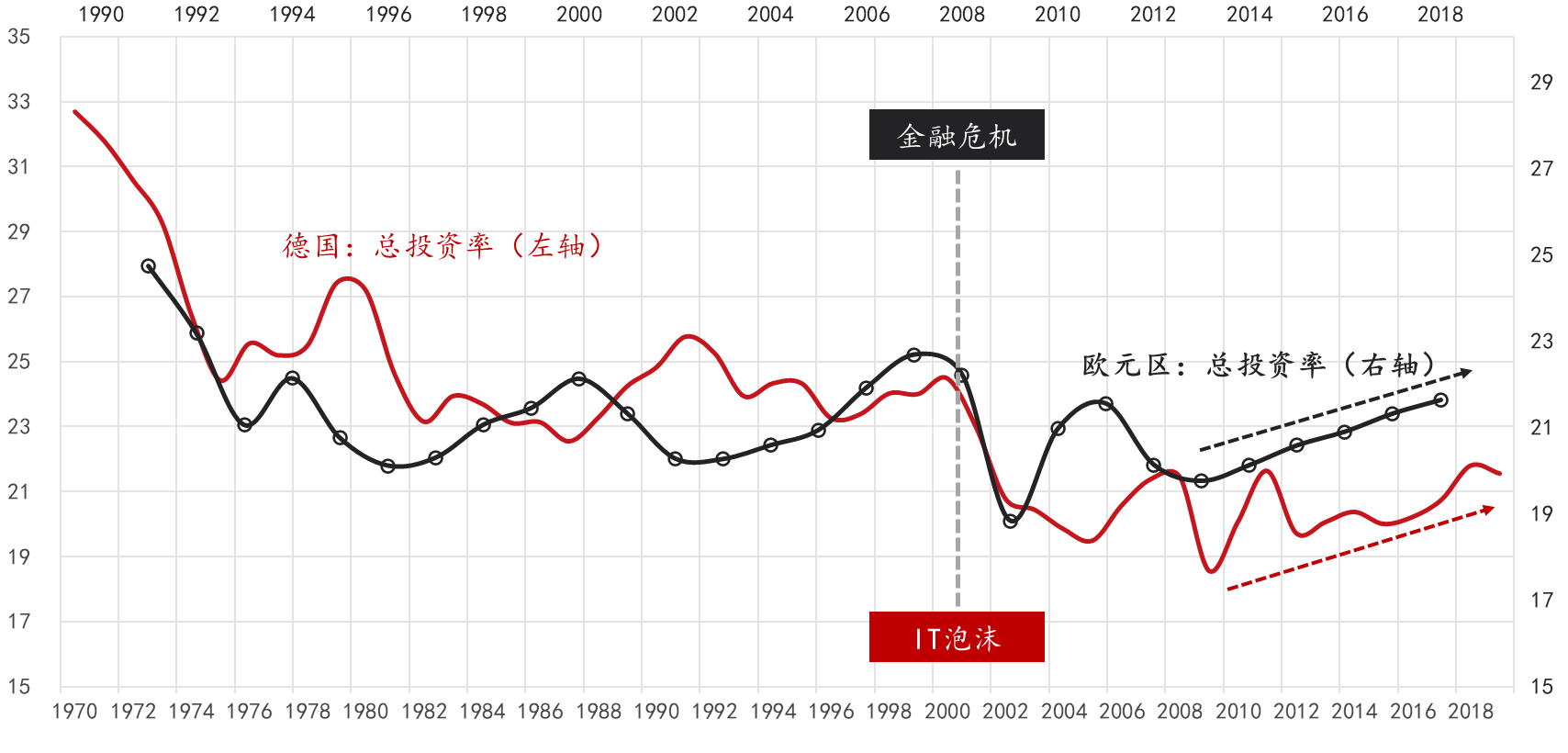

The cycle of the Eurozone is about 8-10 years away from that of Germany. The Eurozone after the financial crisis (or the European debt crisis) is like Germany after the Internet bubble ( Figure 3-6). The current account surplus continued; the total savings rate entered an upward channel and reached its peak in nearly half a century; investment took the lead in falling and then rising, reversing the long-term downward trend; the unemployment rate first went up and then down, the trend was highly consistent, and the turning points appeared in the crisis. 5 years later. Comparing the slopes of the savings rate and the investment rate, we can see that the slope of savings is steeper, which is consistent with the current account’s transition from a deficit to a surplus.

Figure 3: Dislocation of the current account cycle (10 years)

Figure 4: Dislocation of the savings cycle (10 years)

Figure 5: Dislocation of the investment cycle (8 years)

Figure 8: German double loop Trends (from the perspective of demographic structure) Data source: United Nations, CEIC, WIND, Orient Securities

Description: Producers/consumers are the ratio of the working-age population of 15-64 years old to the population of other ages. The inflection point means the aging of the population.

/p>Since the 1990s, in different periods of time, almost all catching-up economies have maintained a long-term balance of payments surplus. In other words, domestic demand has been in a state of repression for a long time. The reason is nothing more than that. Financial repression, slow wage growth, increased polarization between rich and poor, and accumulation of debt, etc. The demand side of the United States has also been suppressed, but it can rely on the issuance of US dollars to absorb the excess production capacity of other countries. In 2019, the global merchandise trade deficit The total amount is about 2.1 trillion US dollars, and the US accounts for 0.85 trillion, accounting for 40%. Among them, the US’s bilateral deficit with China (including Hong Kong) is about 0.32 trillion, accounting for 37%, which is 6 percentage points lower than in 2015. On the contrary, the U.S. trade deficit with the Eurozone has continued to widen. It was 54 billion in 2009 and increased to 160 billion in 2019, and its share increased from 9% to 19%. Among them, the deficit with Germany widened from 29 billion to 19%. 67 billion.

In the medium term, the U.S. dollar’s hegemony is still irreplaceable, but how long can the United States issue U.S. dollars to make up for the lack of effective global demand for games? The Bretton Woods system has been Disintegration, but the predicament still exists, that is, the “Triffin Dilemma.” The trade deficit is not only a condition for maintaining the hegemony of the U.S. dollar, but at the same time it will erode the foundation of hegemony. Under the current international monetary system, global trade imbalances are difficult to solve, but they are It is possible to control within a reasonable boundary. This requires that the major surplus countries of the United States no longer achieve trade surpluses by suppressing domestic demand. Since Trump took office, the US current account deficit (as a proportion of GDP) has begun at the end of 2017 Narrowing, the current account surplus in the euro zone began to shrink, the pull of net exports to GDP peaked and fell in the second quarter of 2018 (refer to Figure 2.12), and the contribution rate of domestic final consumption slowly increased. These new changes have helped alleviate the situation. Global imbalances.

The establishment of the Eurozone has always been regarded as a political act, but its normal operation cannot rely solely on political will. The agreement requires member states to maintain production factors and products. Completely free flow, which requires member states to converge on economic indicators such as prices, fiscal deficits, debt leverage, and long-term interest rates-all of which are the European Central Bank’s “Convergence Report”