_000″>

Data source: CRIC

02

The sales performance threshold of each echelon of real estate companies is raised again

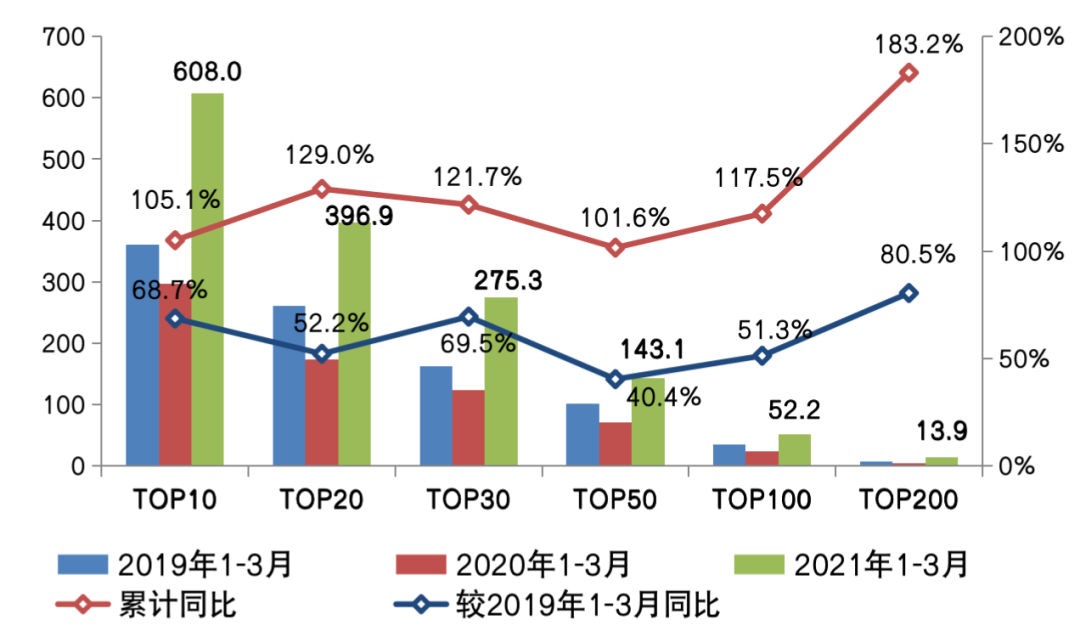

The sales performance threshold of each echelon of real estate companies will continue to increase in the first quarter of 2021, which is a significant increase compared to the same period in 2020 and 2019.

The industry’s leading real estate companies continue to maintain their performance advantages, and their rankings are relatively stable. The threshold for the TOP10 real estate companies to enter the list is 60.80 billion yuan, a year-on-year increase of 105.1%. The TOP20 and TOP30 real estate companies’ sales operators’ thresholds for entry into the list both increased by more than 120% year-on-year.

From the perspective of growth rate, TOP100-TOP200 small housing companies have the highest year-on-year growth rate, and the threshold for the sales amount to enter the list is 1.39 billion yuan, a significant year-on-year increase of 183.2%. The reason is that, on the one hand, the performance of the same period last year was affected by the negative impact of the epidemic, and the low base effect was more pronounced. More importantly, the small real estate enterprises in hot cities accelerated their shipments.

From the performance of the sales threshold of each echelon of real estate companies compared to the same period in 2019, small real estate companies still showed a significant increase, and the growth rate of the threshold for TOP200 real estate companies is still higher than that of other echelon real estate companies. Among the top 100 real estate companies, the growth rate of companies of different magnitudes is relatively low. Among them, the top 30 real estate companies lead the other echelons with a growth rate of 69.5%.

Picture: The threshold (100 million yuan) and changes in the cumulative sales of TOP200 real estate companies from January to March 2021.

Data source: CRIC

03

The performance of over 40% of real estate companies has increased significantly

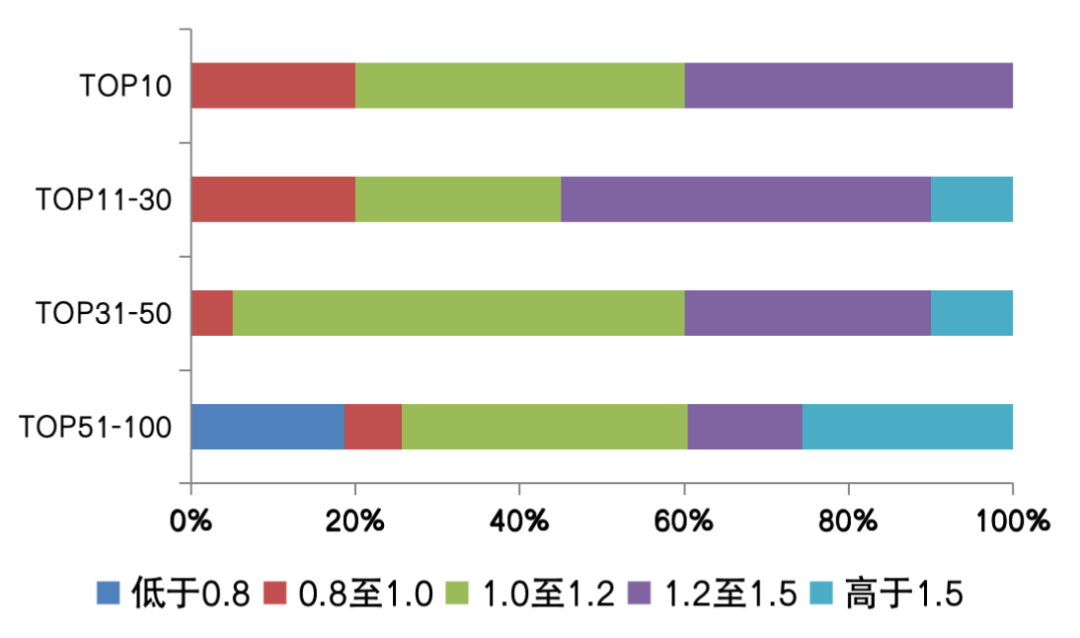

In terms of the performance of real estate companies, in March, 81% of the top 100 real estate companies had better monthly sales performance than last year’s monthly average, and more than 40% of them increased their performance by more than 20%, and the overall performance improved significantly. From the comparison of the sales growth rate of different echelons of real estate companies, the proportion of TOP31-50 real estate companies achieving positive growth is 95%, and the growth is the most prominent among all echelons.

Among the TOP30 real estate companies, although 20% of the companies’ monthly performance is lower than last year’s average, the decline is still less than 20%. Considering their size, the overall performance is still optimistic. TOP51-Among the 100-echelon real estate companies, more than 26% of the companies’ performance has increased by more than 50%, and nearly 20% of companies’ performance has fallen by more than 20%, showing a relatively obvious polarization.

Picture: The distribution of the monthly performance of each echelon of real estate companies in March 2021 compared to the average monthly performance growth in 2020

Note: This figure shows the ratio of the sales amount in March 2021 to the average monthly sales amount in 2020

Data source: CRIC, corporate announcements

04

The policy margins are tightening, and real estate companies still face challenges

The first quarter coincided with the announcement of performance by listed real estate companies. Comprehensive real estate companies’ performance in 2020, slowing revenue growth, and decline in sales gross and net profit margins are common phenomena. On the one hand, the high-priced land acquisition projects of real estate companies during the hot housing market entered the settlement period. On the other hand, affected by the epidemic, the progress of housing companies’ construction has been delayed, and operating costs and marketing expenses have risen during the period. In short, the industry is facing a huge decline in profitability pressure.

In this context, combined with the tightening of policies, real estate companies still face a number of challenges.

First of all, real estate companies are facing a situation where the overall policy environment is becoming tighter. For real estate companies, although transactions in the hot city markets will usher in a certain degree of cooling, the demand for housing-based housing still exists, and the sales window period for real estate companies will continue. As the release pace of residential demand will be delayed, real estate companies need to rebuild the sales rhythm and marketing nodes, and actively accumulate customers to promote sales, so as to ensure the removal of projects and the efficiency of payment collection.

Furthermore, the operation of real estate enterprises has achieved initial results and will still face greater financial pressure in the future. Judging from the information disclosed by the real estate companies in the annual report in March, the “three red lines” of many real estate companies have successfully downgraded, and most of the real estate companies also maintain confidence in downgrading to the “green range” in the next one to two years. Although the rapid downgrade has enabled the comprehensive operational capabilities of high-quality real estate companies to be reflected, real estate companies still face restrictions on the supply-side financing channels and strict inspections of demand-side buyers’ funds, so the pressure on the capital side has not been effectively alleviated. In the future, real estate companies still need to continue to reduce costs and increase efficiency. In terms of “open source”, in addition to guaranteeing the return on sales for normal operations, real estate companies also need to make efforts in revitalizing existing assets, strengthening equity financing, or splitting and listing. In terms of “throttling”, real estate companies need to actively apply big data and digital management methods to project development, It is also necessary to strengthen cost control and improve per capita efficiency.

The “two centralizations” of land supply are new challenges facing real estate companies. The “two concentrations” land supply policy in key cities hopes to increase supply and divert hot land resources so as to ensure rational competition in the land market, but in essence, it increases the operating risks of real estate companies to a certain extent. In the land auction stage, real estate companies need to strengthen their fund co-ordination ability, by adjusting the financing rhythm and the pace of collection, not only to avoid the long-term idle of a large amount of funds, but also to ensure that there is sufficient deposit to participate in the auction of multiple plots. Real estate companies that are already in the “green stall” are expected to replenish high-quality land reserves with their capital advantages, while those with insufficient reserves will face greater pressure to replenish inventory.

Centralized land supply may lead to the concentrated entry of future projects into the market, and the pressure of real estate companies to compete for products will increase. Therefore, in the development stage, it is necessary to improve the standardization of products and speed up the turnover rate, so as to obtain certain advantages in the market launch stage. The future development strategies of real estate companies will also be affected. In hot cities, real estate companies need to strengthen the ability of deep cultivation and precise research and judgment in hot cities to gain an advantage in the concentrated land auction competition.

At the same time, real estate companies also need to moderate their focus on land acquisition to the surrounding areas of hot cities or other non-hot cities, and adjust the sales rhythm of future projects by adjusting the investment structure. In addition, the advantages of real estate companies that have diversified land acquisition capabilities and can replenish land reserves through urban renewal, mergers and acquisitions, etc. have been highlighted. Other real estate companies can also achieve complementary advantages by increasing the proportion of cooperative development.

Attachment: TOP50 real estate sales ranking list in March 2021