Where is the direction of the domestic long video platform efforts

The long video industry has developed to this day, and the user dividends have long been eaten, and more and more short videos, mobile games, etc. are competing for user time, the industry development has reached a platform period.

In the second quarter of 2020, the number of members of iQiyi declined for the first time; in the third quarter of 2020, the number of new global members of Netflix was significantly lower than the same period in 2019, only 2 million, and the growth of membership in the entire industry was weak (Supplement: 2020 Due to the outbreak of the epidemic again in Q4, the number of members increased by 8.5 million due to the home isolation of residents in Africa and Europe. However, judging from the changes in the number of members of the long video platform before and after the epidemic in China, the number of members has declined significantly after the epidemic has improved) .

In addition, advertisements, another important source of revenue for long video platforms, have also been eroded by short video platforms a little bit. The superimposed epidemic has led to the continued shrinking of the advertising market. Both pillars of revenue have reached a bottleneck, and there is no room for imagination for the development of the industry.

Isn’t the long video platform a good business?

Long video platform has not been a good business, high copyright costs & high content production costs, content-based content makes it difficult to form a monopoly, other applications compete for user time (the threshold for long video viewing is relatively high), and the means of monetization is single And so on, are the inherent weaknesses of the long video platform. Next, we analyze separately from the three aspects of cost, revenue, and competitive environment.

Cost

The content of the long video platform comes from copyright purchases and self-made content, and the bulk of the cost is also in these two.

In terms of copyright procurement, the cost of copyright has soared. In 2005, the exclusive copyright price of domestic film and television dramas was only a “cabbage price”. By 2007, the price per episode was around 3,000 to 5,000 yuan, and in 2009, It has soared to as high as 100,000 yuan per episode, and the copyright price has set records in succession since 2010. This phenomenon reached its peak in 2018. The copyright fee for the episode of Ruyi’s Royal Love in the Palace was 14.5 million yuan. However, as policy-based salary restrictions and video platforms increase investment in self-made content, the cost of copyright procurement has declined, and the procurement cost of leading copyright dramas has fallen from over 15 million per episode to less than 8 million. Even so, the cost of copyright is still very high, and continuous payment is required.

The other part is the investment in self-made content. Due to the high cost of copyright purchase, major platforms are focusing on self-made content, which is also an important part of building core competitiveness. As of December 31, 2018, iQiyi’s copyright content assets increased by 45.7% compared to 2017, and its self-produced content assets increased by 139% compared to 2017. Among them, in 2018, iQiyi’s self-made content assets reached 3.736 billion yuan, accounting for 32.4% of content assets, compared with 22.5% in 2017. The growth of self-made content assets accounted for a significant proportion of total content assets.Promote. With the policy-based salary limit order (the total remuneration of all actors and guests for each movie, TV series, and online audio-visual program shall not exceed 40% of the total production cost, the remuneration of the main actors shall not exceed 70% of the total remuneration. The maximum remuneration limit system. Single. The release of the actors’ single-episode remuneration (including tax) shall not exceed 1 million yuan, and the total film remuneration (including tax) shall not exceed 50 million yuan), which reduces the shooting cost a lot.

In general, the cost of copyright purchase and self-made content has decreased in the past two years, but it is still the heaviest burden on the long video platform. To maintain the existing volume, the long video platform has to continue to place bets.

Income

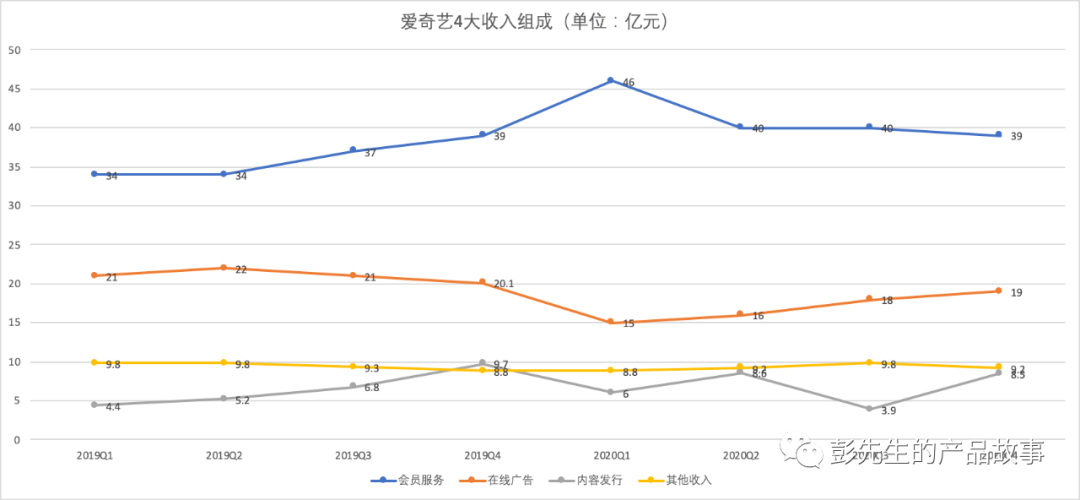

Taking iQiyi as an example, iQiyi’s financial report divides its revenue into four parts: membership services, online advertising, content distribution, and other income. Let’s take a look at the performance of these 4 parts of iQiyi’s revenue in the past 8 quarters. The growth rate of revenue core membership services has entered a plateau after years of rapid growth. It peaked in Q1 in 2020 and then turned down. Some of them It is the impact of the epidemic, but from another perspective, the epidemic should constitute a certain positive for online video. Online advertising has fallen sharply due to the cannibalization of short video platforms and the shrinking of the advertising market caused by the epidemic. It has rebounded in the second three quarters of 2020, but it has not yet returned to the average level in 2019. The growth rate of the content distribution business, which was once high hopes, is not very bright. Before the number of paid members has found a new growth point, it is difficult to see the possibility of continued growth in the revenue of the long video platform.

Source: iqiyi financial report

Competitive environment

Intra-industry competition

The competitors of the long video platform include other long video platforms, as well as long video playback media such as TV and movies. Everyone is fighting for the limited viewing time of users. We won’t repeat the competition between long video platforms. Aiyouteng has been fighting for many years, followed by Mango TV, Watermelon and Station B are eyeing each other, and related articles are too numerous to list. Let’s take a look at the situation of movies and TV. Statistics show that from 2013 to 2018, the number of urban moviegoers has steadily increased, nearly three times higher. The box office of domestic movies has also increased from 21.7 billion to 64.2 billion. Although affected by the epidemic, the total box office in 2020 is only 20.4 billion, but from February 11, 2021, New Year’s Eve to the sixth day of the first day of the first month, the national movie box office reached 78.22. Billion yuan, following 59.0 in 2019After 500 million yuan, it once again broke the national movie box office record for the Spring Festival file. At the same time, it created a number of world records such as the global single-market single-day box office and the global single-market weekend box office. The demand for viewing movies suppressed by the epidemic is gradually being controlled with the epidemic Start to reverse.

The number of TV viewers continues to decline every year, and there is still no sign of a reversal. But from another perspective, Hunan Satellite TV, Hunan Satellite TV and other TV stations that continue to produce high-quality videos still maintain a large fan base and high ratings. It can be seen that content production capacity is a key factor that determines whether TV stations and long-term video platforms can continue to be brilliant.

Source: Meiland Consulting

The relationship between the long video platform and the star studios, content production and distribution companies in the upstream of the industry are also in love and killing each other. Everyone wants to share more benefits on this pie.

Beginning in 2018, the three major video websites of iQiyi, Youku, and Tencent Video, which have always been in the same situation, have jointly issued the “Joint Statement on Suppressing Unreasonable Remunerations and Resisting Unhealthy Trends in the Industry” and “Regarding the Regulation of Film and Television Order “The Initiative to Purify the Industry Ethos”, unanimously resisted the star’s “high-priced film remuneration”. Behind the boycott of sky-high film remuneration, it is actually indirectly cooling down the sky-high copyright fees for years and alleviating the copyright anxiety of video websites. It is not easy to cut people and money, but in the face of profit, everyone can’t help but put down the superficial politeness, and the bayonet is popular.

On March 17, 2021, the TV series “If you are well, it will be sunny” starring Zhang Han and Xu Lu will be broadcast on Dragon TV. Normally, the copyright owner will authorize one or more parent video platforms to play it. But this drama is an exception. According to the producer Yang Li, due to the fact that Ai Yu Teng joined forces to lower the price, the show had no choice but to give up playing on the mainstream long video platform and chose to build an APP for paid on-demand broadcasting. With the gradual deepening of the downturn in the entire industry, this problem may intensify thereafter.

Out-of-industry competition

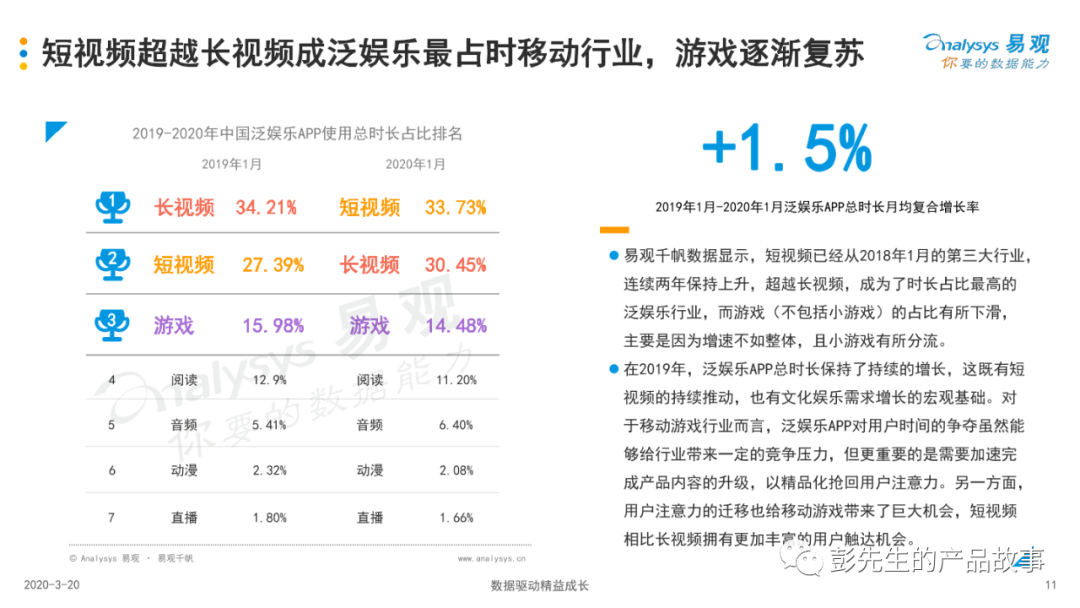

In addition to competition within the industry, competition from other industries such as short videos, games, outdoor entertainment, etc. has also become fiercer. Short videos and games have taken away a lot of user time. The data shows that the penetration rate of short videos continues to increase.

As of December 2020, the number of short video users is 873 million, accounting for more than 80% of all Internet users. The average daily usage time of short video users is 110 minutes, which greatly invades the user’s time to watch long videos. According to Analysys data, from 2019 to 2020, the proportion of short video applications has increased from 27.39% to 33.73%, while the proportion of long video applications has dropped from 34.21% to 30.45%, which is currently short. The erosion of long videos by video has not stopped.

Data source: Analysys

The cost is high and there is no effective means to reduce it, the growth of paid memberships has fallen into a bottleneck leading to the stagnation of income growth, and the competitive environment of internal and external troubles, the long video platform is really not a good business.

Look at the industry prospects from the development of industry leader Netflix

On January 19, 2021, Netflix released its 2020 financial report. In 2020, Netflix’s revenue was 24.996 billion U.S. dollars, compared with 20.156 billion U.S. dollars in the same period last year, a year-on-year increase of 24%; net profit was 2.761 billion U.S. dollars. In the same period of the year, it was 1.867 billion US dollars, a year-on-year increase of 47.9%; diluted earnings per share was 6.08 US dollars, compared with 4.13 US dollars in the same period last year.

In terms of the number of paying users, in the fourth quarter of 2020, the total number of paying users of Netflix’s global streaming media service reached 203.6 million, a year-on-year increase of 21.9%. It was 16709 million in the same period last year, and it also exceeded market expectations of 201.2 million. The net increase in paying subscribers of streaming media services was 8.51 million, far exceeding analysts’ previous average expectations (6.03 million), compared with 8.76 million in the same period last year.

Behind Netflix’s outstanding performance, it is largely due to the spread of the epidemic around the world. Residents in a large number of areas are isolated at home, so the number of paying members has soared.

Source: Netflix earnings report

Of course, while Netflix is benefiting, other long video platforms are also catching up with the east wind. In Q3 2020, Netflix only added 2.2 million new users, while Disney’s Disney+ net added 13.2 million paying users during the quarter, which exceeded market expectations, with the total number of paying users reaching 73 million. On March 10, 2021, Disney CEO Bob Chapek revealed in an interview recently that the number of global subscribers for Disney + has exceeded 100 million. After only more than a year on the line, Disney+ has achieved the results that Netflix took 10 years to achieve. This has a certain relationship with the epidemic, and the bigger reason lies in Disney’s deep accumulation of content. At the same time, the number of subscriptions for Disney’s Hulu (including Live TV) and ESPN+ are currently 39.4 million and 12.1 million, respectively, and the total number of subscriptions for the three has reached 146 million.

HBO, another parent video platform, also delivered brilliant data in 2020. As of the fourth quarter of 2020, the total subscribers of HBO and HBO Max in the United States reached 41.5 million, an increase of 20% from the previous year. HBO Max users reached 37.7 million, of which 30 million users obtained streaming media services through suppliers, and 6.8 million directly purchased HBO Max services. HBO relies on the powerful content creation capabilities of HBO, Warner Bros., DC, and CNN.

How Netflix will continue to maintain growth in the post-epidemic period when the epidemic has gradually subsided is an urgent question before Netflix. It is obvious that the domestic long-term video platform is gradually showing a decline after the epidemic is well controlled, and it may be difficult for Netflix to surprise us.

Where is the direction of the domestic long-term video platform efforts

Based on the above analysis, we can conclude that long-term video platforms, TV stations, etc. ultimately compete for content quality. Whose has more high-quality content is more likely to get users. The creation of long video content is a process in which art is greater than rationality. It is difficult to use formulas to fix production in this process. The final competition is the number and quality of creators, IPs, and artists. How much benefit the company can share in the entire chain of long video IP accumulation, creation, and distribution, as well as the company’s cost control methods, and whether the company can gain more share in the global market determines how far the long video platform can go in the future Core factor.

From the experience of the TV station era, we may be able to get a glimpse of the future of the long video platform. TV stations such as Hunan Satellite TV, Zhejiang Satellite TV, and Beijing Satellite TV with strong creative capabilities continue to maintain vitality and growth, and they have also maintained their strength in the online video era. Competitiveness. At the end of the competition for long video platforms, it may be a similar pattern, except that the number of long video platforms will not be so large. After all, platforms with a small number of users will not continue to live with the support of local and national finances. In this competitive landscape, content costs are always painful, and death is always with you.

AlthoughThe long video platform is not a good business, but if you want to go to the end in the industry, these are two directions you can work hard on.

Industry Integration

A super entertainment complex that integrates IP creation, artist training, content production and distribution, and the entire content production chain layout, which can get the most benefits of the industry under controllable costs. Tencent’s new cultural and creative strategy is this idea. Reading Group and Tencent Animation export IP, Tencent Pictures and Penguin Pictures produce content, Tencent Animation and Tencent Video are responsible for content distribution, and Tencent Games is responsible for the gamification of IP. Create a super entertainment complex by integrating internal resources and teams.

Internationalization

Through acquisitions or cooperation with local companies, or cultural export, more shares in the global market, especially in developing countries such as Southeast Asia, Africa, and South America, are easier to enter and occupy due to their low level of development The market is a battleground. On this road, Netflix has taken the lead. Take the Southeast Asian market as an example. Netflix has occupied 29.4% of the market share, far ahead of the second-ranked iflix (Malaysian long video platform, which has been acquired by Tencent), and Tencent’s WeTV , As the most successful long video platform in China, it only accounts for 2.1% of the market share in Southeast Asia, which is a huge gap with the leader.

Of course, the above two methods require strong financial support and a mature content production industry. At this level, the United States has a first-mover advantage. This is one of the reasons why Netflix can become the world’s largest long video platform. Domestic content production talents and industry-related supporting facilities are very scarce. Films, TV series and other shooting methods and tools, and post-production team technology are many years behind foreign countries.

However, because the current operation of the industry is relatively traditional, there is a lot of room for integration and transformation, and there is also a lot of room for cost optimization. This is an opportunity for the long video platform, and it is also a challenge that the long video platform must face. Although I have left this industry, I still hope that the industry will get better and better. Chinese films, TV series, and variety shows can truly lead the era and be exported to the world. After all, this also means that I can see more outstanding Works, for a movie lover, this is really a very beautiful thing.