The iron cabinets on the street are ill-fated.

Editor’s note: This article is from the public micro-channel number of the “new economy boiling point” (ID: xinjingjifeidian), Author: boiling point.

Two pieces of data have recently attracted my attention. One is from the Securities Daily. As of April 3, 431 bank outlets have ceased operations.

Another one comes from the Central Bank. The “Overall Situation of Payment System Operation in 2020” shows that as of the end of 2020, the number of ATM machines was 1.0139 million, a decrease of 83,900 from the end of 2019, and the number of ATMs per 10,000 people nationwide was 7.24 Taiwan, a year-on-year decrease of 7.95%.

A sharp contrast is the growth of non-cash payment services. In 2020, banks across the country handled 354.721 billion non-cash payment services with an amount of 4013.01 trillion yuan, an increase of 7.16% and 6.18% respectively year-on-year.

The “increasing line” of banking service data and the “downsizing” of offline services reflect the arrival of a cashless society from one side. Behind this, whether it is the popularization of third-party payment, or the era of digital currency that can be expected in the future, it is a general trend that banknotes fade out of most transaction scenarios.

1 Always “non-mainstream”

Even John Barron, the inventor of the ATM machine, predicted today’s situation in an interview with the BBC in 2007: “Traditional money transportation also requires money costs, so I predict that in the next three to five years , The era when humans say goodbye to cash is coming.”

I think Barron invented the ATM machine to realize his wish of “withdrawing banknotes anytime, anywhere”. This 25-year-old young man who joined the Delaru banknote printing company, because of his work, would go to the bank to line up every week, so he started Thinking about how to solve the pain of queuing in banks.

At that time, a self-service chocolate vending machine was popular on the streets of the United Kingdom. After inserting a coin, you could “spit out” the goods with a “ding” sound. Inspired by this, Barron quickly manufactured the first ATM machine, and after persuading Barclays Bank, it was able to install it at the service point of Barclays Bank in London on June 27, 1967.

At that time, the bank card had not yet been invented. The machine hung on the wall of the bank could only ask for withdrawal from the machine with an instruction card printed with a concave and convex mark, and one instruction card could only take 10 pounds, in real life, there are all kinds of withdrawal needs, the function of this machine is too single.

This “invention”, in order to support the machine reading function, put a slight radioactive element “carbon 14” on the instruction board. After the public knew it, it caused a panic when it was used. Barron had to explain later, “The user only eats the carbon element on the 130,000 instruction cards at a time, which may cause damage to health.”

However, this explanation is still of no avail. This “iron box on the street” was still left out in the cold when it was first invented.

Two years later, there is an alternative to “instruction card + ATM machine”. September 2, 1969, Hanhua Bank of the United States launched an ATM machine for magnetic stripe cards. This bank had long foreseen the prospect of ATM machines. As soon as it was launched, it advertised loudly: “I It will never close after it opens at 9 a.m. on September 2nd!”

The embarrassing thing is that this improvement, the technology has not been able to keep up: every time a user uses a magnetic stripe card to withdraw money, he will swallow the card once, and only a few days later can he go to the bank to get it back.

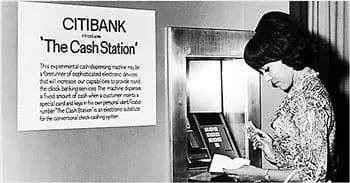

The banking industry did not completely abandon this invention until the Citibank of the United States carried it forward. When Worstone joined Citigroup, he wanted to lead this bank to a turnaround. He focused his energy on this ATM machine that can realize human-computer interaction. This bank spent a huge sum of 160 million US dollars to realize the ATM machine. Cover the entire New York City.

In 1978, an abnormal winter monsoon blizzard swept New York, causing an average snow depth of 40 centimeters throughout the city. Traffic was messed up, and shops closed. Banking services were also paralyzed due to freezing, but there was a long line in front of Citibank’s ATM machines. Citibank seized the marketing opportunity to advertise: Citibank never sleeps.

After the snowstorm, Citibank’s ATM utilization rate increased by 20%, and in just a few years, the bank’s deposit holdings in New York doubled. Due to its early layout, Citibank later monopolized the ATM market in the United States, which was resisted by its peers.

In 1985, six U.S. banks headed by Hanhua Bank joined forces to do one thing: they established the “New York Cash Exchange Network”, which is essentially an “alliance.” , Provides ATM machines with cross-bank deposits and withdrawals within a small range.

The ATM machine after the joint bank facilitated users, forcing Citibank to join the network later, which brought substantial changes to the networked services of ATM machines and formed a service model close to today.

It took 18 years for this small machine to form a mature network from being invented to being used by the industry!

2 Accelerated elimination

It was not until 1987 that China had the first ATM machine. It was introduced by Bank of China Zhuhai Branch. In the future, this method gradually evolved into the “standard configuration” of bank counter services. In addition, Developed “off-site” services deployed in public places such as shopping malls, hotels, airports, and railway stations.

The self-service channel model of ATM machines developed in my country and became the world’s largest ATM market in 2014. According to data from the central bank, at the end of 2015, the number of ATMs in my country was about 860,000; self-service equipment service density increased In 2011, it exceeded the world average. In 2015, my country had 764 ATM devices per million people.

A bank employee recalled from the boiling point of the new economy that during the 2008 Beijing Olympics, domestic ATM business was carried out relatively smoothly. Foreigners who came to China were accustomed to using ATM machines, and Chinese people accepted it after long-term training. ATM machine.

The prosperity of ATM machines in my country’s banking industry is also related to the way banks “transfer traffic”. The above-mentioned bank personnel revealed, “Every financial business serviced by the bank counter staff has a commission, which is reflected in performance. The commission for processing cash deposits and withdrawals is the least. For other financial services, such as wealth management products, the commission is very high. High.”

The work index that guides users to use ATM machines is called “transfer rate” and “automatic equipment utilization”. “If the number of people using ATM machines is not enough, it will also affectPerformance appraisal of bank service outlets. “

At this stage, due to banks’ emphasis on ATM machines, it has also led to the short-term rise of a number of ATM machine manufacturers. For example, Guangdian Express, the first listed ATM company in China, had its net profit soared from 90.14 million yuan to 332 million yuan in less than three years after its IPO on the Shenzhen Stock Exchange in 2007.

But by 2016, the growth rate of ATM in my country has reached a plateau. According to data from the central bank, as of the end of 2016, the total number of ATMs deployed nationwide was 924,200, an increase of 57,500 over the previous year, a growth rate of 6.63%. Compared with the annual growth rate of approximately 25% in 2012 and 2013, this data releases Slow down a lot.

If you look back in 2016 and look at 1967, the starting point of the birth of the first ATM machine, by 1985, when it was commercially mature, it took only 31 years for this invention to truly take center stage and achieve its glory.

In terms of external factors, in 2016, my country’s mobile payment has started and developed rapidly. The “China Payment and Clearing Industry Operation Report (2017)” released by the China Payment and Clearing Association shows that in 2016, a total of 125.111 billion non-cash payment services were processed nationwide, with an amount of 3,687.24 trillion yuan, a year-on-year increase of 32.64% and 6.91% respectively. . From a global comparable perspective, in 2015, the number of non-cash payments in my country accounted for 22.12% of the global number of non-cash payments, and the growth rate was more than 4 times the global average.

From the inside of the banking industry, the greatest service significance of ATM machines is greater than profitability.

As mentioned above, in addition to the supplement of bank counters, the layout of ATM machines is also widely used in shopping malls, airports, subways, hotels and other places. The latter’s “off-line” service, in addition to paying more than 100,000 yuan per unit In addition to the cost of equipment, the bank also pays “outlet rental fees” and daily operating expenses (including communication fees, electricity fees, installation and decoration fees, etc.). In addition, the delivery and maintenance of banknotes are also performed manually.

Take Xidan, a popular business district in Beijing, as an example. Around 2018, the annual rental fee paid by the bank to the mall was more than 10,000 yuan for a machine, and the annual fee for ordinary venues was several thousand yuan.

According to the calculations of the International ATM Industry Alliance, the break-even point of ATM machine operation is that every machine every 24 hours, an effective withdrawal occurs at least every 8 minutes on average, and more than 180 withdrawal transactions per day can be achieved. Guaranteed.

The above-mentioned bank staff who received consultation on the boiling point of the new economy revealed that the off-bank ATM machine has also reached the time point for renewal in recent years. In addition to the retention of areas with a relatively large passenger flow, there are also internal regulations in the bank. To ten years of service life,All plans to withdraw.

“Because the machine was originally installed, it was considered to provide card users with more convenient financial services, but now mobile payment has been highly developed, and people use ATM machines less and less frequently.”

“Previously, ATM machines were installed to solve the needs of customers who have no cash and cannot swipe their cards. They are mainly used for cash transaction services. Nowadays, with technological innovation, users can also complete transfers and micropayments without swiping their cards. Mobile banking APP can do it, you can scan the code to pay.” The above-mentioned person said.

ATM machines are declining, but they will not disappear immediately in the stage of history. First of all, in bank counter services, this kind of human-computer interaction is easy to liberate manpower, so it has also become a bank service outlet The standard configuration, but more intelligent and agile equipment is also accelerating the improvement of banking services, which also provides a direction for the transformation of ATM machine manufacturers.

“The future development direction of ATM machines is to provide solutions for unmanned banks. It has a relatively high technical threshold because it integrates a series of new technologies including artificial intelligence, voice recognition, face recognition, etc.”, Haitong Securities Computer Industry chief analyst Zheng Hongda believes.

Secondly, some users who are accustomed to ATM services still have needs. Although today, this group is shrinking day by day, however, just like the Ministry of Industry and Information Technology recently asked APP to make changes to adapt to the ageing, while companies are making full commercial profits, their social responsibilities are also reflected in the coverage of services for disadvantaged and marginalized people.

Zeng Gang, director of the Banking Research Office of the Institute of Finance of the Chinese Academy of Social Sciences, said in an interview with the media, “ATM changes are not isolated, because the use of cash is declining, and the physical branches of banks are also shrinking, even The banknote printing company may also have a decline in business.”

Speaking of which, by the way, let’s talk about the Delaru banknote printing company where Mr. Barron, the inventor of ATM, worked. This banknote printing company was founded in 1813 and later became the world’s largest banknote printing company. In early December 2019, the BBC reported that it was “on the verge of bankruptcy”, and the main reason was the impact of electronic payments.

Because in real life, the circulation of banknotes has been increasingly replaced by digital methods, and an era has ended in a hurry.