What other subdivisions have hidden opportunities.

Editor’s note: This article from the public micro-channel number ” grape game “(ID: youxiputao) , author: Andrew.

Domestic mobile games are in full bloom in overseas markets.

In mature markets such as the United States, the revenue level of domestic mobile games has seen a visible increase; in emerging markets such as Southeast Asia and Latin America, domestic mobile games have shown significant advantages in download volume and user possession.

ChinaJoy (hereinafter referred to as CJ), Google Google and App Annie jointly released the “2019 China Mobile Games Depth Insight Report”, in which multiple dimensions of data are confirming the results of domestic mobile games.

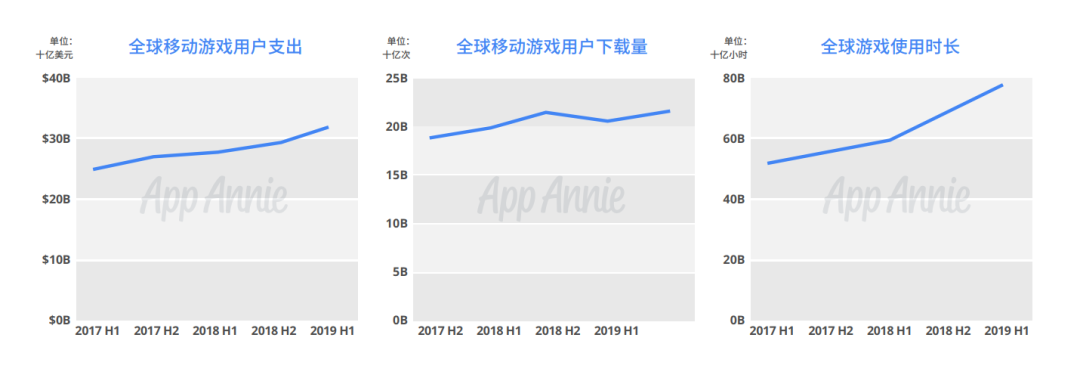

First, although the growth in user downloads in developed regions tends to be flat, the global mobile gaming market has maintained a strong rise in terms of consumption levels and user usage. In other words, the total number of mobile game users has almost stabilized, but their investment in the game is gradually increasing, which is an opportunity for many manufacturers and products to take advantage of.

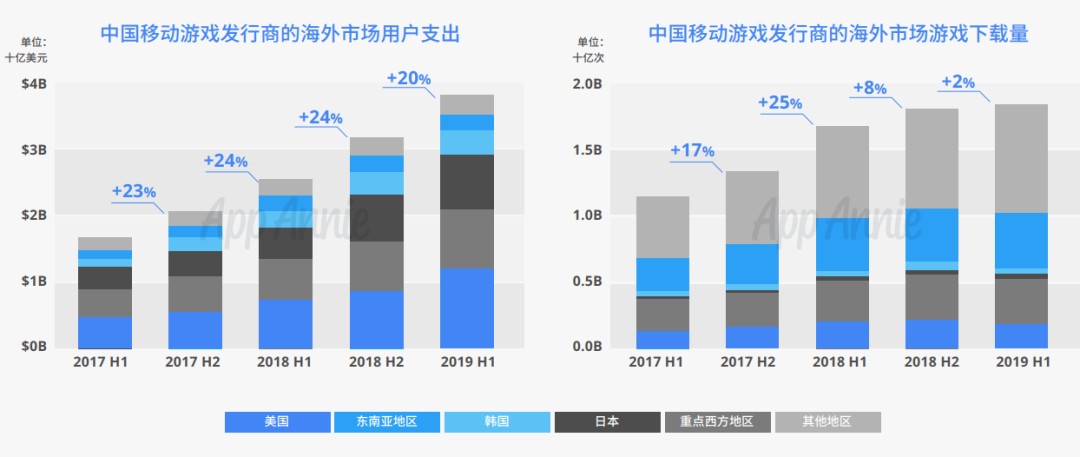

Secondly, the profitability of domestic mobile games in mature markets such as the US is also improving. In the first half of 2019, overseas sales of domestic mobile game users accounted for 16% of the total, up 60% from the same period in 2017. From this point of view, for domestic distributors and products, the macro concept of “overseas region” is still a potential market. In addition, in some emerging markets, domestic publishers are in a leading position in terms of product downloads and user acquisition.

Overseas manufacturers’ overseas user spending increased by 60%,mainly from mature markets

Overall, the opportunities for domestic manufacturers to earn revenue in overseas markets are mainly from the growth of countries such as the United States, Japan and South Korea.

Although the mainstream view is that the competition in mature markets such as the United States is fierce, they still maintain a low growth rate and become the region that contributes the most to the domestic product distribution income.

In the first half of 2019, in the US and Europe, the United States was the market with the highest spending on game users, and its user spending reached 8.29 billion US dollars, which still maintained a good growth rate (24%). Japan and South Korea are close behind.

In emerging markets such as India, Brazil and Russia, domestic publishers have a clear advantage in market share, and user spending in these regions is growing rapidly, with India growing at an annual rate of 110% and Russia’s annual growth at 73. %. But these Emerging markets were not big enough, so they did not show strong competitiveness in their revenue contribution.

In summary, the domestic publishers’ income overseas is still more dependent on mature markets such as the US. Domestic mobile games account for a small market share in these regions, and they also face competitive pressures from manufacturers such as the US, Japan and South Korea. For example, the local publishers in the Korean market accounted for 64% of the revenue, while Japan accounted for 78%. But the user spending of domestic mobile games in these mature markets is also growing rapidly. According to the “2019 China Mobile Games In-depth Insight Report”, this year’s first year of this year increased by 51%.

In addition, if you look closely at these macro-level prosperity, you can also find some details that are not easy to notice.

New liquidation trends are emerging

For example, in terms of income composition, many foreign publishers’ products have chosen a hybrid cashing model in terms of payment, which can be used for domestic seafood products. In the developed regions such as the United Kingdom and the United States, although the cost of passengers has risen, in addition to the few directions that domestic manufacturers are best at, the income potential of other categories is rising. The key lies in how to do themes and categories. Differentiation.

These are nowLike some intrinsic routines, cognitive changes, and the formation of previously overlooked opportunities in overseas markets, from these points spread, perhaps the next stage, new growth space in the sea business .

The bonus of the “previous generation” to play in the sea is gradually weakening

From the perspective of the income distribution of categories, domestic distributors can achieve considerable results overseas, especially in Europe and the United States, from the inertia of some key markets. This part of the market is mature and the user pays higher level, which is usually the key target of domestic publishers. In the first half of 2019, domestic publishers’ overseas user spending increased by 20%, and the main growth was also driven by the earnings of these mature markets.

A few years ago, in the typical market such as the United States, the category with the strongest income performance was undoubtedly SLG (strategy). This is a category that domestic publishers are very good at and one of the most significant categories of revenue-generating results.

Opening the app stores in the UK, the US and other regional markets, Top 10 to Top 50 and even Top 100, SLG is basically one of the most severe types seen. Therefore, in the past 3 to 5 years, the domestically produced mobile games have outstanding achievements, and many of them are similar to the mature SLGs in Europe and America. They are frequent visitors to the top 50 of the best-selling list. SLG single-user value is high, usually with longer-term retention and payment. This is an industry consensus that has not been broken before.

But this consensus is facing challenges.

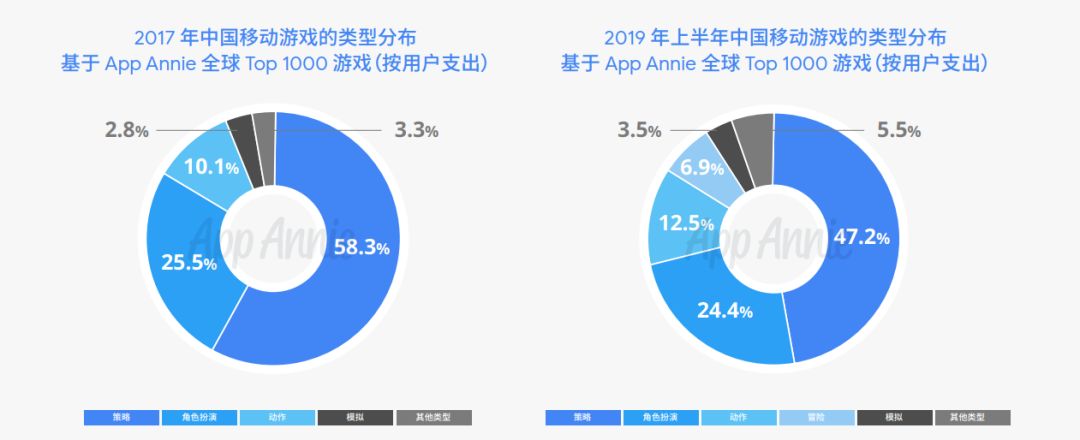

Open the current app store list, although the number of SLGs in the head and waist echelons is still quite large, but its dominance is weakening. On the one hand, the number of distributions in the forefront of the best-selling list has declined; on the other hand, according to the statistics of the “2019 China Mobile Games In-depth Insight Report”, compared to two years ago, the income of SLG games in the Top 1000 is also visible. Sliding down.

From 2017 to 2019, the distribution of strategy classes is gradually decreasing

The 2019 China Mobile Game Depth Insight Report mentions that in the United States, Germany and other regionsIn the market, the strategy category is still a strong category for domestic publishers, and future growth potential may be more biased towards action adventure, role playing and casual play.

New category opportunities

In the US market, user spending in both strategy and action categories has dropped significantly

In overseas markets, the distribution of categories is changing quietly.

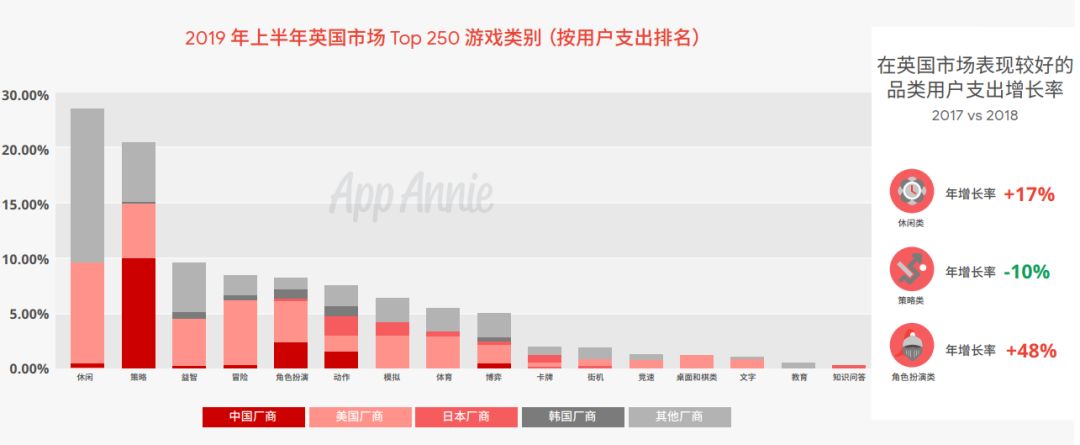

From the largest US market, from 2017 to 2018SLG user spending has dropped significantly, spending is substantial The rise is casual and role-playing. The situation in the United States can largely represent the markets of some developed countries in Europe and America, such as the United Kingdom and Germany.

British market, role-playing user spending has risen dramatically

This is not difficult to understand. We have had the same analysis before. In the past two years, with the further expansion of the total number of users brought by mobile games, more and more casual and casual audiences have been brought. A large number of leisure products enter the head ladder.

Several casual games released by some European and American manufacturers often occupy the top 5 of the free list. There are also several typical manufacturers in China. There are also several fist products in the segment of super leisure, but they do not form a category cluster like SLG. . The head of this category can get hundreds of millions of downloads in a matter of months to a year, and can earn income mainly through advertising.

The user spending of role-playing games has increased significantly in Russia.

In the role-playing direction, we have recently observed some long-term operating products of RPG theme. In the future, we are gradually entering the top 50 of the best-selling list in the app store. The commercial model of such products is good at domestic manufacturers. It is only more advantageous in the integration of subject matter and category. These are the types of domestic publishers who have been less involved in the past, and have shown potential in mature markets such as the US and emerging markets such as Russia.

Of course, the original superior categories such as SLG are not stagnant. There are still some differences in the mature market based on the differences in subject matter and expressiveness. App Annie’s daily overseas income reports often see SLG products from domestic publishers, and established advantages by theme and style. The focus is on the publisher presenting the game according to what the local player likes. This is the reason why in the past one or two years, after the domestic distributor’s SLG products have occupied the North American market, the follow-up products can still stand out from a large number of competing products.

New trends in rapid adoption

In addition to the weakening of SLG’s dominance in the distribution of categories, some of the original cognitions are also suffering from the business model. The emergence of some new forms has expanded more possibilities.

Because of the fact that the previous products were mostly heavy products, and the fact that domestic manufacturers are better at buying free games, the past the domestic products are all in the in-app payment.

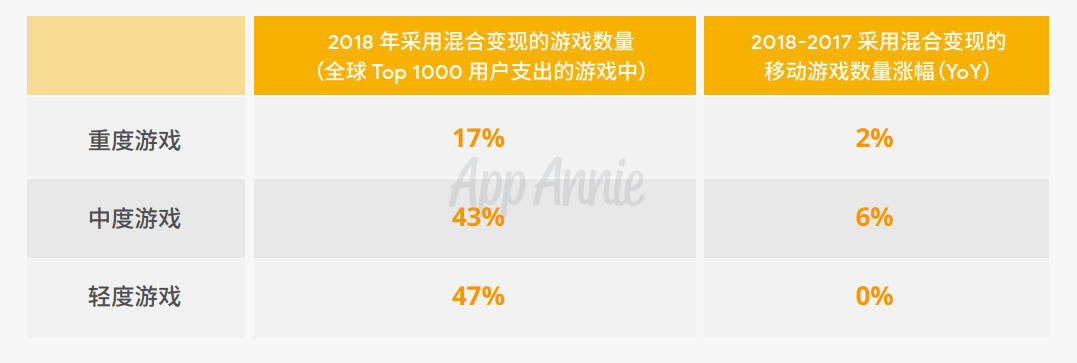

But if you expand your perspective to more advanced mobile gamefronts, you’ll find that mixing and monetizing is becoming the choice of more products. Many games are in addition to user spending, with additional advertising revenue as a revenue supplement, or a subscription-based payment. Among the overseas products with Top 1000, the choice of hybrid cashing method reached 34%, while the proportion of domestic mobile games was only 15%.

According to traditional cognition, the first reaction may be “this is the play of casual games.” But the diversified revenue model is not exclusive to casual categories, 17% of heavy games, and 43% of moderate games, have adopted a hybrid approach. At the same time, this proportion also shows a growing trend.

In the hybrid realisation mode, the more representative ones are subscription payment + in-app purchase + advertisingRealize. At the Google Google Think Games 2019 Game Summit this year, Deng Hui, vice president of the game industry at Google’s Google China Big Clients Department, mentioned that since 2016, the number of game-enabled pay-per-view players has increased by an average of 70% per year. In 2018, games with in-app purchase + traffic monetization increased by 34% compared to last year.

Subscription payment is a business model that many manufacturers are trying. From the host platform to the mobile terminal, they all have their own practical directions. This year, many overseas application stores and platforms have also announced the platform subscription payment scheme. . Previously, subscription services in some game products were often purchased within the mainstream free game, a monthly deductible purchase. Giving the player some extra items, or gains in output, is usually more likely to stimulate small payments.

In terms of advertising, Google’s specific advertising practices have maintained steady growth. At Google’s Google Think Games 2019 Game Summit, Maria Tyutina, director of revenue-generating strategy at Game Insight, said “Game Insight revenue for non-paying users has increased by 30%.” Incentive video ads for intelligent analytics are also enabling more accurate crowd positioning.

These are also part of Google’s key services for game makers. At ChinaJoy, which was just completed some time ago, Google’s Google booth highlighted the cooperation programs of “game experience innovation”, “player interaction innovation” and “business model innovation”.

The core highlights of App campaigns

For example, in terms of player interaction innovation, you can see from the YouTube booth area: Developer’s content marketing can enhance exposure and more touch players through video, KOL anchor and other off-game scenes.

Apps such as App campaigns can be used to attract players to download through premium ad content. At the same time, App campaigns can rely on intelligent algorithms for machine learning, according to search intentions, interests, favorite application types, browsing videos, etc., to reach users with downloading willingness, accurately identify and obtain high-value paying players, and let developers’ games be fully Potential players in the world find and understand player behavior and stay productive.

In addition, the Google AdMob service offers developers more possibilities in the hybrid realm mode.AdMob’s interstitial ads, banner ads, incentive video ads, native ads, and the new open-screen ad App Open Ads, these ad formats, make the domestic game makers more diversified.

In 2019, the game has become a must-have business development direction for many domestic manufacturers. At the game summit, Deng Hui also mentioned that there were 18 domestic manufacturers with annual revenues of 500 million yuan last year, and more and more manufacturers enjoyed the dividend of going out to sea.

Under the background of the traditional growth of the heavy category, the “2019 China Mobile Game Depth Insight Report” pointed out some potential directions worthy of further exploration. In general, for the size of different key markets, in the mature market, try to light and moderate products, layout has been involved in less potential topics and categories; and in emerging markets, with downloads, user advantages, combined with more samples The means of realizing the use of various types of sea-going tools provided by Google Google may be the new opportunities for the next phase of the sea.

Data Source:

“2019 China Mobile Games Going Deep Insight Report

Google Google Think Games 2019 Game Summit

App Annie Leaderboard