New venture capital opportunities for small coffee shops, boutique instant, ready-to-drink coffee.

Editor’s note: This article is from the micro-channel public number “thirty thousand food Yanxishe” (ID: sanwanshipin), Author: thirty thousand Capital Roujia.

In the past three months of 2021, a number of coffee brands have completed a new round of financing: the boutique coffee chain M Stand completed the first round of financing of 100 million yuan, and the valuation of 10 stores exceeded 700 million after the investment; Manner received another round of financing after December last year, with a post-investment valuation of US$1.3 billion; Canadian coffee brand Tim Hortons completed a new round of investment from Sequoia Capital, Tencent, etc., and plans to open more than 200 more this year Stores. In addition, companies from other racetracks have also continued to enter the domestic coffee market. Tongrentang began selling health coffee, new tea brands like Heycha and Naixue launched coffee drinks, Sinopec and Liancafe launched a new brand of Easy Coffee, and Oyo Hotel launched “Fenran”. “Coffee brand…

Enterprises of various backgrounds have entered the game, and there are players in various price bands and consumption scenarios. What are the opportunities for the development of the domestic coffee market where experts gather? This article will analyze the development status of the coffee industry and investment and entrepreneurial opportunities, hoping to inspire everyone.

Main content of this article

I. Overview of the coffee industry

Second, the development of the coffee industry in Japan

Three, the development of my country’s coffee industry

Four. Operation model and development status of domestic coffee industry

V. Investment and entrepreneurial opportunities in the domestic coffee industry

I. Overview of the coffee industry

Coffee is one of the three largest non-alcoholic beverages in the world, and its consumption is concentrated in developed countries such as Europe, the United States, and Japan

Coffee is known as one of the world’s three major beverages (the other two are tea and cocoa). Daily coffee is made from coffee beans through different cooking methods. Coffee beans refer to the nuts in the coffee tree fruits (called berries). Generally speaking, coffee needs to go through the steps of planting, picking, green bean processing, roasting, and extraction to change from a mountain crop to a drink.

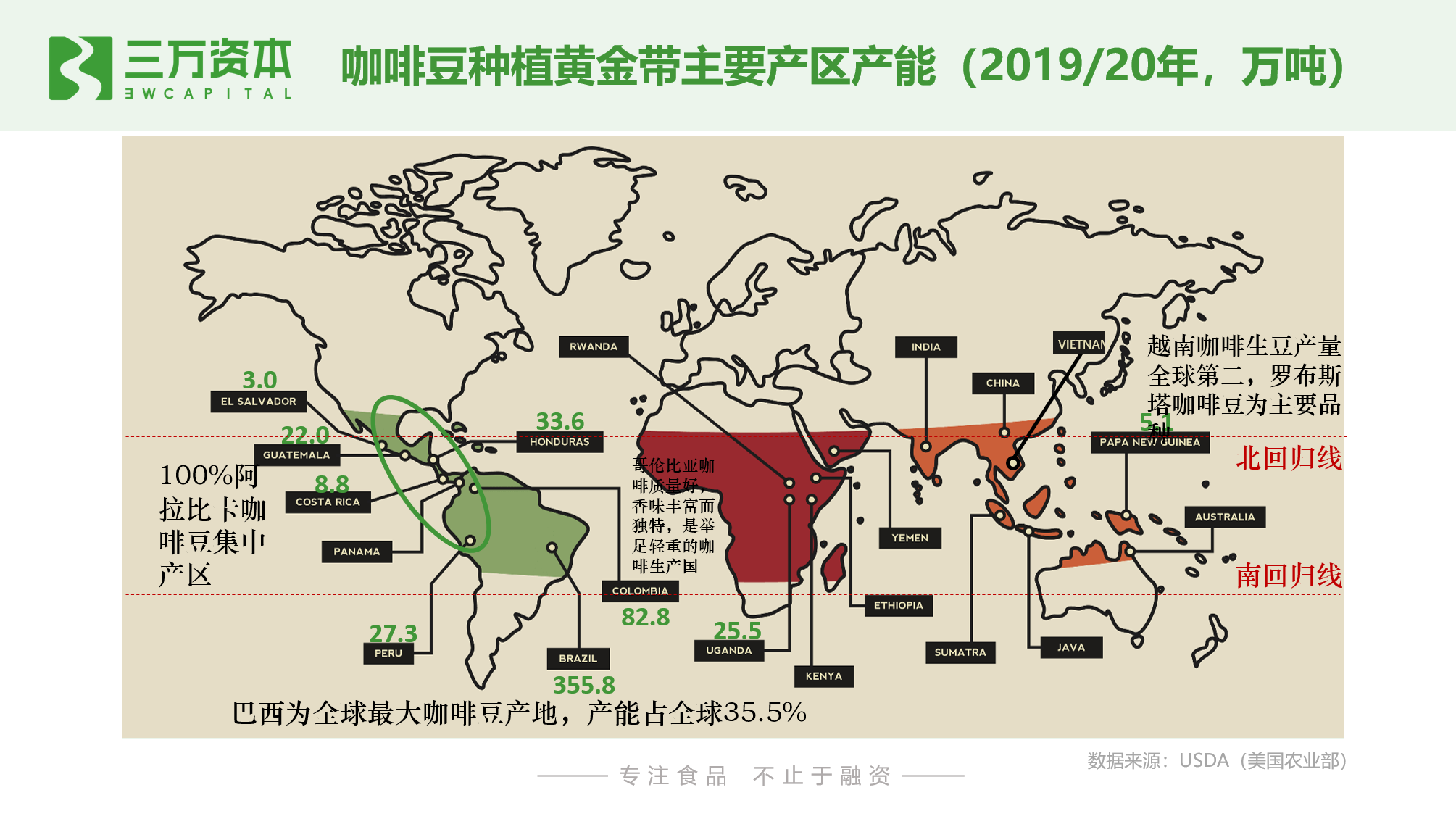

From the origin, the ideal coffee growing place is between 25° north and south latitude, and the average annual temperature in this area is around 20°C.On the right, the average annual precipitation is between 1000-2000mm. The three major coffee producing regions in the world are located in Africa, Southeast Asia, and Central and South America.

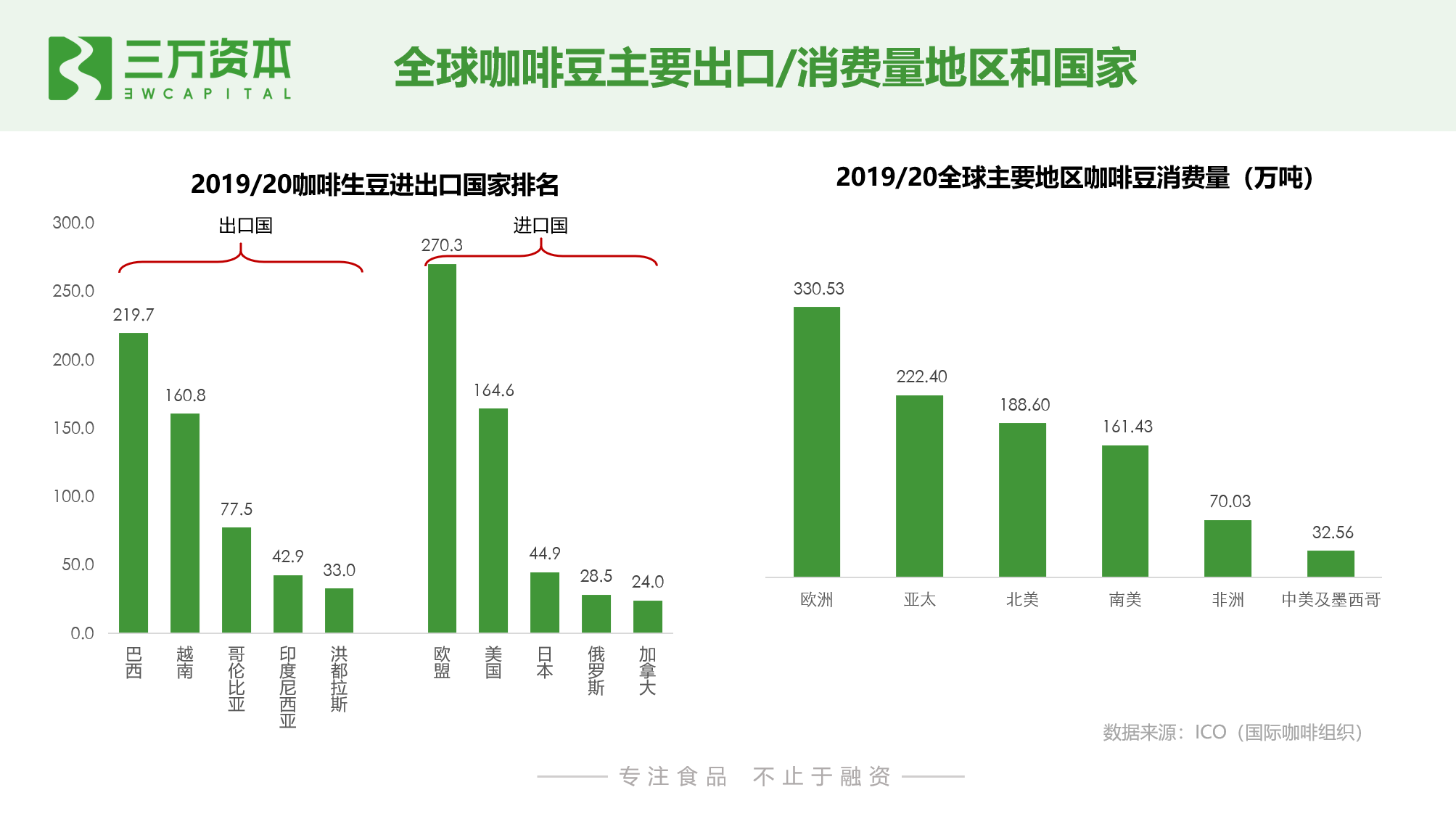

In terms of coffee consumption, due to the difference in the popularity of coffee culture and the purchasing power of residents, coffee consumption varies greatly between different regions. Coffee consumption is mainly concentrated in the economies of Europe, the United States, and Japan. Developed countries and regions, green coffee beans are mainly exported from developing countries to developed countries.

The CAGR of global coffee production/consumption in the past ten years is about 2-2.5%, showing a steady growth trend

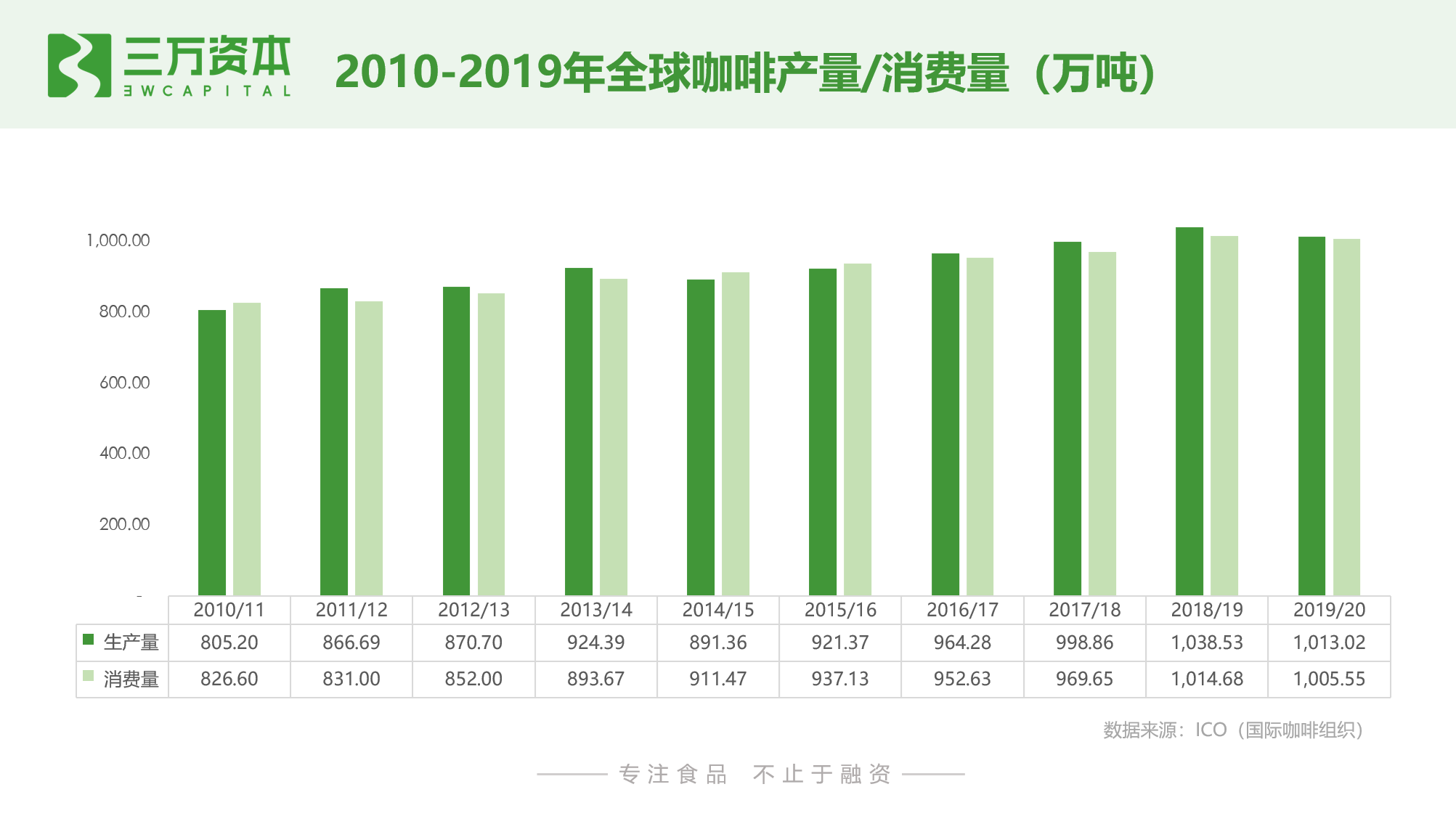

Global coffee production increased from 8.0520 million tons in the 2010/11 production year (October to September of the following year) to 10.1302 million tons in the 2019/20 production year, with a compound annual growth rate of 2.58%; global coffee consumption From 8.26 million tons in the 2010/11 production year to 10.0555 million tons in the 2019/20 production year, a compound annual growth rate of 2.20%. The growth rate of global coffee production/consumption is relatively slow, indicating that the global coffee market has entered a more mature stage of development.

In the past 200 years, European and American countries have gradually evolved into specialty coffee after three waves of coffee

The first wave occurred in 1940-1970, when instant coffee represented by Nestlé rose. Instant coffee was originally developed mainly to understandSolve the problem of overproduction of coffee beans in Brazil in the 1930s. In 1938, the Brazilian government collaborated with Nestlé to develop instant coffee, which transformed coffee from an agricultural product to a standardized product, and coffee began to circulate in the form of coffee powder. During World War II, coffee was used as an armament and cultivated people’s coffee drinking habits.

The second wave appeared in 1971-2000, when brand chain cafes represented by Starbucks expanded. Drinking coffee at this stage has become a comprehensive experience of enjoying coffee and social leisure. Consumers’ demand for coffee is not only a single refreshing effect, but also leisure and social attributes have begun to appear.

The third wave lasted from 2003 to the present, and the development of specialty coffee. People pay more attention to the origin, variety, picking month, altitude, and processing methods. Roasting pays more attention to the original flavor of coffee beans, and hand-punching has become the mainstream.

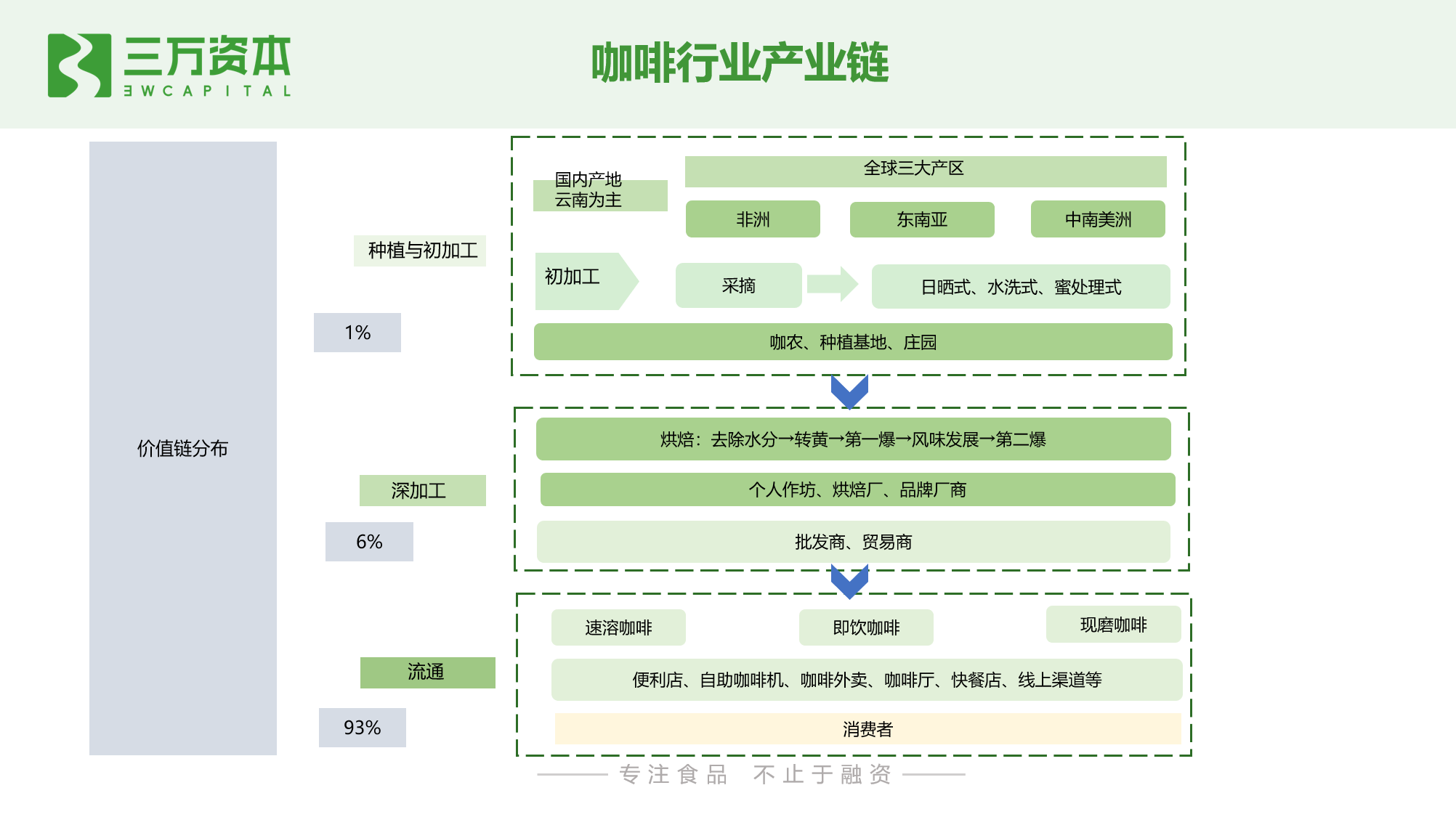

The industry chain is divided into three links: planting, deep processing and circulation, and product innovation is concentrated in the downstream circulation end

Upstream planting and initial processing, the final product type is green coffee beans. The processed green coffee beans will be packed into standard 60kg sacks, enter the trade link, and be sold to midstream roasting factories or traders. The cost of coffee planting mainly includes irrigation, fertilization costs and labor costs. Internationally, the production cost of major coffee producing countries is 12-13.5 yuan/kg. The upstream planting links are relatively scattered, and the participants are mainly small and medium coffee farmers, large planting bases and plantations.

The midstream deep-processing link refers to the process of roasting green beans to mature beans. The main participants are various roasting factories. Raw beans are the main cost of this link, as well as transportation, gas, equipment depreciation, labor, etc. The roasting factory will increase the price by 50%-60% on the basis of the total cost. Generally speaking, domestic coffee shops, hotels and other B-end companies purchase The price of coffee beans is concentrated in 50-150 yuan/kg.

The downstream circulation links mainly include wholesale and retail. The diversification of product forms and channels in the retail sector accounts for a high proportion of the entire coffee industry value chain and is a high-frequency zone where innovative models occur. There are three types of coffee products for end consumers: pre-packaged coffee, ready-to-drink coffee and freshly ground coffee. Major manufacturers focus on these three business types to innovate their products and compete for the consumer market.

Second, the development of the coffee industry in Japan

Coffee was introduced to Japan along with the Western lifestyle and entered a period of rapid development in the late 1960s

In Japan, the emergence of coffee originated at the end of the 18th century. At that time, Dutch residents living in Nagasaki began to drink coffee, and coffee began to appear in Japan; in 1877, Japanese coffee began to be imported in bulk and commercialized; in 1888, Japan’s first A coffee shop opened in Tokyo, and the habit of drinking coffee continued to penetrate; in 1937, the number of coffee imports in Japan reached 140,000 bags; after that, due to the impact of World War II, coffee imports were interrupted until the liberalization of coffee imports in 1961, and imports were imported this year About 250,000 bags of coffee. However, during this period, compared with green tea, coffee was still not a mainstream beverage. Coffee consumers were mainly wealthy adult urban residents.

In the late 1960s and early 1970s, with the widespread penetration and dissemination of instant coffee and cafes, as well as the introduction of ready-drink canned coffee and the expansion of self-service vending machines, coffee was promoted in the younger generation. Consumption Driven by multiple factors, coffee consumption in Japan is increasing rapidly. Over the past 50 years, Japan’s coffee consumption has soared. Japan currently ranks third in the global green coffee importing countries, second only to the European Union and the United States.

The rapid development of coffee consumption in Japan is mainly due to the following reasons:

1. With the westernization of living habits, people’s daily consumption has undergone significant changes.

2. Product innovation and market promotion, from the initial promotion of instant coffee to roasted and freshly ground coffee, diversified and suitable product forms for different scenarios meet the needs of different users.

3. The number of attractive coffee shops continues to grow, and coffee is gradually becoming professional without the support of teahouses. In 1982, the number of coffee shops in Japan reached 162,000.

4. Developed convenience stores and unmanned vending machines have promoted the development of canned coffee. The Japanese canned coffee market has continued to prosper since the introduction of vending machines in 1962. There are more than 5 million vending machines in Japan, half of which Used to sell beverages, including coffee.

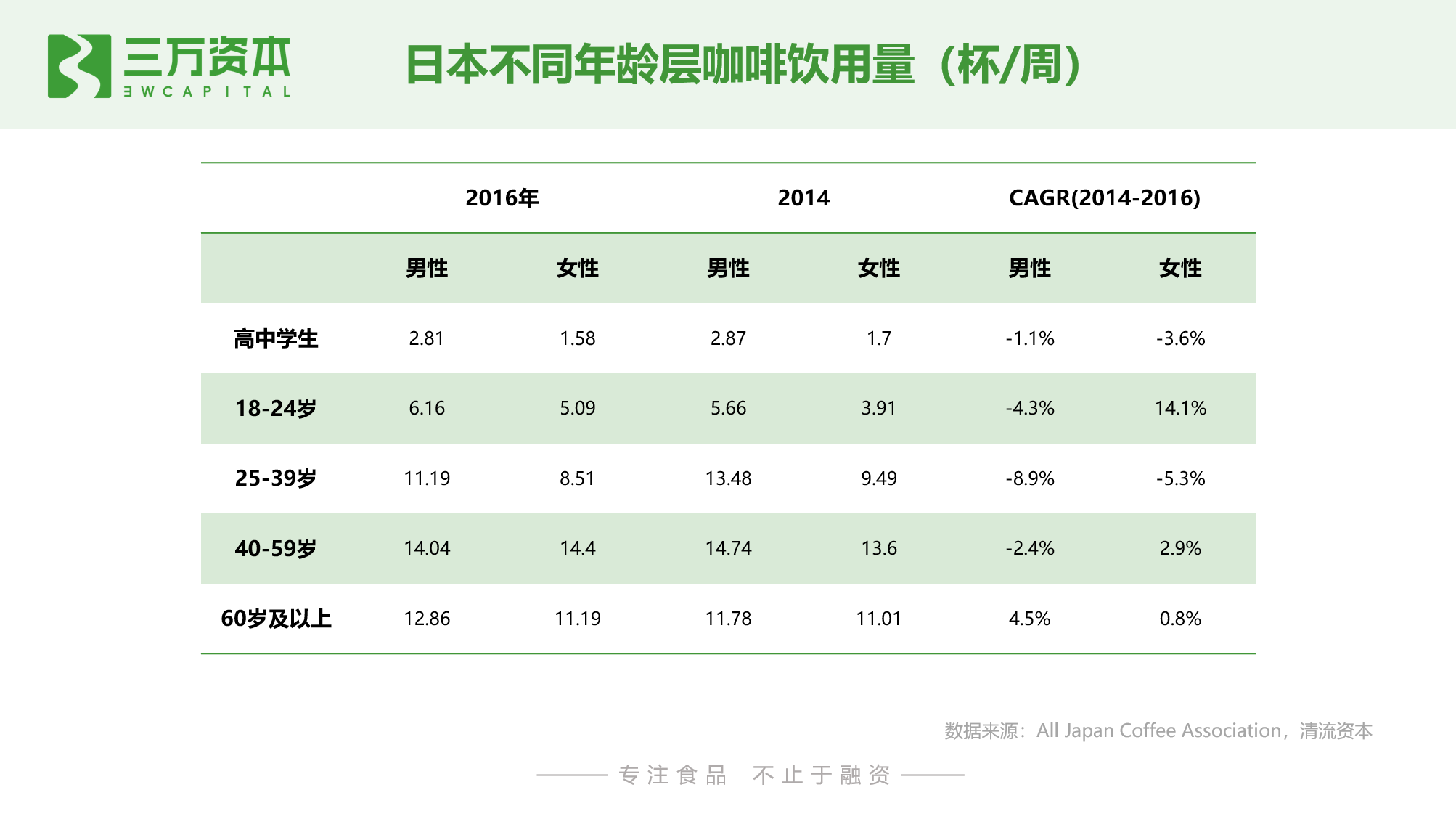

The penetration rate of coffee in Japan is as high as 90%, with an average of 11 cups of coffee per person per week

From the perspective of penetration rate, the penetration rate of Japanese coffee was as high as 89% in 2012 and 90% in 2016. The penetration rate is stable, indicating that the coffee industry in Japan is mature and the market has reached saturation. In terms of the number of cups of coffee consumed, in 2016, the average person in Japan drank 11.1 cups of coffee per week, an increase of 11% compared to 2002. It is worth mentioning that the growth rate of coffee consumption in Japan is mainly driven by middle-aged and elderly people aged 40 and above, and the coffee penetration rate and the number of cups cited by young users under 39 have shown a negative growth.

From 2002 to 2016, the penetration rate of coffee among young users aged 18-39 and the number of coffee drinks per week showed a downward trend; conversely, there was an upward trend among middle-aged people aged 40 and over, especially The growth rate is particularly obvious among the elderly over 60 years old. As we mentioned earlier, in the 1960s and 1970s, the Japanese coffee industry developed rapidly due to multiple factors. At that time, it was during the youth period (1960s-1970s) of this group of people over 60 years old. Coffee consumption habits extend to old age, which also explains the addictive nature of coffee; on the other hand, Japan is aging with a serious trend. Coffee can effectively reduce the incidence of heart and brain diseases, and drinking coffee meets the health needs of the elderly.

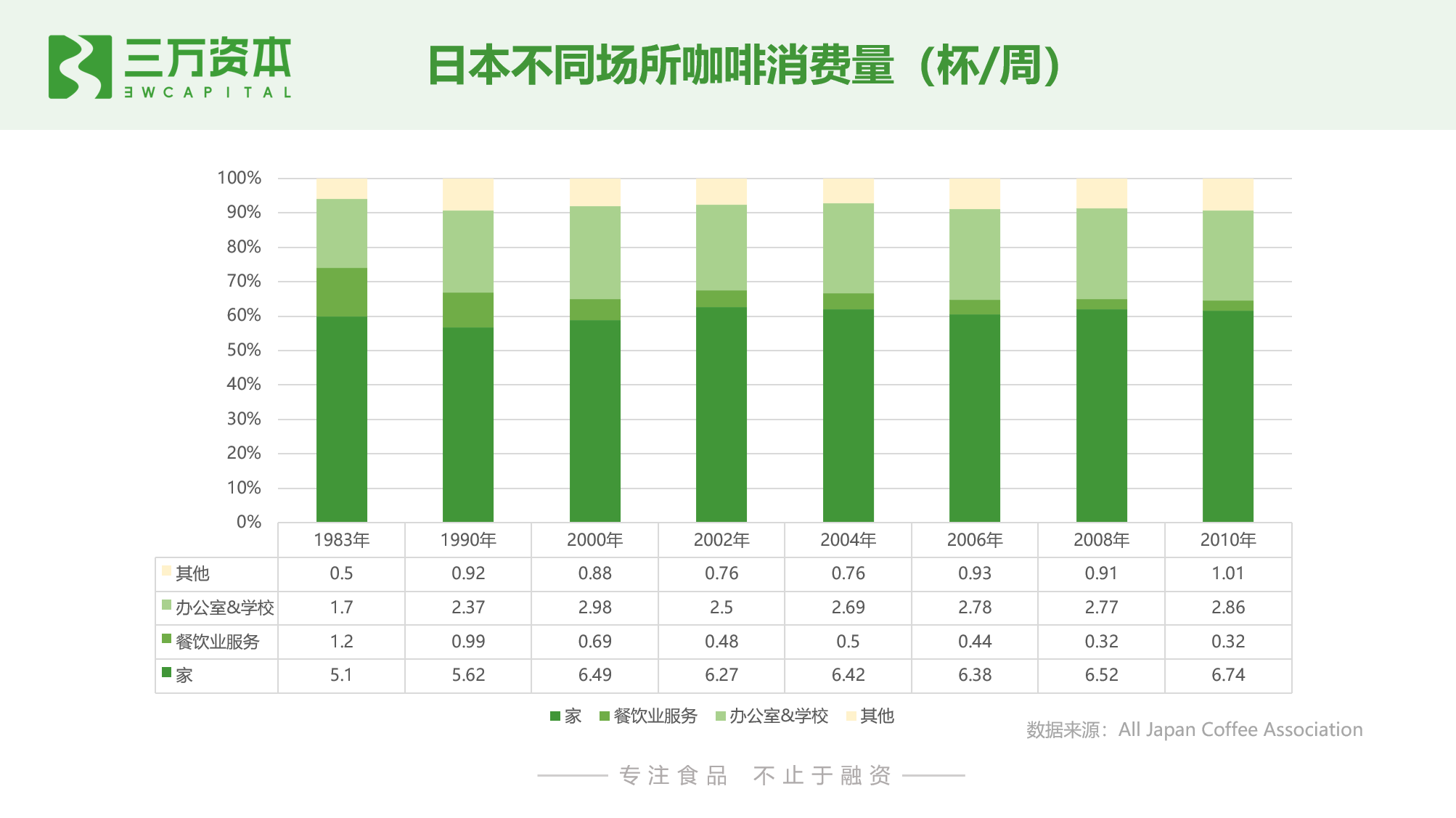

From the perspective of coffee consumption scenarios, Japanese coffee consumption is mainly at home, accounting for more than 50% of the total amount; followed by work/study places such as offices & schools; dining in cafes and other places The consumption of service places accounts for a relatively low proportion, and the downward trend has been significant in recent years.

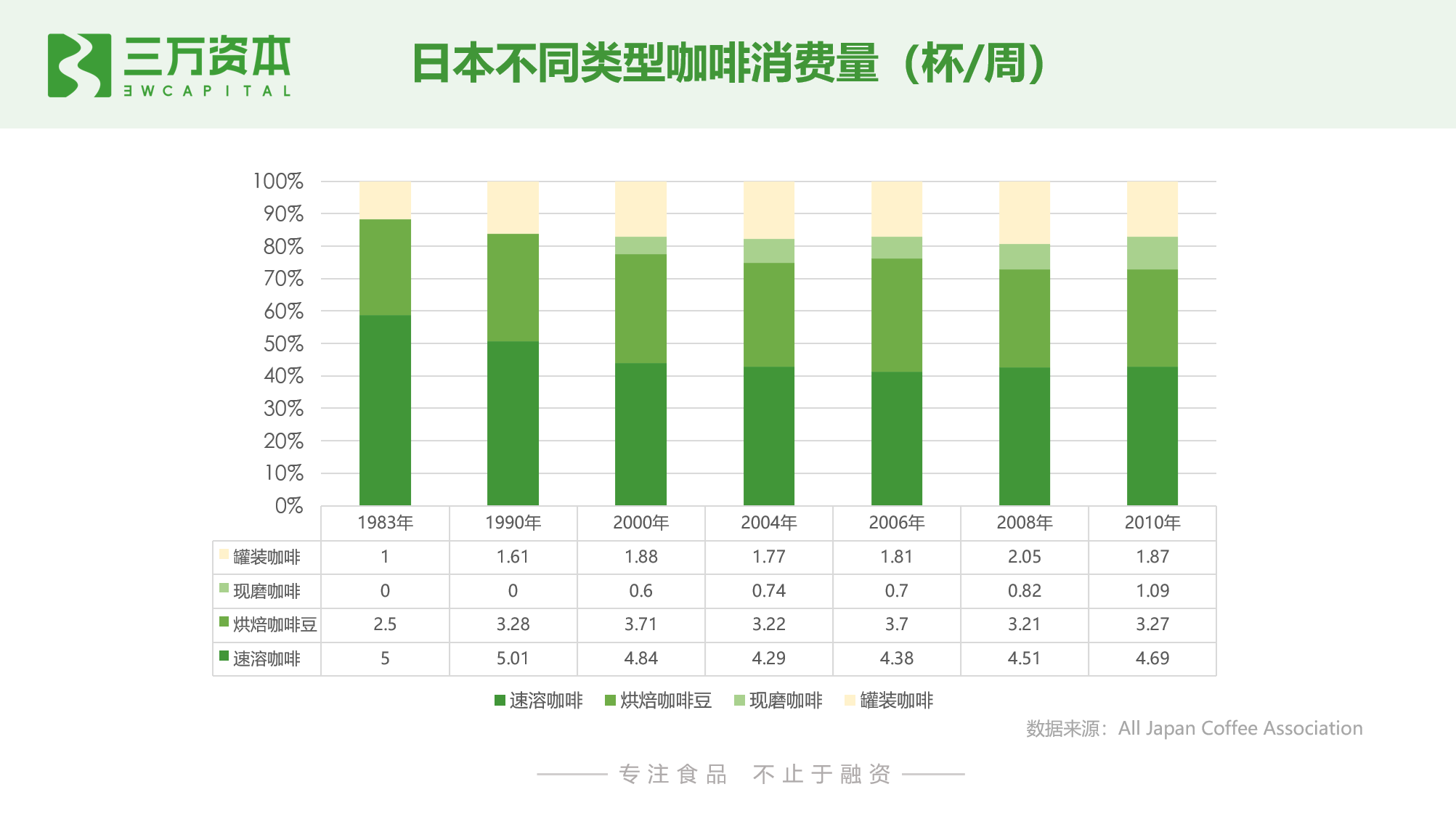

From the perspective of different types of coffee consumption, Instant coffee and coffee roasted beans are the main consumption, which also fits with the Japanese coffee consumption mainly in the family scene. Roasted beans can be used at home. Make your own freshly ground coffee, or brew instant coffee for easy storage. However, in terms of growth rate, the proportion of freshly ground coffee and canned ready-to-drink coffee has increased, while the proportion of instant coffee has shown a downward trend.

Enlightenment from the development and rise of the coffee industry in Japan

1. With the development of the economy and the increase of income, the westernization of lifestyles, the penetration rate of coffee will continue to increase.

2. The promotion of innovative coffee products suitable for different scenarios and the convenience of purchase channels will boost coffee consumption among new people.

3. Coffee is an addictive product, and the drinking habit developed in youth will continue into middle-aged and elderly people.

4. With the increase in penetration rate, the home scene will also become the main consumption place.

Three, the development of my country’s coffee industry

1. Development history

my country’s coffee industry has entered a period of accelerated development, with multiple models and formats coexisting and developing

As early as the end of the 18th century, French missionaries introduced coffee to Yunnan Province. Since then, my country has entered a long embryonic period of coffee culture. The development of my country’s coffee industry can be roughly divided into three stages.

In 1980-1996, instant coffee rose. In the 1980s, instant coffee brands Maxwell and Nestlé successively entered the domestic market to launch instant coffee, marking my country’s entry into the era of instant coffee.

From 1997 to 2014, various types of cafes emerged and developed. Taiwanese, European, American, and Korean cafes have successively entered the domestic market: Taiwanese coffee catering brand Shangdao Coffee entered the mainland market in 1997, Starbucks with Italian coffee culture entered China in 1999, and Man Coffee in 2011 Korean coffee represented by the rise; various domestic cafes have appeared one after another.

From 2015 to present, new domestic coffee brands have emerged, and multiple models have flourished. In recent years, due to changes in consumer concepts, economic development and maturity of Internet technology, China’s coffee market has begun to expand rapidly, and various new models and new formats have emerged one after another. Different from European and American countries gradually starting from instant coffeeCoffee and brand chain cafes have transitioned to specialty coffee, and various coffee models such as premium instant coffee, specialty coffee, self-service coffee machines, coffee shops, tea and coffee, etc., have developed in parallel in my country’s coffee industry to jointly seize the domestic market.

2. Investment and financing analysis

Offline coffee shops and specialty retail coffee are popular investment tracks in recent years

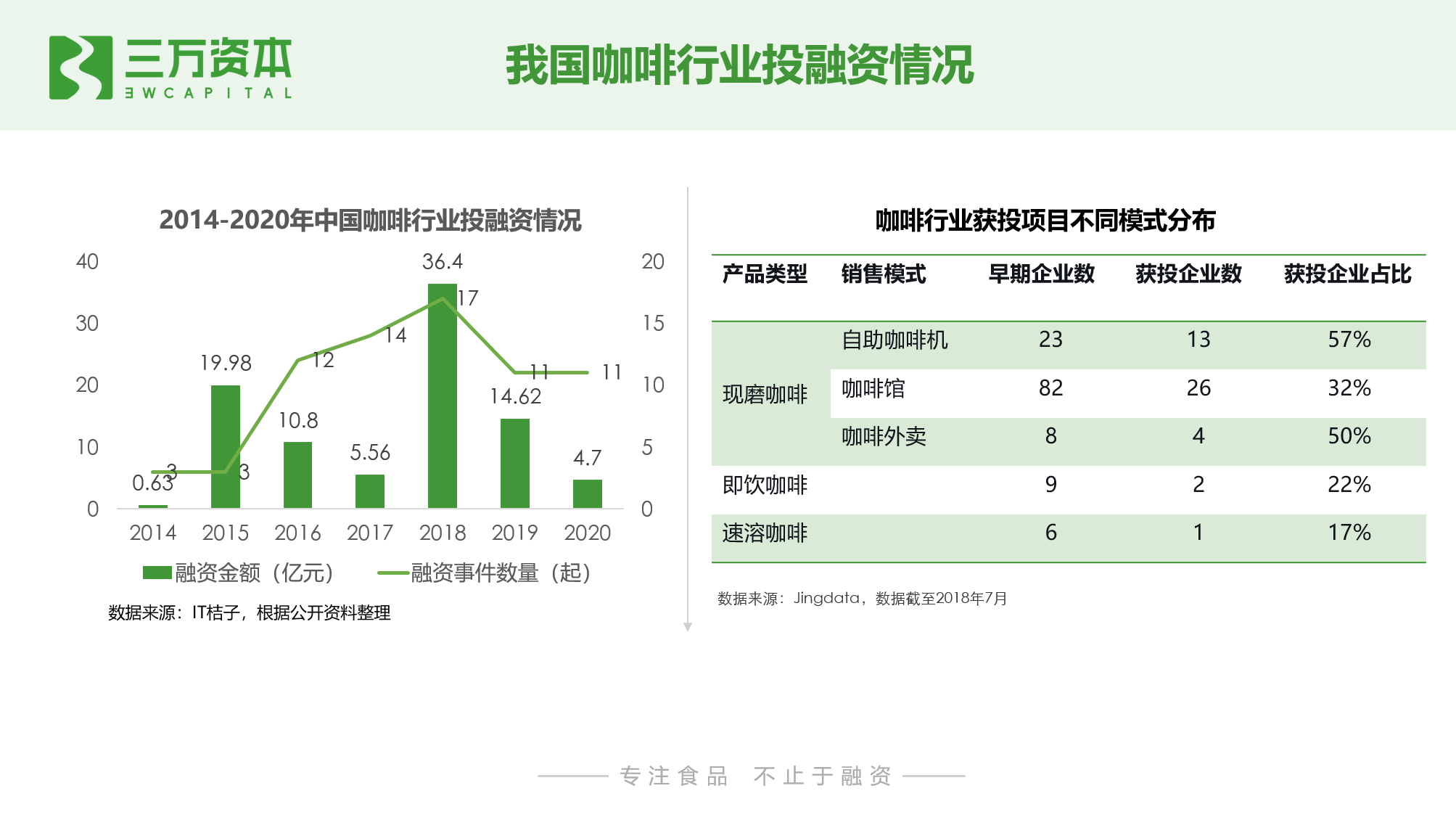

From 2014 to 2020, the amount and amount of financing in my country’s coffee industry showed significant volatility. In terms of the investment company model, 2016-2017, the investment model is dominated by self-service coffee machine mode, and in 2018-2020, it will be dominated by coffee shop and boutique retail coffee mode.

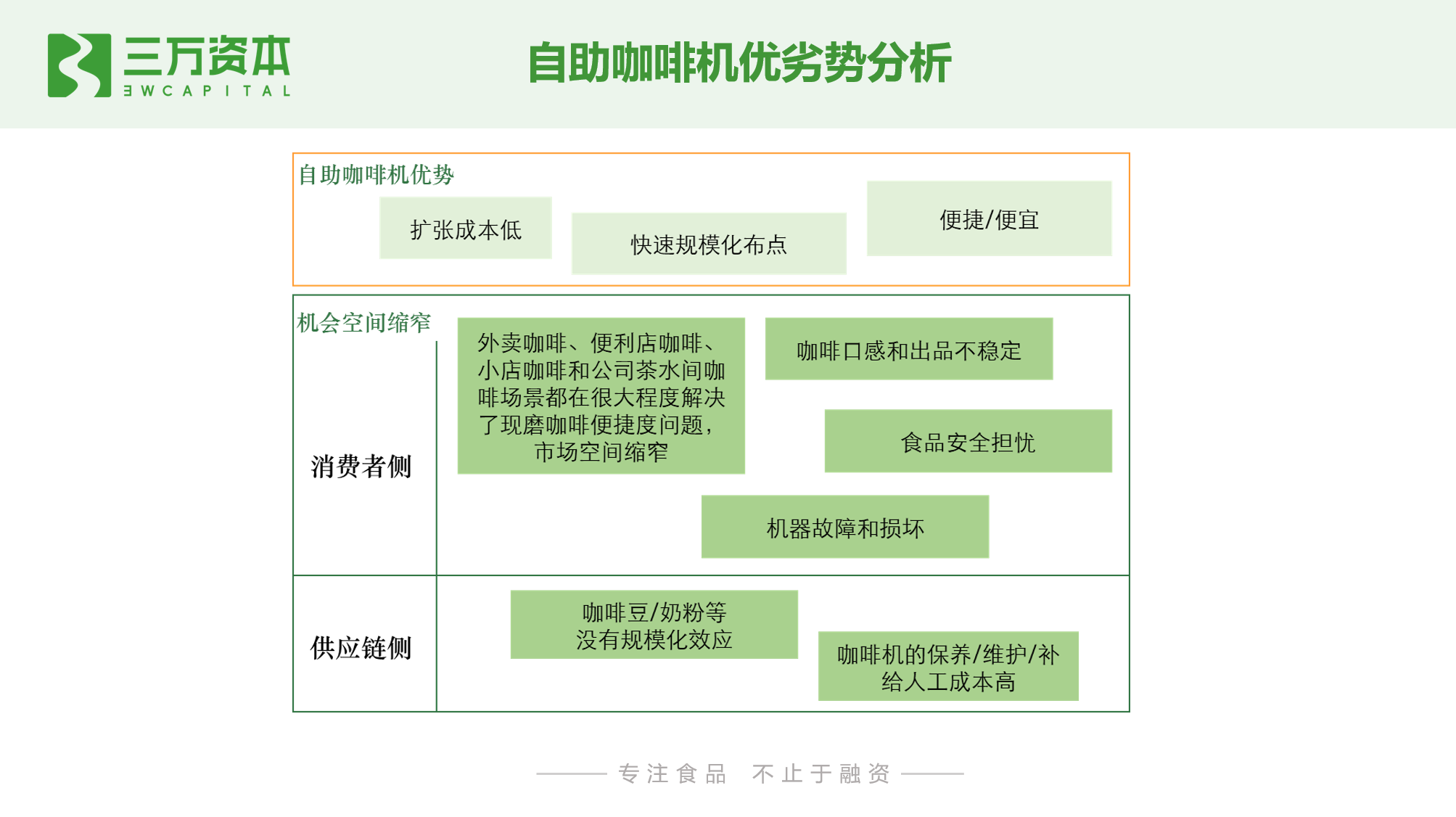

The retail format of self-service vending machines began to appear in coastal cities such as Guangdong in the 1990s, and it has been in my country for 30 years. When unmanned retail was hot in 2017, self-service vending machines were one of the most mature models among the three major unmanned retail formats (unmanned convenience stores, unmanned shelves, and self-service vending machines), and coffee was more developed as a self-service vending machine. For mature and common categories, self-service coffee machine entrepreneurship projects have received greater attention, and self-service coffee machines represented by Lai Cup coffee and a la carte coffee bars have received multiple rounds of financing. However, unlike in Japan, self-service vending machines are one of its mainstream retail formats. my country’s retail channels are diversified. Self-service coffee machines are more of a supplementary retail channel in my country to meet people’s occasional instant shopping needs. The development of self-service coffee machines has been tepid so far, and there is no leading company with a large market share.

Since 2019, specialty coffee retail brands and offline cafes have been favored by capital. The boutique instant coffee brand “Three and a half” has completed 5 rounds of financing from 2018 to 2020; the convenient specialty coffee brand “TIME Cui SERE” Completed A+ rounds of tens of millions of financing; Yongpu Coffee completed two rounds of financing in 2020; Manner, a boutique café that focuses on take-out mode, received strategic investment from Today Capital and Temasek. Today Capital even became the largest shareholder and participated in operations personally.

3. Consumer analysis

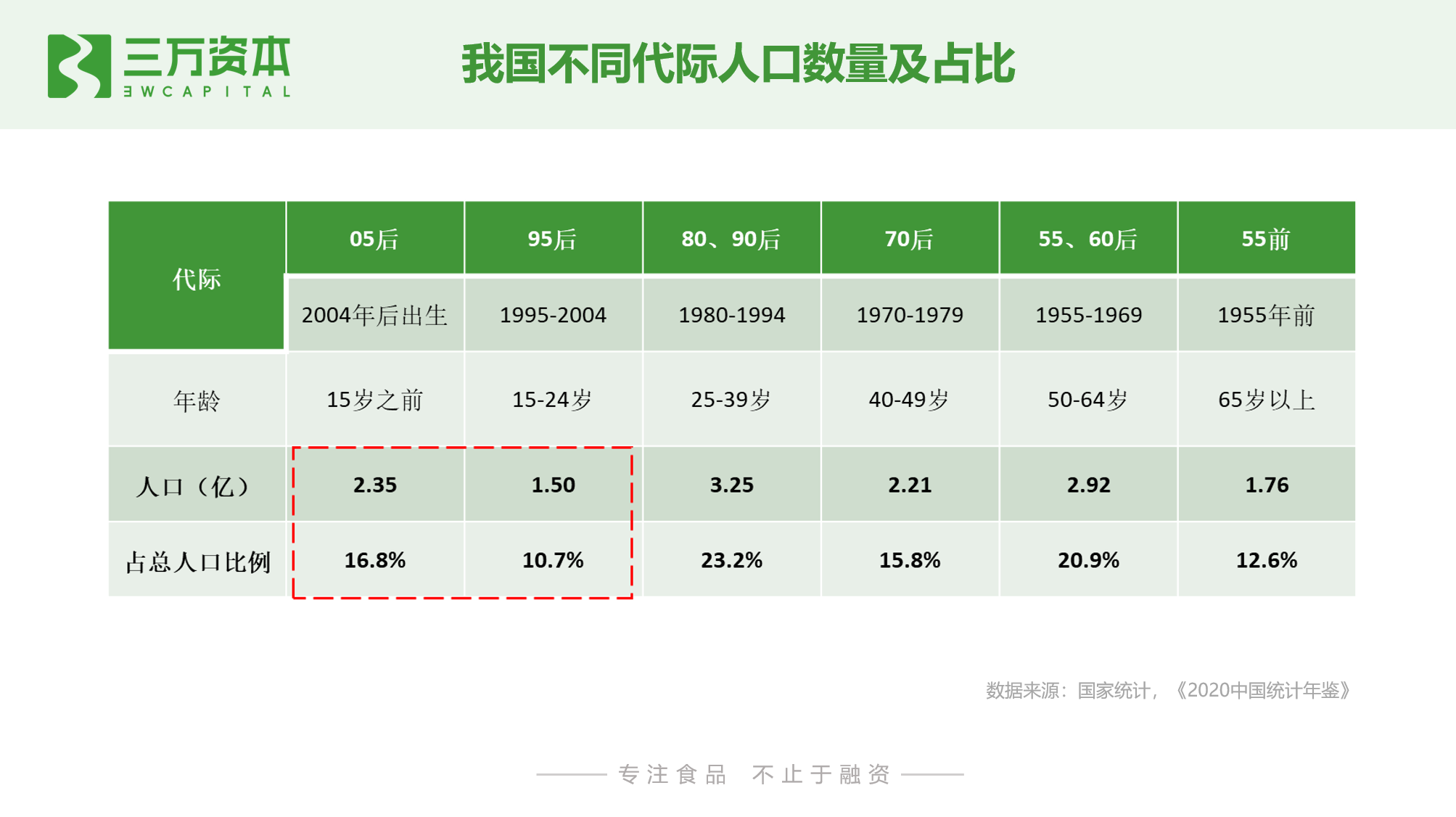

According to the statistics of the China Statistical Yearbook 2020, The number of post-80s/90s reached 325 million, accounting for 23.2% of the total population. These people are the main force in the workplace, with an economic foundation and spending power. Strong is the backbone of society; The post-95 population reached 385 million, accounting for 27.5% of the total population. As the digital natives of the Internet, the post-95s grew up in a prosperous environment with a strong sense of self. For the face value group, impulsive consumption, daring to try new things, is the main force of future consumption.

49% of mobile Internet users have drunk coffee and 77% have drunk instant coffee

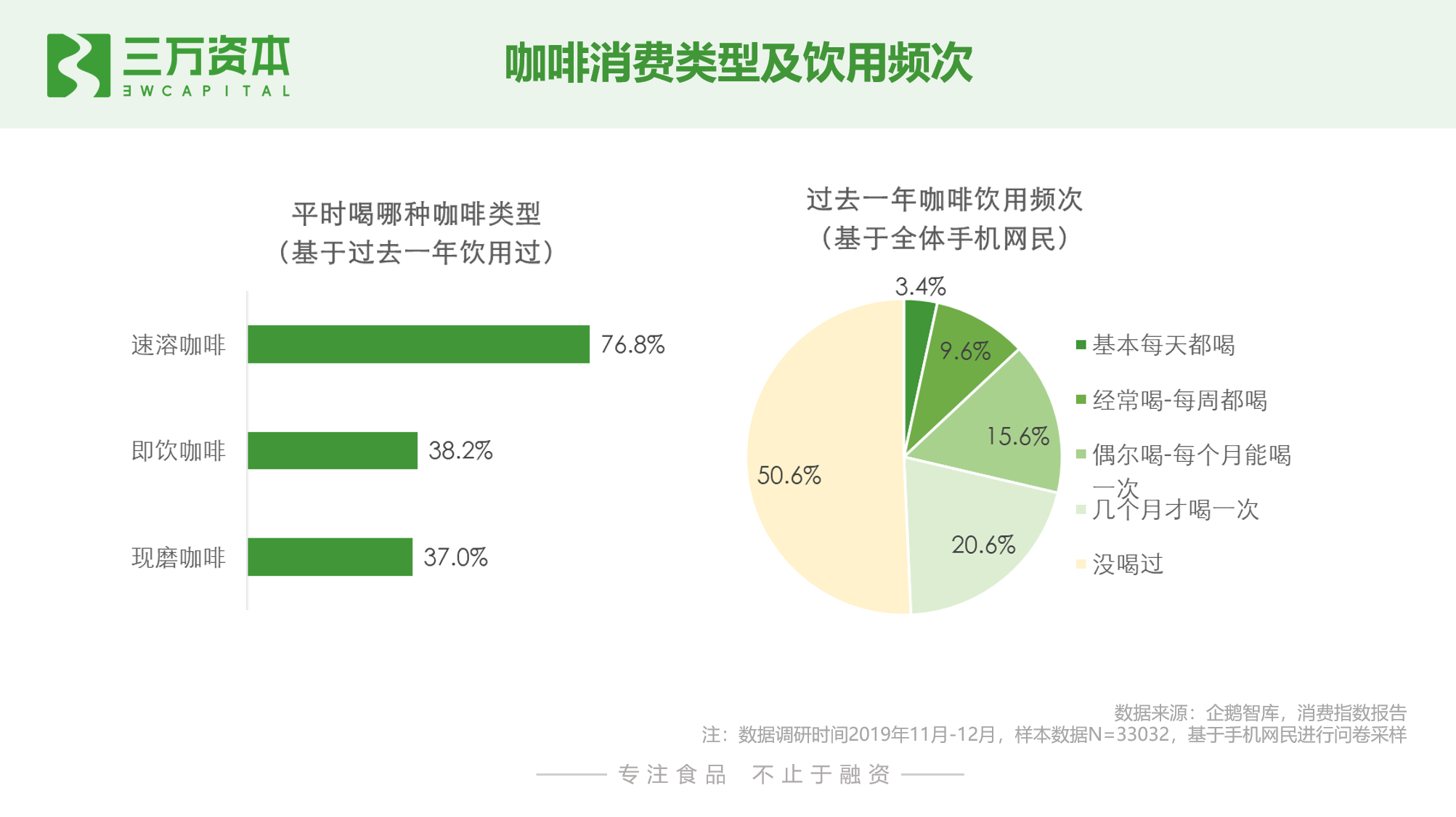

According to consumer survey data from Penguin Think Tank, in 2019, 49.4% of mobile Internet users have used coffee. It can be seen that coffee has a high penetration rate among Internet users, but the overall drinking frequency is low. Only 13% of users drink it, and 20.6% of users drink it only once in a few months. From the perspective of coffee consumption type, 76.8% of consumers have drunk instant coffee, 38.2% and 37% of consumers who have drunk instant coffee and freshly ground coffee, indicating instant coffee It is still the category most frequently consumed by consumers in my country’s coffee market.

49% of consumers are willingThe price paid for each cup of coffee is less than RMB 10

From the perspective of coffee consumption plans, 36% of mobile Internet users said they would buy coffee in the next year, 30% said they didn’t know, and 34% said they would definitely not buy coffee. Consumers who plan to buy coffee in the next year plan to consume 8.7 cups per month on average. The average price consumers are willing to pay for each cup of coffee is 14.5 yuan, and the price range of 5-10 yuan accounts for 28%, followed by those below 5 yuan. It accounts for 21%, which means that consumers in the single-product coffee segment below RMB 10 have the highest purchasing power and willingness to buy.

39.8% of consumers plan to increase the purchase amount, and 6.5% plan to reduce the purchase amount

Among consumers with coffee purchase plans in the coming year, 39.8% of consumers plan to increase their purchase amount, and only 6.5% plan to reduce their purchase amount. It shows that once users start drinking coffee, their habits are easier to maintain. Of the consumers who plan to reduce coffee spending, more than half choose to use plain water or mineral water, traditional Chinese tea instead of coffee consumption, and only 16.1% of consumers choose to consume new tea instead of coffee Among the one-year plans to reduce consumption of new tea drinks, 18.2% of consumers choose to use coffee instead of new tea drinks. It shows that the replacement effect of new-style tea on coffee is weak.

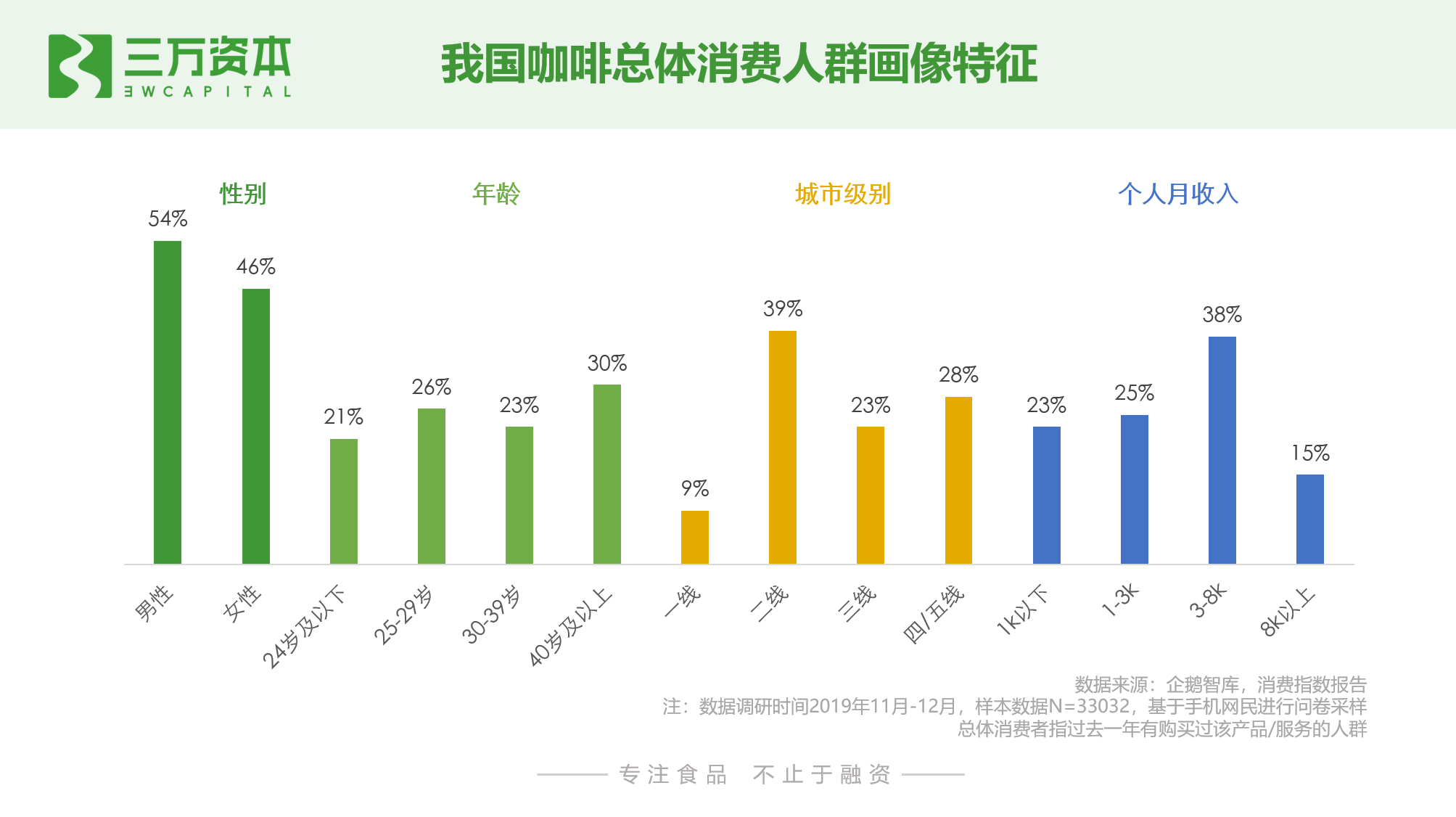

The proportion of males in coffee consumers is slightly higher than that of females. 47% of consumers are 29 years old and below. The majority of coffee drinkers in my country are young consumers;From the perspective of urban distribution, the second-tier Urban consumers account for 39%; in terms of income, 85% of consumers have monthly income below 8k.

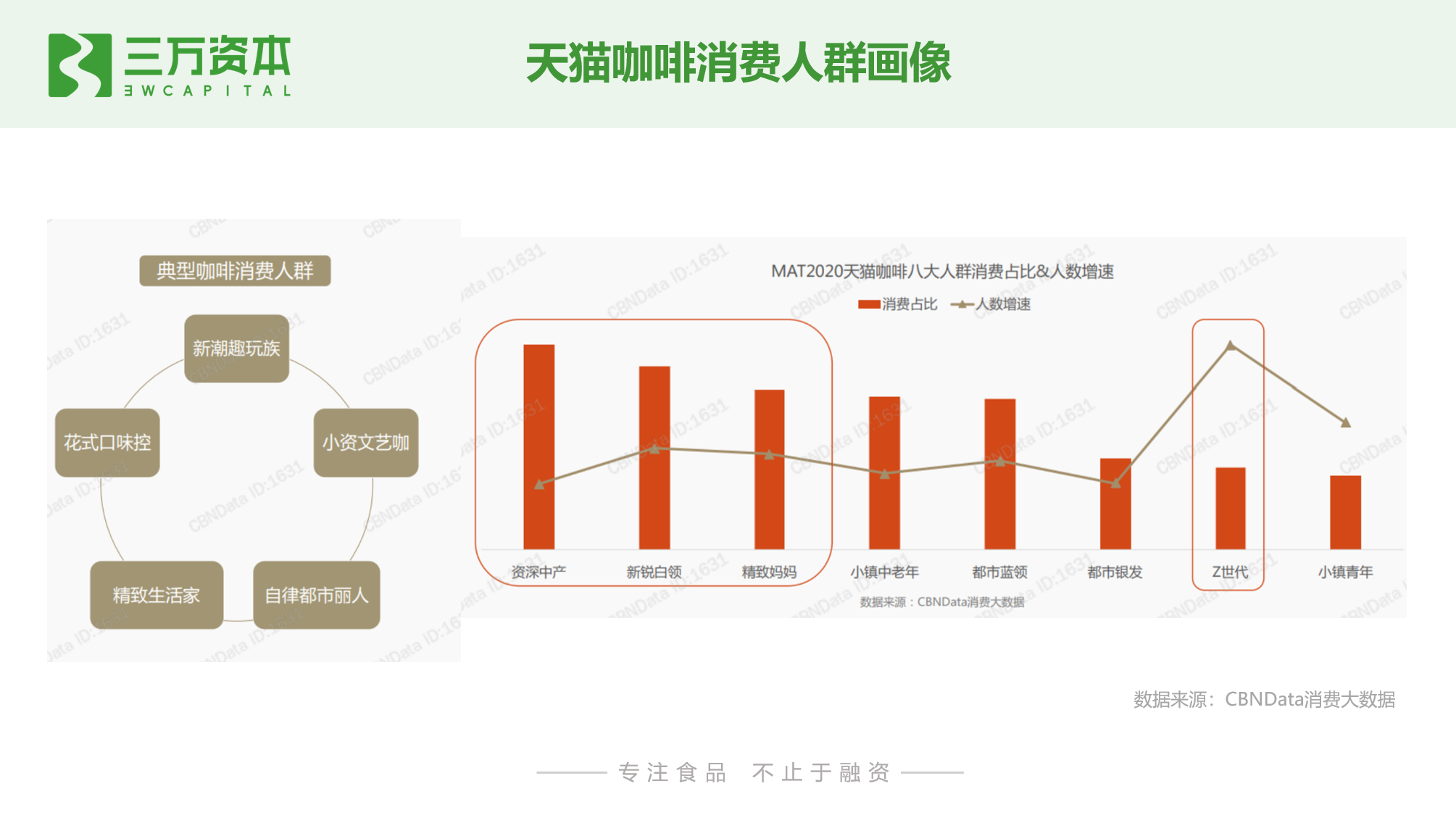

According to data from online coffee consumers on Tmall, senior middle-class, cutting-edge white-collar workers and sophisticated mothers are the main consumers of coffee. The number of coffee consumers of Generation Z has the fastest growth rate, leading the trend of play/art/interesting/novelty.

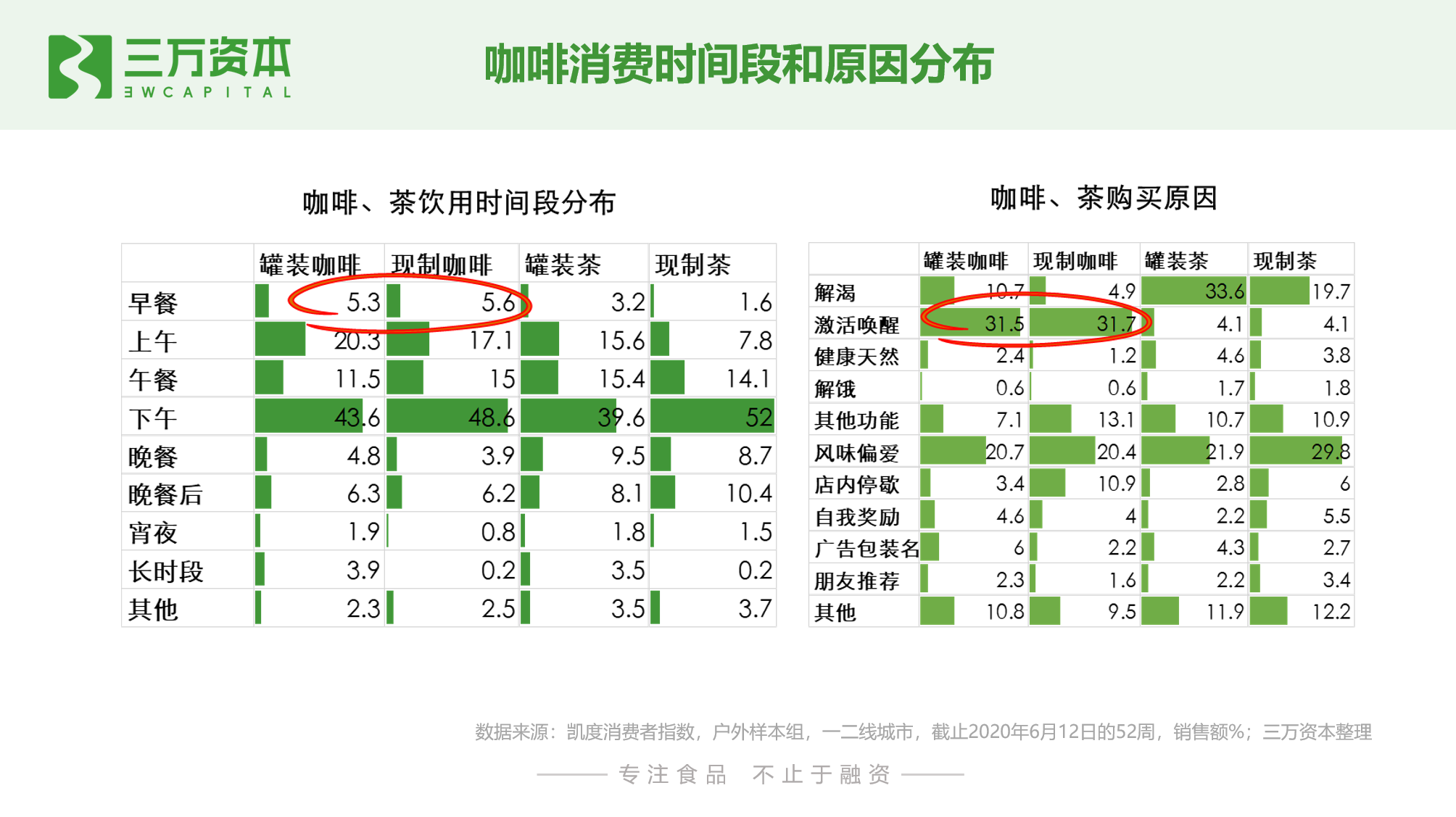

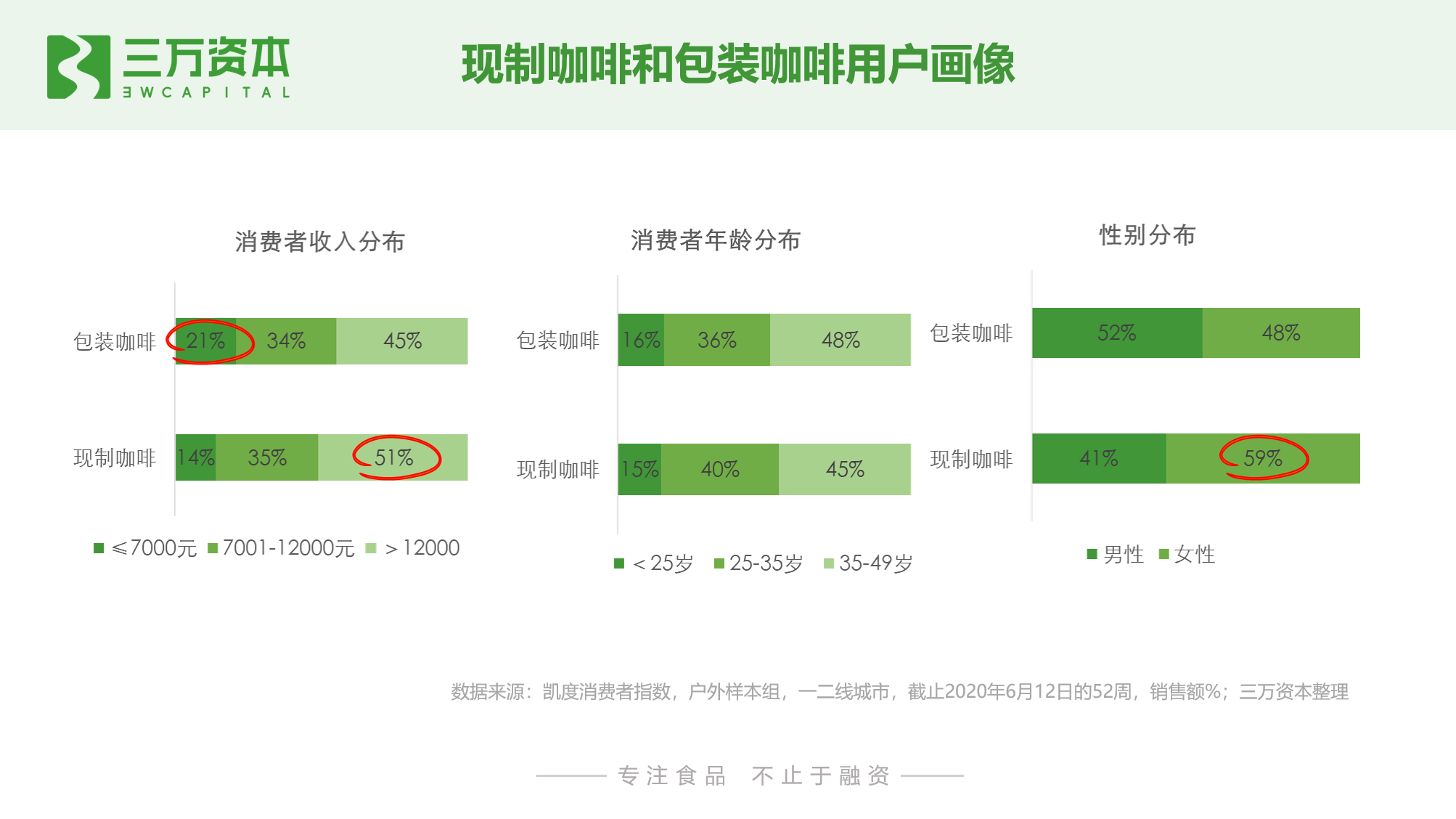

From the perspective of consumption time, coffee consumption is mainly concentrated in the afternoon. Compared with tea, the proportion of coffee consumption during breakfast is higher, especially for fresh coffee. From the perspective of purchase reasons, “activation wake” is the main reason for people to consume coffee, and the main factor for buying tea is “quenching thirst”, which shows that consumers are buying coffee and tea. The functional requirements they value are quite different, indicating that the two are relatively weak in substitutability. Judging from the user portraits of freshly made coffee and packaged coffee, high-income, young, and female users prefer freshly made drinks.

Four. Operation model and development status of domestic coffee industry

The types of coffee products for end consumers are mainly divided into three types: soluble coffee, ready-to-drink coffee and freshly ground coffee. According to different product forms, each type can be divided into multiple types.Different subdivision modes.

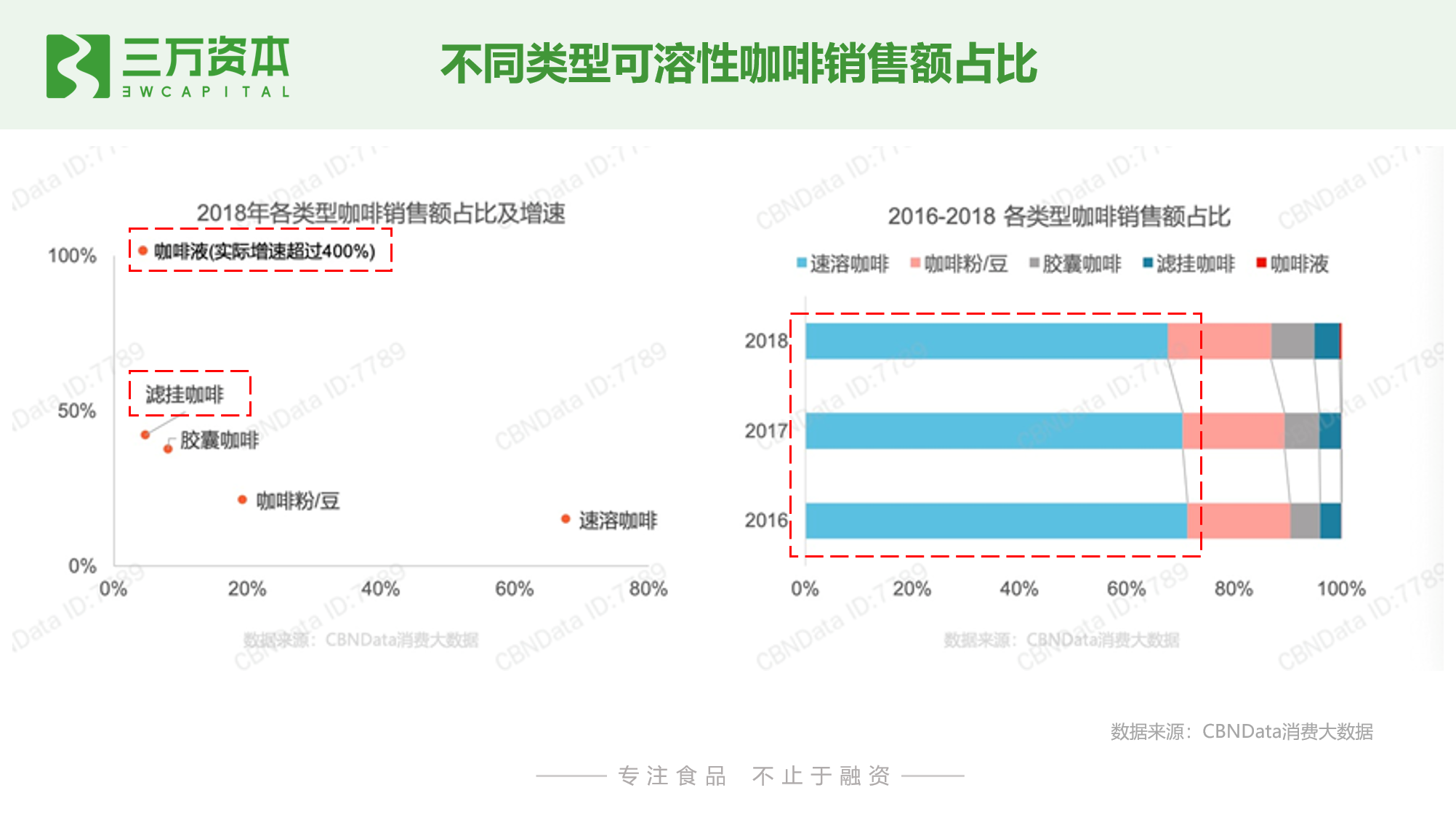

1, soluble coffee

For the convenience of generalization, in this article, we collectively refer to prepackaged coffee products such as instant coffee, hanging ear coffee, coffee extract, and capsule coffee as soluble coffee. Among them, instant coffee has a wide audience due to its convenience, early entry into the market, and price advantage. It is the current mainstream business format. Emerging coffee products such as hanging ear coffee and coffee liquid have a small market base, but their growth rate is fast, and they are especially popular with new trends. Cool young people like it.

Instant coffee opens up the domestic coffee market with its advantages of convenience and low price, and emerging brands focus on the direction of high-quality products

Compared with other types of pre-packaged coffee products such as hanging ear coffee and coffee liquid, instant coffee is the first commercial coffee product that Chinese people come into contact with. It is convenient, fast, and low in price. It has a large consumer base in my country and is currently the mainstream. Coffee format.

Traditional instant coffee ingredients are mainly non-dairy creamer, white sugar, coffee powder, etc. Generally, the extracted coffee liquid is concentrated and dried into powder. During the drying process, the aroma has basically disappeared and the taste is poor, but Low prices and early entry into the market are the first coffee products that many consumers come into contact with, the most common one is Nestlé 1+2.

In recent years, with economic development and consumption upgrades, people pay more attention to their health and quality when buying goods. According to McKinsey’s consumer survey data, 72% of urban consumers said they are actively pursuing a healthier lifestyle; 60% of consumers in large cities said they would often check the ingredient list of packaged foods, and would choose to look at them. Healthier products; 55% of respondents said that “healthy and natural ingredients” are their first choice when buying products.

Following this trend, new entrants focus on high-quality and no-added premium instant coffee. The premium instant coffee adopts freeze-drying instant technology, which reduces the loss of aroma during processing. The ingredients are coffee powder, without non-dairy creamer and white sugar.Adding medicine makes it healthier, which is in line with the consumer trend that people pay more attention to health.

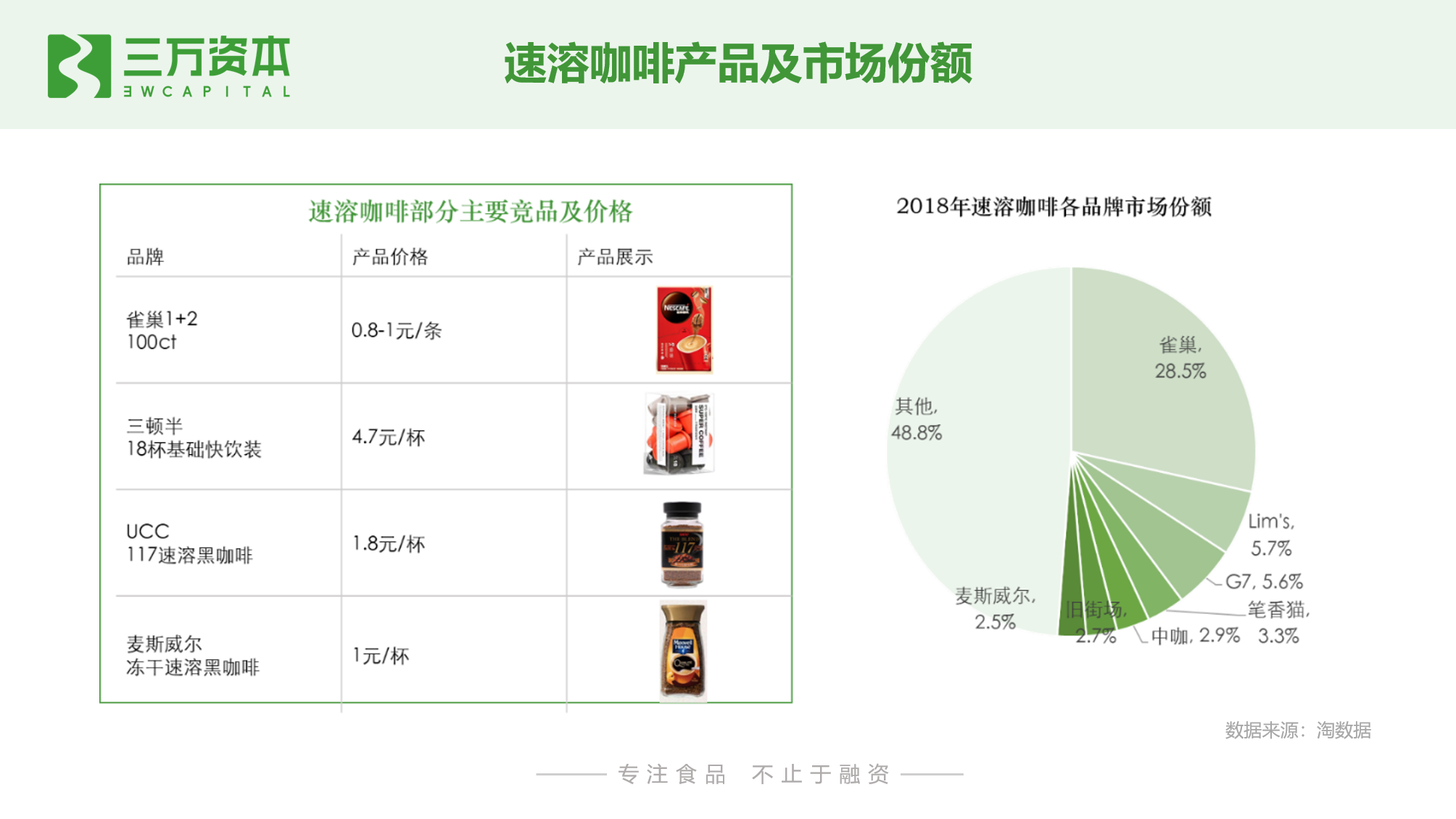

In the instant coffee track, Nestlé is still the leading brand, but its core product line has no transformative innovation, and the brand has aging problems, especially in the minds of the younger generation of consumers. Domestic emerging premium instant coffee brands have a deeper understanding of domestic young consumers and quick response. With the rise of domestic premium instant coffee, it has had an impact on its market, such as the boutique instant coffee established in 2015 for three and a half consecutive years. Tmall double eleven, surpassing Nestle to become the number one coffee category.

Hanging ear coffee has a higher threshold for beginner coffee lovers, mainly for coffee lovers

Hanger Coffee originated in Japan and is a product form that combines freshly ground coffee and retail coffee in cafes. Commodity Bean Hanger Coffee meets consumers’ needs for convenient drinking of standard-flavored freshly ground coffee. Boutique Hanger Coffee meets the needs of niche coffees with unique origins, extending the advantages of offline cafes of producing specialty beans.

Ear-mounted coffee needs to purchase a hand-made pot for use. The threshold is higher for beginner coffee lovers. It is mainly for black coffee lovers. It is convenient without instant coffee, and without the taste and depth of coffee beans. It belongs to a transitional category. , The overall market volume is small.

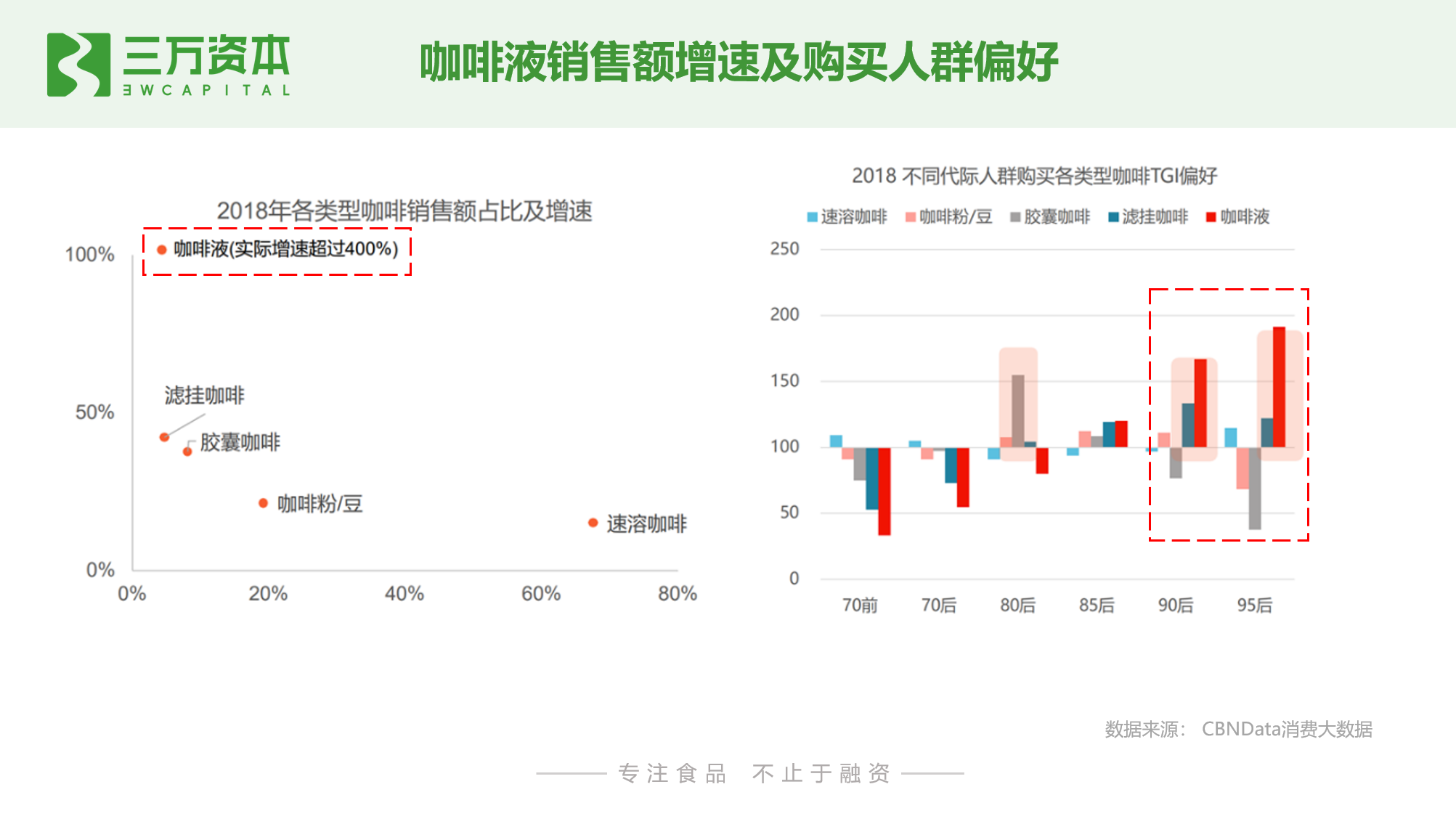

As a new product form of coffee liquid, the younger generation after 90/95 showed obvious preference

Compared to the overall population, the new-fashioned fun clan prefers relatively new categories such as coffee liquid. After 90/95, consumers showed a clear preference for coffee liquid. The coffee liquid category has emerged in new forms such as room temperature coffee liquid/nitrogen coffee liquid, and there is a certain threshold for the construction of a room temperature coffee liquid production line, which requires high capital investment and production line stability.

Currently, the main players of room temperature coffee liquid are Yongpu, Sumidagawa, and Kelin, all of which are made by the same OEM in Japan, with little product differentiation and similar taste. Cold chain coffee liquid can better restore the original flavor of coffee. There are 3-4 domestic manufacturers. However, due to the need for cold chain transportation, the market space is not large at the moment, but the growth rate is relatively fast.

my country’s home coffee culture is weak, home coffee machines and capsule coffee account for a relatively low proportion

The size of China’s coffee machine market is about 1.5-2 billion, with an online growth rate of 27%; among them, fully automatic coffee machines (26.8%) accounted for the highest sales in sub-categories, mainly concentrated in Delong and Philips; capsules Coffee machines accounted for 16.9%, and the top brands were Nespresso and Duoqukusi.

Among different generations of people, post-80s have a significant preference for capsule coffee, with a TGI over 150; post-95s have the lowest preference index for capsule coffee, with a TGI lower than 50 (the TGI index reflects the target group Preference index, a TGI index greater than 100 indicates that the target group has more corresponding tendencies or preferences). Capsule coffee is more troublesome to brew, and it is difficult to meet the convenience of the young consumers born in 1995. As the backbone of the society, most of the people born in the 1980s enter married life and pay more attention to the quality of life. Capsule coffee fits their family use scenes. Judging from the scale of online coffee consumption, capsule coffee has grown rapidly, and sales as a percentage of overall coffee sales have steadily increased.

2, ready-to-drink coffee

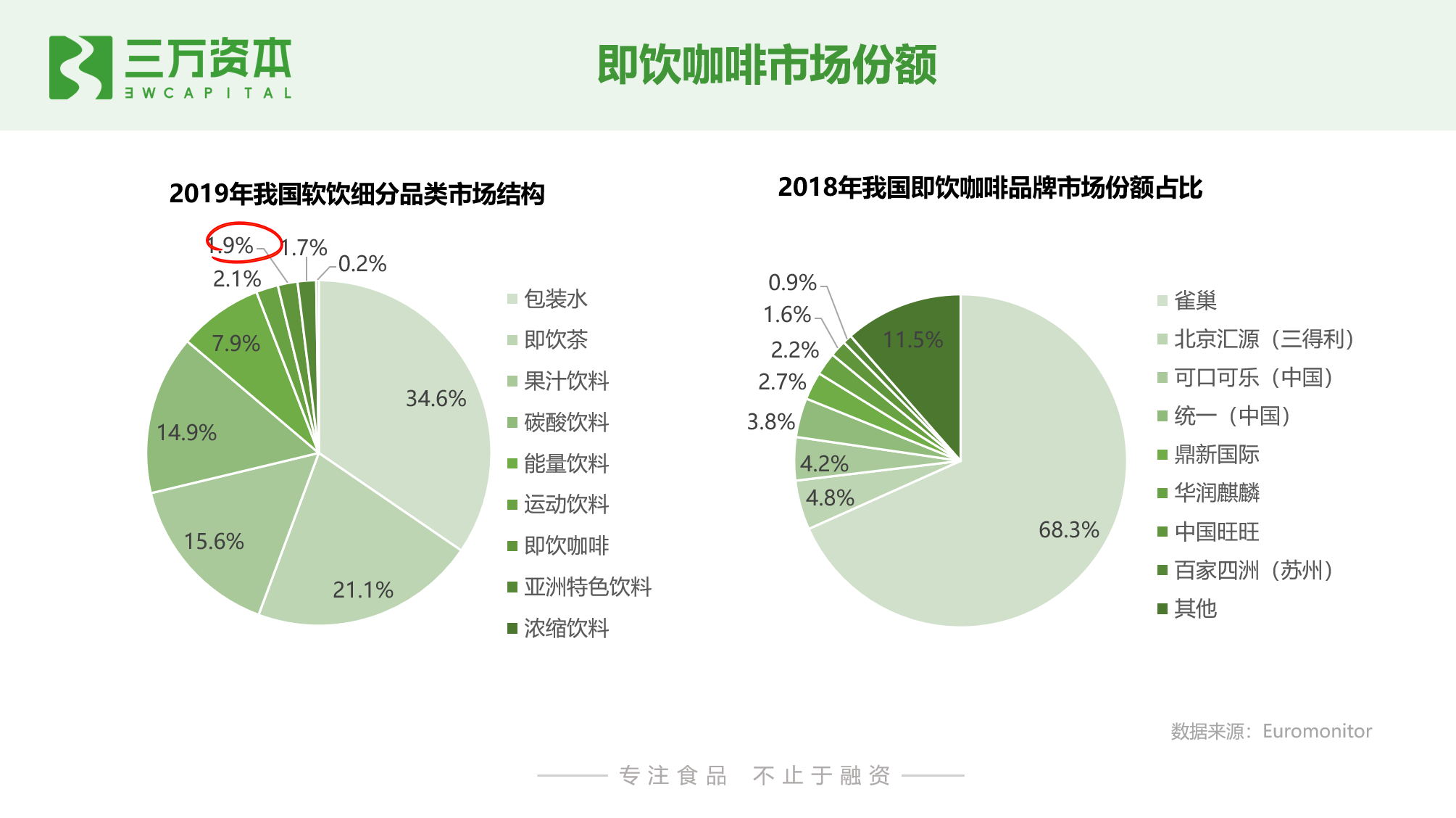

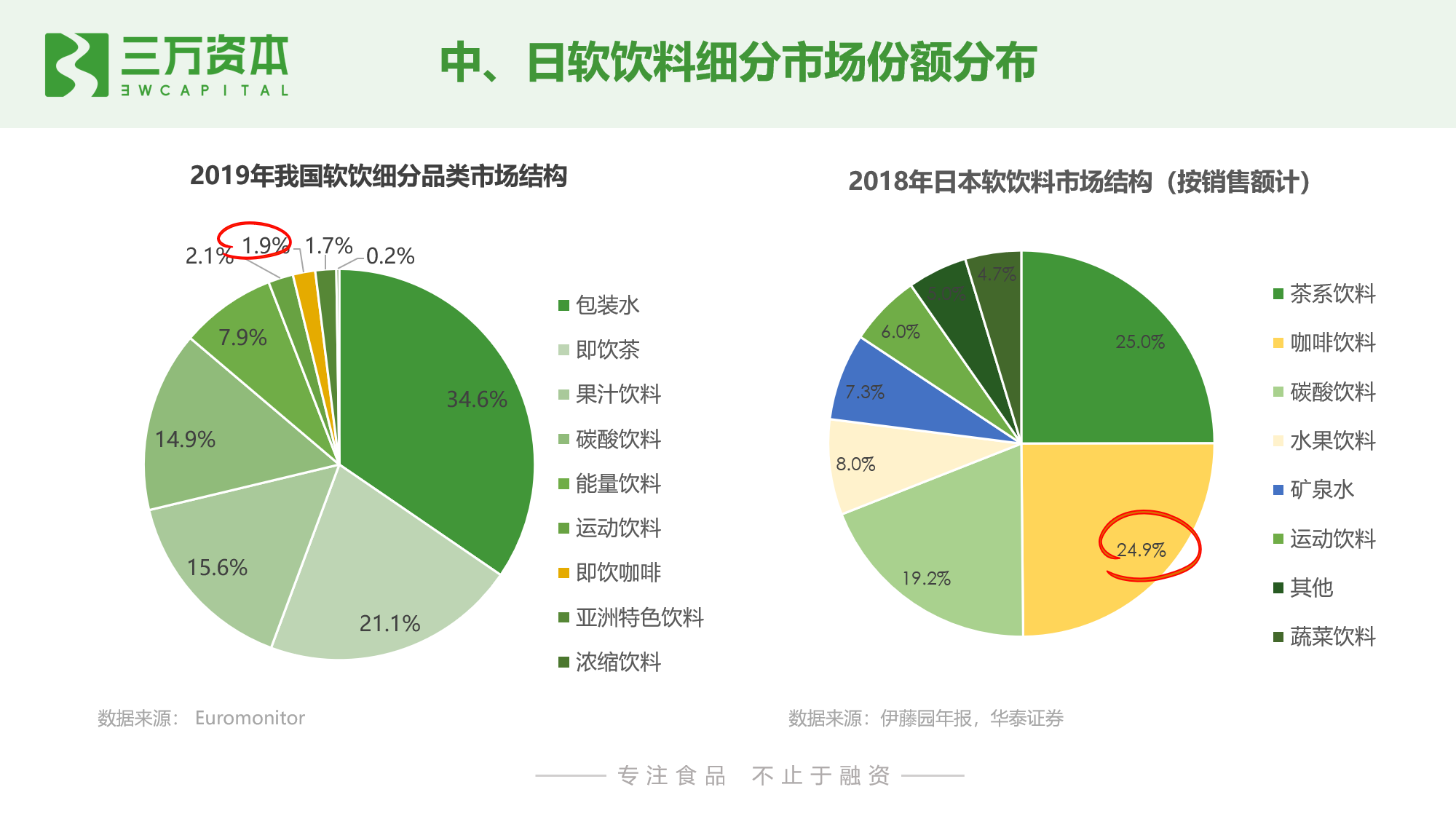

Ready-to-drink coffee eliminates the traditional instant coffee brewing steps, is convenient to drink, and easy to carry and store. Ready-to-drink coffee accounted for about 1.9% of my country’s soft drink market share, and the 2014-2019 CAGR was 14.6%, the highest among all sub-categories (energy drinks 14.3%). The ready-to-drink coffee market is highly concentrated, with Nestlé accounting for 68% of the market share and being the absolute leader.

Traditional beverage giants are major players in the market, and their products are developing towards high-end and high-quality products

Like instant coffee, traditional coffee beverages have many additives, which do not meet consumers’ pursuit of health and quality. With the upgrading of consumption, Xinxing ready-to-drink coffee is developing towards premium ready-to-drink coffee. Most of the premium ready-to-drink coffees use low-temperature coffee extracts, such as Weiquan’s famous selection refrigerated cups, Nestlé’s cold brew coffee series, and Uniform Left Bank refrigerated coffee. The unit price is more than 10 yuan. Improve the quality of coffee through large-scale procurement of fine coffee beans, add high-quality milk sources, and transform from beverages to coffee. Ipsos research shows that 45% of consumers require optimized milk sources and 44% require high-quality coffee beans. In the packaging, coffee is matched with high-end aluminum bottles, from packaging to the inside, both inside and outside.

Currently, most of the traditional beverage giants are laying out this track, and there are few start-up companies. Beverage giants are laying out the ready-to-drink coffee track one after another. For example, Yili launched St. Ruisi coffee beverage, which claims to be added with 100% New Zealand milk; Nongfu Spring and Costa, which was acquired by Coca-Cola, both launched carbonated coffee with unique flavors; Benasson launched a high-end single-origin coffee bean ready-to-drink cold cup. In addition, offline coffee retailers have also launched their own bottled coffees, such as the chain coffee brand Starbucks, the American specialty coffee originator Peet’s, and the specialty coffee chain Blue B.ottle, in order to expand its coffee drinking occasions and frequency, has launched instant coffee products. Ready-to-drink coffee requires brands to have a strong offline dealer management and in-depth distribution system to expand offline sales. In particular, high-quality ready-to-drink coffee has a short shelf life, requires full refrigeration and cold chain transportation, and requires high logistics capabilities. The advantages of traditional beverage giants can reuse the offline distribution system that has been cultivated for many years.

3. Freshly ground coffee

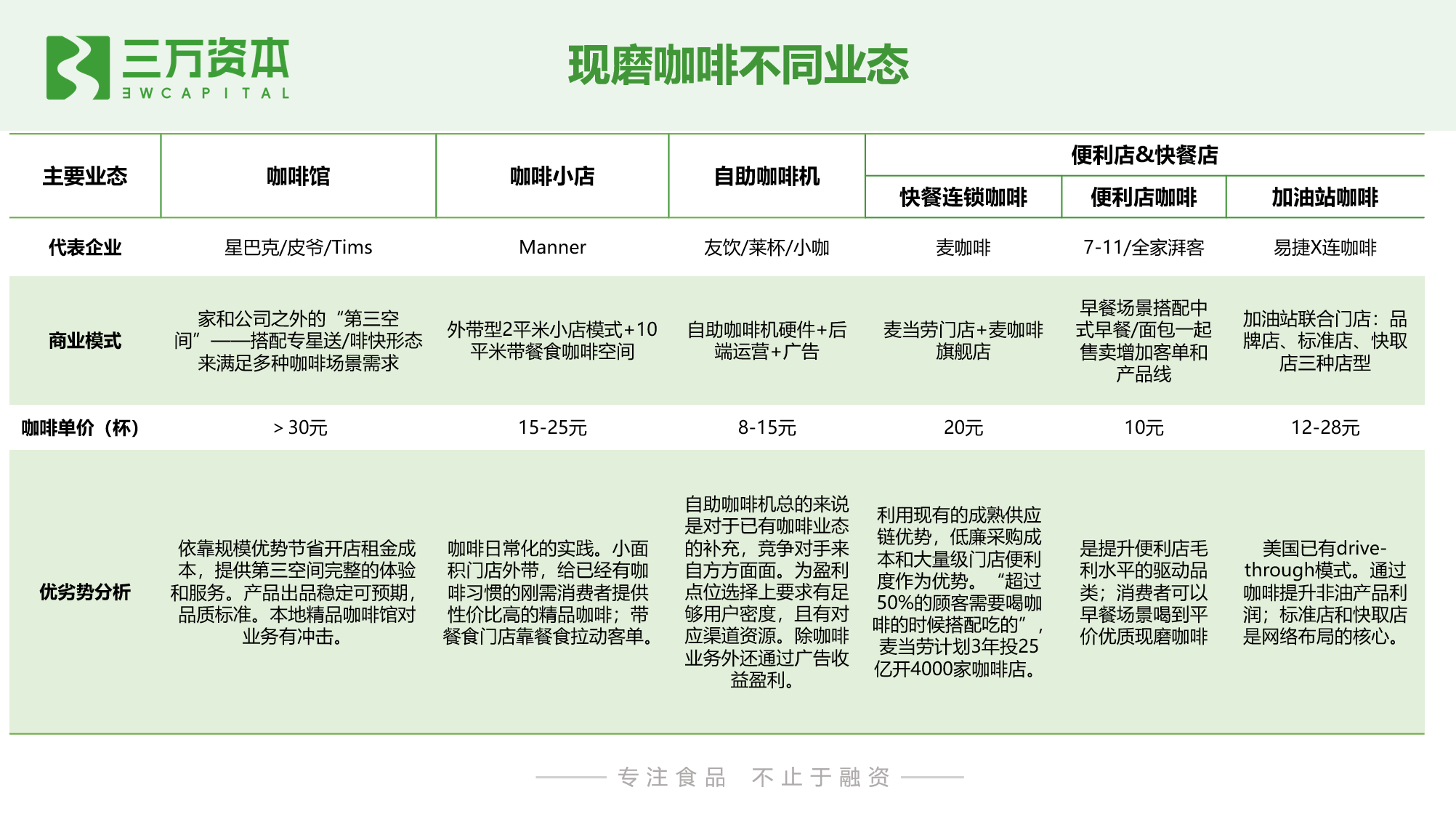

According to different sales channels and store types, freshly ground coffee can be divided into four types of business: coffee shop, coffee shop, convenience store & fast food cafe, and self-service coffee machine.

Cafe: fixed cost support is high, chain giants get rent discounts at brand premiums, and new entrants are more differentiated.

According to Euromonitor’s data, the domestic coffee shop market emerged around 2000, and the number of freshly ground coffee shops in China will be about 50,000 in 2020. Among them, Shanghai has added 1,500 coffee-related companies in the past three years, and the number of coffee shops First in the country. Cafes are mainly freshly ground franchise stores, and the number of coffee + catering stores has been declining year by year.

In addition to functional requirements, cafes meet social needs such as making friends, business negotiations, etc. The location of cafes affects the size of its passenger flow, and the service capabilities and product quality of store personnel affect customers’ buying experience. Although the gross profit of the product is as high as about 70%, the high fixed cost expenditures such as store rent, labor cost, depreciation and amortization, and the commercial nature of the main social space, result in a low turnover rate and no brand premium advantage. It is difficult for ordinary coffee shops to make a profit. Well-known chain coffee shops such as Starbucks have a drainage effect, so they can usually get rent concessions by relying on their brand premiums.

In 2020, a number of international chain brands will enter the market, and they will force domestic offline coffee shops: Tim Hortons has more than 100 stores in China and wonHundreds of millions of dollars have been invested; Peet’s Coffee will open the country’s first black label store in Shanghai in August 2020; %Arabica has successively entered 15 cities including Beijing, Shanghai, Shenzhen, and Chengdu.

Domestic start-up companies mostly take the route of boutique cafes, and through the establishment of brand characteristics, differentiated competition with large-scale coffee chain brands, such as S.Engine Yingji Coffee, founded in 2016, established Seesaw Coffee in 2012. The advantage of boutique cafes is that they can increase their profitability through high customer unit prices, high premiums and consumption of peripheral products. This group of people has high requirements for coffee quality and shop experience, and is not sensitive to price. The customer group is relatively stable, but they consume at the same time. The crowd is also relatively small.

Coffee shops: return to the essence of coffee demand, which is conducive to achieving a balance between product quality, price and profitability

Coffee shops are essentially a kind of coffee shops, and they are the most sought after emerging coffee categories in the capital market, such as Manner and M stand. This type of model does not sell social spaces, there is almost no dine-in service or a few seats, mainly for take-out. This service model is similar to the early tea shops.

Coffee shops focus on providing coffee products themselves. The product quality is high, and the product quality is similar to Starbucks. About half of Starbucks’ customer unit price is usually around 15-20 yuan. Due to the low customer unit price, it can only be increased Sales to increase overall revenue.

Therefore, for small coffee shops, on the one hand, it is important to choose a location with a large number of people in the target customer group. Brands often choose office lobbies or street shops close to office buildings. On the other hand, they have The coffee shop’s cost-effective products attract customers and increase the repurchase rate. The popularization of traffic tools such as takeaway platforms and small programs has also greatly improved the efficiency and human efficiency of a single store, which is conducive to achieving a balance between product quality, price and profitability.

According to the author’s staying point and comparing the serial number, the monthly order of a single store in M Stand Shanghai is around 10,000 orders, and the order volume of Manner is about 30% higher than this. It is a very good single store model in Shanghai. The payback period for a single store is 7-10 months. However, it remains to be verified whether it can replicate such a single-store model and the ceiling of the number of stores outside of Shanghai, the first city of coffee with a deep user base and a large number of high-quality office buildings.

In fact, the originator of the coffee shop is Ruixing Coffee, which was once in the limelight. The author observes that Ruixing Coffee’s business has not been greatly affected by the delisting, and the operating conditions of many stores are even growing steadily. Leaving aside the issue of financial fraud, Luckin’s business model actually provides insight and satisfies the needs of users, and the financial model can also work, that is, it has taken too much steps in the development process. Can Luckin come back against the wind? We will wait and see.

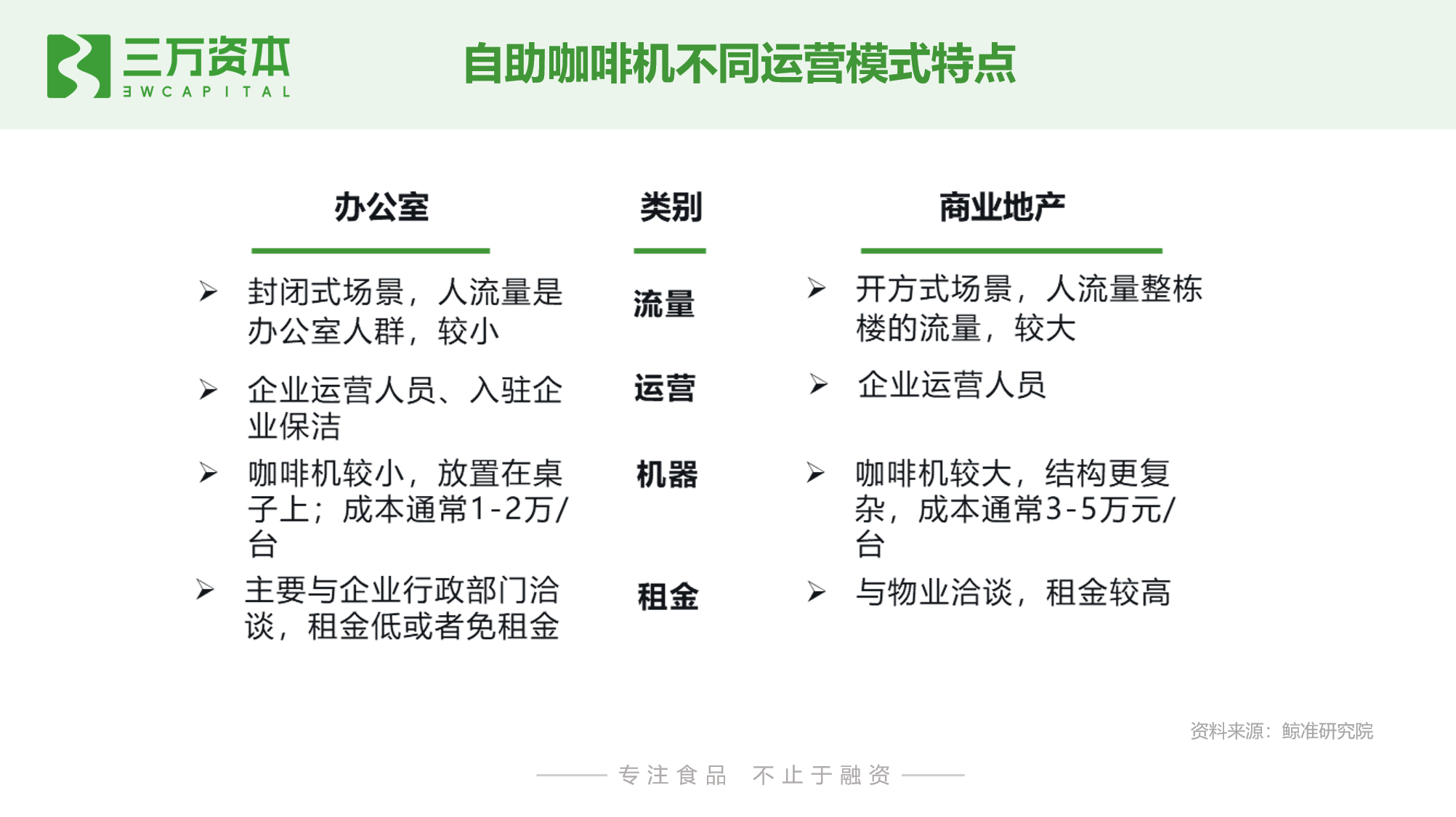

Self-service coffee machines: supplementary retail channels. The emergence of new formats has further narrowed the space for self-service coffee machines

The biggest feature of the self-service coffee machine model is that there are no clerk at the front end and no need to rent a store, thereby saving manpower and rental costs. The product price is lower, usually 8-15 yuan. According to the different placement scenes, it can be divided into two modes: one is for open scenes such as commercial real estate, such as Lai Cup coffee, which most companies focus on; the other is for closed office scenes, such as small coffee. The cost structure of the two different scenarios is also different.

The retail format of self-service vending machines began to appear in coastal cities such as Guangdong in the 1990s, and it has been in my country for 30 years. Now that the self-service vending machine has developed, hardware R&D and manufacturing capabilities have been relatively mature. The main test is the company’s acquisition of high-quality point resources and refined operation capabilities. The number of high-quality points is limited, so enter first Of companies have obvious first-mover advantages. Most domestic self-service coffee machine companies were established around 2015, and their development has been tepid.

In 2018, Coffee Wings acquired Lai Cup Coffee, an operator of self-service coffee machines. Lai Cup Coffee was established in 2015. Before the acquisition, it had obtained three financings from Zhene Fund, Meihua Angel, Xianfeng Evergreen and other institutions. Coffee, as the leading company on this track, was eventually acquired, which also shows that self-service coffee machines are more of a supplementary retail channel, and the future development of this model is limited.

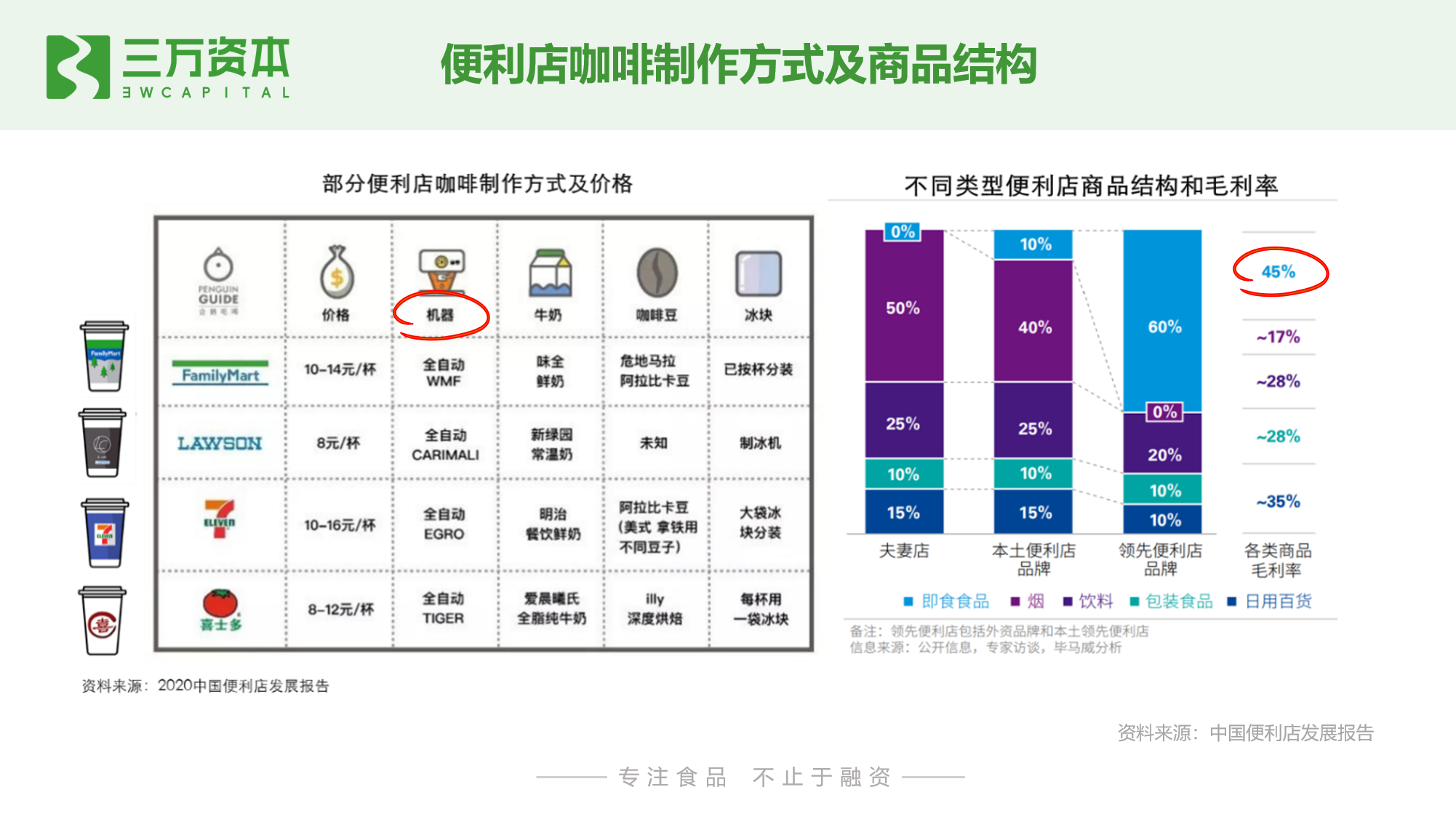

Convenience store & fast food restaurant: cheap and numerous, covering the breakfast scene, the development space needs to be further released

Convenience stores increase coffee business, no additional rent and labor costs are required, only coffee machines and related raw materials are needed. Most coffee machines choose automatic coffee equipment, and employees do not need to master too many coffee brewing skills, and simple training can be used. . From the perspective of the product structure of convenience stores, the gross profit margin of fresh food is much higher than other categories. The introduction of ground coffee in convenience stores will also help them improve store efficiency.

Compared with professional coffee brands with baristas, convenience store coffee is average in terms of taste quality and service experience, but its price of 8-12 yuan per cup is compared to coffee shops (15-25 yuan/cup), coffee shops (>25 yuan/cup) and other formats are also more advantageous.

We mentioned earlier that, compared with tea, people consume more coffee during breakfast, especially fresh coffee. In the future, with the daily consumption of coffee, the penetration rate in the breakfast scene of office workers is expected to further increase. Convenience stores cover the breakfast consumption scene of office workers, and the rich breakfast categories of convenience stores are conducive to driving coffee consumption, and the coffee sales of convenience stores are expected to further increase.

V. Investment and entrepreneurial opportunities in the domestic coffee industry

In the previous article, we analyzed the development status of the coffee industry and various operating models. Next, we will summarize and answer the most critical question in this article: investment and entrepreneurial opportunities in the coffee industry in my country.

1. Does the domestic coffee industry have investment value?

my country’s coffee industry has a large stock market, a fast annual compound growth rate, multiple growth drivers, and many investment and entrepreneurial opportunities.

➀ Calculating the future potential space of the domestic coffee industry

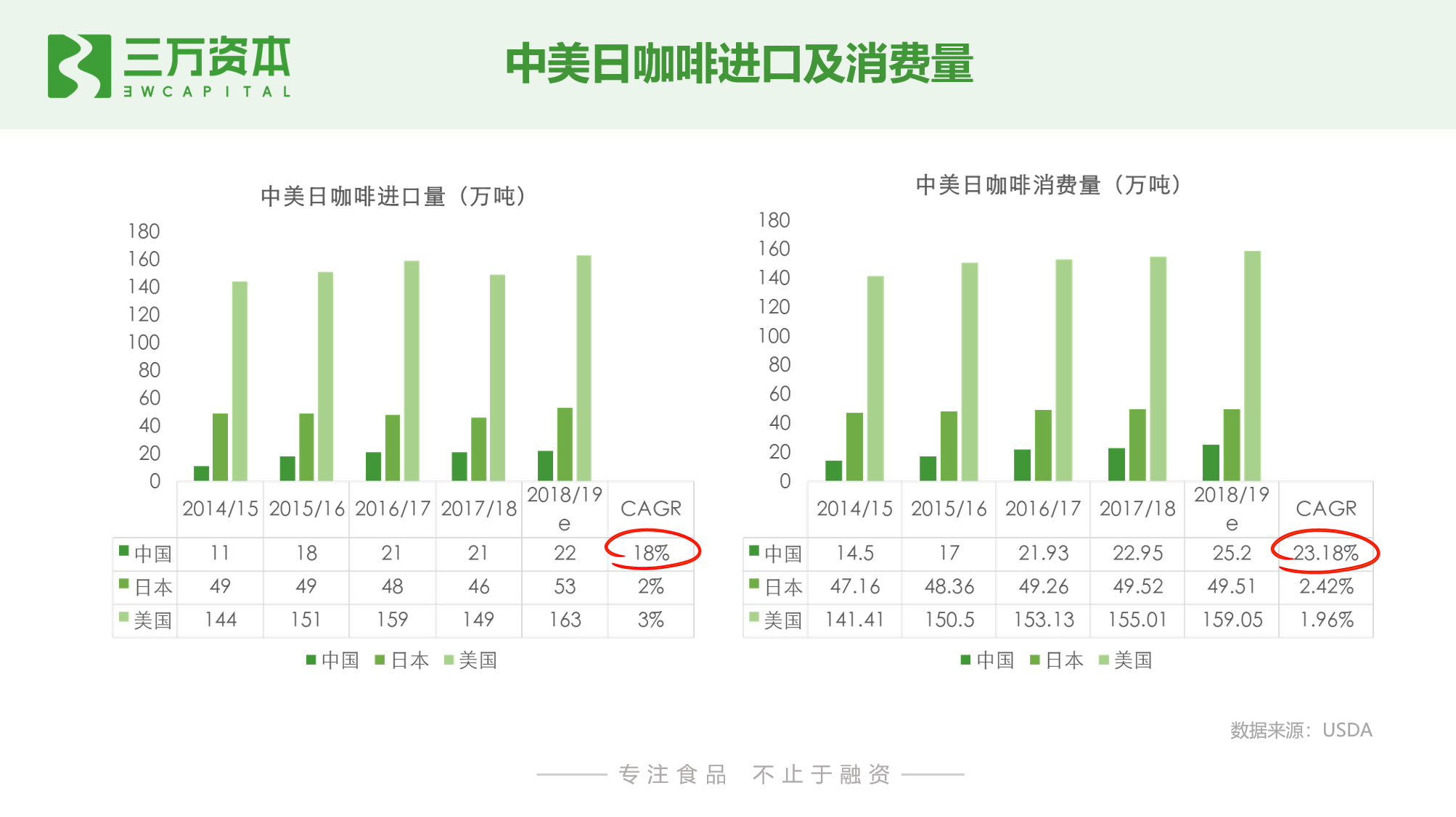

The CAGR of my country’s coffee imports and consumption in the past five years are 18% and 23%, respectively, far exceeding the mature markets of the United States and Japan

Compared with the United States and Japan, my country’s coffee imports and consumption are low, but the growth rate is fast. The compound growth rate in the past five years was 18% and 23%, while the growth rate of mature markets in the United States and Japan was only 2%. about.

The per capita consumption of the domestic coffee industry is much lower than that of Japan, Hong Kong and Taiwan, which are also in Asia, and there is great room for growth

There are many forecast data on the market size of the coffee industry in the market, but there are discrepancies in the data of various institutions. It is biased to refer to the data of one institution. Therefore, we collate the data of different institutions for cross-comparison, although it is difficult to draw A definite data can still draw some common conclusions: the per capita consumption of my country’s coffee industry is much lower than that of Japan, Hong Kong and Taiwan, which are also Asian regions, and there is a large room for growth.

The domestic coffee industry stock market size is about 100 billion, and the potential market space is about 600 billion, with a large incremental space

Dividing my country’s cities into lines according to the level of economic development,The coefficients are calculated for the per capita cups of coffee consumption and the price per cup in different tier-level cities, and then the population is multiplied by the per capita cups of coffee consumption in each tier-level city and then multiplied by the price per cup to calculate the coffee market in my country. The scale range, We take the most conservative value, the potential market space of my country’s coffee industry is 600 billion yuan. Although some articles and institutions predict that my country’s coffee industry will have a trillion-dollar market by 2025, it is too exaggerated, but by measuring regional coffee with similar standard food cultures, it can be concluded that the coffee industry in my country has room for growth. In the industry, there are development opportunities.

➁ Analysis of the long-term growth drivers of the domestic coffee industry

Coffee meets the needs of people to refresh themselves and please themselves, and the addictive characteristics of coffee itself, the product users have a long life cycle

With the fast-paced life of people in modern society, in the face of work pressure, drinking coffee to replenish energy has become a habit of many working professionals. The paper “Taste under Stress” published by the Suntory Institute of Basic Research pointed out that mental fatigue will reduce the sensitivity to bitterness, while physical fatigue will reduce the sensitivity to sourness. According to Kantar Worldpanel, the increasing demand for activation of wake-up (32%) is the main reason for people to consume coffee, while tea drinks that also contain caffeine and have a refreshing function account for only 4%. Among the consumers who plan to reduce coffee spending, only 16.1% of consumers choose to consume new tea instead of coffee, indicating that the new tea has a weaker substitution effect on coffee. The rapid development of my country’s new tea drink market will not squeeze the coffee market in the short term.

From the perspective of product characteristics, the caffeine in coffee is addictive, and users develop consumption habits and are not easy to quit. We can see this from the coffee industry in Japan. In the previous article, we analyzed the current situation of the coffee industry in Japan. The coffee penetration rate of consumers over 60 in Japan is high, and the rapid development of the coffee industry in Japan during the 1960s-1970s coincided with this part of the 60s. As the first generation of consumers who have been exposed to coffee extensively in their youth, the coffee consumption habits developed during their youth have extended to old age, indicating the addictive characteristics of coffee. The churn rate of existing consumers is low, and repurchase High rate, high LTV.

The emergence of a variety of innovative coffee models, and the increase and decrease in residents’ payable incomeThe user’s purchase threshold

In the early days of the industry, coffee was positioned as an imported product and the petty bourgeoisie style of cafes. The unit price of freshly ground coffee was high. Therefore, coffee was often regarded as an elite consumer product in the past, rather than a daily drink. According to Frost&Sullivan data, as of the end of 2017, the average single cup price of freshly ground coffee in China’s top 5 coffee chains was 30 yuan. However, in the industry survey conducted by Frost & Sullivan in January 2019, only 26% of respondents were willing to pay for a cup of freshly ground coffee with a price of more than RMB 30. A survey from the Penguin Think Tank shows that only 13% of users are willing to pay more than RMB 30 per cup of coffee. It can be seen that in the early stages of the development of the coffee market in my country, the contradiction between the high price of freshly ground coffee and the lower willingness of consumers to pay restricted the consumption of coffee by users.

Luckin’s subsidy policy in the early stage of development has attracted many new users to try coffee, which educates market users to a certain extent. Since then, with the development of a variety of innovative models such as coffee shops and coffee takeaways, the unit price of coffee has continued to decrease, lowering the threshold for purchase, and users’ consumption habits have gradually developed. On the other hand, with the development of my country’s economy and the increase in the disposable income of residents, coffee is expected to complete the transition from optional consumption to daily consumption.

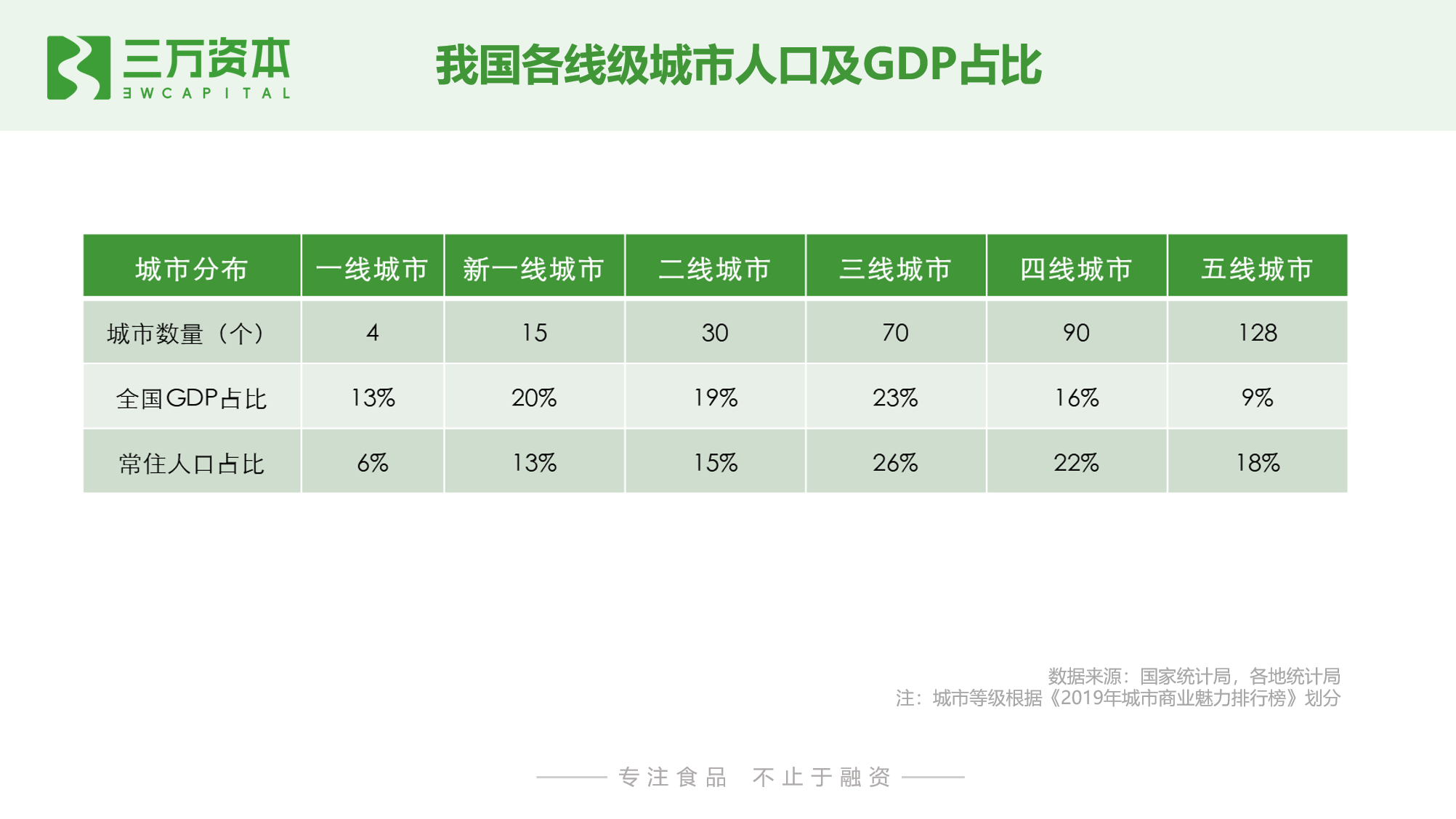

The sinking market has a large consumer base, and with the penetration of coffee consumption culture, there is great potential for development

Although the coffee culture and consumption foundation in low-tier cities is currently weak, with the population flow, young people in first-tier and new-tier cities will bring the lifestyle habits of high-tier cities back to their hometowns and help sink Coffee sales in the market have grown. On the other hand, the maturity of the Internet infrastructure and the popularity of short videos have changed people’s entertainment methods, accelerated the flow of information between different regions, and lowered information barriers. Coffee consumption culture can also be passed through Xiaohongshu, Douyin, and B stations. The video images and texts of other social platforms deliver various consumption information to users in lower-tier cities.

From the perspective of population distribution and income level, the population of my country’s second-tier and lower cities account for 81% of the country’s total population (third-tier cities and lower 64%), and the consumer groups in lower-tier cities are huge. According to data from McKinsey, from 2010 to 2018, the compound annual growth rate of the number of well-off and mass affluent families in first- and second-tier cities was 23%, while that in third- and fourth-tier cities was 38%. The percentage of mass affluent households has almost reached the level of five years ago in first- and second-tier cities, indicating that affluent consumers in third- and fourth-tier cities have increased significantly and their consumption potential is great.

2. We are optimistic about coffee investment and entrepreneurial opportunities

➀ Premium soluble coffee:

High-quality portable coffee meets consumers’ pursuit of product health and quality. The price range of 4-10 yuan also meets the purchasing power of most consumers for coffee, and there are few in-band substitutes at the same price. From the perspective of market competition, since Santon Ban has detonated the market through premium freeze-dried powder coffee, more and more brands have entered this track. Santon Ban is an early pioneer in the market and has a high degree of recognition in the minds of users. , Has a market-leading advantage in the category of premium freeze-dried coffee.

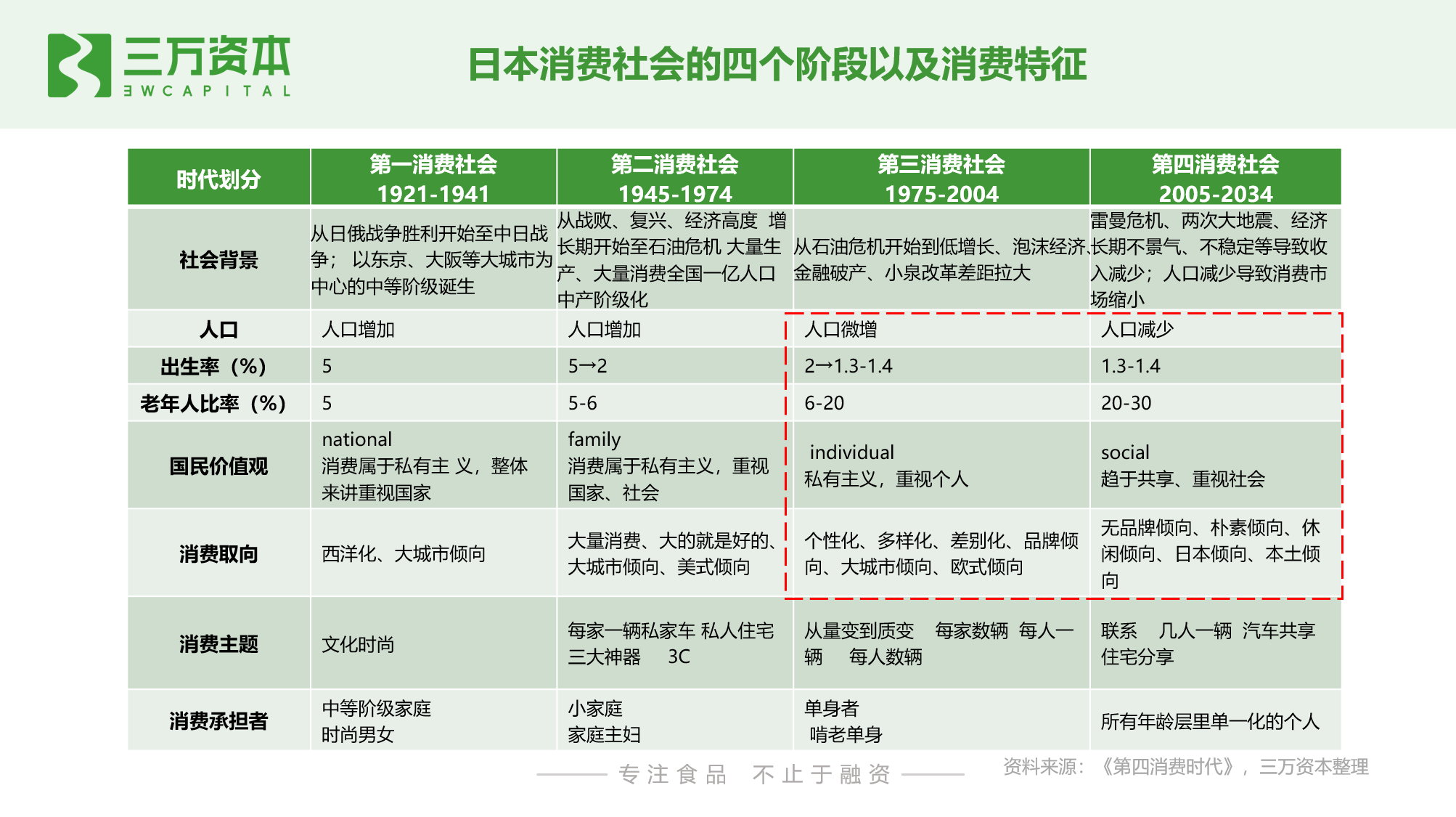

In recent years, my country’s birth rate has been declining, the aging trend has been significant, and the income of residents has continued to increase with economic development. From the perspective of the changes in the consumer society, my country is currently in a transitional period from the third consumer society to the fourth consumer society. On the demand side, user consumption orientation presents the characteristics of individualization, diversification, and differentiation, and user needs are still differentiated. From the perspective of the supply side, freeze-drying technology is not necessarily the ultimate form. The cross-border application of cold extraction technology, the localization of room temperature coffee liquid, and even the entry of medical technology to reduce dimensionality, all have the opportunity to produce revolutionary new products. . There are still great opportunities for the development of premium portable coffee that can meet the demands of different users in the future.

➁ Premium ready-to-drink coffee

Currently, this model is mainly based on the original beverage manufacturers or coffee retail companies. In recent years, major beverage manufacturers have made high-end products in terms of coffee beans, milk sources, production technology and packaging on the original basis. upgrade. At present, few start-up companies have entered this track, and there are no market leaders and hot items with obvious advantages.

From the perspective of global ready-to-drink coffee consumption, according to Euromonitor data, the CAGR of global ready-to-drink coffee is expected to be as high as 7.5% in 2017-2022, which is much higher than the average level of 2.9% for soft drinks, and its growth rate also exceeds that of bottled water. Tops the growth rate of soft drinks. In addition, against Japan, which has similar dietary habits with my country, coffee beverages account for 24.9% of the Japanese soft drink market, which is the second most popular beverage after tea beverages (25%); while coffee beverages are in my country’s soft drinks market. drinkThe market share is only 1.33%, and there is a lot of room for growth.

Premium ready-to-drink coffee is a category with high growth potential that deserves attention. It has the convenience and quality that freshly ground and instant dissolve do not have, and it is in line with people’s pursuit of coffee convenience. At present, there is no market leader occupying the minds of users on this track. In the future, emerging companies that can achieve breakthroughs in product strength, marketing, innovation, etc., have the potential to produce explosive items. Recently, Yuanji Forest has also controlled its investment in the ready-to-drink coffee brand NEVER COFFEE. It is recommended to pay close attention to the track, especially the dynamics of large companies.

➂ Coffee shop

The profitability pain points of traditional cafes are high rent and fixed cost of labor, low turnover rate and low floor efficiency. The coffee shop optimizes the cost structure of traditional cafes by reducing front-end fixed cost expenses, and achieves a balance between product price, customer experience and store profitability, which is a direction for the development of freshly ground coffee in the future.

From the demand side, as my country gradually enters the fourth consumer society, people pay more attention to the essence of products, and there is no brand tendency and localization tendency is obvious. The coffee shop provides freshly ground coffee with high quality and high cost performance, which meets consumers’ demands for high-quality coffee and cost-effectiveness, and conforms to the consumer concept of future users.

Various evolved Ruixing models are coming back out of the world, and more and more thousand-store brands will appear. After user cultivation and infrastructure are further improved, coffee shops have the opportunity to open to a more sinking four-five-six In seventh-tier cities, China’s Wandian coffee brand may even appear.